July 21, 2026

When Spare Capacity Becomes a Strategic Liability Inside OPEC

Within the architecture of global oil cartels, spare production capacity is typically considered a strategic asset. For most OPEC members, the mere existence of unused barrels represents bargaining power, a cushion against oil price volatility, and a tool for disciplining rival producers. But for the United Arab Emirates, that same spare capacity had quietly transformed into something else entirely: a source of compounding economic frustration.

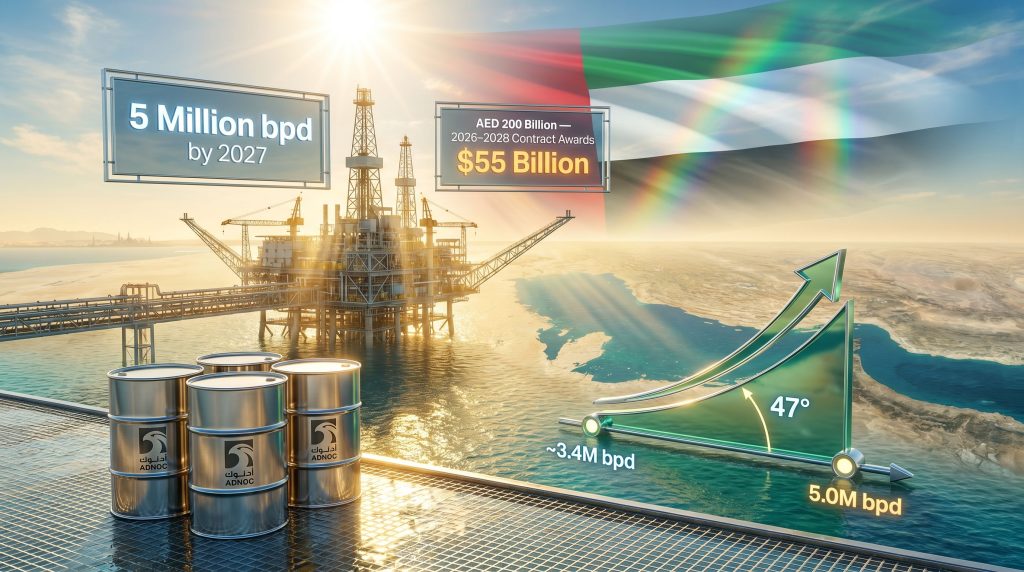

The UAE spent years methodically expanding ADNOC's upstream infrastructure, targeting a production ceiling of 5 million barrels per day by 2027, only to find itself repeatedly constrained by collective output quotas that failed to account for Abu Dhabi's unique investment cycle. As the gap between what ADNOC could produce and what OPEC+ allowed it to produce widened, the economic calculus of cartel membership grew increasingly difficult to justify. By May 1, 2026, that calculus had reached its conclusion.

The UAE's formal departure from OPEC, effective that date, ended a membership relationship stretching back to 1967 via Abu Dhabi, roughly 59 years of participation in the world's most influential production alliance. What followed within days was not coincidental. ADNOC accelerates $55 billion investment after UAE OPEC exit, announcing plans to deploy up to $55 billion (AED 200 billion) in upstream and downstream project awards between 2026 and 2028, confirming what analysts had long suspected: the exit was the precondition, and the investment acceleration was always the intended consequence.

According to Wood Mackenzie, the UAE holds a disproportionately large share of unused productive capacity relative to other OPEC members, and without quota restrictions, that capacity can be put to commercial use in a way previously unavailable to Abu Dhabi.

Understanding how OPEC shapes oil markets helps contextualise why the UAE's departure carries such strategic weight. Furthermore, OPEC production decisions have long constrained members with significant spare capacity, making departure an increasingly rational option for producers like Abu Dhabi.

