June 18, 2026

The Architecture of a New Global Gas Power: Understanding the Strategic Logic Behind ADNOC's US Investment Push

There is a particular kind of infrastructure investment that does not simply seek returns on capital. It seeks to reshape the conditions under which returns are generated across an entire commodity system. The liquefied natural gas industry has historically been structured around discrete, bilateral relationships: upstream producers sell to midstream processors, who sell to terminal operators, who sell to utility buyers. Each handoff extracts a margin. Each link in the chain represents a dependency.

What Abu Dhabi National Oil Company is now assembling through its international investment vehicle XRG represents something categorically different from the transactional model that has defined Gulf energy exports for decades. The ADNOC investment in US gas business is not a portfolio allocation. It is an architectural project: the deliberate construction of an end-to-end gas enterprise spanning American production fields, transmission infrastructure, liquefaction capacity, and potentially regasification terminals in destination markets. Understanding why this matters requires examining the mechanics of the LNG value chain itself, the structural forces driving demand, and the strategic logic that makes the United States the optimal geography for this ambition.

When big ASX news breaks, our subscribers know first

XRG: The Investment Engine Powering Abu Dhabi's Global Gas Vision

From Regional Producer to Global Gas Integrator

For most of its history, ADNOC operated as a classic resource-rich national oil company: extract hydrocarbons, monetise them through long-term offtake contracts, and deliver commodity revenues to the Abu Dhabi state. That model was effective in an era when Gulf producers controlled the supply side of a price-inelastic energy market. The strategic environment has changed fundamentally.

Global LNG trade now exceeds 420 million tonnes per annum in total market capacity, with the United States Gulf Coast emerging as one of the dominant export hubs following the shale revolution (International Gas Union, World LNG Report, 2025). The LNG supply outlook points to the centre of gravity in the gas industry having shifted from the Middle East to North America. For a national oil company with ambitions beyond its home basin, the response is not to compete with this shift but to participate in it.

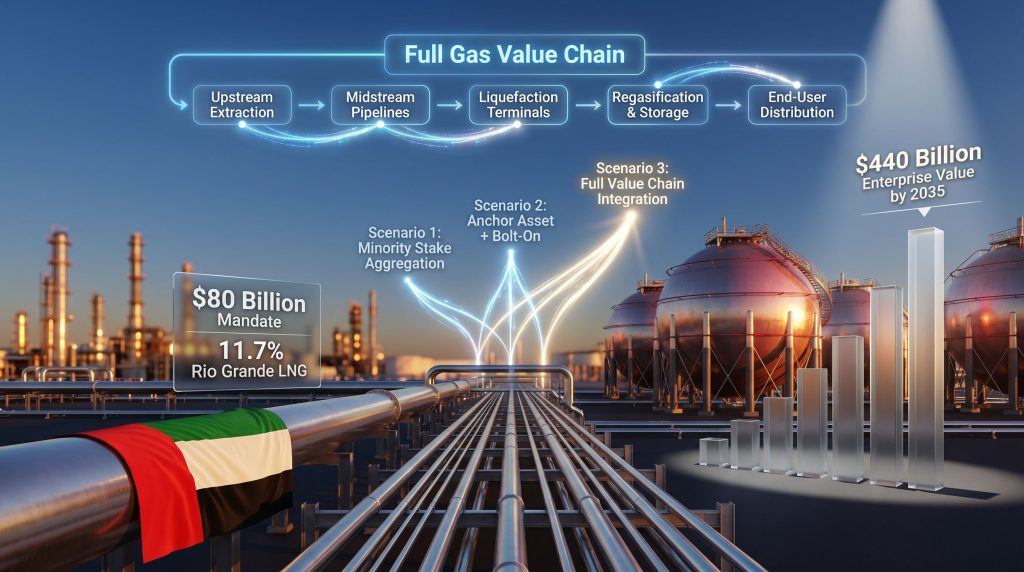

XRG was established as ADNOC's dedicated overseas investment arm precisely to enable this repositioning. It carries an $80 billion mandate focused on gas, LNG, chemicals, and lower-carbon energy solutions, with the United States identified as a priority deployment market. Critically, XRG's chief investment officer Nameer Siddiqui has described the strategy as one of diversifying commodity exposure by operating across the entire gas value chain rather than concentrating exposure at any single node, as reported by the Financial Times (April 2026) and cited via Zawya.

The $80 Billion Mandate and What It Actually Buys

An $80 billion capital mandate is large enough to acquire controlling positions in multiple major energy companies. Deployed across a value chain build-out rather than a single corporate acquisition, it is large enough to assemble something considerably more durable: a vertically integrated gas business that captures economics at every stage of the commodity's journey from reservoir to end user.

