May 9, 2026

Global commodity markets operate within intricate networks where supply chain vulnerabilities can rapidly escalate into systemic disruptions. When production capacity becomes concentrated in geopolitically sensitive regions, the resulting supply-demand imbalances can create extraordinary market conditions that challenge traditional economic models. Furthermore, understanding these dynamics becomes essential for investors navigating periods of heightened uncertainty, particularly when aluminum black hole fears threaten to disrupt established market volatility hedging strategies.

Understanding Supply Chain Vulnerabilities in Critical Metal Markets

Defining the Black Hole Scenario

Market analysts have identified a phenomenon known as the "aluminum black hole" where supply deficits reach critical thresholds beyond normal market correction mechanisms. This condition emerges when production disruptions exceed the market's ability to substitute demand or implement alternative sourcing strategies within reasonable timeframes.

JPMorgan Chase & Co. issued a formal warning characterising current aluminum market conditions as approaching this black hole scenario, representing a serious and prolonged supply deficit affecting global market participants. Moreover, the banking institution's assessment highlights how structural supply constraints can overwhelm traditional market equilibrium forces.

Key statistical indicators demonstrate the severity of current market conditions:

• Aluminum prices have surged more than 15% since geopolitical conflicts began

• The metal has reached four-year price highs approaching previous record levels

• Market movements have occurred despite ongoing supply chain uncertainty

The "black hole" terminology reflects conditions where normal price discovery mechanisms become distorted by physical supply realities rather than speculative trading patterns. Unlike typical commodity cycles, this scenario involves both immediate production losses and infrastructure damage extending recovery timelines beyond conventional market expectations.

The Perfect Storm of Market Conditions

Current aluminum market dynamics reflect a convergence of multiple risk factors creating amplified volatility patterns. In addition, the concentration of global production in specific geographic regions has created vulnerability points that extend beyond simple supply-demand calculations.

According to analyst Gao Yin from Shuohe Asset Management, traders are actively positioning ahead of anticipated aluminum supply disruptions, engaging in front-running behaviour based on certainty of physical supply gaps rather than speculative geopolitical outcomes. This positioning strategy indicates professional market participants recognise structural supply constraints as independent variables from political resolution timelines.

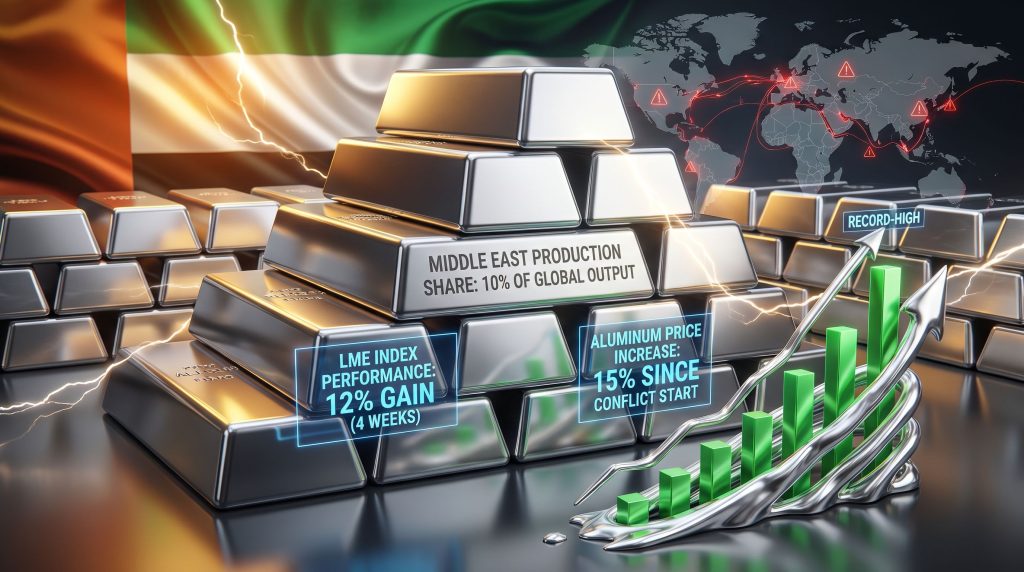

The Middle East accounts for approximately 10% of global aluminum output, representing a critical concentration risk despite not constituting a dominant production share. Recent targeting of two major smelting facilities in Abu Dhabi and Bahrain has created immediate production capacity losses while simultaneously demonstrating infrastructure vulnerability across the region.

Energy-intensive aluminum production requirements create additional complexity layers during crisis periods. Consequently, smelting operations cannot be quickly restarted due to technical complexity and integrated supply chain dependencies, extending disruption impacts beyond initial damage assessments.

