June 5, 2026

Vertical Integration Over Export Arbitrage: Understanding the Gulf State Playbook in African Copper

The global race to secure copper supply chains has entered a new phase, one where the most strategically sophisticated investors are no longer simply buying mines and shipping concentrate to the highest bidder. Across the Central African Copperbelt, a fundamental shift is underway in how resource-rich nations and their mining partners think about value creation. The old extractive model, in which semi-processed ore leaves a country as quickly as possible, is being challenged by a longer-horizon thesis rooted in refining infrastructure, sovereign alignment, and patient capital deployment.

Nowhere is this shift more visible than in Zambia, where the Abu Dhabi IRH Zambian copper concentrate waiver has been declined three consecutive times by International Resources Holding (IRH), each time receiving the largest single quota on offer. Understanding why requires unpacking both the mechanics of Zambia's export duty framework and the broader investment logic driving Gulf state resource acquisition across sub-Saharan Africa.

When big ASX news breaks, our subscribers know first

How Zambia's Copper Concentrate Export Duty System Functions

The 10% Export Duty and Its Policy Purpose

Zambia maintains a 10% export duty on copper concentrate as a structural incentive designed to keep semi-processed ore flowing into domestic smelters rather than overseas refineries. The underlying policy rationale is straightforward: by making it more expensive to export raw concentrate, the government encourages miners to add value within Zambia's borders, supporting local employment, industrial capacity, and tax revenues derived from refined metal production.

Copper concentrate is not finished copper. It is a partially processed material typically containing between 25% and 35% copper by weight, alongside iron sulphides, silica, and trace amounts of other metals. The concentrate must undergo smelting and subsequent electrorefining before it becomes the copper cathode used in wiring, electric motors, and energy transition infrastructure. Furthermore, exporting concentrate essentially exports the processing margin alongside the raw material, which is precisely what Zambia's duty framework is designed to prevent.

When Waivers Are Triggered and How They Operate

The waiver mechanism is not a permanent policy shift or a liberalisation signal. It functions as a temporary pressure-release valve activated specifically when domestic smelting capacity falls below the threshold required to absorb all available concentrate production.

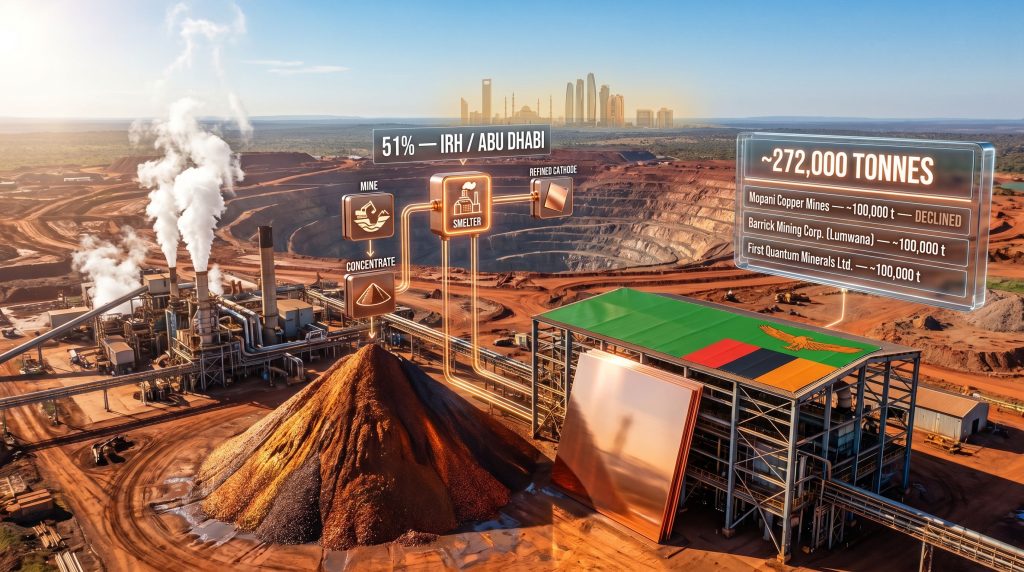

The June 2, 2026 suspension covers approximately 272,000 tonnes of copper concentrate eligible for export over a three-month window, routed through state-owned Industrial Resources Ltd. (IRL), which holds a metals-trading arrangement with commodity trading house Mercuria Energy Group. This state intermediation layer is deliberate: it gives the Zambian government visibility into export volumes, participation in trading revenues, and a mechanism to enforce quota compliance.

The proximate trigger for this latest round was the announcement by Konkola Copper Mines on May 29, 2026, that its smelter had entered a planned 60-day maintenance and repair shutdown. With one of Zambia's four operational copper smelters offline, the system lacked the aggregate throughput capacity to process all concentrate being produced nationally, creating the conditions that justify temporary export relief. According to reporting from Mining.com, Zambia has extended its duty-free copper concentrate export waiver to address these ongoing smelter outages.

