June 28, 2026

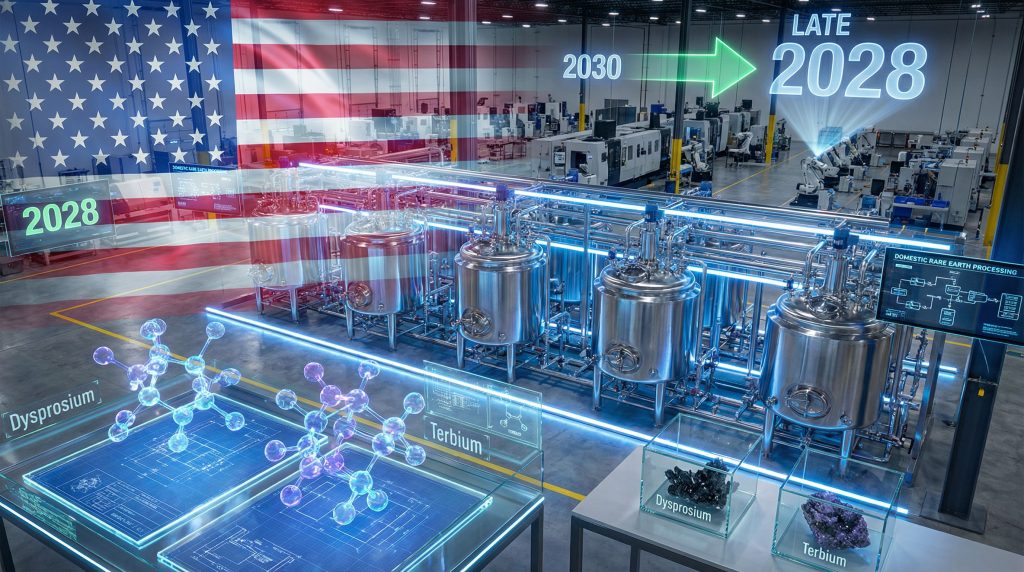

USA Rare Earth Round Top production acceleration represents a pivotal development in establishing domestic supply chain security for critical materials. The company's announcement to advance commercial production by two years, targeting late 2028, positions this project at the forefront of U.S. efforts to reduce dependence on foreign sources for essential rare earth elements. This accelerated timeline, however, introduces significant technical and financial challenges that require careful evaluation of feasibility and execution risks.

Strategic Fundamentals: The Critical Materials Imperative

Global supply chains for critical materials operate within frameworks of concentrated production and processing capacity, creating systemic vulnerabilities during periods of geopolitical tension. Heavy rare earth elements present particularly acute challenges, as their extraction and refinement require specialized technical capabilities currently dominated by single-nation producers.

The strategic importance of elements like dysprosium and terbium extends beyond traditional industrial applications into defense systems, renewable energy infrastructure, and next-generation transportation technologies. These materials enable high-performance permanent magnets that maintain magnetic properties at elevated temperatures, making them irreplaceable in applications ranging from military guidance systems to offshore wind turbines.

Current U.S. dependency on foreign processing creates vulnerability points that extend beyond simple supply disruption. The technical knowledge required for rare earth separation, particularly for heavy rare earth elements, represents decades of accumulated expertise that cannot be rapidly replicated during supply chain emergencies. This reality drives strategic initiatives toward integrated domestic production capabilities.

Furthermore, the development of a critical raw materials facility demonstrates the global nature of supply chain diversification efforts. The critical minerals energy transition requires substantial rare earth element inputs, making domestic production increasingly vital for national security.

When big ASX news breaks, our subscribers know first

Acceleration Timeline: Technical Validation vs Market Positioning

USA Rare Earth Round Top production acceleration represents a significant departure from conventional rare earth development timelines. The company's announcement of a two-year advancement, targeting late 2028 commercial production, positions the project as potentially the first operational U.S. heavy rare earth facility with integrated magnet manufacturing capabilities.