When big ASX news breaks, our subscribers know first

How Geopolitical Events Reshape Industrial Metal Supply Chains

Regional Production Concentration Analysis

Geographic concentration of aluminum production creates systemic vulnerabilities that extend far beyond the mathematical percentage of global output affected. The targeting of specific smelting facilities demonstrates how concentrated infrastructure can become strategic targets during geopolitical conflicts.

The two facilities struck in Abu Dhabi and Bahrain represent more than simple production capacity. These operations function as critical nodes within integrated supply networks, where disruption creates cascading effects across multiple market participants and geographic regions.

Infrastructure interdependencies compound the immediate impact of facility damage. Modern aluminum smelting requires:

• Continuous power supply for maintaining furnace temperatures

• Specialised logistics networks for raw material delivery

• Integrated export facilities for finished product distribution

• Technical expertise for complex production processes

When any component within this integrated system becomes compromised, the entire production chain experiences reduced efficiency or complete shutdown. This systemic vulnerability explains why relatively small geographic production shares can create disproportionate market disruptions.

Transportation Chokepoint Vulnerabilities

The Strait of Hormuz represents a critical transportation artery for Middle Eastern metal exports, currently subject to a dual blockade maintained by both the United States and Iran. This shipping lane closure creates immediate logistical complications extending beyond affected production facilities.

Transportation disruptions amplify production losses through multiple mechanisms:

• Physical prevention of finished product export from operational facilities

• Increased shipping costs for alternative routing arrangements

• Extended delivery timelines for international market participants

• Inventory accumulation at production sites lacking export capacity

The combination of reduced production capacity and blocked export channels creates a compound supply disruption affecting global aluminum availability. Even facilities continuing operations cannot deliver products to international markets, effectively removing their output from available supply calculations.

Alternative routing options exist but involve significant cost increases and extended transit times. However, shipping companies must navigate around affected regions, utilising longer routes that increase fuel consumption, insurance premiums, and delivery schedules.

What Drives the LME Index to Record Highs During Crisis Periods?

Index Composition and Weighting Analysis

The London Metal Exchange Index achieved an all-time peak closing price, driven primarily by aluminum's dominant weighting within the six-metal gauge structure. This mathematical relationship demonstrates how concentrated exposure to specific metals can amplify individual commodity movements into broader index performance.

Statistical performance indicators reveal the magnitude of current market movements:

| Metric | Performance Data | Market Impact |

|---|---|---|

| LME Index Rally | 12% gain over 4 weeks | All-time high achieved |

| Aluminum Price Increase | 15% since conflict start | Four-year high levels |

| Copper Price Recovery | 11% four-week gain | Near January record levels |

| Combined Index Weight | 75% copper + aluminum | Dual-metal rally driving gains |

Aluminum maintains the largest weighting within the LME gauge, creating mathematical leverage where price movements in the underlying metal produce amplified effects on overall index performance. For instance, this weighting structure explains how aluminum's 15% price increase, combined with copper's 11% recovery, generates the 12% index rally.

Furthermore, the index composition creates feedback loops during crisis periods where individual metal performance influences investor sentiment across the entire complex. Nickel, zinc, and tin have also experienced rallies during the current period, though none have reached individual all-time highs.

Price Discovery Mechanisms During Market Stress

Price discovery during supply crises operates through different mechanisms than normal market conditions. Current aluminum pricing reflects the integration of multiple information sources including physical supply assessments, forward demand projections, and risk premium calculations.

Professional traders documented by market analysts are trading on certainty of aluminum supply disruptions rather than speculating on geopolitical resolution outcomes. This approach indicates that price discovery mechanisms are incorporating physical supply realities independent of political negotiation progress.

Market participants differentiate between three distinct elements affecting pricing:

• Immediate supply disruption (assessed as certain)

• Geopolitical resolution timeline (considered uncertain)

• Underlying demand conditions (showing improvement signals)

This three-factor analysis framework allows institutional investors to position based on known physical constraints while maintaining flexibility regarding uncertain political developments. The approach explains why aluminum black hole fears have maintained elevated price levels despite ongoing diplomatic efforts.

The LMEX Metals Index gained 3.6% during the week through Thursday, reflecting concentrated trading activity focused on supply-constrained metals. However, most metals declined on Friday, with aluminum falling 0.4% to $3,629 per ton, demonstrating ongoing volatility patterns characteristic of crisis-driven markets.

Investment Flow Patterns During Commodity Crises

Institutional investment strategies during commodity supply crises reveal sophisticated approaches to managing uncertainty while capitalising on known disruptions. Mercuria Energy Group and BMO Capital Markets issued forecasts predicting copper would surpass January record highs, citing Chinese buyer reactivation and anticipated White House tariff decisions.

