June 26, 2026

India's Corporate Profitability and the Geopolitics of Energy: Understanding the Stakes

Few forces reshape corporate earnings as swiftly and indiscriminately as an energy price shock rooted in geopolitical conflict. When supply routes for crude oil and natural gas face sudden disruption, the damage does not stay contained within the energy sector. It radiates outward through input costs, currency valuations, inflation dynamics, and ultimately the profit margins of businesses with no direct connection to energy. For India, this transmission mechanism is especially potent given the country's structural dependence on imported hydrocarbons, and the West Asia truce impact on India Inc profitability has become one of the most consequential economic stories of the current fiscal year.

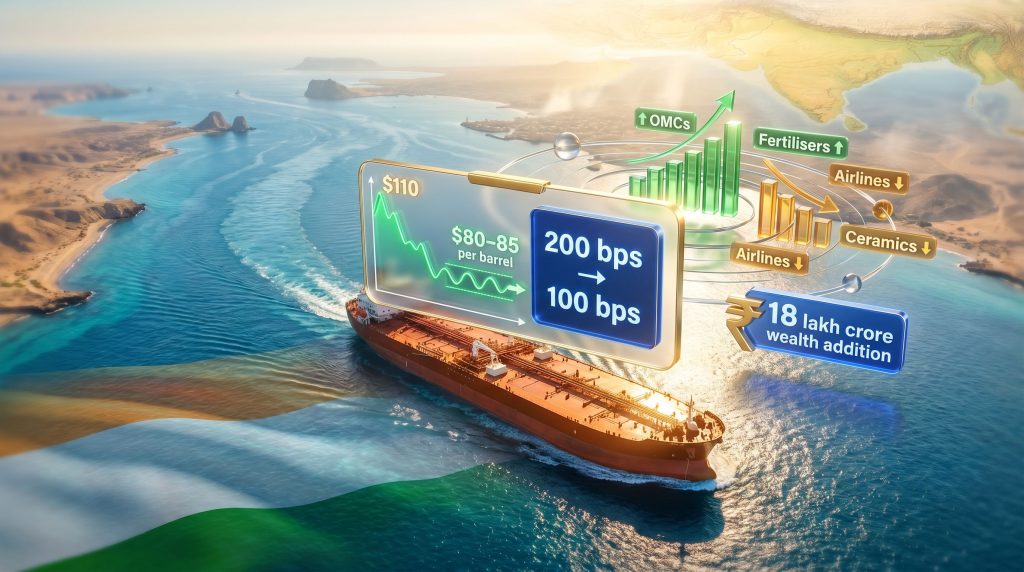

The shift from a prolonged-conflict scenario to a fragile but operative diplomatic understanding between the United States and Iran has materially altered the earnings trajectory for Indian corporates. According to CRISIL Ratings, the projected compression in India Inc's operating margins has been halved, falling from an estimated 200 basis points under the extended conflict model to approximately 100 basis points under the revised post-truce outlook. Understanding what that number means in practice requires examining both the structural vulnerabilities that created the exposure and the sectoral mechanics through which relief is now flowing.

When big ASX news breaks, our subscribers know first

India's Deep Energy Import Dependency: The Macro Foundation of Corporate Risk

India's reliance on imported crude oil sits at well above four-fifths of total national consumption, with official data from the Petroleum Planning and Analysis Cell (PPAC) consistently placing this figure in the vicinity of 85% in recent fiscal years. This level of dependence transforms every major geopolitical event in hydrocarbon-producing regions into a direct concern for Indian businesses, regardless of their sector.

The mechanism is multilayered. When crude prices rise, energy-intensive manufacturers face immediate input cost inflation. When supply routes are disrupted, the problem compounds because price increases alone no longer guarantee physical availability of inputs. For sectors such as ceramics, fertilisers, and specialty chemicals, natural gas is not merely a fuel source but a core production input. A disruption in gas supply cannot simply be absorbed through hedging or cost pass-through in the short term, as it threatens production volumes themselves.

A further transmission channel operates through the Indian rupee. Elevated oil prices widen India's current account deficit by increasing the import bill in US dollar terms, placing depreciation pressure on the currency. A weaker rupee then amplifies import costs across the entire economy, creating a secondary inflation wave that extends far beyond energy-intensive sectors. Furthermore, understanding the oil price rally dynamics from earlier in 2025 provides useful context for how quickly these price mechanisms can shift corporate cost structures.

India's corporate profitability is not merely a function of domestic demand. It is structurally tethered to geopolitical stability in West Asia through the twin channels of crude oil pricing and natural gas supply continuity.