To understand the financial architecture this creates, consider the cost structure of each value chain segment:

| Value Chain Stage | Typical Capital Intensity | Return Profile | Strategic Benefit for XRG |

|---|---|---|---|

| Upstream Extraction | $5-8M per thousand boe/d | Commodity-linked, cyclical | Feedstock cost control and price hedging |

| Midstream Pipelines | $200-500M per large processing plant | Regulated or contracted, 5-8% WACC | Predictable cash flows independent of spot pricing |

| Liquefaction Terminals | $1-3B per mtpa of capacity | Scale-dependent, long-term contracted | Access to global seaborne LNG markets |

| Regasification & Storage | $300-800M per terminal | Fixed-fee or regulated | Geographic arbitrage and end-market control |

| End-User Distribution | Lower capex, higher volume | 8-15% above wholesale | Long-term offtake security and demand visibility |

Sources: McKinsey & Company, "The Future of LNG," 2024; Rystad Energy, "Global LNG Capex and Economics," 2025; U.S. Energy Information Administration, 2025

The logic of stacking ownership across these stages is not merely additive. When a single entity controls feedstock costs, processing costs, liquefaction costs, and export pricing, it possesses natural hedges against commodity price volatility that no single-stage participant can replicate. During the 2020 LNG market downturn, Asian spot prices fell below $3 per million British thermal units, a level that made standalone export terminal economics deeply problematic. Integrated operators with low-cost upstream positions were insulated from the worst of that margin compression in ways their non-integrated counterparts were not.

What Vertical Integration Actually Means in the US Gas Value Chain

Breaking Down the Full Gas Value Chain: From Wellhead to End User

The phrase vertical integration is used loosely in energy commentary but its operational meaning is precise. In the US natural gas context, full integration spans five distinct infrastructure categories, each governed by separate regulatory frameworks and each presenting distinct capital and operational requirements.

-

Upstream extraction involves acquiring production rights, drilling wells, and producing raw natural gas from reservoirs. In the United States, this is regulated at the state level by agencies such as the Texas Railroad Commission and the Louisiana Department of Natural Resources, with federal oversight applying to leases on federal lands. The US produced approximately 1,362 billion cubic metres of natural gas in 2024, maintaining its position as the world's largest producer (U.S. Energy Information Administration, April 2026).

-

Midstream infrastructure includes the approximately 305,000 miles of onshore natural gas transmission and distribution pipelines that constitute the world's largest integrated gas network (EIA, 2025). Midstream assets are subject to Federal Energy Regulatory Commission rate-of-return regulation under the Natural Gas Act Section 7(c), creating relatively predictable, utility-like return profiles.

-

Liquefaction terminals convert pipeline gas into the dense liquid form required for ocean shipping. Capital costs run at approximately $1-3 billion per million tonnes per annum of capacity, with facilities operating at 85% or above capacity utilisation achieving unit costs of roughly $8-12 per tonne. Below 70% utilisation, those unit costs rise toward $14-18 per tonne as fixed cost absorption deteriorates (Wood Mackenzie, Global LNG Cost Curve, 2024).

-

Regasification and storage on the receiving end involves converting LNG back to gaseous form for injection into destination market distribution networks, at capital costs of $300-800 million per terminal node.

-

End-user distribution captures the final-mile margin between wholesale and retail or industrial pricing, typically 8-15% above wholesale benchmark pricing with volume providing scale economics.

Why Full-Chain Ownership Transforms Investment Economics

Cheniere Energy's development of the Sabine Pass LNG export facility in Louisiana provides the closest domestic reference point for what integrated margin capture looks like in practice. By combining contracted input gas costs with long-term export offtake agreements, Cheniere constructed a business largely insulated from spot market volatility. Royal Dutch Shell's broader integrated LNG supply chain, which spans Gulf of Mexico production through export partnership positions and regasification interests in multiple destination markets, demonstrates the same logic at the major IOC scale (Shell, Integrated LNG Strategy, 2024 Annual Report).

The 29-Deal Pipeline: What Portfolio Construction Looks Like in Practice

XRG is simultaneously reviewing 29 potential transactions across the US gas value chain, as confirmed by reporting in the Financial Times (April 2026, via Zawya). This number deserves careful interpretation. Typical private equity or infrastructure fund deal pipelines include 50-150 opportunities to identify 3-5 investable platforms. A curated review of 29 transactions suggests a targeted, relationship-driven deal sourcing process rather than broad-market scanning. It implies that XRG has already pre-identified the asset categories and counterparty profiles it wants and is now conducting structured diligence across a defined opportunity set.

