Australia's commitment to securing domestic steel production capabilities has reached a critical juncture as global supply chains undergo fundamental restructuring. The Whyalla magnetite expansion represents a strategic positioning of magnetite resources within this transformation, reflecting broader economic forces that extend far beyond traditional mining operations, encompassing energy transition preparedness and industrial policy coordination through the Australia iron ore industry.

The economic rationale for prioritising magnetite development stems from recognition that steel self-sufficiency requires coordinated intervention beyond market mechanisms alone. This approach positions Australia at the intersection of decarbonisation trends and industrial competitiveness, creating foundations for resilient supply chains that can withstand future disruptions.

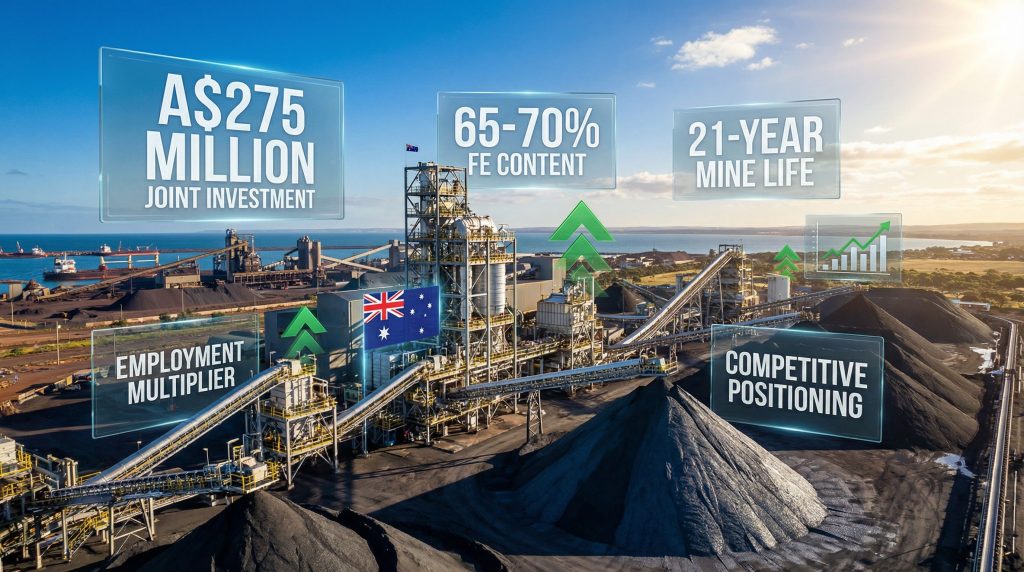

Investment Scale and Structure

The A$275 million joint government investment in the Whyalla magnetite expansion represents equal cost-sharing between Commonwealth and South Australian governments, with each jurisdiction contributing A$137.5 million. An initial A$20 million loan component supports early works operations, demonstrating government confidence in project viability while maintaining fiscal accountability through repayment mechanisms.

This funding structure provides several strategic advantages:

- Risk mitigation through diversified government backing

- Political sustainability across electoral cycles

- Operational flexibility during market volatility

- Investment confidence for potential private buyers

Furthermore, the project aligns with broader critical minerals energy transition objectives, positioning Australia to benefit from global decarbonisation trends.

When big ASX news breaks, our subscribers know first

Resource Security and Export Diversification

By prioritising magnetite over traditional hematite extraction, Australia positions itself to capture higher value-added segments of the steel supply chain rather than remaining solely a raw material exporter. This strategic shift aligns with global trends where countries increasingly prioritise domestic processing capabilities and downstream value creation.

However, the mining industry evolution demonstrates that technological advancement must accompany resource development to maintain competitive advantages in international markets.

What Makes Magnetite Essential for Future Steel Production?

Technical Advantages of Magnetite Processing

Magnetite's superior iron content compared to hematite creates significant processing efficiencies that translate into economic advantages across the steel production value chain. The mineral's magnetic properties enable more precise beneficiation, reducing waste streams and improving concentrate quality for downstream applications.