When big ASX news breaks, our subscribers know first

The $55 Billion Plan: Acceleration, Not Invention

A critical distinction often lost in the coverage of ADNOC's investment announcement is that the $55 billion is not new money. It represents an accelerated deployment phase within a pre-existing capital framework. ADNOC's broader $150 billion five-year capital expenditure programme, spanning 2026 to 2030, was formally approved in November 2025. The $55 billion tranche covers project awards specifically scheduled between 2026 and 2028, now fast-tracked following the removal of OPEC+ quota constraints.

Understanding this distinction matters for investors and market observers alike. ADNOC is not responding to the OPEC exit by inventing new capital commitments. It is unlocking the execution velocity of a plan already embedded in Abu Dhabi's sovereign energy strategy. The sequencing was deliberate: establish the regulatory freedom first, then mobilise the capital infrastructure at pace.

How Significant Is the Capacity Target?

The scale of the capacity expansion target is considerable. ADNOC currently operates at approximately 3.4 million barrels per day (bpd). The 2027 production target of 5 million bpd represents an incremental addition of roughly 1.6 million bpd, equivalent to a 47% increase over the pre-programme baseline. To contextualise that figure, 1.6 million bpd is roughly equivalent to the entire current production output of several mid-tier OPEC members.

| Capital Programme Metric | Detail |

|---|---|

| Near-term contract awards (2026–2028) | Up to $55 billion (AED 200 billion) |

| Broader five-year capex programme | $150 billion (2026–2030) |

| Capex plan approval date | November 2025 |

| Current production capacity | ~3.4 million bpd |

| 2027 production capacity target | 5.0 million bpd |

| Incremental expansion | ~1.6 million bpd (+47%) |

| Investment categories | Upstream and downstream operations |

The $55 billion programme spans both upstream capacity expansion and downstream integration, covering refining infrastructure, petrochemical operations, and manufacturing. This dual-axis investment approach reflects a broader institutional philosophy: ADNOC does not view energy production and economic diversification as separate mandates. They are, in Abu Dhabi's strategic framework, the same project.

Bloomberg's coverage of ADNOC's post-OPEC acceleration reinforces this framing, noting that the capital deployment is firmly tied to the removal of quota constraints rather than representing a reactive policy shift.

The Make It With ADNOC Forum and the Industrial Policy Dimension

ADNOC chose the inaugural Make it With ADNOC Forum in Abu Dhabi as the formal announcement platform for the accelerated investment programme. The timing was pointed. The forum was designed to provide supply chain participants with direct visibility into ADNOC's project pipeline while simultaneously showcasing domestic manufacturing opportunities under the company's "Local+" procurement initiative.

Sultan Al Jaber, ADNOC Group's chief executive and UAE Minister of Industry and Advanced Technology, framed the programme explicitly around a dual mandate: meeting the world's rising energy requirements while simultaneously building out the UAE's domestic industrial and manufacturing capacity. In Al Jaber's articulation, local manufacturing is not a secondary consideration but a structural pillar of ADNOC's procurement, construction, and project execution strategies.

What Does the "Local+" Initiative Mean in Practice?

This framing carries significant analytical weight. It positions ADNOC's capital deployment not merely as an upstream volume play but as a national economic development instrument, one that generates industrial multiplier effects within the UAE economy rather than simply importing foreign contractor services. The "Local+" initiative prioritises UAE-manufactured products and domestically based suppliers, creating a feedback loop between energy investment and industrial capability-building.

ADNOC's capital programme is simultaneously an energy infrastructure expansion and a deliberate effort to deepen the UAE's manufacturing base, a dual mandate that distinguishes Abu Dhabi's approach from most other national oil company investment strategies globally.

The National News reports that ADNOC will award AED 200 billion in contracts to support these supply chain ambitions, with local manufacturing forming a core pillar of the execution strategy.

Spare Capacity, Fiscal Resilience, and Why the UAE Could Afford to Leave

Not every OPEC member could walk away from the cartel and survive the consequences. The strategic logic of the UAE's departure rests on two structural advantages that most peers cannot replicate.