"This is not deal-by-deal opportunism. A simultaneous multi-asset review of this scale reflects a platform-building logic: assembling complementary assets across sequential value chain stages rather than accumulating isolated positions. The goal is systemic margin capture, not individual transaction returns."

Existing US Stakes Reveal the Acquisition Playbook

XRG's current US portfolio already demonstrates a deliberate progression from minority participation toward more comprehensive value chain coverage.

| Asset | Partner | XRG Stake | Asset Type | Strategic Role |

|---|---|---|---|---|

| Rio Grande LNG Phase 1 | NextDecade | 11.7% | LNG Liquefaction | Export infrastructure access |

| Baytown H₂/Ammonia Plant | ExxonMobil | 35% | Low-Carbon Chemicals | Transition-era commodity diversification |

| Texas DAC Project | Occidental (1PointFive) | TBD (Framework) | Carbon Removal | Carbon balance and ESG optionality |

| US Natural Gas Fields | TBD | Under Review | Upstream Production | Feedstock security and cost base |

Rio Grande LNG: A Foothold at the Export Node

NextDecade's Rio Grande LNG facility on the Texas Gulf Coast is designed to deliver approximately 8.4 million tonnes per annum of capacity in Phase 1, scaling toward 12.7 mtpa across both phases. XRG's 11.7% stake in Phase 1 positions it at one of the most strategically significant liquefaction nodes on the US Gulf Coast without requiring majority control or operational responsibility. Based on comparable LNG project valuations, this stake represents indirect exposure to an asset enterprise value in the range of $15-18 billion (Wood Mackenzie, Global LNG FID Analysis, 2024).

Baytown: Bridging Conventional Gas and Low-Carbon Chemistry

The 35% stake in ExxonMobil's Baytown hydrogen and ammonia production facility in Texas is arguably the most structurally interesting position in XRG's current US portfolio. The facility is designed to produce blue hydrogen using natural gas feedstock combined with carbon capture, alongside low-carbon ammonia for industrial markets. This is not simply an energy transition gesture. Ammonia is a globally traded commodity with established shipping infrastructure, and blue hydrogen produced from US gas at competitive input costs has potential to become a meaningful export product to European and Asian industrial buyers seeking to decarbonise hard-to-abate sectors.

The Direct Air Capture Option: Carbon Removal as Strategic Infrastructure

The framework agreement covering potential investment in Occidental's 1PointFive direct air capture project in Texas, with designed capacity to permanently remove up to 500,000 tonnes of CO₂ annually, represents a third strategic logic: the ability to generate and monetise carbon removal credits that offset the emissions profile of XRG's gas and LNG operations. This positions XRG within the emerging US carbon removal infrastructure landscape before that market achieves commodity-scale pricing.

The Macro Demand Forces Making US Gas Infrastructure Attractive

Structural LNG Demand Drivers Through 2035

Three independent demand forces are converging to support sustained investment in US LNG export infrastructure:

-

Energy security diversification across European buyers following the disruption of traditional pipeline supply routes has created structural demand for long-term LNG supply contracts from stable, rule-of-law jurisdictions.

-

Industrial decarbonisation pathways in Asia and Europe continue to rely on natural gas as a transition bridge fuel, particularly in power generation and industrial heat applications where renewable alternatives remain technically or economically limited.

-

Emerging market electrification requires flexible, dispatchable power generation capacity. Natural gas-fired peaker plants and combined-cycle facilities provide the baseload flexibility that intermittent renewables alone cannot deliver at the current technology cost curves.

The Data Centre Energy Equation

One of the less commonly discussed drivers in XRG's strategic calculus is the direct relationship between artificial intelligence infrastructure buildout and US natural gas demand. US data centre electricity consumption is projected to reach 9-17% of total US electricity generation by 2030, compared to approximately 3-4% in 2023, according to the International Energy Agency (Data Centres and Energy, 2024) and the Lawrence Berkeley National Laboratory (Data Centre Energy Usage Report, 2024).

Natural gas-fired generation provides the always-on, weather-independent baseload capacity that hyperscale data centre operators require. This creates a domestic US demand pull for gas production and midstream infrastructure that operates independently of export market dynamics. For XRG, upstream and midstream assets serving this domestic demand profile carry a demand floor that reduces commodity cycle risk.

"The intersection of AI infrastructure growth and natural gas demand represents one of the more underappreciated structural tailwinds for US gas investment. Data centre operators are not price-sensitive on energy in the same way industrial customers are; uptime is the primary constraint, which supports premium pricing for reliable gas-fired generation capacity."

