June 18, 2026

Global energy markets face an unprecedented paradox: nations with the world's largest proven reserves often struggle to monetise their resources effectively. This phenomenon reflects deeper structural challenges within the petroleum industry, where institutional frameworks, governance quality, and investment climate determine production capacity more than geological endowments alone.

The disconnect between resource abundance and actual output represents a critical vulnerability in global energy security. As consuming nations seek supply diversification and price stability, the ability to convert reserves into reliable production streams becomes paramount. This dynamic reshapes traditional energy geopolitics, where resource ownership no longer guarantees market influence without corresponding institutional capacity.

Venezuela oil governance and supply challenges exemplify this broader trend, where political instability and policy failures have transformed a resource-rich nation into a cautionary tale for the international petroleum sector. Understanding these mechanisms provides essential insights for energy market participants, policymakers, and investors navigating an increasingly complex global supply landscape.

Understanding Venezuela's Energy Paradox: Reserves vs. Reality

The Resource-Production Disconnect in Numbers

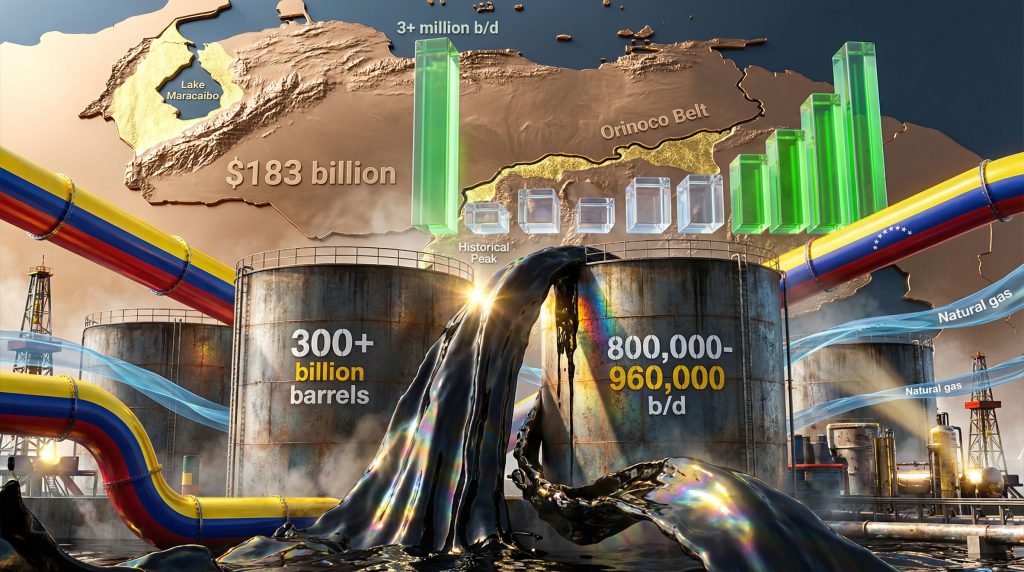

Venezuela maintains some of the world's largest proven oil reserves, yet current production levels remain dramatically below historical capacity and resource potential. This disparity illustrates how geological abundance fails to translate into energy security without proper institutional frameworks.

The nation's current output of approximately 800,000 to 960,000 barrels per day represents a stark contrast to North Dakota's production levels, despite the South American country's vastly superior reserve base. This comparison highlights the fundamental principle that energy strength derives from operational efficiency, investment climate, and governance quality rather than resource endowments alone.

| Production Metric | Venezuela | North Dakota | Variance |

|---|---|---|---|

| Current Daily Output | 800,000-960,000 bbl/d | 1,200,000+ bbl/d | -25% to -33% |

| Peak Historical Production | 3,200,000 bbl/d | 1,500,000 bbl/d | +113% |

| Reserve Base | 300+ billion barrels | 7.4 billion barrels | +4,000% |

| Production Efficiency | 0.3% of reserves annually | 4.5% of reserves annually | -93% |

Historical production data reveals Venezuela achieved peak output exceeding 3.2 million barrels per day during the late 1990s, demonstrating the technical feasibility of substantial production from existing fields. The subsequent decline trajectory correlates directly with policy changes, institutional deterioration, and foreign investment withdrawal.

