July 27, 2026

Understanding Modern Aluminum Market Vulnerabilities Through Geopolitical Risk Lens

Global commodity markets face increasing complexity as traditional supply-demand fundamentals intersect with geopolitical instability. The aluminum industry exemplifies this transformation, where physical infrastructure vulnerability creates unprecedented market dynamics distinct from historical commodity cycles. Unlike speculative price movements driven by financial positioning, current aluminum market stress stems from tangible supply chain destruction that cannot be easily reversed through monetary policy or inventory adjustments.

The aluminum supply crisis due to Iran war represents a fundamental shift in how global markets price physical commodity risk. Traditional hedging mechanisms prove inadequate when military conflict directly targets production infrastructure, creating supply inelasticity that financial instruments cannot resolve. This crisis exposes the limitations of globalised supply chains concentrated in geopolitically unstable regions.

Market participants who focused on copper scarcity narratives in early 2026 fundamentally misread the evolving supply risk landscape. While copper accumulated substantial exchange inventory reaching 1.4 million metric tons by March 2026, aluminum faced genuine capacity destruction through coordinated infrastructure attacks. The aluminum futures price of $3,314.25 per ton as of April 2026 reflects this physical reality rather than speculative positioning.

When big ASX news breaks, our subscribers know first

Regional Production Concentration Creates Systemic Supply Chain Fragility

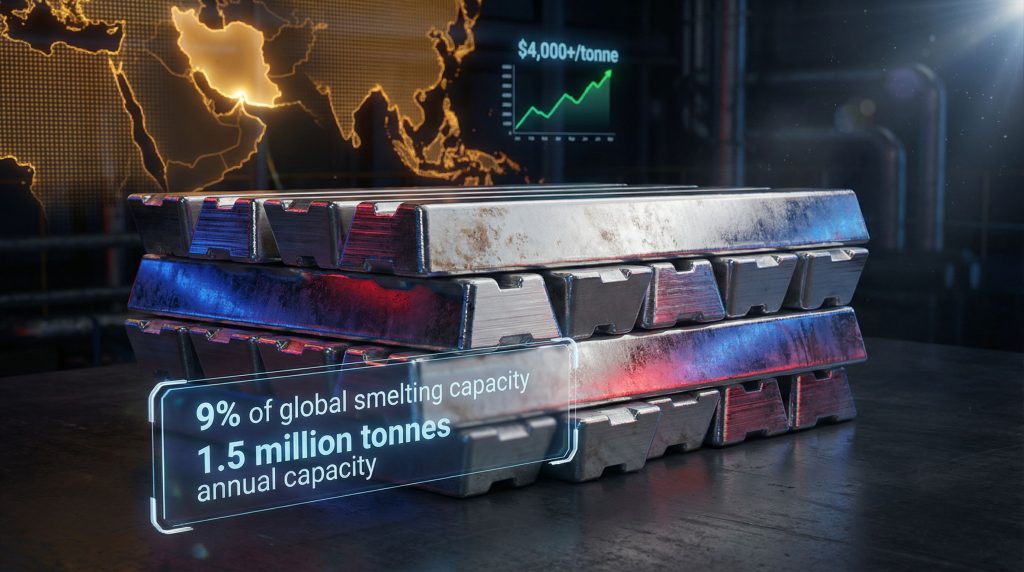

The Persian Gulf's aluminum smelting infrastructure represents approximately 9% of global production capacity, yet accounts for 18% of international aluminum exports outside China. This disproportionate export concentration creates amplified market impact when regional disruption occurs. Three major facilities demonstrate the vulnerability of clustered production assets.

Furthermore, the simultaneous targeting of complementary production facilities reveals strategic military planning designed to maximise supply chain disruption. Al Taweelah's complete shutdown eliminates 1.5 million tonnes of annual capacity, while Alba's operational reduction removes an additional 1.12 million tonnes from normal output levels. Combined with Qatalum's precautionary capacity reduction, the Gulf region has lost approximately 2.1 million tonnes of active production capacity.

