July 27, 2026

The Diamond Industry at a Crossroads: Why Natural Stones Face a Structural Reckoning

Few commodity sectors have experienced as sudden and as profound a disruption to their value proposition as the natural diamond market. What took decades to build through carefully cultivated emotional marketing and artificial supply management has been partially unravelled in a relatively short period by a combination of technological disruption, shifting generational values, and a global macroeconomic environment that has made luxury discretionary spending deeply vulnerable. Against this backdrop, the Anglo American divestment of De Beers is not simply a corporate portfolio adjustment. It is a signal that one of the world's most sophisticated mining companies no longer believes diamonds belong in a forward-looking commodity strategy.

Understanding why this transaction is taking longer than originally anticipated requires looking beyond the deal mechanics and into the deeper structural forces shaping buyer appetite, sovereign interests, and the diamond market itself.

When big ASX news breaks, our subscribers know first

Why Anglo American Has Decided to Exit the Diamond Business

Realigning Around Future-Facing Commodities

Anglo American's strategic transformation represents one of the most significant portfolio overhauls undertaken by any major diversified miner in recent memory. The company is actively concentrating its asset base around copper, premium iron ore, and crop nutrients, three commodity categories that share a common thread: structural demand growth tied to global decarbonisation and food security imperatives.

The copper demand outlook sits at the centre of electrification infrastructure, from electric vehicle drivetrains to grid-scale battery storage and renewable energy transmission. Premium iron ore demand underpins steel production in markets with tightening emissions standards. Crop nutrients address long-term agricultural productivity challenges as global food demand rises alongside population growth. Each of these commodities carries identifiable macro demand tailwinds.

Diamonds, by contrast, sit in the discretionary luxury category. Their demand is cyclically sensitive, emotionally driven, and increasingly contested by synthetic alternatives. For a company repositioning around structural commodity demand, the logic for retaining a diamond business weakens considerably.

The Structural Forces Pressuring Diamond Valuations

The rough diamond market has been navigating a convergence of disruptive pressures that have fundamentally altered the sector's supply and demand dynamics. These pressures are not temporary cyclical headwinds but structural shifts with long-term implications:

-

Lab-grown diamonds have captured meaningful market share by delivering optically comparable stones at a fraction of the cost of mined alternatives. The technology enabling synthetic diamond production has improved rapidly, lowering production costs while maintaining gem quality.

-

Shifting consumer preferences, particularly among younger demographics, have eroded the premium traditionally attached to mined stones. Younger buyers are more receptive to lab-grown alternatives and less influenced by the heritage marketing that sustained natural diamond premiums for decades.

-

Geopolitical headwinds and global tariff pressures have compounded already-weak rough diamond trading conditions, restricting demand in key consumer markets and adding layers of uncertainty to pricing forecasts.

-

Chinese demand weakness has been a persistent drag on rough diamond volumes, as China's luxury consumption has not recovered to the levels anticipated following its post-pandemic reopening.

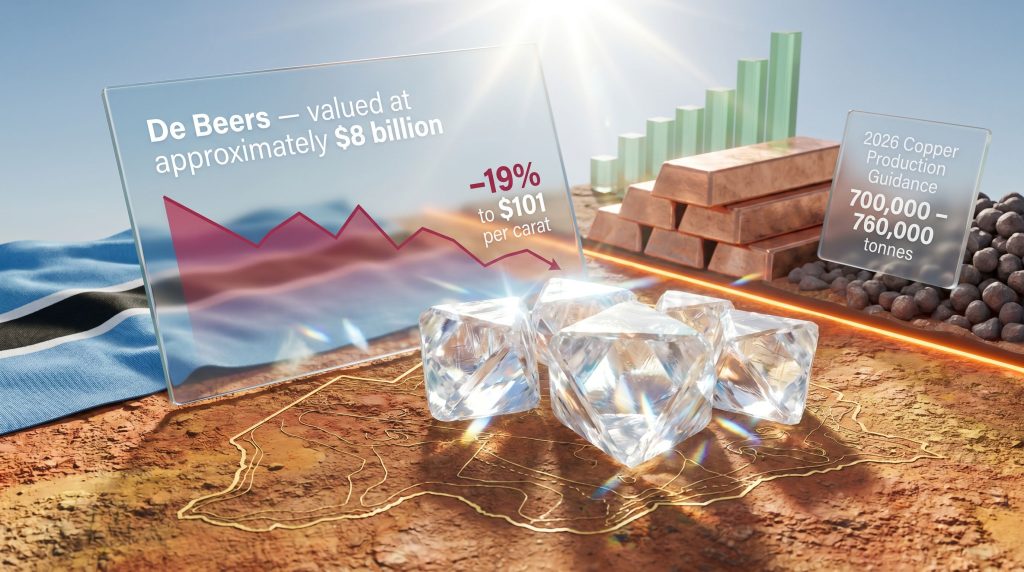

The combined effect of these forces has been severe. During the first quarter of 2026, the consolidated average realised price for De Beers diamonds fell 19% to $101 per carat, driven by a 17% decline in the average rough price index alongside a shift in sales mix toward a higher proportion of lower-value goods. This dual compression, falling unit prices and a deteriorating product mix, creates a compounding drag on total revenue that is particularly damaging to buyer valuation models.

