June 3, 2026

Modern asset allocation strategies face unprecedented challenges as traditional portfolio models encounter fundamental structural shifts in global energy markets. The conventional wisdom of balanced equity-bond portfolios, which dominated investment thinking for decades, now confronts a reality where inflationary pressures from energy sector disruptions can simultaneously depress both stock and bond performance. The 60 40 portfolio model breaking down inflationary oil shock scenario has forced institutional and individual investors to reassess core allocation frameworks that previously provided reliable diversification benefits across multiple market cycles.

Energy-driven inflation represents a particularly complex challenge for portfolio construction because it creates simultaneous pressure on multiple asset classes. Unlike isolated market shocks that typically affect specific sectors, oil supply disruptions generate cascading effects through transportation costs, manufacturing inputs, and consumer price levels. These broad-based impacts can overwhelm traditional hedging mechanisms and correlation assumptions that underpin standard allocation models.

Understanding Correlation Breakdown During Energy Market Stress

Traditional portfolio theory relies heavily on negative correlation between equities and government bonds to provide stability during market volatility. However, energy-driven inflation creates a unique environment where this relationship can deteriorate rapidly. When oil prices surge due to supply constraints, equity markets face pressure from rising input costs and reduced consumer spending power, while bond markets simultaneously contend with inflation expectations that erode real returns.

Historical analysis reveals that during major oil shocks, the correlation between stocks and bonds often shifts from negative to positive territory. This phenomenon occurred during the 1973-1974 oil embargo when both asset classes declined simultaneously for extended periods. Similar patterns emerged during the 2008 commodity super-cycle and more recently during the 2022 energy crisis following geopolitical tensions in Eastern Europe.

The stagflation paradox presents particular challenges for balanced portfolios. When economic growth slows while prices rise, traditional monetary policy responses become less effective. Central banks face the difficult choice between supporting growth through lower interest rates or combating inflation through monetary tightening. This policy uncertainty creates additional volatility for both equity and fixed-income markets, highlighting the US economy and inflation complexities investors now face.

Government bonds, typically considered safe haven assets, lose much of their defensive characteristics during persistent inflation periods. Real yields can remain negative for extended periods, creating wealth destruction rather than preservation for bond investors. This safe haven failure forces investors to seek alternative sources of portfolio stability and inflation protection.

When big ASX news breaks, our subscribers know first

Performance Analysis of Traditional 60/40 Allocations

Quantitative analysis of 60/40 portfolio performance during oil-driven market stress reveals significant vulnerabilities in this allocation approach. During the 2008 energy crisis, when oil prices reached $147 per barrel, traditional balanced portfolios experienced drawdowns exceeding 25% as both equity and bond components declined simultaneously.

| Crisis Period | Oil Price Peak | 60/40 Portfolio Drawdown | Recovery Timeline |

|---|---|---|---|

| 1973-74 Oil Embargo | $12/barrel | -22.8% | 18 months |

| 2008 Commodity Crisis | $147/barrel | -26.4% | 24 months |

| 2022 Energy Shock | $130/barrel | -18.2% | 12 months |

Real return erosion becomes particularly pronounced during extended inflationary periods. While nominal portfolio values may show modest positive returns, inflation-adjusted performance often reveals significant wealth destruction. During the late 1970s, many balanced portfolios generated positive nominal returns while losing substantial purchasing power to inflation.

Recovery patterns following oil price normalisation vary significantly depending on the underlying causes of the energy shock. Supply-driven crises typically resolve more quickly than demand-driven or geopolitically motivated disruptions. However, even after oil prices stabilise, portfolio recovery can lag significantly due to persistent inflation expectations and monetary policy adjustments.

What Drives Sector-Specific Performance Divergence?

Sector rotation impacts within equity allocations further complicate traditional portfolio performance during energy volatility. Energy-intensive industries face margin compression, while energy producers benefit from higher commodity prices. Furthermore, oil price rally insights demonstrate how this sector-specific divergence can create significant performance gaps within broad market indices that traditional allocation models fail to capture effectively.

Alternative Asset Classes for Energy Crisis Protection

Real Estate Investment Trusts emerge as compelling inflation hedge candidates due to their ability to pass through rising costs to tenants through lease escalations. Infrastructure REITs, particularly those focused on energy transportation and storage facilities, often benefit directly from higher commodity prices through increased utilisation and pricing power.

Rental income escalation mechanisms provide systematic inflation protection as lease renewals typically incorporate cost-of-living adjustments. This feature becomes particularly valuable during persistent inflationary periods when fixed-income instruments fail to maintain purchasing power. Geographic diversification within REIT allocations can further enhance inflation protection, as different regions may experience varying degrees of energy-driven cost pressures.