The technical specifications demonstrate magnetite's processing advantages:

- Higher iron content concentration enables more efficient extraction

- Magnetic separation properties reduce processing complexity

- Superior concentrate quality suitable for advanced steelmaking processes

- Reduced environmental impact through minimised waste generation

Direct Reduction Compatibility

Unlike blast furnace processes that rely heavily on coking coal, magnetite concentrates excel in direct reduction iron (DRI) applications. This compatibility becomes crucial as steel producers transition toward hydrogen-based reduction processes, positioning magnetite as the preferred feedstock for low-emissions steel production.

The Whyalla magnetite expansion project expects to support production of up to 2.5 million tonnes annually once MEP1 becomes operational, with an estimated mine life of 21 years. This production capacity enables both domestic steel production security and export market participation simultaneously, as confirmed by the Australian government's backing of Whyalla's future expansion.

Infrastructure Advantages

Whyalla Steelworks possesses existing infrastructure including concentration plants, pelletising facilities, and port access that provides immediate competitive advantages. This infrastructure readiness reduces capital requirements for downstream processing and accelerates time-to-market for magnetite concentrates.

Economic Impact Analysis: Beyond the Initial Investment

Employment Generation and Regional Development

The magnetite expansion creates a foundation for broader industrial development in South Australia's Upper Spencer Gulf region. The project expects to underpin more than 300 direct mining jobs, with additional employment generated through support services and construction activities.

| Impact Category | Direct Employment | Regional Economic Effect |

|---|---|---|

| Mining Operations | 300+ positions | Long-term industrial base |

| Training Programs | 27 apprentices commenced | Skills development pipeline |

| Infrastructure Investment | A$1 million TAFE funding | Educational capacity building |

Performance Improvements and Operational Excellence

Since administration processes began, Whyalla Steelworks has demonstrated measurable operational improvements including best open pour billet casting performance since 1999, record short-term dispatch results, and highest 24-hour production results for specific casting types since infrastructure commissioning.

These performance metrics validate the investment thesis and demonstrate operational capability under proper management structures. The improvements suggest that with adequate funding and strategic direction, the facilities can achieve competitive operational standards.

Regional Economic Transformation

Beyond immediate mining employment, the project enables downstream processing opportunities, equipment manufacturing, and specialised service provision that compounds economic benefits over the projected operational period. The 21-year mine life provides sufficient duration for secondary industry development and regional economic diversification.

How Does Government Funding Structure Support Long-term Viability?

Joint Funding Mechanism Analysis

The equal cost-sharing between Commonwealth and South Australian governments reflects strategic alignment on steel industry preservation while distributing financial and political risks across jurisdictions. This structure provides operational sustainability that extends beyond individual electoral cycles, particularly important given the complex geopolitical mining landscape affecting global steel markets.

The A$20 million loan component for early works demonstrates several important characteristics:

- Accountability mechanisms through repayment obligations

- Performance incentives linked to operational targets

- Risk sharing between public and private sectors

- Revenue potential for government stakeholders

Administrative Oversight and Transition Planning

KordaMentha's appointment as administrator provides professional management during the transition period, ensuring operational continuity while preparing for private sector ownership. This administrative model creates structured oversight mechanisms while maintaining operational flexibility, addressing potential investment risk management concerns for prospective buyers.

Private Sector Interest and Sale Process

The steelworks sale process has attracted five domestic and international industrial groups from more than 70 initial expressions of interest. International delegations from Japan, Korea, India, Vietnam, and Europe have undertaken site visits, with binding bids expected in coming months, demonstrating substantial market confidence in the transformed operations.

What Are the Global Market Implications?

Supply Chain Positioning Strategy

Australia's magnetite expansion occurs amid global supply chain restructuring where countries prioritise domestic processing capabilities over raw material exports. This strategic positioning enables participation in higher value-added steel industry segments while maintaining export flexibility.

Decarbonisation Timeline Alignment

Global steel producers face increasing pressure to reduce carbon emissions, with many targeting net-zero by 2050. The magnetite expansion timeline aligns with this decarbonisation schedule, ensuring Australia can supply essential feedstock as hydrogen-based steel production scales internationally.