First: spare production capacity. The UAE and Saudi Arabia are among the very few producers globally, not just within OPEC, that maintained meaningful volumes of unused productive capacity prior to the current regional disruption environment. For most OPEC members, quota allocations sit at or near actual production capability. Quota restrictions therefore impose limited opportunity cost on producers already operating at capacity limits.

For the UAE, however, each barrel of quota-imposed restriction represented a direct, quantifiable revenue foregone against infrastructure already built and ready to produce. Consequently, the incentive to depart grew stronger with every investment cycle.

Second: fiscal resilience. Wood Mackenzie analysts noted that the UAE operates with significantly lower fiscal oil price breakeven levels compared to most regional peers. This structural advantage means Abu Dhabi can sustain a period of lower oil prices without the same degree of budgetary stress that would constrain higher-breakeven producers. In practical terms, the UAE can afford to prioritise production volume over price maximisation in a way that countries like Venezuela, Nigeria, or even Russia cannot.

These two conditions, spare capacity plus fiscal resilience, created the economic foundation for departure. Without both, the price coordination benefits of OPEC membership would likely still outweigh the production freedom gained by leaving.

The Hormuz Paradox: Freedom Without an Exit Route

Despite the regulatory liberation achieved through the OPEC exit, ADNOC faces an immediate operational constraint that no policy decision can resolve. The Strait of Hormuz, through which approximately 20% of global oil supplies transit, remains closed amid the broader US-Iran-Israel conflict. This closure effectively neutralises near-term production increases across all Gulf producers, regardless of their OPEC+ status.

The paradox is stark: ADNOC now has the capital, the institutional mandate, and the regulatory freedom to expand output at pace, but the physical export pathway remains blocked. Infrastructure attacks targeting gas processing facilities, refineries, and LNG liquefaction sites across the Gulf have further curtailed both upstream and downstream operational capacity in the short term.

| Time Horizon | Primary Constraint | ADNOC Strategic Position |

|---|---|---|

| Immediate (2026) | Strait of Hormuz closure | Output curtailed regardless of quota status |

| Medium-term (2026–2027) | Infrastructure recovery | Project awards and supply chain mobilisation accelerating |

| Long-term (2027–2030) | Global demand and price dynamics | Full 5 million bpd capacity deployment targeted |

This temporal structure is important for interpreting ADNOC's investment acceleration correctly. The $55 billion programme is not designed to immediately flood markets with new barrels. It is a medium-to-long-term positioning exercise, using the current disruption period to advance project awards, mobilise supply chains, and build capacity so that ADNOC is ready to scale rapidly once export routes normalise.

The Hormuz disruption has simultaneously driven Brent crude above $114 per barrel following Iranian strikes on UAE port infrastructure, embedding a significant supply shock premium into global oil prices. Analysts have identified $125 per barrel as a potential threshold beyond which global demand destruction and recessionary risks materially increase. Monitoring current crude price trends and geopolitical oil price risks remains essential for understanding ADNOC's long-term revenue modelling assumptions.

OPEC Cohesion Under Stress: What the UAE's Exit Signals for the Alliance

The geopolitical implications of the UAE's departure extend well beyond Abu Dhabi's own production strategy. As the fourth-largest OPEC producer prior to exit, the UAE's decision to prioritise sovereign production independence over collective price coordination raises a question the remaining alliance members cannot easily avoid: if one of the most financially resilient and capacity-rich members concluded that membership no longer served its interests, what does that imply for the long-term durability of OPEC+ as an institution?

Kazakhstan's decision to remain within OPEC+ following the UAE's exit provides a near-term data point suggesting the alliance is not in immediate collapse. Russia publicly dismissed concerns about a price war following the UAE's departure, adopting a posture of strategic indifference. However, neither response resolves the underlying tension between the collective output discipline that OPEC+ demands and the individual production ambitions of capacity-rich members.

Does the UAE's Departure Set a Precedent?