Critical Production Assets Under Threat:

• Al Taweelah Smelter: Complete operational shutdown following power plant destruction

• Aluminium Bahrain (Alba): Operating at 30% capacity after missile strikes

• Qatalum Qatar: Reduced to 60% operations due to raw material preservation

Geographic Risk Assessment Matrix:

| Production Region | Global Capacity Share | Export Orientation | Disruption Risk Level |

|---|---|---|---|

| Persian Gulf | 9% | Export-focused (85%) | Critical |

| China | 58% | Domestic-focused (90%) | Low |

| North America | 8% | Balanced (60%) | Low |

| Europe | 7% | Import-dependent (40%) | Medium |

This concentration pattern creates asymmetric market vulnerability where relatively small capacity losses generate disproportionate global price impacts. The Gulf facilities serve specific market segments including automotive lightweight components, aerospace structural materials, and premium packaging applications that cannot easily substitute alternative materials.

However, regional smelters operate with technological configurations optimised for their customer base, meaning production losses cannot be offset by increasing output at facilities designed for different aluminum grades or specifications. Al Taweelah's automotive-grade aluminum capacity cannot be replaced by increasing packaging-grade production elsewhere, creating sector-specific shortages within the broader aluminum market.

Maritime Trade Routes Amplify Infrastructure Vulnerability

The Strait of Hormuz closure demonstrates how maritime chokepoints create cascading supply chain failures beyond direct production losses. Aluminum smelting requires continuous feedstock flow of processed alumina, typically imported from Australian and Indonesian refineries. The effective closure of this critical shipping route forced both Qatalum and Alba to implement precautionary operational reductions to preserve remaining raw material inventories.

Supply Chain Disruption Mechanisms:

• Alumina Feedstock Interruption: 60% of regional smelter inputs blocked through maritime constraints

• Natural Gas Energy Supply: 80-85% of smelting energy requirements dependent on maritime LNG shipments

• Finished Product Export Blockade: 18% of global non-Chinese aluminum exports unable to reach destination markets

Unlike oil tankers that can economically reroute around the Cape of Good Hope despite increased transit time and cost, aluminum value chains lack comparable flexibility. Alumina refineries cannot rapidly increase production to compensate for supply route disruption, and aluminum smelters cannot economically stockpile months of raw material inventory due to storage and working capital constraints.

In addition, the dual vulnerability of both pipeline and maritime energy supply creates unprecedented risk concentration. Gulf smelters depend on natural gas either through overland pipelines vulnerable to territorial interdiction or LNG tankers subject to maritime blockade. This simultaneous exposure eliminates redundant energy pathways that typically provide supply chain resilience.

Comparative Route Analysis:

| Shipping Route | Transit Time | Cost Premium | Vessel Availability |

|---|---|---|---|

| Strait of Hormuz | 10-14 days | Baseline | High |

| Cape of Good Hope | 40-45 days | +40-60% | Limited |

| Suez Canal Alternative | 18-22 days | +15-25% | Moderate |

The economic constraints of alternative routing effectively eliminate viable substitutes for Strait of Hormuz passage. The additional transit time requires proportionally more working capital tied up in inventory, while limited vessel availability creates logistical bottlenecks that cannot absorb diverted cargo volume from the Gulf region.

Economic Scenario Modelling for Prolonged Supply Disruption

Strategic scenario analysis reveals multiple potential market outcomes depending on conflict duration and infrastructure reconstruction timelines. Current aluminum pricing at $3,314.25 per ton represents initial market adjustment, with further escalation dependent on supply restoration prospects and demand elasticity responses.

What Are the Short-Term Market Implications?

Scenario 1: Short-Term Disruption (3-6 months)

• Price Range: $3,500-4,000 per tonne sustained levels

• Regional Premiums: 15-25% above LME baseline pricing

• Demand Response: Limited substitution due to aluminum's unique properties

• Government Intervention: Strategic reserve releases likely

• Industry Impact: Automotive and packaging sectors implement temporary design modifications

How Would Extended Conflict Reshape the Market?

Scenario 2: Extended Conflict (6-18 months)

• Structural Price Floor: $4,000+ per tonne becoming normalised

• Industrial Demand Destruction: 8-12% reduction in energy-intensive applications

• Substitution Acceleration: Steel and aluminum tariffs and composite materials gaining market share

• Investment Response: Alternative capacity development initiated

• Supply Chain Restructuring: Long-term sourcing diversification programs launched

Scenario 3: Permanent Capacity Loss

• Market Rebalancing Timeline: 3-5 years for full supply restoration

• Capital Investment Requirements: $15-20 billion in alternative production capacity

• Geopolitical Realignment: Strategic mineral policy reformulation

• Technology Acceleration: Advanced recycling and efficiency improvements prioritised

Current market behaviour suggests Scenario 2 probability increasing as conflict extends beyond initial expectations. The combination of rising aluminum prices and sharp increases in physical delivery premiums indicates that market participants are pricing extended disruption duration rather than temporary logistics delays.

