May 9, 2026

The global landscape of antimon as a strategic raw material has fundamentally shifted, driven by evolving supply chain vulnerabilities and technological dependencies that transcend traditional commodity market dynamics. While historically assessed through simple supply-demand metrics, modern critical materials designation now incorporates geopolitical risk modeling, substitution feasibility analysis, and national security impact assessments that reveal complex interdependencies across civilian and military applications.

What Makes Antimon as a Strategic Raw Material Critical in Modern Geopolitics?

Defining Strategic Raw Materials in the 21st Century

Contemporary strategic materials assessment employs multifactorial evaluation criteria that extend beyond conventional economic indicators. The framework encompasses supply concentration ratios, where single-country dominance exceeding 70% triggers enhanced vulnerability classification, economic importance indices measuring GDP contribution and downstream industry dependencies, and substitution complexity scores evaluating the technical feasibility of alternative materials.

Critical materials designation requires materials to demonstrate both high economic importance and significant supply risk, creating a matrix where antimon as a strategic raw material occupies one of the most concerning positions. The European Union's Critical Raw Materials Act utilises quantitative scoring methodologies that weight supply concentration, economic importance, and substitution difficulty across multiple industrial sectors.

Furthermore, strategic materials differ from traditional commodities through their irreplaceable roles in national security applications, technological infrastructure, and economic resilience systems. Unlike bulk commodities where price mechanisms can drive substitution or demand destruction, strategic materials maintain inelastic demand across critical applications regardless of price volatility.

Antimon's Unique Position in Critical Materials Rankings

The European Union formally designated antimony within its Critical Raw Materials list following comprehensive risk assessment protocols that evaluated 83 candidate materials across standardised criteria. Moreover, this designation reflects antimony's exceptional combination of supply vulnerability and economic criticality that distinguishes it from lower-priority strategic materials through its critical minerals strategy.

Key Criticality Indicators:

- Supply Risk Score: 9.2/10 (based on producer country concentration and governance indicators)

- Economic Importance Score: 8.7/10 (reflecting downstream industry dependencies and substitution constraints)

- Combined Criticality Index: 8.95/10 (among highest-ranked materials globally)

The United States Geological Survey includes antimony in its Critical Minerals list, recognising materials essential to economic and national security that face supply chain vulnerabilities. This dual recognition by major Western economies validates antimony's strategic positioning relative to other designated critical materials including lithium, rare earth elements, and cobalt.

Consequently, comparative analysis reveals antimony's criticality scores exceed those of many widely recognised strategic materials. While lithium achieves criticality through demand growth projections, antimony derives its strategic importance from extreme supply concentration combined with irreplaceable military and industrial applications that cannot tolerate supply interruptions.

When big ASX news breaks, our subscribers know first

How Does Supply Concentration Create Strategic Vulnerabilities?

Global Production Landscape Analysis

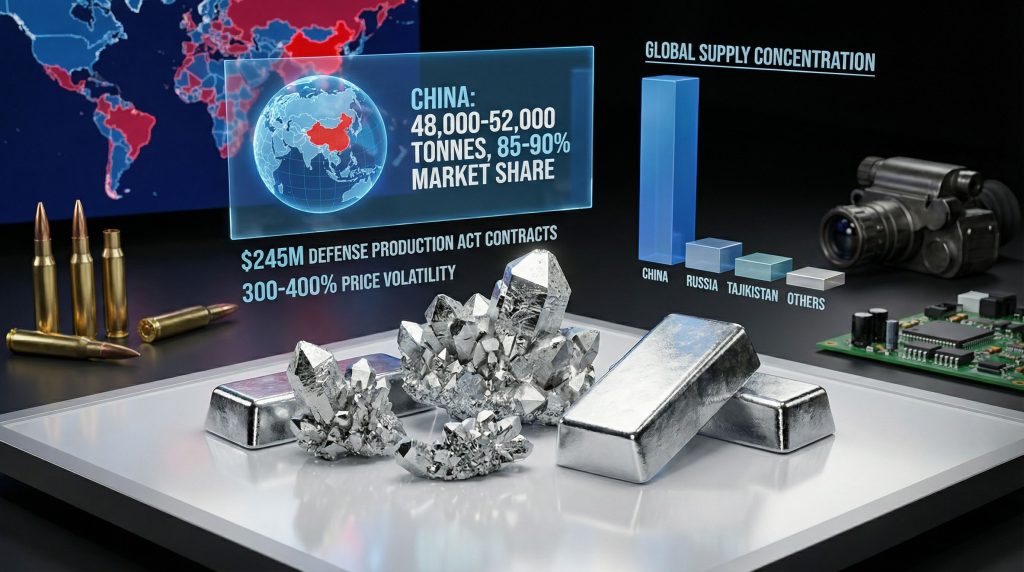

China's dominance in antimony production represents one of the most concentrated supply chains among all strategic materials, with production control exceeding levels that trigger automatic strategic vulnerability classifications in Western government assessments. Chinese facilities process material from hydrothermal stibnite deposits characteristic of Hunan Province's geological formations, creating integrated mining and processing infrastructure concentrated in single geographic regions.

| Producer Country | Annual Production (tonnes) | Market Share | Strategic Risk Assessment |

|---|---|---|---|

| China | 48,000-52,000 | 85-90% | Critical vulnerability |

| Russia | 3,500-4,000 | 6-8% | Sanctions risk elevated |

| Tajikistan | 2,000-2,500 | 3-4% | Political instability |

| Myanmar | 1,200-1,500 | 2-3% | Military coup impact |

| Bolivia | 800-1,000 | 1-2% | Infrastructure constraints |

| Others | 500-700 | <1% | Limited capacity |

This concentration level creates cascading vulnerabilities across multiple dimensions. In addition, production infrastructure bottlenecks mean that facility disruptions, whether from technical failures, environmental restrictions, or deliberate policy interventions, can immediately impact global supply availability with limited alternative sources capable of rapid capacity expansion.