Geopolitical Context: Capital Deployment Under Pressure

Why Regional Uncertainty Strengthens the US Investment Case

XRG's reaffirmation of its commitment to deploy tens of billions of dollars into the US energy value chain, characterised by Siddiqui as unwavering despite regional geopolitical headwinds (as reported by Zawya citing the Financial Times, April 2026), functions as more than a financial statement. It is a credibility signal directed at potential US joint venture partners, co-investors, and regulatory bodies.

For US energy companies seeking long-term anchor investors in capital-intensive LNG export projects, a counterparty that demonstrates conviction under adverse conditions is more valuable than one that recalibrates commitments when geopolitical circumstances shift. The publicly stated commitment to deploy at scale, conditioned only on adequate return thresholds rather than geopolitical calm, positions XRG as a structurally committed partner. Furthermore, the US-China trade war impacts on global energy flows have reinforced the appeal of stable, rules-based investment environments like the United States for sovereign capital allocators.

The US market's appeal in this context is partly a function of its relative regulatory stability compared to other geographies where XRG might deploy comparable capital. Federal regulatory frameworks, FERC oversight of infrastructure, and the established legal architecture around foreign investment in energy assets create a predictable operating environment that emerging market deployments cannot match.

The next major ASX story will hit our subscribers first

Scenario Modelling: Three Pathways for XRG's US Build-Out

The 29-deal pipeline review creates optionality across meaningfully different strategic outcomes. Three scenarios bracket the realistic range:

Scenario 1: Minority Stake Aggregation (Low Disruption, High Optionality)

XRG acquires sub-50% positions across multiple value chain nodes, preserving operational flexibility while building market knowledge and regulatory relationships. This path involves lower capital concentration per deal, reduced CFIUS complexity, and maximum reversibility. The trade-off is limited pricing power in offtake negotiations and dependence on operating partners for operational decisions.

Scenario 2: Anchor Asset Acquisition with Bolt-On Strategy (Moderate Disruption)

XRG acquires one or two controlling upstream or liquefaction positions and uses these as platforms to layer complementary midstream and downstream stakes. This mirrors the approach of mid-major integrated LNG operators. Capital concentration risk is higher, and FERC and CFIUS scrutiny of foreign control in energy infrastructure would intensify, but margin capture and strategic leverage improve materially.

Scenario 3: Full Value Chain Integration (High Disruption, Maximum Strategic Leverage)

XRG assembles a vertically integrated US gas business spanning production through end-user delivery, mirroring the model of major international oil companies operating domestically. Execution complexity across a 29-deal process, regulatory review timelines, and the capital requirements of operating control at multiple chain stages represent the principal constraints on this pathway. The strategic upside, however, is transformative: Abu Dhabi would effectively operate as a global gas major with a US production and export base, not merely a financial co-investor.

Risk Factors and Structural Constraints

Any realistic assessment of the ADNOC investment in US gas business must account for the constraints that could limit or reshape the build-out:

-

CFIUS review applies to foreign acquisitions of US businesses involved in critical infrastructure, including energy transmission and production assets. Majority control positions in midstream or upstream assets would trigger the most intensive review processes, potentially extending deal timelines by 12-18 months and requiring structural remedies.

-

Return threshold discipline is explicit in Siddiqui's framing: deployment is conditional on adequate return expectations, not unconditional. Consequently, natural gas price trends directly affect acquisition valuations for upstream assets, and the gap between seller price expectations and buyer valuation creates negotiation friction in any market environment.

-

Execution risk across a 29-deal review pipeline is substantial. Managing simultaneous diligence processes across upstream, midstream, and export infrastructure requires specialised legal, technical, and financial teams with deep US market knowledge. Integration of acquired assets into a coherent operational system adds a second layer of execution complexity.

-

Commodity price exposure runs in both directions: higher gas prices inflate the cost of upstream acquisition but improve downstream export economics. Lower prices reduce acquisition costs but compress export margins. Integrated operators can partially hedge this symmetry, but cannot eliminate it entirely.

How ADNOC's US Strategy Compares to Other National Oil Company Models

| National Oil Company | US Market Strategy | Primary Asset Focus | Integration Depth |

|---|---|---|---|

| ADNOC / XRG | Full value chain build-out | Gas, LNG, Chemicals, Carbon | High (vertical integration target) |

| QatarEnergy | Equity LNG partnerships | LNG liquefaction offtake | Moderate (upstream + export) |

| Saudi Aramco | Downstream refining and chemicals | Refinery stakes, petrochemicals | High (downstream-focused) |

QatarEnergy's North Field Expansion strategy, which targeted an incremental 64 mtpa of LNG capacity through partnerships with ExxonMobil, ConocoPhillips, and Shell, demonstrates a partnership-intensive model that preserves upstream control while leveraging international operator expertise. Saudi Aramco's acquisition of a 50% stake in Shell's Motiva refining joint venture in 2017 for approximately $13.1 billion established downstream integration precedent in the US market but focused on refining rather than gas (Reuters, 2017).