Timeline Comparison Analysis

| Development Phase | Original Target | Accelerated Target | Industry Standard |

|---|---|---|---|

| Pilot Operations | 2026-2027 | Early 2026 | 2-3 years |

| Commercial Production | 2030 | Late 2028 | 5-8 years post-pilot |

| Integrated Magnet Production | 2031+ | 2029 | Varies by integration complexity |

The acceleration hinges entirely on the Hydromet demonstration facility in Wheat Ridge, Colorado, scheduled for early 2026 commissioning. This facility will operate five continuous solvent-extraction circuits for 2,000 to 4,000 hours, generating operational data critical for commercial plant design optimisation.

Historical precedent suggests that rare earth separation technology scale-up frequently reveals challenges not apparent during bench-scale testing. Reagent consumption variability, impurity management complexities, and process reproducibility concerns often emerge during continuous operation periods, potentially affecting timeline feasibility.

However, the strategic significance extends beyond USA Rare Earth's corporate timeline. Successfully executing this acceleration could establish the United States as the second major global producer of heavy rare earth elements, fundamentally altering supply chain dynamics for defense and renewable energy applications. Moreover, the broader mining industry evolution suggests increasing pressure for accelerated development timelines across critical mineral projects.

Hydrometallurgical Processing: The Technology Cornerstone

The Hydromet demonstration facility represents the critical technical validation phase for Round Top's commercial viability. Continuous solvent-extraction processing for heavy rare earth separation demands precise control of multiple chemical and physical parameters to achieve commercial purity standards.

Critical Technical Specifications:

- Five parallel solvent-extraction circuits

- 2,000-4,000 hours continuous operation requirement

- Dysprosium and terbium separation validation

- Commercial plant design parameter generation

- Impurity management protocol development

Solvent-extraction technology separates rare earth elements based on differential chemical affinities between aqueous and organic phases. For heavy rare earth elements with nearly identical chemical properties, multiple extraction stages become necessary to achieve the 99.9% purity levels required for high-performance magnet applications.

The technical challenge intensifies when processing complex ore compositions. Round Top's mineralisation includes uranium and thorium co-occurrence, requiring specialised extraction protocols to remove radioactive elements while maintaining high recovery rates for target rare earth elements.

Scale-Up Risk Factors:

- Reagent consumption exceeding theoretical calculations by 10-30%

- Impurity bleed-off variability affecting product consistency

- Process reproducibility challenges with variable feedstock

- Equipment fouling and maintenance cycle optimisation

- Solvent degradation and regeneration efficiency

Industry experience demonstrates that continuous operation data provides insights unavailable through batch testing. Equipment reliability, reagent stability, and process control optimisation require extended operational periods to validate commercial feasibility assumptions.

"The transition from laboratory-scale separation to continuous pilot operations frequently reveals unexpected technical challenges that can significantly impact capital and operating cost projections."

Vertical Integration Strategy: Comprehensive Value Chain Control

USA Rare Earth's approach combines the Round Top deposit with the Stillwater, Oklahoma magnet manufacturing facility, designed as a 310,000 square-foot integrated metal-and-alloy production plant. This strategy aims to capture value across multiple supply chain segments while establishing domestic alternatives to Chinese-dominated production networks.

Integration Advantages:

- Reduced supply chain complexity and transportation costs

- Enhanced quality control across production stages

- Improved margin capture through value-added processing

- Strategic positioning for government procurement preferences

- Technical optimisation opportunities between mining and manufacturing

The Stillwater facility is positioned as the largest metal-and-alloy production facility outside China, addressing a critical gap in U.S. permanent magnet manufacturing capabilities. Current global production capacity remains concentrated in Chinese facilities, creating supply chain vulnerabilities for defense and renewable energy applications.

Nevertheless, mining operational challenges directly impact magnet facility feedstock availability and utilisation rates. Conversely, magnet production delays or quality issues affect the economic justification for mining operations, creating interdependent risk exposure across both facilities.