"The rough diamond market is not experiencing a temporary correction. It is navigating a structural repricing driven by synthetic competition and demand-side shifts that have no clear reversal mechanism in the near term."

Where the Anglo American Divestment of De Beers Stands in 2026

A Formal Process Without a Fixed Endpoint

Anglo American has confirmed it is actively running a formal sale process for De Beers, but as of April 2026, no specific completion date has been publicly committed to. The company's position, as communicated by CEO Duncan Wanblad through Q1 2026 production results, is that progress is being made and material updates will be provided during the course of the year.

The absence of a firm timeline does not necessarily reflect hesitation or strategic indecision. More likely, it reflects the genuine complexity of the transaction structure, which involves sovereign stakeholders, operationally interdependent joint ventures, and a commodity market backdrop that continues to create valuation uncertainty for both seller and potential buyers. Indeed, Anglo coal sale risks have already illustrated how quickly deal conditions can shift in volatile commodity environments.

Q1 2026 Market Performance: A Valuation Headwind in Numbers

| Metric | Q1 2026 Status |

|---|---|

| Consolidated average realised price | $101 per carat |

| Price movement year-on-year | Down 19% |

| Average rough price index movement | Down 17% year-on-year |

| Sales mix composition | Higher proportion of lower-value goods |

| 2026 production guidance | 21 to 26 million carats (unchanged) |

Source: MiningMX reporting on Anglo American Q1 2026 production results, Brendan Ryan, April 28, 2026.

De Beers is actively monitoring rough diamond trading conditions to calibrate output against prevailing demand, suggesting a supply management approach designed to protect price floors rather than maximise volume. Maintaining unchanged production guidance of 21 to 26 million carats despite significant price deterioration indicates the company is relying on output flexibility within this range rather than issuing formal production cuts, which could signal distress to prospective buyers.

The Hidden Complexity of the Sales Mix Shift

One dimension of the De Beers valuation challenge that receives less attention than headline price declines is the sales mix degradation. When the composition of sales shifts toward lower-value goods, the impact on revenue per carat compounds the headline price decline. This is not simply about lower prices for the same stones; it reflects a quality-weighted deterioration in what is actually being sold.

In rough diamond markets, higher-value goods command significant premiums over lower-value categories. A shift toward lower-value goods in the sales mix may reflect weaker demand from high-end jewellers and stronger demand from industrial or lower-tier jewellery manufacturers. It can also reflect inventory management decisions by sightholders who may be selectively passing on premium goods when market conditions are uncertain.

The Buyer Landscape: Why Sovereign Interests Complicate the Transaction

A Deal Involving More Than Commercial Buyers

The most plausible transaction structure for the Anglo American divestment of De Beers involves a consortium with significant sovereign participation rather than a straightforward acquisition by a single corporate buyer. This reflects the unique ownership and operational architecture of De Beers, which is deeply intertwined with the economic interests of multiple African nations.

Botswana holds a 15% direct equity stake in De Beers and exercises dominant influence over production through the Debswana joint venture, which controls approximately 70% of De Beers' total output. For Botswana, diamonds are not merely a commercial commodity. They represent approximately 80% of the country's total export earnings and contribute roughly 30% of national GDP, making De Beers ownership a question of economic sovereignty.

President Duma Boko has publicly positioned securing full national control over De Beers and the complete diamond value chain as a national priority. This political objective effectively gives Botswana a structurally significant role in any ownership transition, as any new owner must establish a functional working relationship with a government that controls the majority of the company's production base.

Multi-Sovereign Complexity

Beyond Botswana, two additional African nations have signalled interest in participatory ownership roles:

-

Angola has expressed interest in acquiring a stake of between 20% and 30%, seeking to extend its influence over the diamond value chain beyond its own domestic production.

-

Namibia has also indicated interest in a participatory ownership structure, reflecting its position as a significant diamond-producing nation with existing operational exposure to De Beers through the Namdeb joint venture.

The emergence of multiple sovereign prospective buyers fundamentally changes the negotiation dynamics. Rather than a bilateral commercial transaction, the sale process must accommodate the distinct economic objectives, financing capacities, and political timelines of at least three sovereign entities. This introduces a diplomatic dimension to what would otherwise be a straightforward M&A process, and these mining geopolitical risks are not unique to De Beers alone.