The timing advantage becomes critical as:

- Infrastructure development requires multi-year lead times

- Technology transitions create new feedstock requirements

- Supply chain security becomes increasingly prioritised

- Carbon intensity regulations intensify globally

Market Positioning and Competitive Dynamics

High-quality magnetite concentrates command premium prices in international markets, particularly as global steel producers seek cleaner feedstock options. The expansion positions Australia to serve both domestic security requirements and export market opportunities simultaneously.

The next major ASX story will hit our subscribers first

Why Is Timing Critical for This Expansion?

Infrastructure Advantage Window

Existing infrastructure at Whyalla provides immediate competitive advantages that could be lost if expansion is delayed. Alternative supply chains developed by other regions might capture market share while Australia's infrastructure advantages deteriorate without investment.

Technology Transition Pressures

The transition toward hydrogen-based steel production creates new technical requirements for feedstock quality and processing characteristics. Magnetite's compatibility with these emerging technologies provides strategic advantages that may not persist if alternative production methods emerge.

Market Window Considerations

Steel markets remain cyclical, with magnetite demand subject to global economic conditions and trade policy changes. The current alignment of government support, private sector interest, and international market demand creates an opportunity window that may not recur under different economic conditions.

What Risks Could Impact Project Success?

Market Volatility and Demand Sustainability

The 21-year mine life projection assumes sustained demand for high-grade iron ore, dependent on continued steel production growth and decarbonisation adoption rates. Economic downturns or technological breakthroughs could alter these assumptions significantly.

Technology Disruption Scenarios

While magnetite suits current direct reduction technologies, breakthrough innovations in steel production could alter feedstock requirements. The project's success depends on magnetite remaining competitive against alternative production methods or increased recycled steel utilisation.

Operational and Financial Risk Factors

Key risk considerations include:

- Steel market cyclicality and price volatility

- Technology transition uncertainties

- International trade policy changes

- Environmental regulation evolution

- Competition from alternative feedstock sources

Geotechnical drilling currently underway at Iron Duke, approximately 56 kilometres from Whyalla, represents the initial phase of technical validation for the expansion project, as detailed by Iron Duke expansion plans. These investigations provide critical data for mine planning and infrastructure development decisions.

How Will This Impact Australia's Steel Industry Structure?

Vertical Integration Opportunities

The Whyalla magnetite expansion enables potential vertical integration from mining through steel production, creating opportunities for Australian companies to capture more value chain segments. This integration reduces dependence on imported processed materials while strengthening domestic industrial capabilities.

Strategic Asset Classification and Protection

Magnetite resources increasingly qualify as strategic assets given their role in decarbonised steel production. This classification suggests continued government support and protection from foreign acquisition restrictions, providing long-term operational security for investors and stakeholders.

Export Market Development Potential

Beyond domestic steel production requirements, premium magnetite concentrates serve international markets seeking cleaner feedstock alternatives. This dual-market approach provides revenue diversification while maintaining domestic supply security.

What Does This Mean for Investors and Industry Stakeholders?

Investment Thesis Validation

The substantial government backing validates investment assumptions about steel industry modernisation, providing confidence for private capital deployment. The competitive sale process demonstrates market recognition of the asset's strategic value and operational potential.

Long-term Value Creation Framework

The project creates value through multiple channels:

- Resource security for domestic steel production

- Export revenue from premium concentrate sales

- Employment stability supporting regional economies

- Technology positioning for clean steel production

- Infrastructure utilisation maximising existing asset value

Risk-Return Profile Assessment

Government backing reduces political and regulatory risks while the 21-year mine life provides sufficient duration for return on investment. However, market volatility and technology transition uncertainties require careful risk management and operational flexibility.

Disclaimer: This analysis is based on publicly available information and government announcements. Steel industry investments involve inherent risks including market volatility, regulatory changes, and technology transitions. Investors should conduct independent due diligence and consider professional advice before making investment decisions. Future performance projections are subject to numerous variables and uncertainties that may materially affect actual outcomes.

Looking to Capitalise on Major Mining Developments?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities as they emerge from Australia's resource sector. Start your 14-day free trial today and explore how historic discoveries have generated substantial returns for early investors.