The waiver system reveals an often-overlooked structural vulnerability in Zambia's domestic processing model: the country's smelting network has limited redundancy, meaning a single planned shutdown can ripple through the entire regulatory framework, triggering export duty suspensions and activating state trading mechanisms.

IRH, Mopani, and the Abu Dhabi Copper Strategy

Who Controls Mopani and Why It Matters

International Resources Holding (IRH) acquired a 51% controlling stake in Mopani Copper Mines in early 2024, taking on an asset with deep operational history in Zambia's Copperbelt. IRH is part of a large conglomerate structure connected to UAE national security leadership, reflecting the geopolitical dimension that increasingly underpins Gulf state natural resource investment.

The Mopani acquisition was not an isolated transaction. It sits within a broader pattern of Abu Dhabi-linked entities acquiring strategic positions in copper, cobalt, lithium, and rare earth assets across Africa, Central Asia, and Latin America. The common thread is not simply financial return optimisation. It is commodity access, supply chain positioning, and long-term industrial relevance in a world increasingly structured around electrification and energy transition infrastructure. Consequently, understanding these copper price drivers becomes essential for contextualising IRH's positioning.

The Three Consecutive Waiver Rejections: A Snapshot

| Waiver Round | Mopani Allocation | Mopani Decision |

|---|---|---|

| July 2025 | ~100,000 tonnes | Declined |

| March 2026 | ~100,000 tonnes | Declined |

| June 2026 | ~100,000 tonnes | Declined |

The consistency of this pattern is analytically significant. Three identical decisions across nearly 12 months cannot be attributed to operational coincidence or short-term logistics. It reflects a fixed strategic posture: Mopani's priority is to smelt all available concentrate through its own processing facility, not to monetise export quota access. Bloomberg has confirmed that IRH's Zambia copper unit declined to take up the concentrate export waiver, underscoring the deliberateness of this strategy.

How the June 2026 Allocation Compared Across Operators

| Mining Entity | Approximate Allocation | Export Decision |

|---|---|---|

| Mopani Copper Mines (IRH) | ~100,000 tonnes | Declined |

| Barrick Mining Corp. (Lumwana) | Combined ~100,000 tonnes | Eligible for export |

| First Quantum Minerals Ltd. | Combined ~100,000 tonnes | Eligible for export |

| Total Waiver Volume | ~272,000 tonnes | Via IRL / Mercuria trading route |

The allocation structure is itself revealing. Mopani's single-entity quota is equal to the combined allocation of Zambia's two other largest mining operators, Barrick's Lumwana mine and First Quantum's operations. This concentration reflects Mopani's scale as a dominant concentrate producer within the national system, and it raises legitimate questions about whether the waiver methodology should be recalibrated when the largest recipient consistently declines to use its allocation.

The Economics of Choosing Smelting Over Export Revenue

Why Domestic Processing Captures More Value

The financial logic behind Mopani's decision is not opaque. Exporting copper concentrate at current market prices means selling a product that is roughly 25-35% copper by mass at a per-tonne price that reflects the buyer's smelting discount. Refiners and smelters purchasing concentrate apply treatment charges and refining charges (known in the industry as TC/RCs) that effectively transfer a portion of the value creation from the seller to the processor.

By smelting concentrate domestically and producing refined copper cathode, Mopani captures that processing margin internally. The value-add between concentrate and cathode is not trivial. Copper cathode commands a significant premium over the equivalent copper content in concentrate, and the margin has historically widened during periods of tight global refined copper supply. In addition, the copper supply crunch adds further urgency to vertical integration decisions of this kind.

For a vertically integrated operator, the decision to smelt rather than export is not purely about current spot prices. It is about controlling the full value chain from ore to refined metal, which provides both superior margin capture and insulation from the TC/RC volatility that can periodically erode concentrate seller economics.

TC/RC Dynamics: A Lesser-Known Driver of the Export-or-Smelt Decision

Treatment charges and refining charges are the fees paid by miners to smelters for processing concentrate into refined metal. These charges are benchmarked annually through negotiations between major miners and smelters, historically led by Japanese smelters and Chinese processors. When TC/RCs are high, it is relatively more expensive to sell concentrate to third-party smelters. When they are low, as has been the case during periods of global concentrate tightness, miners with their own smelting capacity are in an advantaged position.

For IRH and Mopani, owning the smelter transforms the TC/RC question entirely. Rather than paying external smelters to process their concentrate, Mopani internalises those charges. In a copper market that faces structural supply constraints over the medium term, this vertical integration premium is likely to grow rather than diminish.

Gulf State Resource Strategy: Patient Capital and Long-Term Positioning

Why Abu Dhabi Invests in Copper Processing, Not Just Mining

The Abu Dhabi IRH Zambian copper concentrate waiver decision is a window into a much larger strategic picture. Gulf sovereign investment vehicles have historically allocated capital toward financial assets and real estate. However, the current generation of investment is markedly different, oriented toward physical commodity control at a time when energy transition demand is creating structural deficits in copper, cobalt, and other critical materials.