Governance Fundamentals That Determine Energy Strength

The relationship between institutional quality and energy production capacity operates through several critical mechanisms. Contract sanctity serves as the foundational requirement for long-term capital deployment in petroleum development projects, which typically require 15-20 year investment horizons to achieve acceptable returns.

Rule of law provides the predictable regulatory environment necessary for international oil companies to commit substantial capital resources. Without legal protections for foreign investment, multinational corporations cannot justify the financial exposure required for large-scale upstream development projects.

Investment security encompasses both physical asset protection and policy continuity. Energy infrastructure represents high-value, immobile capital that remains vulnerable to expropriation, nationalisation, or regulatory changes that fundamentally alter project economics. This vulnerability requires premium risk adjustments that often render projects economically unviable.

Key governance requirements for sustainable energy development include:

• Transparent regulatory frameworks with consistent application across all market participants

• Independent judicial systems capable of enforcing contractual obligations

• Stable fiscal regimes that balance government revenue needs with investor returns

• Professional regulatory agencies insulated from short-term political pressures

• Clear dispute resolution mechanisms recognised by international arbitration bodies

The absence of these institutional foundations creates a risk premium that often exceeds potential project returns, effectively preventing capital deployment regardless of resource quality or market conditions.

When big ASX news breaks, our subscribers know first

What Are the Macro-Economic Drivers Behind Venezuela's Supply Constraints?

Infrastructure Capital Depreciation Analysis

Years of deferred maintenance and underinvestment have created substantial infrastructure decay across Venezuela's petroleum sector. This deterioration extends beyond individual well sites to encompass entire production systems, including gathering networks, processing facilities, and transportation infrastructure.

The economic impact of infrastructure degradation compounds over time through several mechanisms. Production decline rates accelerate when preventive maintenance programmes are suspended, requiring increasingly expensive remedial interventions to restore capacity. Operating costs per barrel increase as ageing equipment requires more frequent repairs and operates at reduced efficiency.

Moreover, analysing the Venezuela crisis reveals how institutional breakdown compounds infrastructure challenges, creating a vicious cycle of declining production and reduced investment capacity. Furthermore, understanding broader oil production challenges provides context for the systematic nature of these infrastructure failures.

Critical infrastructure assessment reveals that deferred maintenance costs compound exponentially, with each year of delay typically doubling the ultimate restoration expense while reducing recoverable reserves.

Cost-benefit analysis comparing rehabilitation versus new development presents stark choices:

• Rehabilitation advantages: Existing infrastructure foundation, proven reservoir characteristics, established transportation networks

• Rehabilitation challenges: Unknown condition of subsurface equipment, outdated technology standards, contamination and safety hazards

• New development advantages: Modern technology integration, optimised field layouts, comprehensive environmental compliance

• New development disadvantages: Higher capital requirements, longer development timelines, regulatory approval complexities

The infrastructure decay timeline suggests that certain assets may have crossed economic viability thresholds, where restoration costs exceed replacement alternatives. This analysis becomes critical for international investors evaluating entry strategies and capital allocation priorities.

Heavy Crude Economics and Market Positioning

Venezuelan oil production consists predominantly of heavy crude grades, particularly from the Orinoco Belt region, with API gravities typically ranging from 8 to 16 degrees. These heavy crude characteristics create specific economic and technical challenges that influence production economics and market access.

Processing cost structure for heavy crude includes:

• Enhanced extraction requirements: Steam injection, chemical flooding, or other enhanced oil recovery techniques

• Specialised transportation: Diluent addition or heating requirements for pipeline transport

• Complex refining specifications: Higher conversion costs and specialised refinery configurations

• Environmental compliance: Increased sulphur content requiring additional processing to meet fuel specifications

Price differentials between heavy and light crude typically range from $10 to $25 per barrel, depending on market conditions and refining capacity utilisation. These discounts must be offset by lower production costs or higher recovery factors to maintain project economics.

Global refining capacity specifically configured for heavy crude processing remains concentrated among a limited number of facilities, primarily in the United States Gulf Coast, Canada, and select international locations. This concentration creates potential bottlenecks for Venezuelan crude marketing and limits pricing flexibility.

How Do Geopolitical Transitions Impact Energy Market Fundamentals?