Under the prolonged conflict stress scenario modelled earlier this year, Brent crude was tested at $110 per barrel, a threshold that CRISIL assessed would trigger meaningful margin compression across 22 of 34 sectors in the Indian economy. Gas supply disruptions in that scenario were projected to persist for up to three quarters, posing an existential operational threat to manufacturers with gas-intensive production processes.

The Truce Mechanism: How Diplomatic Progress Translated Into Economic Relief

The partial reopening of key West Asian shipping routes following an interim understanding between Washington and Tehran produced an immediate and measurable shift in energy market conditions. The stabilisation of supply route access reduced the geopolitical risk premium embedded in crude oil prices, enabling a significant correction from conflict-era levels.

CRISIL now projects Brent crude to average $80-85 per barrel for the current fiscal year, down from the $110 stress-case assumption. Gas supply disruptions are now expected to last approximately four months, considerably shorter than the prior projection of up to three quarters. These two revisions alone substantially alter the input cost environment for corporate India.

The macroeconomic transmission was rapid. The rupee strengthened by approximately 40 paise against the US dollar, settling around ₹84.20. Indian equity markets responded with an addition of roughly ₹18 lakh crore in investor wealth following the truce announcement, reflecting the speed at which geopolitical risk premiums were repriced out of valuations. Market volatility of this magnitude underscores how sensitive Indian equities have become to West Asian geopolitical developments.

The table below summarises the key scenario shifts driving the revised profitability outlook:

| Macro Indicator | Conflict Scenario | Post-Truce Outlook | Net Benefit |

|---|---|---|---|

| Brent Crude (avg. per barrel) | ~$110 | $80-85 | ~$25-30 reduction |

| Gas Supply Disruption Duration | Up to 3 quarters | ~4 months | Significantly shorter |

| India Inc Operating Margin Compression | 200 bps | 100 bps | Halved |

| Median Operating Margins | ~10% | ~11% | +1 percentage point |

| Pre-Conflict Baseline Margins | ~12% | ~12% | Baseline reference |

| Rupee Movement | Depreciation pressure | Rose ~40 paise to ₹84.20 | Strengthened |

| Investor Wealth Impact | Erosion risk | ₹18 lakh crore addition | Significant recovery |

| Sectors Facing Meaningful Margin Pressure | 22 sectors | 10 sectors | More than halved |

Lower crude prices also carry a significant fiscal dividend for the Indian government. Analysts estimate the reduction in the national oil import bill translates to approximately 0.5-0.8% of GDP in fiscal savings, preserving government capacity to sustain infrastructure spending while simultaneously reducing the inflationary pressure that had been building through petroleum product pricing.

Sectoral Profitability Under the Revised Outlook: Recovery Is Uneven

The headline improvement in aggregate margin compression from 200 bps to 100 bps conceals substantial variation across sectors. The relief is not uniformly distributed, and several industries continue to carry significant earnings risk even under the improved scenario.

Sectors Positioned for Recovery

Oil marketing companies (OMCs) represent one of the clearest beneficiaries of the crude price correction. These companies accumulated an estimated ₹40,000-45,000 crore in net under-recoveries between March and May as they absorbed the gap between global crude costs and domestic retail fuel prices. As crude normalises toward the $80-85 range, OMCs are now projected to post positive operating profits for the full fiscal year, reversing what had appeared to be a structurally loss-making period.

Fertiliser manufacturers benefit through the gas supply normalisation channel. Natural gas is the primary feedstock for urea and other nitrogenous fertilisers, meaning gas shortages directly constrain production capacity rather than merely elevating costs. With supply disruptions now expected to be contained to approximately four months, fertiliser producers can restore production economics and margin predictability.

Downstream petrochemical producers and refiners also benefit from easing feedstock costs, with processing margins improving as the crude-to-product spread normalises. According to CRISIL's detailed analysis of West Asia's economic impact, the degree of recovery across these downstream segments is closely tied to how durably the truce conditions hold through the second half of the fiscal year.

Sectors Remaining Under Structural Pressure

| Sector | Primary Stress Driver | Margin Risk Profile |

|---|---|---|

| Airlines | Aviation turbine fuel costs + currency weakness | Elevated |

| Ceramics | Prior gas shortages; lagged cost absorption | Severe |

| Specialty Chemicals | Feedstock cost volatility | Moderate to High |

| Flexible Packaging | Crude-linked polymer input costs | Moderate |

| Polyester Textiles | PTA/MEG feedstock pricing | Moderate |

The ceramics sector carries the most acute residual risk among all affected industries. Revenue in this segment could fall by more than one-third, with profitability potentially halving due to the lagged financial impact of gas shortages already incurred during the conflict period. Even as forward gas prices ease, manufacturers that purchased inputs at peak conflict-era prices will carry elevated cost bases through the first two quarters of the fiscal year.