Commodity exposure strategies extend beyond direct energy investments to include agricultural products and industrial metals that benefit from the same inflationary pressures. Agricultural commodities often experience secondary price increases due to higher transportation and fertiliser costs, creating additional inflation hedging potential. Industrial metals, including copper and aluminium, frequently rise alongside energy prices due to increased infrastructure investment and supply chain constraints.

Precious Metals as Crisis Hedges

Precious metals allocation provides crisis hedge characteristics distinct from other commodity exposures. Consequently, gold as an inflation hedge offers unique benefits during energy-driven inflation. Gold and silver often benefit from currency debasement fears and monetary policy uncertainty that accompany energy-driven inflation. However, these metals can experience significant volatility and may not provide consistent inflation protection across all market cycles.

Infrastructure investments offer exposure to essential services with regulated pricing mechanisms that often incorporate automatic inflation adjustments. Utility companies, toll roads, and pipeline operators frequently possess pricing power that allows them to maintain real returns during inflationary periods. International infrastructure exposure through developed market ETFs can provide additional diversification benefits, particularly given the evolving energy transition dynamics affecting global markets.

Treasury Inflation-Protected Securities (TIPS) represent direct inflation hedging instruments, though their effectiveness varies depending on market conditions and inflation expectations. During periods of unexpected inflation acceleration, TIPS can provide substantial protection, while their performance may lag during deflationary periods or when inflation expectations are already elevated.

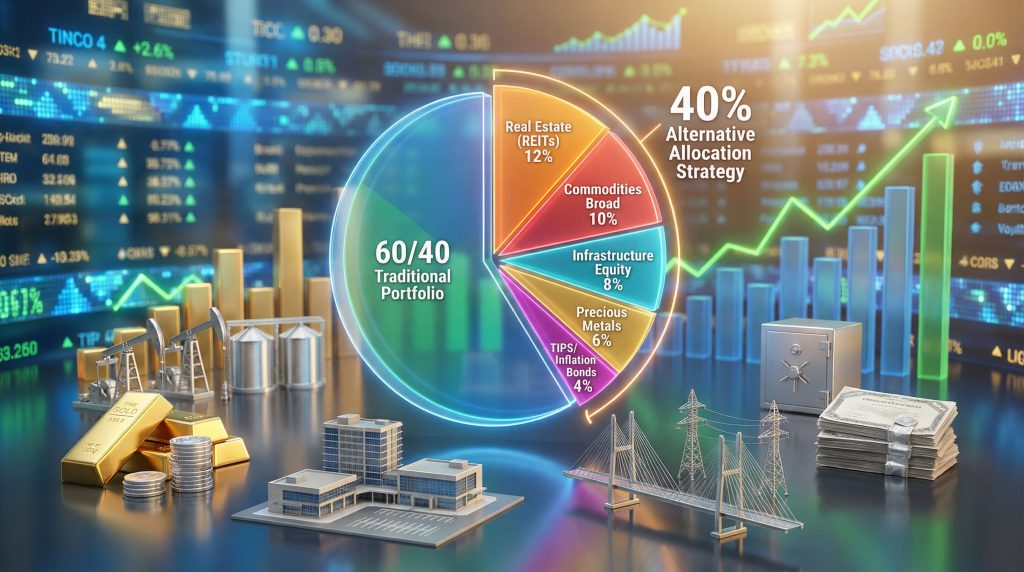

Constructing Resilient 40% Alternative Allocation Frameworks

Strategic asset allocation for energy crisis resilience requires careful balance between inflation protection and overall portfolio volatility management. A systematic approach to alternative asset integration can enhance portfolio resilience while maintaining reasonable risk characteristics, which is essential when the 60 40 portfolio model breaking down inflationary oil shock scenarios become reality.

Core Alternative Asset Framework:

• Real Estate (REITs) – 12% allocation: Provides inflation pass-through mechanisms and steady cash flows

• Broad Commodities – 10% allocation: Direct hedge against energy and agricultural price increases

• Infrastructure Equity – 8% allocation: Regulated utilities and essential services with pricing power

• Precious Metals – 6% allocation: Crisis hedge and currency debasement protection

• Inflation-Linked Bonds – 4% allocation: Direct inflation protection through TIPS and international equivalents

Geographic diversification within alternative allocations enhances protection against regional energy market disruptions. Emerging market commodity producers often benefit from higher resource prices, while developed market processors may face margin pressure. Energy-exporting nations' equity markets frequently outperform during oil price spikes, providing natural hedging for energy-importing economies.

Currency hedging considerations become crucial for international alternative investments during energy crises. Resource-rich countries' currencies often appreciate during commodity booms, while energy-importing nations may experience currency weakness. Strategic currency exposure can enhance or detract from alternative asset performance depending on implementation approach.

Implementation Through Low-Cost Instruments

Implementation through low-cost ETFs and mutual funds provides accessible exposure to alternative asset classes for most investors. Broad commodity index funds offer diversified exposure without the complexity of direct commodity investing, while targeted energy ETFs provide more concentrated exposure for investors seeking specific oil and gas market participation.