Capital allocation between mining and magnet production creates complexity in financial planning and execution priority. The company must successfully execute two technically challenging operations simultaneously while managing funding requirements across both facilities.

Additionally, integrated production enables USA Rare Earth to serve applications requiring complete supply chain traceability, particularly for defense and aerospace applications where material provenance verification is mandatory. This capability provides competitive advantages in government procurement processes that prioritise domestic supply chain validation.

Financial Execution Challenges: Capital Requirements and Market Reality

The accelerated timeline amplifies existing financial execution challenges, particularly given the company's Q3 going-concern warnings and uncertain funding landscape for commercial build-out phases. Rare earth development projects typically require substantial capital investments before generating revenue streams.

Estimated Capital Requirements

| Development Phase | Capital Estimate | Funding Status | Risk Assessment |

|---|---|---|---|

| Hydromet Pilot Facility | $15-25 million | Partially secured | Medium |

| Definitive Feasibility Study | $5-10 million | Uncertain | High |

| Commercial Mining Operations | $150-250 million | Unfunded | Very High |

| Magnet Facility Completion | $50-150 million | Partially committed | High |

The going-concern warnings in recent SEC filings highlight immediate liquidity challenges that could derail development timelines regardless of technical success. Rare earth projects face particular funding challenges due to long development timelines, technical complexity, and volatile commodity pricing.

Traditional debt financing for rare earth projects remains limited due to technical risk profiles and long payback periods. Equity financing dilutes existing shareholders but provides operational flexibility. Government incentives and strategic partnerships offer alternative funding sources but typically include operational requirements and oversight obligations.

The accelerated timeline requires simultaneous capital deployment across multiple facilities, intensifying funding pressure during critical development phases. Delays in securing adequate financing could force timeline extensions regardless of technical readiness.

Consequently, uranium market volatility demonstrates how commodity price fluctuations can impact project economics. Heavy rare earth pricing remains subject to global supply-demand dynamics and geopolitical influences, requiring sustained pricing over multi-year production periods for commercial viability.

What Are the Technical Complexities of Heavy Rare Earth Separation?

Heavy rare earth separation represents the primary bottleneck for establishing commercial U.S. production capabilities. Dysprosium and terbium separation requires sophisticated chemical processing techniques due to the elements' nearly identical chemical properties.

Heavy rare earth separation typically involves 6-10 sequential solvent-extraction stages to achieve commercial purity standards exceeding 99.9%. Each stage requires precise pH control, temperature management, and reagent concentration optimisation to maintain separation efficiency.

Critical Quality Parameters:

- Dysprosium oxide purity: >99.9%

- Terbium oxide purity: >99.9%

- Iron content: <100 ppm

- Other transition metals: <50 ppm

- Moisture content: <0.5%

- Particle size distribution: Controlled for downstream processing

The Round Top deposit presents additional complexity due to its unique mineralogy and co-occurring elements. Uranium and thorium removal requires specialised extraction protocols that must maintain high recovery rates for target rare earth elements while meeting environmental and safety regulations.

Solvent-extraction processes utilise organophosphoric compounds as extractants, with di-2-ethylhexyl phosphoric acid (HDEHP) representing the most common choice for heavy rare earth applications. Reagent consumption optimisation directly impacts operating costs and environmental management requirements.

Extraction efficiency depends on precise control of organic-to-aqueous phase ratios, contact time, and stripping agent concentrations. Pilot operations provide data for optimising these parameters at commercial scale while identifying potential reagent degradation and regeneration requirements.

The next major ASX story will hit our subscribers first

How Does USA Rare Earth Compare to Global Competitors?

USA Rare Earth's acceleration timeline positions the project within a rapidly evolving global competitive landscape for heavy rare earth production. Understanding this context provides insight into market opportunities and competitive pressures affecting project viability.

China maintains approximately 85% market share in heavy rare earth production and processing, with established operations in Jiangxi and Guangdong provinces. Chinese facilities benefit from decades of operational experience, established supply chains, and integrated processing capabilities.