Demand Elasticity by Sector:

| Industrial Sector | Price Sensitivity | Substitution Options | Adjustment Timeline |

|---|---|---|---|

| Automotive | High | Limited alternatives | 18-24 months |

| Packaging | Medium | Steel cans viable | 6-12 months |

| Aerospace | Low | Critical applications | 36+ months |

| Construction | High | Multiple alternatives | 3-6 months |

Sectoral Impact Analysis Across Aluminum-Dependent Industries

Different industries exhibit varying vulnerability to aluminum supply constraints based on material intensity, substitution possibilities, and inventory management practices. The automotive sector demonstrates highest risk exposure due to lightweighting mandates and limited short-term alternatives to aluminum components.

High-Risk Industry Exposure:

• Automotive Manufacturing: Average 180kg aluminum per vehicle in modern designs

• Aerospace Industry: 75-80% aluminum content in commercial aircraft structures

• Packaging Industry: 70% of global aluminum beverage can production capacity affected

The automotive industry's aluminum dependency has increased substantially over the past decade as manufacturers pursue fuel efficiency improvements through weight reduction. Electric vehicle production particularly relies on aluminum battery enclosures and structural components that cannot utilise traditional steel substitutes without significant engineering redesign.

Furthermore, aerospace applications present the most inflexible demand profile, with aluminum alloy specifications integral to aircraft certification and safety requirements. Unlike automotive applications where steel substitution remains feasible despite weight penalties, aerospace aluminum shortage creates potential production bottlenecks with no immediate alternatives.

Medium-Risk Sector Adaptations:

• Construction Industry: Steel and composite substitution viable but costly

• Electronics Manufacturing: Aluminum heat sinks critical but lower volume requirements

• Renewable Energy: Solar panel frames and wind turbine components affected

Construction applications demonstrate greater flexibility through material substitution, though cost implications and performance trade-offs limit practical alternatives. Steel framing systems can replace aluminum extrusions, whilst composite materials offer specialised applications despite higher unit costs.

Risk Mitigation Strategies by Industry:

| Industry Sector | Primary Mitigation | Secondary Option | Timeline |

|---|---|---|---|

| Automotive | Strategic inventory buildup | Design modification | 6-18 months |

| Packaging | Steel can conversion | Aluminum thickness reduction | 3-9 months |

| Aerospace | Long-term contracts | Alternative alloy grades | 12-36 months |

| Electronics | Copper substitution | Thermal design changes | 6-12 months |

Energy Price Dynamics Compound Supply Chain Stress

Aluminum smelting's extreme energy intensity creates compounding pressure from both supply disruption and input cost inflation. The industry requires 13-15 MWh of electricity per tonne of aluminum production, making energy costs the dominant operational expense for smelter operators worldwide.

The Iran conflict has disrupted natural gas supplies that provide 40% of Gulf smelting energy requirements, whilst simultaneously driving global energy price increases that affect all aluminum producers. This dual impact creates cost pressure on both damaged Gulf facilities during reconstruction and alternative producers attempting to increase output. War pushes fragile aluminium markets to the brink of disaster as industry experts have warned throughout the crisis.

Global Energy Cost Multipliers:

• European Smelters: 2.1x pre-crisis electricity costs limiting expansion potential

• North American Facilities: 1.4x pre-crisis natural gas price forecasts affecting competitiveness

• Asia-Pacific Operations: 1.8x regional energy benchmarks constraining growth

The energy cost escalation particularly affects European smelting operations that rely heavily on natural gas-powered electricity generation. Several facilities have implemented temporary production curtailments as energy costs exceed aluminum selling prices, effectively removing additional supply from global markets beyond the Gulf region disruption.

Alternative Energy Source Analysis:

| Energy Source | Cost Premium | Availability | Infrastructure Requirements |

|---|---|---|---|

| Renewable Power | 15-25% higher | Limited capacity | Grid connection delays |

| Coal-Fired Power | 25-30% higher | Adequate supply | Environmental constraints |

| Nuclear Power | Baseline cost | High availability | Long-term contracts only |

| Hydroelectric | 10-20% lower | Geographic limited | Seasonal variability |

Coal-fired power generation offers the most readily available alternative to natural gas for aluminum smelting, though environmental regulations and carbon pricing mechanisms increase effective operating costs. Renewable energy sources provide long-term cost advantages but lack sufficient current capacity to absorb significant production increases.