U.S. Oversight Model and Market Control Mechanisms

The potential framework for renewed U.S.-Venezuela energy cooperation involves sophisticated oversight mechanisms designed to balance commercial objectives with policy compliance requirements. These structures would likely incorporate revenue management systems that channel proceeds through controlled accounts to ensure transparency and appropriate allocation.

Furthermore, the oil price rally analysis suggests that Venezuelan production recovery could significantly impact global pricing dynamics, particularly if market conditions favour increased supply diversity.

Export licensing frameworks under consideration include:

• Competitive bidding processes for marketing and transportation services

• Third-party verification systems for production volumes and revenue calculations

• Escrow account management with international banking institution oversight

• Graduated licensing scales tied to governance improvements and compliance metrics

Strategic petroleum relationships between the United States and Venezuela would require bilateral agreements addressing worker safety protocols, environmental standards, and operational oversight mechanisms. These agreements must balance commercial viability with political risk mitigation for both governments.

The proposed oversight model draws from historical precedents in sanctions management and post-conflict economic reconstruction, adapted for the unique characteristics of petroleum sector operations. Implementation would require coordination between multiple U.S. government agencies and international monitoring organisations.

International Investment Climate Assessment

Risk-return analysis for major oil companies evaluating Venezuelan entry reveals complex decision matrices balancing potential returns against political, operational, and reputational risks. International oil companies must evaluate investment opportunities through multiple risk frameworks:

-

Political risk assessment: Government stability, policy continuity, and expropriation probability

-

Operational risk evaluation: Infrastructure condition, workforce availability, and security requirements

-

Commercial risk analysis: Market access, price realisation, and cost structure competitiveness

-

Regulatory compliance risk: Sanctions compliance, environmental standards, and reporting obligations

-

Reputational risk management: Stakeholder perception, ESG compliance, and brand protection

Legal framework requirements for sustainable foreign investment include:

• International arbitration clauses with enforcement mechanisms recognised by major financial centres

• Stabilisation provisions protecting against adverse regulatory changes

• Force majeure protections covering political events and security disruptions

• Currency conversion guarantees and capital repatriation rights

Production-sharing contract models under development would need to address the unique characteristics of Venezuelan heavy crude production while providing adequate returns to justify the elevated risk profile. These contracts must balance government revenue objectives with investor requirements for acceptable risk-adjusted returns.

What Investment Capital Requirements Drive Venezuelan Oil Recovery?

Short-Term Production Enhancement Scenarios

Analysis of Venezuela's near-term production potential reveals differentiated opportunities based on geographical location and existing infrastructure condition. Lake Maracaibo region offers the most immediate production enhancement possibilities, given existing operations and relatively better-maintained infrastructure.

However, tariff policy implications could significantly affect the economics of Venezuelan oil investments, particularly regarding equipment imports and technology transfers needed for production enhancement.

12-18 month capacity addition scenarios suggest:

• Incremental production potential: 200,000 to 600,000 barrels per day

• Capital requirements: $2 to $5 billion for quick-win projects

• Primary focus areas: Well re-completion, facility rehabilitation, and transportation bottleneck resolution

• Expected timeline: First production increases within 6-12 months of investment commencement

Lake Maracaibo's advantages include existing Chevron operations providing operational continuity, established transportation infrastructure to export terminals, and conventional crude grades requiring less complex processing than Orinoco Belt production.

The Orinoco Belt presents longer-term opportunities but requires substantially higher capital commitments due to the heavy crude characteristics and more extensive infrastructure requirements. Development economics favour conventional crude restoration before proceeding to capital-intensive unconventional projects.

Quick-win investment strategies prioritise:

-

Workover programmes on temporarily abandoned wells with known production history

-

Facility restoration projects targeting processing and separation equipment

-

Transportation infrastructure repair including pipelines and loading facilities

-

Power generation capacity restoration to support production operations

Long-Term Sector Reconstruction Economics

Comprehensive sector reconstruction to achieve historical production levels requires substantial capital deployment across multiple development phases. Industry estimates suggest total investment requirements approaching $183 billion to restore production capacity to 3 million barrels per day, though this figure requires verification against current cost structures and technology standards.