International Development Projects:

- Australia: Lynas Rare Earths expanding heavy rare earth separation capabilities

- Canada: Multiple projects in feasibility and permitting phases

- Greenland: Tanbreez project advancing toward development decisions

- Vietnam: Dong Pao project under evaluation

- Madagascar: Tantalus Rare Earths development initiatives

USA Rare Earth accelerates Texas rare earth production timeline, potentially establishing the United States as the second major global producer of heavy rare earth elements by 2028-2029, significantly ahead of other international projects currently in development phases.

Market demand for heavy rare earth elements continues expanding due to renewable energy infrastructure deployment and defense modernisation programmes. The International Energy Agency projects global demand growth of 7-10% annually through 2030, creating market opportunities for new production capacity.

However, Chinese producers retain the ability to influence global pricing through production adjustments and export policies. New entrants must demonstrate cost competitiveness and supply reliability to establish sustainable market positions.

Additionally, critical production timeline advancements highlight the competitive pressure facing international rare earth development projects. Technology and innovation factors, including advances in permanent magnet design and recycling technologies, could affect long-term demand dynamics.

Risk Assessment Framework: Multiple Development Scenarios

Evaluating USA Rare Earth's acceleration requires comprehensive risk assessment across technical, financial, and market dimensions. Multiple development scenarios provide insight into potential outcomes and investment implications.

Scenario 1: Successful Technical Execution (Estimated Probability: 35%)

The Hydromet facility demonstrates stable operation with commercial-grade separation efficiency. Capital requirements remain within projected ranges, and integrated magnet production achieves design specifications.

Outcome Implications:

- USA Rare Earth establishes market-leading position in U.S. heavy rare earth production

- Integrated operations provide competitive advantages and margin optimisation

- Government procurement relationships support revenue stability

- Significant value creation potential for early investors

Scenario 2: Technical Challenges with Timeline Delays (Estimated Probability: 45%)

Pilot operations reveal technical challenges requiring additional optimisation and capital investment. Production timeline extends to 2029-2031, but ultimately achieves commercial viability.

Outcome Implications:

- Delayed market entry reduces first-mover advantages

- Additional capital requirements pressure financial returns

- Competitive positioning affected by alternative project development

- Moderate value creation potential with extended development timeline

Scenario 3: Technical or Financial Failure (Estimated Probability: 20%)

Pilot operations demonstrate insufficient separation efficiency, excessive reagent consumption, or insurmountable technical challenges. Financial constraints prevent adequate capital deployment for problem resolution.

Outcome Implications:

- Project abandonment or indefinite delay

- Asset write-downs and shareholder losses

- Reduced investor confidence in domestic rare earth development

- Continued U.S. dependence on foreign heavy rare earth sources

Investors considering USA Rare Earth exposure should evaluate position sizing relative to risk tolerance and portfolio diversification requirements. The speculative nature of rare earth development requires careful assessment of potential loss scenarios alongside return opportunities.

Government policy support and strategic partnerships could reduce execution risks while providing operational advantages. Monitoring policy developments and potential strategic investor participation provides insight into project viability and support mechanisms.

Critical Decision Points: Evaluating Technical and Commercial Readiness

The next 18 months represent critical decision points for USA Rare Earth's accelerated timeline. Specific milestones and performance metrics will determine whether the acceleration represents genuine technical readiness or optimistic market positioning.

The Hydromet facility commissioning in early 2026 provides the first critical validation point. Successful pilot operation requires demonstrating stable separation efficiency, manageable reagent consumption, and reproducible product quality across continuous operation periods.

Key Performance Indicators to Monitor:

- Continuous operation stability: >95% uptime during test periods

- Dysprosium separation efficiency: >98% recovery rates

- Terbium purity achievement: >99.9% consistent production

- Reagent consumption: Within 10% of theoretical requirements

- Impurity management: Consistent removal of uranium and thorium

Definitive Feasibility Study completion by early 2027 requires adequate funding and successful pilot validation. The DFS provides updated capital cost estimates, operating cost projections, and economic analysis based on pilot operation data.