These institutional positions reflect differentiated analysis between metals experiencing different fundamental drivers:

• Aluminum positioning based on supply constraint certainty

• Copper positioning driven by demand recovery expectations

• Combined exposure capturing both supply disruption and demand improvement

Chinese buyers returning to copper markets provides a demand-side indicator influencing institutional positioning strategies. This reactivation signals to professional investors that underlying consumption conditions support higher prices beyond immediate crisis premiums.

Front-running behaviour documented by analysts represents strategic positioning ahead of anticipated supply gaps rather than speculative trading on geopolitical outcomes. This distinction indicates sophisticated risk assessment techniques employed by institutional market participants during periods when aluminum black hole fears dominate market sentiment.

Professional positioning strategies appear to incorporate scenario analysis where different outcomes require different portfolio allocations. The certainty of supply disruption allows for higher conviction positioning compared to uncertain geopolitical resolution timelines.

How Do Energy Costs Amplify Metal Market Volatility?

Aluminum's Energy-Intensive Production Profile

Aluminum production represents one of the most energy-intensive industrial processes, consuming substantial electricity for smelting operations. This energy dependency creates additional vulnerability layers during periods of regional instability affecting both production facilities and power generation infrastructure.

The smelting process requires continuous high-temperature operations that cannot be easily interrupted without significant restart costs and technical complications. Power supply interruptions can damage furnace equipment and require extended reconstruction periods before normal production can resume.

Energy cost fluctuations directly impact aluminum production economics through multiple channels:

• Direct electricity consumption for smelting operations

• Natural gas requirements for subsidiary production processes

• Transportation fuel costs for raw material delivery

• Backup power generation during grid instability periods

Regional variations in electricity pricing create competitive advantages or disadvantages for different production facilities. Areas with stable, low-cost power generation maintain operational viability during crisis periods while facilities dependent on volatile energy sources face production curtailment decisions.

Energy Security Implications for Metal Producers

Energy security considerations extend beyond simple cost calculations to encompass supply reliability and infrastructure resilience. Aluminum producers require guaranteed power availability to maintain continuous operations, making energy contract structures critical for operational planning.

Modern smelting facilities implement sophisticated energy management systems including:

• Long-term electricity purchase agreements for cost stability

• Backup power generation capabilities for emergency situations

• Energy storage systems for managing supply fluctuations

• Grid interconnection redundancy for reliability enhancement

Geopolitical conflicts affecting energy infrastructure create compounding effects on metal production beyond direct facility damage. Power grid instability or natural gas supply disruptions can force production curtailments even at undamaged facilities.

The relationship between energy costs and aluminum competitiveness becomes particularly acute during crisis periods when energy premiums increase across affected regions. Consequently, producers with access to stable, low-cost energy sources gain market share while facilities dependent on volatile energy markets face operational challenges.

What Are the Long-Term Structural Changes in Aluminum Markets?

Supply Chain Diversification Imperatives

Current supply disruptions are accelerating long-term structural changes in global aluminum production geography. Industrial companies and governments are reassessing supply chain concentration risks and implementing diversification strategies to reduce dependency on geopolitically sensitive regions.

Investment capital is increasingly flowing toward projects in politically stable jurisdictions, even when production costs may be higher than traditional locations. This risk premium calculation reflects evolving corporate risk management approaches prioritising supply security over marginal cost advantages, particularly as aluminum black hole fears highlight vulnerability concentrations.

Technology transfer requirements for new smelting capacity create additional considerations for supply chain diversification. Establishing new aluminum production requires:

• Specialised technical expertise for facility design and operation

• Substantial capital investment with extended payback periods

• Environmental permitting and regulatory compliance

• Integrated logistics infrastructure for raw material supply

Timeline considerations for bringing new production online typically span multiple years from initial planning through full operational capacity. This extended development period means current supply disruptions will influence market dynamics for extended periods regardless of immediate crisis resolution.

Strategic Reserve Policies and Government Intervention

Government policy responses to aluminum supply vulnerabilities are evolving toward more active intervention in strategic material markets. National stockpiling programmes and trade policy modifications reflect recognition that metal supply security represents a national security consideration.

President Donald Trump made claims regarding Iranian agreement to nuclear terms, though Tehran has not confirmed making such concessions. These statements reflect ongoing diplomatic efforts while market participants continue positioning based on physical supply realities rather than political rhetoric.