The next major ASX story will hit our subscribers first

Strategic Reserve Policies and Government Intervention Mechanisms

Government strategic reserve releases represent the most immediate policy tool for aluminum market stabilisation, though implementation faces political constraints and limited inventory availability. The United States Strategic National Defence Stockpile contains approximately 500,000 tonnes of aluminum, whilst European strategic reserves hold an additional 300,000 tonnes across member nations.

Policy Intervention Options:

• Emergency Stock Releases: 500,000-1,000,000 tonne global capacity available

• Import Tariff Suspensions: Temporary duty elimination on aluminum imports

• Production Subsidies: Energy cost support for domestic smelter operations

• International Coordination: G7 joint reserve management protocols

Strategic reserve releases provide rapid market relief but limited duration impact due to finite inventory levels. The combined global strategic reserves could offset approximately 6-8 weeks of Gulf production losses, requiring parallel measures for sustained market stabilisation.

However, import tariff suspension offers broader market access though limited immediate supply increase due to global production capacity constraints. Existing aluminum trade barriers average 15-25% across major economies, with removal potentially reducing domestic price premiums though not addressing fundamental supply shortage.

Policy Effectiveness Assessment:

| Intervention Type | Market Impact | Implementation Speed | Political Feasibility | Duration |

|---|---|---|---|---|

| Reserve Releases | High | 30-60 days | Moderate | 6-12 months |

| Tariff Suspension | Medium | 15-30 days | High | 12-24 months |

| Production Subsidies | High | 6-12 months | Low | 24+ months |

| Export Restrictions | Medium | 7-14 days | Low | 6-18 months |

Production subsidies offer the most sustainable long-term solution through domestic capacity expansion, though implementation requires substantial fiscal commitment and extended development timelines. Energy cost support programmes could enable mothballed smelting capacity reactivation whilst encouraging new facility development in stable jurisdictions.

Investment Capital Reallocation and Geographic Diversification

Crisis-driven investment flows accelerate fundamental restructuring of global aluminum production geography, with capital allocation prioritising supply chain security over pure cost optimisation. North American aluminum smelting capacity could receive $8-12 billion in investment over the next 5 years, driven by strategic mineral security considerations rather than traditional economic factors.

Regional Investment Opportunities:

• North American Expansion: Renewable energy-powered smelting development

• Australian Capacity Growth: Hydroelectric and solar-powered production scaling

• African Development: Hydroelectric-based smelting infrastructure investment

• European Reconstruction: Energy-efficient technology deployment

Australian aluminum production offers particular strategic value due to abundant renewable energy resources and stable political environment. Hydroelectric capacity in Tasmania and solar potential in Queensland provide sustainable energy sources for aluminum smelting whilst reducing carbon footprint compared to fossil fuel alternatives.

For instance, African aluminum development presents longer-term opportunity through unexploited hydroelectric resources in Central and West Africa. The Democratic Republic of Congo's Inga Dam potential could support substantial aluminum smelting capacity, though infrastructure development requirements extend implementation timelines to 7-10 years.

Technology Investment Priorities:

| Technology Category | Investment Focus | Payback Timeline | Risk Level |

|---|---|---|---|

| Energy Efficiency | Next-generation smelting cells | 3-5 years | Low |

| Recycling Infrastructure | Secondary production scaling | 2-4 years | Low |

| Alternative Materials | Aluminum substitute development | 5-10 years | High |

| Carbon Reduction | Inert anode technology | 8-12 years | High |

Energy efficiency improvements offer the most immediate investment returns through reduced operational costs and enhanced competitiveness. Advanced smelting cell technology can reduce electricity consumption by 15-20% compared to current industry standards, providing both cost advantages and environmental benefits.

Long-Term Structural Industry Transformation

The aluminum supply crisis due to Iran war catalyses permanent industry restructuring beyond immediate crisis resolution, with implications extending across the entire aluminum value chain from raw material procurement to end-user applications. Geographic diversification becomes a strategic imperative rather than cost optimisation consideration.