Kiln operations in ceramics are particularly sensitive to gas price and availability because the fuel cannot be easily substituted in the short term without significant capital expenditure.

Airlines face a structural double burden that is unlikely to be resolved quickly. Aviation turbine fuel costs remain elevated relative to pre-conflict levels, and currency weakness relative to pre-truce conditions limits the ability to hedge international route exposure effectively. The sector also has limited pricing power in a competitive domestic market, constraining the degree to which fuel cost increases can be passed through to passengers.

The Lagged Cost Absorption Problem: A Less-Discussed Risk

One of the less-examined dynamics in the post-truce outlook is the distinction between forward cost relief and backward cost absorption. When energy prices fall, the immediate benefit flows to companies purchasing inputs at spot prices going forward. However, businesses that locked in procurement contracts, built inventory at elevated prices, or structured long-term input agreements during the peak conflict period do not immediately benefit from the price correction.

This lagged absorption problem is particularly acute in manufacturing sectors with long production cycles. Ceramics manufacturers, for instance, may have committed to gas supply agreements at conflict-era pricing that persist through Q1 and Q2. Their reported margins in these quarters will therefore reflect the cost environment of the conflict period rather than the improved post-truce conditions. Investors and analysts relying solely on forward guidance without accounting for this legacy cost burden risk overestimating near-term earnings recovery.

This dynamic also has implications for how corporate boards and CFOs should approach scenario planning. The West Asia situation has demonstrated that multi-scenario financial modelling, including stress tests at $110 crude, provides material operational advantages. Companies with pre-existing hedge positions and scenario-tested procurement frameworks were better placed to navigate the conflict period and are now better positioned to capitalise on the recovery.

Demand-Side Dynamics: The Domestic Stabilisers

While the supply-side story has dominated coverage of the West Asia truce impact on India Inc profitability, demand-side factors have played an equally important stabilising role. Government infrastructure expenditure has continued to underpin order books across construction, cement, and capital goods manufacturing. Lower energy input costs improve project economics for infrastructure developers, potentially accelerating project delivery timelines and unlocking incremental orders.

Consumer-facing sectors including FMCG, retail, and consumer durables carry limited direct energy exposure and are expected to largely preserve pre-conflict margin profiles. Perhaps more importantly, the easing of inflationary pressure from lower oil prices has the effect of expanding real consumer purchasing power, providing a modest but meaningful demand tailwind for businesses serving domestic households.

Rural income stability and urban wage growth have maintained consumption resilience through the conflict period, providing a demand floor that has partially offset cost-side pressures in sectors exposed to energy inflation.

The next major ASX story will hit our subscribers first

Risk Factors That Could Reverse the Recovery

The improved profitability outlook is explicitly contingent on a set of assumptions that carry meaningful uncertainty. The US-Iran understanding is characterised as interim and conditional, not a binding formal treaty. Any deterioration in relations, renewed proxy conflict escalation, or breakdown in compliance monitoring could rapidly restore conflict-level crude pricing and re-expose the sectors currently assessed as facing minimal disruption.

The 100 bps margin compression estimate is contingent on the West Asia truce holding through the fiscal year. A renewed escalation scenario could rapidly push compression back toward the original 200 bps projection, re-exposing a significantly broader set of Indian industries to profitability stress.

Three additional risk factors deserve attention:

-

Monsoon performance: A below-average monsoon would compress rural incomes and reduce agricultural output, creating a demand-side headwind for sectors with significant rural revenue exposure including two-wheelers, agrochemicals, and FMCG. Combined with residual energy cost pressure, this could create a compounded profitability squeeze independent of the geopolitical trajectory.

-

Currency reversal risk: The rupee's recent strengthening is partly a function of improved risk sentiment following the truce. Any reversal driven by global risk-off dynamics or a deterioration in India's current account position would re-amplify import cost pressures, partially unwinding the post-truce margin relief.

-

Foreign institutional investor (FII) sensitivity: Equity markets repriced geopolitical risk premiums rapidly following the truce announcement. An equally rapid reversal is structurally possible if escalation resumes, affecting corporate financing costs and capital availability.

In addition, the broader context of global trade war impacts and tariffs and investment markets further complicates the external environment that Indian corporates must navigate alongside these geopolitical energy risks.