Strategic reserve policies under consideration include:

• Government purchasing programmes for critical raw materials supply stockpiles

• Trade agreement modifications prioritising supply chain security

• Investment incentives for domestic production capacity development

• International cooperation frameworks for metal supply security

These policy responses indicate growing recognition that commodity market stability requires active government involvement beyond traditional free market mechanisms during crisis periods. Furthermore, the mining industry evolution reflects these changing dynamics.

How Should Investors Position for Commodity Supply Shocks?

Portfolio Construction During Market Disruption

Current aluminum market conditions provide important case study material for portfolio construction strategies during commodity supply shocks. Successful positioning requires differentiation between crisis-driven price movements and underlying fundamental value creation.

Direct Metal Exposure Strategies:

• Physical metal storage for investors seeking direct commodity exposure

• Exchange-traded funds providing commodity exposure without storage complications

• Futures market positioning for different time horizon objectives

• Options strategies for managing volatility while maintaining upside participation

Statistical performance data demonstrates the magnitude of opportunity and risk during supply disruption periods. Aluminum's 15% price increase since conflict initiation represents substantial return potential while also indicating elevated volatility requiring careful position sizing.

Copper's performance illustrates how related metals can benefit from broad-based institutional positioning during commodity crisis periods. This correlation provides diversification opportunities within metal exposure strategies.

Risk Management Framework for Commodity Investing

Professional risk management during commodity supply shocks requires sophisticated scenario analysis incorporating multiple potential outcomes with different probability assessments and timeline expectations.

Volatility Management Techniques:

• Position sizing based on historical volatility patterns during similar events

• Correlation analysis accounting for breakdown in normal relationships

• Hedge ratio calculations for different exposure levels

• Exit strategy development for various resolution scenarios

The LMEX Metals Index gained 3.6% during one week while experiencing daily fluctuations including a 0.4% aluminum decline on Friday. This volatility pattern illustrates the importance of managing position sizes appropriate for elevated uncertainty periods.

However, scenario planning frameworks should incorporate base case, optimistic, and pessimistic outcomes with specific price targets and timeline expectations. The current situation demonstrates how supply disruption certainty can coexist with resolution timeline uncertainty.

The next major ASX story will hit our subscribers first

What Does Market Recovery Look Like After Supply Shock Resolution?

Historical Pattern Analysis

Previous commodity crisis resolution periods provide instructive patterns for understanding potential recovery scenarios following current aluminum supply disruptions. Price normalisation typically occurs through phases rather than immediate corrections.

Market participants documented by analysts are already positioning for different resolution scenarios while maintaining exposure to ongoing supply constraints. This forward-looking positioning indicates professional expectations for gradual rather than sudden market normalisation.

Recovery Phase Characteristics:

• Initial price volatility during uncertainty periods

• Gradual inventory rebuilding as supply sources become available

• Production restart announcements from previously affected facilities

• Forward curve shape changes reflecting supply expectation modifications

Aluminum prices reaching four-year highs while approaching previous Ukraine invasion levels suggests market participants are incorporating historical precedent analysis into current positioning strategies. Additionally, concerns about US tariffs and inflation add complexity to recovery scenarios.

Investment Implications for Different Recovery Scenarios

Investment strategy during potential recovery periods requires preparation for multiple possible outcomes with different implications for aluminum and related metals pricing. Understanding how tariffs impact markets becomes crucial for positioning strategies.

Gradual Normalisation Pathway:

Sustained elevated pricing would support marginal production facilities and encourage investment in alternative supply sources. This scenario benefits producers with operational flexibility and low-cost production profiles while creating opportunities for supply chain diversification investments.

Rapid Resolution Impact Assessment:

Quick geopolitical resolution could trigger significant price corrections as supply expectations normalise rapidly. However, the infrastructure damage component suggests that even diplomatic resolution will require extended timelines for full production capacity restoration.

Market share redistribution among global producers represents a permanent structural change regardless of crisis resolution timeline. Companies and regions demonstrating supply reliability during crisis periods typically retain competitive advantages in subsequent normal market conditions.

The combination of immediate supply constraints, infrastructure reconstruction requirements, and accelerated diversification efforts suggests aluminum market dynamics will reflect current disruption impacts for extended periods beyond immediate crisis resolution. These aluminum black hole fears fundamentally reshape long-term supply chain strategies across the global metals complex.

Investment Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Commodity markets involve substantial risk including potential loss of principal. Investors should conduct independent research and consult qualified professionals before making investment decisions. Past performance does not guarantee future results, and geopolitical events can create unpredictable market volatility.

Ready to Capitalise on Critical Metal Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market during volatile commodity periods. Understand why major mineral discoveries can lead to substantial market returns by exploring historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of supply shock opportunities.