Phased development timeline encompasses:

Phase 1 (Years 1-3): Infrastructure rehabilitation and quick-win projects targeting 1.5 million barrels per day

Phase 2 (Years 4-7): Enhanced oil recovery implementation and new field development reaching 2.2 million barrels per day

Phase 3 (Years 8-12): Full Orinoco Belt development and advanced technology deployment achieving 3+ million barrels per day target

Capital deployment strategies must account for the sequential nature of petroleum development, where early-phase investments in infrastructure and basic production systems enable subsequent phases requiring higher technology and capital intensity.

Economic modelling for 2040 production goals considers:

• Technology advancement impacts on recovery factors and operational costs

• Market demand scenarios and price realisation assumptions

• Alternative supply source competition from U.S. unconventional, deepwater, and renewable energy sources

• Climate policy impacts on long-term crude oil demand growth

The investment timeline extends beyond typical corporate planning horizons, requiring governmental policy commitment and international financial institution support to maintain funding continuity throughout the development cycle.

How Do Environmental Costs Factor Into Venezuelan Oil Economics?

Carbon Intensity and Climate Risk Assessment

Venezuelan heavy crude production presents elevated carbon intensity compared to conventional crude oil sources, primarily due to enhanced extraction requirements and processing complexity. Carbon footprint analysis reveals multiple emission sources throughout the production and processing value chain.

Additionally, energy transition challenges faced by other oil-producing nations provide valuable lessons for Venezuela's environmental planning and carbon management strategies.

Heavy crude carbon footprint components include:

• Enhanced extraction emissions: Steam generation for thermal recovery operations

• Processing energy requirements: Additional refining complexity for heavy crude conversion

• Transportation impacts: Diluent requirements and heating for pipeline transport

• Flaring and venting losses: Associated gas handling in remote production areas

Climate transition risks for Venezuelan oil development projects encompass both physical climate impacts and policy-driven demand changes. Physical risks include increased extreme weather events affecting production infrastructure and transportation systems.

Policy risks involve:

• Carbon border adjustments in major consuming markets affecting price realisation

• Fuel quality standards requiring additional processing investments

• Net-zero commitments by major oil companies limiting high-carbon project participation

• Stranded asset risks as renewable energy deployment accelerates

Environmental compliance costs represent an increasingly significant component of total project economics, requiring integration into investment analysis and capital budgeting processes.

Operational Environmental Economics

Environmental management for Venezuelan oil operations requires substantial upfront investment in prevention systems and ongoing monitoring programmes. Spill prevention and remediation cost structures reflect the challenging operational environment and ageing infrastructure condition.

Environmental compliance budget allocations typically include:

-

Spill prevention systems: Pipeline integrity monitoring, leak detection systems, and containment infrastructure

-

Remediation reserves: Financial provisions for historical contamination cleanup and ongoing incidents

-

Air quality management: Emissions monitoring, flare gas recovery, and methane capture systems

-

Water treatment facilities: Produced water handling, groundwater protection, and discharge compliance

-

Wildlife protection measures: Habitat preservation, migration corridor maintenance, and biodiversity monitoring

Methane capture technology investment requirements have increased significantly due to enhanced regulatory focus on greenhouse gas emissions. Modern methane capture systems can achieve 95%+ efficiency rates but require substantial capital investment and ongoing maintenance commitments.

Operational environmental economics must account for the long-term nature of environmental liabilities, which often extend decades beyond active production periods. This extended liability timeline affects project economics and requires conservative financial provisioning to ensure adequate cleanup funding availability.

What Does Venezuela's Experience Reveal About Global Energy Market Resilience?

Supply Diversification and Market Stability Analysis

The transformation of global energy market dynamics reflects fundamental shifts in production geography and supply chain resilience. U.S. production growth has fundamentally altered traditional energy security calculations, reducing dependence on potentially unstable supply sources.

Current U.S. oil and gas production exceeds the combined output of Iran and Venezuela by substantial margins, representing a structural change in global supply patterns. This production diversification has enabled Middle East imports to decline to generational lows, reducing vulnerability to geopolitical supply disruptions.

Furthermore, OPEC market influence has diminished as non-OPEC production, particularly from the United States, has provided alternative supply sources and reduced traditional producer leverage.