"When sovereign buyers are involved in major natural resource transactions, commercial timelines become secondary to political consensus-building. Each government stakeholder has domestic constituencies to satisfy, legislative processes to navigate, and economic priorities that may not perfectly align with Anglo American's preferred transaction structure or timing."

The S&P Botswana Rating Cut: A Marker of Diamond Market Severity

The depth of the diamond market's challenges is further illustrated by S&P's decision to cut Botswana's sovereign credit rating in response to diamond market weakness. This is a rare instance where a single commodity's market deterioration triggers a sovereign credit event, underscoring just how concentrated Botswana's economic exposure to diamonds remains and how much is at stake for the government in the De Beers ownership transition.

Anglo American's Broader Divestment Programme: Running Multiple Processes Simultaneously

The Steelmaking Coal Sale as a Case Study in M&A Risk

Anglo American is managing several major asset disposals concurrently, with the De Beers process being the most complex. The steelmaking coal sale is the most advanced, with the company expecting to reach a binding agreement within Q2 2026.

The coal sale process itself has already demonstrated the risks inherent in divesting operational mining assets. Anglo American's original agreement to sell its steelmaking coal operations to Peabody Energy for $3.8 billion collapsed after a fire closed the Moranbah South mine. Furthermore, the Moranbah mine disruption serves as a precise case study in how operational incidents can derail even well-progressed M&A transactions, a risk that remains directly relevant to the De Beers process given ongoing commodity market volatility.

The current status of the coal assets:

-

Moranbah South mine: Has transitioned back to normal longwall operations and is progressing through a production ramp-up phase.

-

Grosvenor mine: Permission to re-enter underground areas was granted by the regulator in August 2025. The re-entry and rectification process is in its final stages with operational readiness assessments complete. Longwall production restart is targeted for late 2027, subject to investment approval.

Core Asset Production Providing Strategic Stability

While Anglo American pursues its divestment programme, its retained core assets are providing operational and financial stability that reduces urgency around deal timing. Production guidance for 2026 across the flagship assets remains unchanged:

| Asset | 2026 Production Guidance |

|---|---|

| Copper | 700,000 to 760,000 tonnes |

| Total iron ore | 55 to 59 million tonnes |

| Kumba Iron Ore (subset of total iron ore) | 31 to 33 million tonnes |

Source: Anglo American Q1 2026 production results via MiningMX, April 28, 2026.

This operational stability means Anglo American is not a distressed seller. The company has the financial flexibility to pursue the De Beers and coal disposals on terms it deems acceptable rather than accepting below-market pricing under balance sheet pressure. Consequently, this suggests Anglo American will hold firm on valuation expectations even as De Beers' near-term earnings profile deteriorates.

The Teck Merger: The Other Half of Anglo American's Strategic Equation

A Transformative Acquisition Advancing Toward Completion

The Anglo American divestment of De Beers does not exist in isolation. It is one element of a dual-track strategic transformation that simultaneously involves acquiring scale in future-facing commodities through the merger with Teck Resources, the Canadian diversified mining group.

According to Wanblad's Q1 2026 commentary, the Teck merger is on track for an expected close window of September 2026 to March 2027. Regulatory approval has been secured from South Korea, with China's anti-trust clearance remaining the final outstanding regulatory milestone before closing conditions are satisfied.

The Teck transaction primarily brings additional copper assets into the Anglo American portfolio, reinforcing the company's positioning in a commodity central to global electrification infrastructure. The strategic logic is coherent: as Anglo American exits diamonds and coal, it is simultaneously adding copper exposure at scale.

Two Sides of the Same Strategic Transformation

The De Beers divestment and the Teck merger are structurally complementary strategic moves:

-

De Beers exit removes exposure to discretionary luxury demand cycles, lab-grown competition, and geopolitical diamond trade risks.

-

Teck acquisition adds exposure to copper, a metal with near-certain structural demand growth from EV manufacturing, grid expansion, and renewable energy infrastructure.

-

Together, both moves reflect a deliberate portfolio migration from legacy extractive industries toward commodities embedded in the global energy transition.

The next major ASX story will hit our subscribers first

Key Risk Factors That Could Further Delay the De Beers Sale

A Multi-Dimensional Risk Landscape

Investors and analysts monitoring the Anglo American divestment of De Beers should be aware of several risk factors that could extend the transaction timeline or affect final pricing:

1. Sovereign Negotiation Complexity

Multi-party government negotiations involving Botswana, Angola, and potentially Namibia introduce diplomatic timelines that operate independently of commercial deal-making schedules. Political consensus within each government adds duration beyond typical M&A processes.

2. Diamond Market Valuation Gap

Persistent price weakness reduces De Beers' near-term earnings multiple, potentially creating a gap between Anglo American's valuation expectations and what buyers are willing to pay. The 19% decline in realised prices to $101 per carat creates a moving target for both sides of the negotiation.