IRH's approach in Zambia demonstrates several characteristics of the Gulf state resource acquisition model:

- Long investment horizons that tolerate near-term foregone revenue in exchange for long-term asset control

- Vertical integration priorities that seek to own processing capacity alongside extraction rights

- Sovereign alignment strategies that build political relationships with host governments by supporting national industrialisation goals

- Supply chain security as a primary objective, not merely financial return maximisation

The Geopolitical Layer: Zambia at the Intersection of Competing Interests

Zambia's position within the Central African Copperbelt makes it one of the most contested resource geographies on the planet. The country shares the Copperbelt geology with the Democratic Republic of Congo, which together host some of the world's highest-grade copper and cobalt deposits. Chinese, Western, and Gulf state entities are all competing for influence over this corridor's production and processing output.

IRH's commitment to domestic smelting and its consistent refusal to use export waivers strengthens its relationship with the Zambian government, which has made local beneficiation a cornerstone of its mining policy agenda. This alignment mirrors the broader global copper trade strategy being pursued by other sovereign-linked entities seeking to embed themselves within host nation industrial policy. Furthermore, this creates the conditions for expanded operational licences, future acquisition opportunities, and preferential treatment in policy discussions.

Structural Gaps in Zambia's Processing Infrastructure

The Smelter Redundancy Problem

Zambia copper production ambitions are constrained by the fact that the country currently operates only four active copper smelters. When one enters planned maintenance, the system's aggregate processing capacity drops materially, triggering the waiver mechanism. This pattern reveals that Zambia's domestic processing infrastructure, while functional, lacks the redundancy needed to absorb normal operational disruptions without resorting to export relief.

A more resilient smelting network would allow Zambia to maintain its no-export-duty stance even when individual smelters cycle through maintenance periods. Building that resilience requires either:

- Investment in additional smelting capacity to provide buffer throughput

- Improved coordination of planned maintenance schedules across operators to prevent simultaneous downtime

- Temporary concentrate storage infrastructure that allows stockpiles to be managed without export pressure

Until these structural gaps are addressed, the waiver mechanism will continue to be activated periodically, creating a tension between Zambia's long-term beneficiation ambitions and its short-term processing constraints.

What Mopani's Strategy Signals for the Future of African Copper Policy

The broader implication of IRH's approach in Zambia extends beyond a single company's operational decisions. If a major mining operator consistently demonstrates that domestic smelting is both economically viable and strategically preferable to concentrate export, it strengthens the policy case for other African copper producers to invest in similar processing infrastructure.

This creates a potential template for resource nationalism that is not adversarial toward foreign investors but rather aligned with them, provided those investors share the host government's beneficiation ambitions. The Abu Dhabi IRH Zambian copper concentrate waiver model, moreover, may prove more durable and replicable than extractive investment structures that treat the export of raw materials as the default outcome. For investors seeking to understand the implications, exploring copper investment strategies tailored to this evolving landscape is increasingly worthwhile.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Zambia Copper Concentrate Export Waivers

What is a copper concentrate export waiver in Zambia?

A copper concentrate export waiver is a temporary government measure suspending Zambia's standard 10% export duty on semi-processed copper ore. It allows mining companies to export concentrate that would otherwise be required to flow through domestic smelters. Waivers are issued when national smelting capacity is constrained, typically due to planned or unplanned maintenance shutdowns at one or more of Zambia's four operational smelters.

Why did Mopani Copper Mines decline its export allocation three times?

Mopani's consistent position across July 2025, March 2026, and June 2026 is that its operational priority is to direct all available concentrate into its own smelter. This reflects a deliberate vertical integration strategy that captures additional processing value in-country rather than selling semi-processed material at a discount to overseas refiners.

What are treatment charges and refining charges in copper mining?

TC/RCs are fees paid by copper concentrate sellers to smelters for processing ore into refined metal. They represent a transfer of value from the miner to the processor. Miners with their own smelting operations internalise these charges, improving overall margin capture and reducing exposure to TC/RC market volatility.

Who controls Mopani Copper Mines?

Abu Dhabi's International Resources Holding holds a 51% controlling stake in Mopani Copper Mines, acquired in early 2024. Zambian government-linked entities hold the remaining interest.

How large is the June 2026 waiver and who triggered it?

The June 2, 2026 waiver covers approximately 272,000 tonnes of copper concentrate eligible for export over three months. Konkola Copper Mines announced on May 29, 2026 that its smelter had entered a planned 60-day maintenance shutdown, reducing Zambia's aggregate domestic processing capacity and triggering the waiver conditions under the country's mining policy framework.

This article contains forward-looking analysis and references to investment strategies and market dynamics. Readers should note that commodity markets, corporate strategies, and regulatory frameworks are subject to change. Nothing in this article constitutes financial or investment advice. Independent verification of all data points and professional advice should be sought before making investment decisions.

Want To Stay Ahead of Significant ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex mineral data into actionable insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns or start your 14-day free trial today to position yourself ahead of the market.