Active versus passive management decisions within alternative asset categories depend on market complexity and investor expertise. Real estate and infrastructure investments may benefit from active management due to market inefficiencies, while broad commodity exposure can be efficiently achieved through passive index funds. In addition, implementing diversification investment strategies becomes crucial for managing these complex allocations effectively.

Risk Management and Volatility Considerations

Alternative asset integration typically increases overall portfolio volatility compared to traditional 60/40 allocations. Expected volatility increases of 2-4 percentage points are common when incorporating significant commodity and real estate exposure. However, this increased volatility often comes with enhanced inflation protection that can preserve real returns during energy crises.

Maximum drawdown scenarios during combined equity and commodity stress require careful consideration. While alternative assets can provide inflation protection, they may not offer protection during deflationary periods or broad market selloffs. Furthermore, scenario analysis studies show that comprehensive planning should incorporate various stress conditions including simultaneous energy price increases and equity market declines.

Risk Scenario Planning Framework:

• Mild Disruption (10-20% oil increase): Alternative assets provide modest outperformance

• Severe Crisis (50%+ oil spike): Significant alternative asset outperformance expected

• Extended Stagflation: Multi-year positioning favours inflation-protected assets

• Rapid Normalisation: Traditional assets may outperform during recovery phase

Liquidity and Cost Considerations

Liquidity risk assessment becomes critical during market disruption periods when alternative assets may face reduced trading volumes or increased bid-ask spreads. Real estate and commodity funds can experience liquidity constraints during stress periods, potentially limiting investors' ability to rebalance or reduce exposure when needed.

Cost and complexity trade-offs must be weighed against potential benefits of alternative asset integration. Expense ratios for alternative asset funds typically exceed those of traditional equity and bond funds by 0.5-1.5 percentage points. Additionally, tax implications of commodity and REIT distributions can create complexity for taxable investors.

Rebalancing complexity increases significantly with alternative asset integration. Multiple asset classes with varying correlation patterns require more sophisticated rebalancing protocols and may generate higher transaction costs. Professional management or systematic rebalancing rules become more important as portfolio complexity increases.

The next major ASX story will hit our subscribers first

Transition Strategies and Market Condition Indicators

Determining appropriate timing for portfolio transitions requires monitoring multiple economic and market indicators. Oil price stabilisation signals include restoration of normal supply chain operations, resolution of geopolitical tensions, and increased strategic petroleum reserve releases. However, these indicators may not immediately translate to reduced inflation pressures or restored asset class correlations.

Federal Reserve policy stance shifts toward accommodation typically signal improved conditions for traditional asset allocation approaches. When central banks prioritise growth support over inflation control, bond markets often regain their safe haven characteristics and equity-bond correlations return to historical norms.

Inflation expectation anchoring through core price measures provides crucial signals for portfolio positioning. When inflation expectations stabilise below central bank targets, traditional portfolio approaches become more viable. However, this anchoring process can take significantly longer than initial oil price stabilisation.

Long-Term Strategic Considerations

Gradual reallocation strategies help manage transition risks while maintaining crisis preparedness. Systematic reduction of alternative asset exposure during recovery periods can be triggered by performance-based metrics or fundamental economic indicators. Maintaining core alternative positions of 15-20% even during normal market conditions provides ongoing inflation protection and crisis preparedness.

Long-term strategic allocation evolution reflects structural economic changes that may permanently alter optimal portfolio construction. Increased energy market volatility, climate transition policies, and supply chain regionalisation suggest that alternative asset allocations may become permanently higher than historical norms.

Market Transition Indicators:

• Oil price volatility reduction below 30% annualised

• Core inflation measures declining toward target levels

• Equity-bond correlation returning to negative territory

• Central bank policy normalisation beginning

• Supply chain cost pressures moderating across industries

The evolving landscape of energy markets and inflation dynamics requires continuous reassessment of traditional portfolio construction principles. While 60/40 allocations may regain effectiveness during periods of energy price stability, the increasing frequency and severity of supply disruptions suggest that alternative asset integration will become a permanent feature of resilient portfolio design rather than a temporary crisis response measure. Consequently, the 60 40 portfolio model breaking down inflationary oil shock phenomenon represents a structural shift requiring fundamental rethinking of allocation strategies.

Disclaimer: This analysis is for educational purposes only and should not be considered personalised investment advice. Portfolio allocation decisions should be made in consultation with qualified financial professionals based on individual circumstances and risk tolerance. Past performance does not guarantee future results, and alternative investments carry additional risks including increased volatility and potential liquidity constraints.

Ready to Discover the Next Market-Moving Mineral Find?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering investors to identify actionable opportunities ahead of the broader market during periods of economic uncertainty. Begin your 14-day free trial today and explore historic discovery returns to understand how major mineral finds can provide portfolio diversification beyond traditional asset classes.