Market resilience metrics during recent geopolitical events demonstrate:

• Reduced price volatility during supply disruption events

• Faster market adjustment mechanisms through U.S. production flexibility

• Enhanced strategic petroleum reserve effectiveness supported by domestic production capacity

• Improved supply chain redundancy across multiple production regions

The strategic implications extend beyond immediate supply security to encompass broader energy diplomacy and international relations. Reduced import dependence provides greater foreign policy flexibility and reduces economic vulnerability to supply manipulation by producing nations.

Supply diversification benefits include:

• Economic stability: Reduced exposure to external price shocks and supply interruptions

• Energy security enhancement: Domestic production capacity providing strategic flexibility

• Investment attraction: Stable energy costs supporting manufacturing competitiveness

• Geopolitical independence: Reduced influence of unstable producing regions on domestic policy

Demand Growth Patterns and Supply Security

Contrary to peak demand theories that suggested global energy consumption would plateau, recent consumption data reveals continued growth across multiple energy sectors. Oil, natural gas, LNG, and electricity consumption all achieved record levels in recent years, challenging assumptions about demand saturation.

This demand growth occurs despite significant renewable energy deployment and efficiency improvements, suggesting that global energy markets remain supply-constrained rather than demand-limited. The persistence of demand growth creates ongoing requirements for reliable supply sources and infrastructure investment.

Global energy consumption trends reveal:

| Energy Source | Annual Growth Rate | Primary Drivers |

|---|---|---|

| Natural Gas | 2.5-3.2% | Power generation, industrial applications, LNG exports |

| Crude Oil | 1.8-2.4% | Transportation demand, petrochemical feedstock |

| Electricity | 3.1-4.2% | Economic development, electrification trends |

| LNG Trade | 4.8-6.1% | Energy security diversification, coal replacement |

Peak demand theory reassessment based on current consumption patterns suggests that global energy markets will continue requiring substantial supply additions throughout the next two decades. This sustained demand outlook supports investment in diverse supply sources, including potentially controversial projects in challenging jurisdictions.

LNG export opportunities represent a particular growth area, with global trade volumes expanding rapidly as nations seek supply diversification and cleaner-burning alternatives to coal and oil products. Natural gas market expansion creates additional development opportunities for resource-rich nations with appropriate infrastructure and governance frameworks.

The next major ASX story will hit our subscribers first

Strategic Investment Implications for Energy Market Participants

Risk Assessment Framework for Venezuelan Energy Investments

Investment evaluation in Venezuela's energy sector requires sophisticated risk assessment frameworks that account for the unique combination of resource potential and institutional challenges. Political risk evaluation criteria must encompass both current conditions and trajectory analysis for institutional improvement.

Considering US economic pressures affecting global investment flows, Venezuelan energy investments face additional complexity from macroeconomic policy changes that could impact financing availability and project economics.

Comprehensive due diligence requirements include:

• Governance assessment: Institutional capacity, policy continuity, and regulatory predictability evaluation

• Operational analysis: Infrastructure condition, workforce availability, and security environment assessment

• Financial framework: Currency risks, capital controls, and repatriation mechanisms analysis

• Legal structure: Contract enforceability, dispute resolution, and asset protection evaluation

• Market access: Export logistics, processing capacity, and buyer diversification assessment

Political risk mitigation strategies involve:

-

Phased investment approaches limiting initial capital exposure while establishing operational presence

-

International insurance coverage through political risk insurance providers and multilateral agencies

-

Diversified partnership structures involving multiple international companies and local entities

-

Contingency planning for various political and economic scenarios affecting operations

-

Stakeholder engagement with government officials, civil society, and international oversight bodies

Contract structure recommendations emphasise flexibility and protection mechanisms that can adapt to changing political and economic conditions while maintaining commercial viability for all parties.

Portfolio Diversification Lessons from Venezuelan Energy Sector

The Venezuelan experience provides valuable insights for energy portfolio management and geographic risk distribution strategies. Governance quality emerges as the primary determinant of long-term investment success, often outweighing traditional geological and economic factors.