3. Lab-Grown Diamond Market Share Expansion

Continued synthetic diamond market share gains may further compress the long-term earnings outlook for natural diamond mining, reducing buyer confidence in premium valuation assumptions and making it harder to justify higher multiples.

4. Operational Performance During the Sale Process

Any deterioration in production volumes, realised prices, or key mine performance during the sale process could trigger buyer renegotiation or withdrawal, precisely as demonstrated by the Peabody Energy coal deal collapse.

5. Geopolitical and Tariff Environment

Ongoing global trade tensions and tariff headwinds identified as contributing factors to Q1 2026 diamond market weakness represent an external variable neither Anglo American nor prospective buyers can fully control or forecast.

6. Financing Capacity of Sovereign Buyers

The financial capacity of Botswana, Angola, and Namibia to fund meaningful equity stakes in De Beers at Anglo American's expected valuation range adds another layer of uncertainty. S&P's downgrade of Botswana's credit rating raises questions about the government's borrowing capacity at a time when it is pursuing increased asset ownership.

What the De Beers Sale Means for the Global Diamond Industry

A Generational Shift in Diamond Ownership

Rio Tinto's exit from the diamond sector after more than five decades, including the closure of the Argyle mine, established a clear precedent: major diversified miners are retreating from diamonds as a strategic commodity. Anglo American's intended separation from De Beers follows this trajectory, representing a second major signal within a short period that the natural diamond sector no longer commands the strategic premium it once did within large mining portfolios.

If the anticipated consortium structure proceeds, with Botswana, Angola, and possibly Namibia holding substantial combined equity positions, the diamond industry's ownership architecture would shift fundamentally toward the producing nations themselves. This would represent a rebalancing of industry control with significant implications for how the natural diamond narrative is managed globally, who controls pricing and supply, and how the sector responds to the continuing challenge from synthetic alternatives.

The Sightholder System and Future Commercial Dynamics

One aspect of the De Beers ownership transition that carries substantial industry significance is the future of the sightholder system. De Beers operates through a tightly controlled distribution model in which a select group of approved buyers purchase rough diamonds at ten annual sales events at non-negotiable prices. This system has historically allowed De Beers to exercise significant price discipline over the rough diamond market.

Any ownership change that introduces multiple sovereign stakeholders with potentially competing commercial objectives could complicate the maintenance of this pricing discipline. Sovereign owners focused on maximising production revenue may prioritise volume over price management, which could accelerate the very pricing weakness that has made the De Beers sale so complex in the first place.

"The long-term viability of the natural diamond premium depends on the industry's capacity to differentiate mined stones from lab-grown alternatives through provenance, certification, and emotional marketing. Whoever controls De Beers post-divestment will inherit both this challenge and the responsibility for how the natural diamond story is told to the next generation of consumers."

Frequently Asked Questions About the Anglo American Divestment of De Beers

Has Anglo American set a deadline for completing the De Beers sale?

No firm completion date has been announced as of April 2026. Anglo American has confirmed it is running a formal sale process and expects to provide updates during the course of 2026, but has not committed to a specific transaction close date.

What is De Beers currently valued at?

De Beers has been valued at approximately $8 billion, though the prevailing weakness in rough diamond markets, including the 19% decline in average realised prices to $101 per carat recorded in Q1 2026, may influence final transaction pricing depending on when a deal is agreed.

Why does Botswana have such significant influence over the De Beers sale?

Botswana holds a 15% direct equity stake in De Beers and controls approximately 70% of De Beers' total production through the Debswana joint venture. Diamonds represent around 80% of Botswana's export earnings and approximately 30% of GDP, giving the government both economic dependency and operational leverage over any ownership transition.

Is the diamond market expected to recover in the near term?

The rough diamond market faces structural headwinds from lab-grown competition, shifting consumer preferences among younger buyers, and geopolitical trade pressures. De Beers continues to monitor conditions and align output with demand, but no near-term price recovery has been signalled by Anglo American's management.

What other major transactions is Anglo American managing alongside the De Beers sale?

Anglo American is also divesting its steelmaking coal operations, with a sale agreement expected in Q2 2026. The company is simultaneously advancing its merger with Teck Resources, targeting a close window between September 2026 and March 2027, pending final anti-trust approval from China.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Statements regarding transaction timelines, valuations, production guidance, and market conditions are based on publicly available reporting as of April 2026 and are subject to change. Readers should conduct independent research and consult qualified financial advisors before making investment decisions. References to potential buyer interest, sovereign ownership structures, and market forecasts involve a degree of uncertainty and should not be interpreted as confirmed outcomes.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While the diamond sector navigates structural decline, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries across copper, iron ore, and more than 30 other commodities — the very materials driving the global energy transition. Explore how major discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.