Department of Defense procurement commitments, Department of Energy loan guarantee evaluations, and strategic investor participation provide insight into external validation of project viability and strategic importance. Furthermore, the establishment of an australia critical minerals strategic reserve demonstrates international recognition of the strategic importance of domestic critical mineral capabilities.

Securing long-term supply agreements for magnet production and establishing relationships with defense contractors and renewable energy manufacturers demonstrate market acceptance and revenue stability potential.

Investors should prioritise understanding specific technical achievements at bench scale, validated reagent suppliers and costs, environmental permitting status, and management team execution experience in rare earth development projects.

Industry Implications: Reshaping Domestic Critical Materials Strategy

USA Rare Earth's acceleration timeline, regardless of ultimate execution success, influences broader U.S. critical materials strategy and investment allocation across domestic rare earth development initiatives.

Successful execution validates the integrated mine-to-magnet approach, potentially influencing government policy support for similar projects. The Defense Production Act and other strategic initiatives could prioritise integrated operations that demonstrate supply chain resilience and traceability capabilities.

Project success could attract additional capital to domestic rare earth development while failure could reinforce investor scepticism about technical feasibility and commercial viability of U.S. rare earth projects.

The Hydromet facility pilot operations will generate technical data and operational experience valuable for future rare earth separation projects. Process optimisation insights and equipment performance data could accelerate development timelines for subsequent projects.

Establishing domestic heavy rare earth production capabilities reduces strategic vulnerability while providing alternatives for defense and critical infrastructure applications. This capability strengthens negotiating positions with international suppliers and provides crisis response options.

Chinese producers may respond to successful U.S. production through pricing strategies or technology advancement initiatives. International projects in Australia and Canada could accelerate development timelines to maintain competitive positioning.

Conclusion: A Calculated Strategic Gamble

USA Rare Earth Round Top production acceleration represents a high-stakes strategic gamble with significant implications for U.S. critical materials security and domestic rare earth industry development. The two-year timeline compression amplifies both opportunity potential and execution risks across technical and financial dimensions.

The success or failure of this acceleration will be determined primarily by the Hydromet demonstration facility performance in 2026. Technical validation of continuous solvent-extraction operations for heavy rare earth separation represents the critical bottleneck that will determine timeline feasibility and commercial viability.

Financial execution challenges, highlighted by recent going-concern warnings, create additional uncertainty regardless of technical success. The company must simultaneously secure adequate funding for pilot operations, definitive feasibility studies, and eventual commercial construction while managing cash flow requirements across integrated operations.

For investors, the USA Rare Earth acceleration timeline requires balancing significant upside potential against substantial execution risks. The project's strategic importance for U.S. supply chain security provides policy support and potential government partnership opportunities while market positioning advantages create competitive moats if successfully executed.

The next 18 months will provide critical validation data for technical feasibility, financial viability, and market acceptance. Pilot operation results, funding commitments, and strategic partnership development will determine whether this acceleration represents genuine technical readiness or ambitious market positioning under financial pressure.

Success would establish a precedent for integrated rare earth development in the United States while demonstrating technical feasibility for heavy rare earth separation at commercial scale. Failure could delay domestic rare earth development initiatives and reinforce dependence on international supply sources during a period of increasing geopolitical uncertainty.

The strategic importance of establishing domestic heavy rare earth production capabilities extends beyond USA Rare Earth's corporate objectives to national security and industrial competitiveness considerations. This broader context provides additional motivation for successful execution while increasing stakeholder scrutiny of development progress and milestone achievement.

Investors considering exposure to this strategic gamble should carefully evaluate risk tolerance, position sizing, and portfolio diversification while monitoring technical validation milestones and funding developments throughout the critical validation period ahead.

Ready to Capitalise on Critical Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across critical materials sectors, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring major mineral discovery outcomes and begin your 30-day free trial today to position yourself ahead of the market.