What differentiates XRG's approach is the simultaneous pursuit of gas, chemicals, and carbon removal within a single investment mandate. This portfolio architecture is designed to capture value across multiple energy system states: high-carbon conventional gas markets, transitional low-carbon chemistry markets, and emerging carbon removal infrastructure. No other national oil company is currently pursuing this precise combination at comparable scale in the US market. In addition, the North West Shelf extension debate in Australia illustrates how national energy asset decisions increasingly intersect with global LNG investment strategies of this kind.

In the broader context, the broader energy price trends across oil and gas markets will play a significant role in shaping which of XRG's three strategic scenarios ultimately materialises and at what pace capital is deployed.

Frequently Asked Questions: ADNOC's US Gas Strategy

What is XRG and how does it relate to ADNOC?

XRG is ADNOC's dedicated international investment vehicle, operating with an $80 billion mandate focused on gas, LNG, chemicals, and lower-carbon energy solutions globally. It functions as the offshore capital deployment arm for ADNOC's international ambitions, distinct from ADNOC's core UAE-based hydrocarbon operations.

How much is ADNOC planning to invest in the US gas sector?

ADNOC has publicly committed to deploying tens of billions of dollars into the US energy value chain through XRG, conditioned on meeting adequate return thresholds. A broader UAE energy investment target of $440 billion in enterprise value by 2035 frames the scale of the long-term capital deployment ambition, though this figure represents a projection rather than a confirmed commitment.

What types of US gas assets is XRG targeting?

XRG's stated strategy covers the full gas value chain: upstream production fields, midstream pipelines and processing plants, liquefaction export terminals, and potentially regasification facilities and end-user distribution networks in destination countries.

Does ADNOC already have investments in US energy infrastructure?

Yes. According to ADNOC's own reporting, XRG currently holds an 11.7% stake in Phase 1 of NextDecade's Rio Grande LNG export facility in Texas, a 35% stake in ExxonMobil's Baytown low-carbon hydrogen and ammonia facility, and a framework agreement for potential investment in Occidental's 1PointFive direct air capture project in Texas.

What regulatory approvals would large-scale US energy acquisitions require?

Acquisitions of US energy infrastructure by foreign entities are subject to CFIUS national security review, FERC regulatory approval for midstream assets, Department of Energy export authorisation for LNG terminals, and state-level environmental and operational permitting. Majority control positions in critical energy infrastructure trigger the most intensive review processes.

How does the data centre energy boom factor into ADNOC's gas strategy?

US data centre electricity consumption is projected to reach 9-17% of total US generation by 2030, with natural gas-fired generation providing the reliable baseload capacity that AI infrastructure operators require. This creates domestic US demand for gas production and midstream infrastructure that supports asset valuations independently of export market conditions.

Key Takeaways

-

XRG's 29-deal review pipeline signals a portfolio construction approach rather than isolated transaction opportunism, aimed at assembling complementary assets across sequential value chain stages.

-

Existing stakes in Rio Grande LNG, Baytown hydrogen, and the Occidental DAC framework represent proof-of-concept positions establishing regulatory familiarity and partnership credibility ahead of larger-scale deployment.

-

The full vertical integration thesis creates natural hedges against commodity price volatility that single-stage LNG participants cannot replicate, as demonstrated by integrated operators during the 2020 spot price collapse.

-

Data centre energy demand growth adds a domestic US demand floor to upstream and midstream asset valuations, reducing commodity cycle risk for integrated US gas portfolio holders.

-

The commitment to deploy at scale, conditioned on return thresholds rather than geopolitical stability, positions XRG as a structurally committed partner in a US energy market actively seeking long-term anchor investors for capital-intensive export infrastructure.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements, projections, and scenario analyses involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent research before making any investment decisions.

For ongoing coverage of Gulf energy investment and LNG infrastructure developments, Zawya's Energy section at zawya.com provides regular reporting on ADNOC, XRG, and related developments across the regional and global energy sector.

Want to Know When the Next Major Energy Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral and energy discoveries before the broader market reacts — the same intelligence that has helped investors capitalise on transformative finds like those by De Grey Mining and WA1 Resources. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to secure a market-leading edge.