Investment Strategy Implications: Positioning for the Post-Truce Environment

The ₹18 lakh crore addition to investor wealth following the truce announcement illustrates a well-documented principle in equity market dynamics: when geopolitical risk premiums are elevated, they tend to be priced indiscriminately across sectors, creating valuation dislocations in businesses with strong underlying fundamentals.

For investors assessing sector rotation opportunities in the post-truce environment, a sound investment strategy and the margin recovery trajectory suggest the following framework:

Sectors warranting constructive positioning:

- OMCs, given the under-recovery normalisation trajectory and crude price tailwind

- Fertiliser manufacturers, benefiting from gas supply restoration and production predictability

- Infrastructure-linked plays, supported by government spending anchors and improving project economics

Sectors requiring close monitoring:

- Airlines, where structural fuel cost vulnerability persists beyond the near-term truce relief

- Ceramics, where lagged gas cost absorption creates near-term earnings risk that forward price improvements do not immediately resolve

- Specialty chemicals, where feedstock volatility remains only partially resolved

The broader signal for Indian equity investors is that geopolitical risk in West Asia should now be treated as a persistent, cyclically recurring variable in portfolio construction rather than an episodic event. Furthermore, Fortune India's coverage of the CRISIL assessment highlights that while credit quality has remained resilient, the speed of both the market sell-off during conflict escalation and the subsequent ₹18 lakh crore recovery underscores the asymmetric return potential available to investors who maintain a framework for identifying geopolitically mispriced assets.

Frequently Asked Questions: West Asia Truce and India Inc Profitability

What is the projected impact of the West Asia truce on India Inc's operating margins?

CRISIL Ratings now projects operating margin compression of approximately 100 basis points for the current fiscal year, down from the 200 basis point estimate under the prolonged conflict scenario. Median operating margins are forecast at around 11%, compared to a pre-conflict baseline of approximately 12%.

Which sectors remain most at risk despite the improved outlook?

Airlines and ceramics carry the highest residual risk. Airlines face elevated fuel costs and currency headwinds, while ceramics manufacturers are absorbing lagged gas costs from the conflict period. Specialty chemicals, flexible packaging, and polyester textiles also face continued margin pressure from input cost volatility.

How does lower crude oil pricing benefit India's broader economy?

Lower crude prices reduce India's import bill, ease domestic inflationary pressure, support rupee stability, and preserve fiscal capacity, with the combined GDP-level benefit estimated at approximately 0.5-0.8% of annual output.

What could reverse the profitability recovery?

The primary risks are a breakdown of the US-Iran diplomatic arrangement restoring conflict-level crude prices, a weak monsoon compressing rural demand, and renewed currency depreciation amplifying import costs. These risks are independent and could compound if they materialise simultaneously.

How many sectors now face meaningful margin pressure?

Under the revised post-truce scenario, approximately 10 sectors are expected to face meaningful margin pressure, down from 22 sectors under the prolonged conflict model.

A Reprieve With Conditions: What India Inc Should Do With This Window

The West Asia truce impact on India Inc profitability has delivered a material but explicitly conditional improvement in the earnings outlook. The reduction in projected margin compression from 200 basis points to 100 basis points represents genuine relief, but the distribution of that relief is sharply uneven across sectors, and the underlying diplomatic arrangement remains fragile by design.

The most strategically important response for Indian corporates is to treat this as an operational window rather than a resolution. Companies in energy-intensive sectors that survived the conflict period without meaningful hedging infrastructure now have an opportunity to build those capabilities before the next cycle of geopolitical tension. Supply chain diversification, multi-scenario financial modelling, and structured energy procurement strategies are no longer optional refinements for large industrials but baseline risk management requirements in an era where West Asian geopolitics can reshape Indian corporate margins within a single quarter.

For investors, the episode reinforces the value of maintaining analytical frameworks that price geopolitical risk premiums systematically rather than reactively. The businesses best positioned to generate long-term returns through these cycles will be those with structural cost hedges, flexible procurement, and boards that treat energy geopolitics as a core strategic variable rather than an exogenous shock.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking projections regarding corporate margins, crude oil prices, and sectoral performance are based on publicly available CRISIL Ratings assessments as reported by ETEnergyWorld and are subject to material uncertainty. Investors should conduct independent due diligence before making any investment decisions.

Want to Stay Ahead of the Next Major Market-Moving Discovery?

While India Inc navigates the ripple effects of West Asian geopolitical risk on corporate margins, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into actionable investment insights — explore historic discoveries and their returns to see how early positioning can generate exceptional outcomes, and begin your 14-day free trial today to secure a market-leading edge.