Transformation Timeline and Phases:

• Phase 1 (0-2 years): Emergency capacity activation and strategic reserve utilisation

• Phase 2 (2-5 years): New facility construction and mining industry innovations deployment

• Phase 3 (5-10 years): Comprehensive supply chain restructuring and innovation adoption

Phase 1 responses focus on maximising existing global capacity utilisation through operational improvements and temporary capacity reactivation. Mothballed smelters in North America and Europe could restore approximately 800,000 tonnes of annual capacity within 18-24 months, though energy cost constraints limit economic viability without policy support.

Consequently, Phase 2 development emphasises new facility construction in politically stable regions with abundant renewable energy resources. Australia, Canada, and certain African nations emerge as preferred locations for large-scale aluminum smelting investment, with project timelines extending 3-5 years from initial development to commercial operation.

Structural Change Drivers:

- Supply Chain Risk Management: Geographic diversification requirements

- Energy Transition Acceleration: Renewable-powered production preference

- Recycling Infrastructure Development: Circular economy implementation

- Material Innovation: Aluminum-alternative research and development

Recycling infrastructure represents the most sustainable long-term response to supply constraints, with secondary aluminum production requiring only 5% of the energy needed for primary smelting. Current global recycling rates of approximately 75% for aluminum could increase to 85-90% through improved collection systems and processing technology.

Critical Minerals Strategy Integration and Cross-Commodity Implications

The aluminum supply crisis due to Iran war highlights systemic vulnerabilities across critical mineral supply chains, influencing strategic policy frameworks beyond aluminum-specific responses. Energy-intensive mineral processing operations face similar geographic concentration risks and infrastructure vulnerability patterns.

Cross-Commodity Risk Assessment:

• Lithium Processing: Battery manufacturing aluminum content creates downstream vulnerability

• Rare Earth Refining: Shared energy infrastructure and processing facility risks

• Copper Production: Alternative material competition during aluminum shortage periods

Lithium battery production utilises substantial aluminum content for casing, heat dissipation, and structural components, creating indirect exposure to aluminum supply constraints. Electric vehicle manufacturers face compounding material cost pressures as both lithium and aluminum markets experience simultaneous stress.

Moreover, rare earth refining operations share energy infrastructure vulnerability with aluminum smelting, particularly in regions with concentrated processing capacity. China's dominance in rare earth processing creates similar chokepoint risks to Gulf aluminum concentration, though with different geopolitical dynamics. As Reuters reported, aluminium hits four-year peak after Iran attacks Middle East smelters, demonstrating the severe market impact of targeted infrastructure disruption.

Strategic Mineral Security Framework:

| Policy Element | Implementation Strategy | Timeline | Success Metrics |

|---|---|---|---|

| Supply Diversification | Multi-source procurement mandates | 2-5 years | Reduced concentration ratios |

| Domestic Processing | Value-added manufacturing incentives | 3-7 years | Processing capacity growth |

| Allied Cooperation | Resource sharing agreements | 1-3 years | Strategic partnership depth |

| Innovation Investment | Alternative technology development | 5-10 years | Technology substitution rates |

The aluminum supply crisis due to Iran war serves as a catalyst for broader critical minerals energy transition policy reform, with lessons applicable across multiple commodity sectors. Strategic stockpiling, supply chain diversification, and domestic processing capacity development emerge as priority policy responses with implications extending beyond aluminum markets.

International cooperation mechanisms gain importance as individual nations lack sufficient resources to address critical mineral security independently. Allied nation resource-sharing agreements and coordinated strategic reserve management provide collective resilience against supply disruption whilst maintaining competitive market dynamics.

How Does This Compare to Other Trade Disruptions?

Unlike traditional trade disputes, the current crisis involves direct physical destruction of production assets rather than tariff barriers or regulatory constraints. This fundamental difference means that resolution requires infrastructure reconstruction rather than policy negotiation, creating extended timeline implications that distinguish it from conventional US–China trade war impact scenarios.

Investment Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and geopolitical developments. Aluminum market outcomes depend on numerous variables including conflict duration, infrastructure reconstruction timelines, government policy responses, and global economic conditions. Readers should conduct independent research and consider professional advice before making investment decisions.

Looking for Opportunities in Critical Metals During Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including critical metals and industrial commodities that benefit from supply chain disruptions. Stay ahead of market movements by accessing instant alerts on actionable investment opportunities, ensuring you're positioned to capitalise on emerging trends. Begin your 14-day free trial today and gain the market-leading edge needed during these unprecedented commodity market conditions.