Geographic risk distribution principles include:

• Institutional diversity: Balancing investments across different governance quality levels and political systems

• Operational risk spreading: Avoiding concentration in similar operational environments or infrastructure dependencies

• Market access diversification: Ensuring multiple export routes and buyer relationships across different regions

• Currency risk management: Distributing revenue streams across multiple currency zones and exchange rate regimes

Governance quality metrics for investment decisions encompass:

- Rule of law indicators: Legal system effectiveness, contract enforcement, and property rights protection

- Regulatory quality measures: Policy consistency, regulatory burden, and administrative efficiency

- Political stability assessment: Government effectiveness, political violence, and policy continuity

- Corruption control evaluation: Transparency levels, administrative integrity, and anti-corruption effectiveness

Long-term energy security planning for institutional investors requires recognition that resource endowments alone do not guarantee investment success. Institutional capacity and governance quality often determine project viability more than geological or market factors.

Portfolio construction lessons from Venezuelan energy sector include:

• Governance risk assessment as primary screening criterion for energy investments

• Institutional capacity evaluation before committing substantial capital to resource development projects

• Political risk insurance as essential component of emerging market energy investments

• Stakeholder engagement strategies for managing community relations and government partnerships

• Exit strategy planning for investments in politically volatile jurisdictions

Governance-Driven Energy Market Dynamics

Key Takeaways for Energy Market Analysis

The Venezuelan experience demonstrates that governance quality serves as the fundamental determinant of successful resource monetisation, regardless of geological endowments or market conditions. This principle applies broadly across global energy markets, where institutional capacity often matters more than resource abundance.

Investment climate requirements for sustainable energy development include:

• Legal framework stability providing predictable operating conditions for long-term projects

• Contract sanctity protection ensuring agreements remain enforceable throughout project lifecycles

• Regulatory consistency maintaining stable fiscal and operational requirements

• Infrastructure investment capacity supporting necessary development and maintenance programmes

• Security frameworks protecting personnel and assets from political and criminal risks

Market resilience factors in global energy supply chains have evolved significantly, with production diversification providing enhanced stability during geopolitical disruptions. The United States' role as the world's largest energy producer has fundamentally altered traditional energy security calculations and reduced market vulnerability to individual country supply disruptions.

These dynamics suggest that future energy market analysis must incorporate governance assessment as a primary analytical framework, rather than focusing primarily on geological or economic factors. Institutional quality provides the foundation for all other investment considerations in energy sector development.

Future Outlook for Venezuelan Energy Sector Integration

Timeline projections for meaningful Venezuelan production recovery span multiple decades, with initial improvements possible within 12-18 months under favourable policy conditions, but substantial capacity restoration requiring 10-15 years of sustained investment and institutional development.

Realistic production recovery scenarios include:

Optimistic scenario (2026-2030): 1.5-2.0 million barrels per day through infrastructure rehabilitation and quick-win projects

Base case scenario (2030-2035): 2.0-2.5 million barrels per day with sustained foreign investment and governance improvements

Full recovery scenario (2035-2040): 3.0+ million barrels per day requiring comprehensive sector reconstruction and advanced technology deployment

Global market impact scenarios based on Venezuelan supply return suggest modest effects on global balances, given current U.S. production capacity and market diversification. However, regional market dynamics could experience more significant impacts, particularly in Caribbean and Latin American crude oil markets.

Strategic considerations for international energy market participants include the long-term nature of Venezuelan recovery, the substantial capital requirements involved, and the continued political and operational risks that may persist despite policy improvements.

Disclaimer: This analysis contains forward-looking projections and investment considerations that involve substantial uncertainties. Political developments, economic conditions, and regulatory changes could materially affect actual outcomes. Readers should conduct independent due diligence and consult qualified professionals before making investment decisions related to Venezuelan energy sector opportunities.

The Venezuela oil governance and supply challenges serve as a comprehensive case study in the complex relationships between institutional quality, resource development, and market dynamics. Understanding these relationships provides essential insights for navigating an increasingly complex global energy landscape where governance quality often determines investment success more than traditional geological or economic factors.

Ready to Identify Energy Market Opportunities Before They're Widely Recognised?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications about significant ASX mineral discoveries, including critical energy transition metals that power the global shift to renewable energy. Subscribers gain immediate access to actionable investment insights that help identify emerging opportunities in the mining sector before broader market recognition develops. Begin your 30-day free trial today and secure your competitive advantage in the rapidly evolving energy and resources markets.