JP Morgan noted that the UAE's OPEC exit could attract increased US investment flows into Abu Dhabi's energy sector, introducing a geopolitical dimension that reaches beyond pure production economics. An ADNOC that operates as a sovereign independent producer, aligned with Western capital markets and free from cartel output constraints, represents a meaningfully different strategic partner than an OPEC member operating under collective production discipline.

A less widely discussed dimension of this dynamic involves what might be called the quota credibility problem. OPEC+ production agreements have historically relied on the collective willingness of members to accept below-capacity output in exchange for price support. The UAE's departure signals that when a member's spare capacity is large enough, and its fiscal position strong enough, that bargain breaks down. This precedent may not trigger immediate exits by other members, but it fundamentally alters the negotiating posture of capacity-rich producers within the alliance.

The next major ASX story will hit our subscribers first

Three Scenarios for ADNOC's Market Impact Through 2030

How ADNOC's investment acceleration ultimately reshapes global oil supply architecture depends significantly on variables outside Abu Dhabi's direct control. Three broad scenarios frame the range of outcomes.

Scenario 1: Rapid Normalisation. The Strait of Hormuz reopens within six to twelve months, ADNOC executes its 2026 to 2028 project awards on schedule, and the UAE adds more than one million bpd of new capacity to global markets by late 2028. Under this scenario, ADNOC's expansion meaningfully pressures OPEC+ price coordination capability and potentially incentivises additional capacity-rich members to reassess their own membership calculus.

Scenario 2: Prolonged Disruption. The Hormuz closure extends through 2027, delaying production ramp-up despite continued project mobilisation. ADNOC's fiscal resilience allows it to sustain the investment programme without requiring immediate revenue returns, but the capacity addition timeline shifts into 2029 and 2030. Global oil markets remain supply-constrained for longer, keeping prices elevated and partially offsetting the revenue impact of delayed production.

Scenario 3: Structural Market Realignment. The UAE's exit triggers a gradual reassessment among other OPEC+ members with significant spare capacity. The alliance does not collapse, but its effective production discipline weakens materially. Global oil supply architecture begins shifting toward bilateral sovereign-led production strategies rather than collective cartel coordination, a structural shift with decade-long implications for how energy markets are priced and how geopolitical energy relationships are structured.

Key Indicators for Monitoring ADNOC's Strategic Execution

For those tracking the trajectory of ADNOC accelerates $55 billion investment after UAE OPEC exit and its broader market implications, the following indicators offer the most direct signal value:

- Progress and pace of ADNOC's 2026 to 2028 project award announcements and contractor mobilisation timelines

- Status of the Strait of Hormuz closure and the trajectory of conflict resolution between the US, Iran, and Israel

- OPEC+ cohesion signals, particularly whether other capacity-rich members publicly reassess their production strategy in light of the UAE's departure

- UAE fiscal performance under current oil price conditions, especially relative to the country's breakeven thresholds

- Institutional capital flows into UAE energy assets, following JP Morgan's observation that the OPEC exit may enhance Abu Dhabi's appeal to US and Western investors

- Demand-side indicators around the $125 per barrel recession threshold, which represents the key ceiling on ADNOC's revenue assumptions in a prolonged high-price environment

The convergence of a 59-year OPEC membership ending, a $150 billion capital programme entering its most intensive execution phase, and a regional conflict simultaneously constraining short-term output creates one of the most analytically complex moments in Gulf energy history. ADNOC's bet is ultimately a long-duration one: that the physical, regulatory, and financial infrastructure being built today will translate into durable production advantage once the immediate disruption environment resolves.

Whether that bet pays off depends less on what happens in Abu Dhabi and more on what happens in the Strait of Hormuz.

This article is intended for informational purposes only and does not constitute financial or investment advice. Oil market projections, scenario analyses, and analyst assessments referenced herein involve inherent uncertainty. Readers should conduct independent research before making any investment decisions. Price data and geopolitical developments referenced reflect conditions as reported at the time of publication.

Want To Capitalise On The Next Major Energy Or Mineral Discovery Before The Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data into actionable investment insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional market returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.