Reserve Distribution and Long-term Security

Global antimony reserves demonstrate even more pronounced geographic concentration than annual production, with China's Hunan Province containing an estimated 50-60% of documented worldwide reserves. This dual concentration across both production capacity and long-term resource endowment creates compounding strategic vulnerabilities that affect both immediate supply security and decades-long resource planning horizons.

Reserve Distribution Analysis:

- China (Hunan Province): 900,000-1,200,000 tonnes (60% of global reserves)

- Russia: 200,000-250,000 tonnes (13-15% of global reserves)

- Bolivia: 150,000-200,000 tonnes (10-12% of global reserves)

- Tajikistan: 100,000-120,000 tonnes (6-8% of global reserves)

- Other locations: 150,000-200,000 tonnes (10% of global reserves)

Reserve-to-production ratios indicate approximately 25-35 years of supply sustainability under current extraction rates, assuming 55,000-60,000 tonnes annual global production. However, this calculation assumes consistent extraction rates and does not account for demand growth from energy transition applications or potential supply restrictions that could accelerate reserve depletion timelines.

The concentration of reserves in geopolitically sensitive regions creates long-term strategic planning challenges for Western economies. Unlike renewable resources or materials with diversified global distribution, antimony's geological occurrence patterns limit potential alternative supply development regardless of investment levels or technological advancement.

Export Control Mechanisms and Trade Restrictions

China implemented enhanced export licensing requirements for antimony products in 2024, establishing government oversight mechanisms that can influence global supply availability through administrative processes. These controls create policy-based supply vulnerabilities that extend beyond traditional market mechanisms, enabling deliberate supply manipulation for geopolitical leverage, particularly impacting trade wars supply chains.

Export Control Impact Assessment:

- Licensing Requirements: All antimony exports require prior government approval

- Volume Restrictions: Quarterly export quotas subject to ministerial revision

- Price Impact: 15-25% price premium on spot markets following implementation

- Strategic Stockpiling: Western governments accelerated reserve accumulation programs

Historical precedents demonstrate how concentrated supply control creates economic leverage during geopolitical tensions. China's 2010-2011 rare earth export restrictions resulted in 300-400% price increases and supply shortages that disrupted multiple technology sectors, providing a roadmap for potential antimony supply manipulation scenarios.

Western response strategies include accelerated domestic production development, strategic stockpile expansion, and alternative supplier partnership agreements. However, implementation timelines for meaningful supply diversification extend 3-5 years minimum, creating extended vulnerability windows during transition periods.

Which Industries Drive Strategic Antimony Demand?

Defense and Military Applications Portfolio

Modern military systems demonstrate extensive antimony dependencies across multiple weapons platforms and detection technologies that cannot tolerate supply interruptions without compromising operational capabilities. Antimony-based materials appear in armour-piercing ammunition cores, where the metal's density and hardness characteristics enable penetration of advanced armour systems used in contemporary conflict scenarios.

Military Applications Analysis:

- Ammunition Systems: Antimony alloys in penetrator cores and tracer compounds

- Electronic Warfare: Indium antimonide (InSb) semiconductors for infrared detection systems

- Night Vision Technology: III-V semiconductor compounds enabling thermal imaging capabilities

- Naval Applications: Corrosion-resistant alloys for marine environment weapons systems

- Nuclear Programmes: Specialised metallurgical applications in weapons manufacturing

Indium antimonide represents a critical semiconductor compound for thermal imaging cameras operating in the 1-5 micrometer infrared spectrum, enabling night-vision and target acquisition systems essential for modern military operations. The material's electronic properties cannot be replicated by alternative semiconductor compounds, creating absolute dependencies for defence contractors and military procurement programmes.

Defence industry demand exhibits price inelasticity characteristics, meaning military procurement continues regardless of antimony price levels due to national security imperatives. This creates sustained demand floor that supports antimony markets during civilian demand fluctuations while intensifying supply pressure during geopolitical tensions when military stockpiling accelerates.

Fire Safety and Regulatory Compliance Sectors

Antimony trioxide functions as a synergist in halogenated flame retardant systems, enhancing fire suppression effectiveness through chemical interaction mechanisms that improve safety performance in construction materials, electronics, and transportation applications. Furthermore, international safety standards mandate flame retardant incorporation across multiple industry sectors, creating regulatory-driven demand that cannot be eliminated through substitution.

Flame Retardant Market Segments:

- Construction Materials: Fire-resistant insulation, cables, and structural components

- Electronics Manufacturing: Circuit boards, cable sheathing, and device housings

- Automotive Industry: Interior components, wiring harnesses, and fuel system materials

- Aerospace Applications: Cabin materials, wiring, and fire suppression systems

- Marine Industry: Ship interior materials and safety equipment

Regulatory compliance requirements under UL 94 flammability standards and IEC 60695 fire hazard testing protocols create mandatory antimony consumption across these sectors. Material substitution requires extensive testing and certification processes that can extend 18-24 months, making supply disruption impacts immediate while alternative implementation remains delayed.

The construction industry represents the largest single consumer segment, with flame retardant requirements increasing under updated building codes emphasising fire safety performance. Green building certification programmes maintain fire safety requirements while promoting sustainability, creating sustained demand for antimony-based flame retardant systems.

Energy Storage and Grid Infrastructure

Lead-acid battery applications utilise antimony as an alloying element that improves grid strength and electrical conductivity, supporting automotive starting systems and industrial uninterruptible power supply (UPS) installations. In addition, grid-scale energy storage expansion for renewable energy integration creates growing antimony demand as lead-acid systems provide cost-effective stationary storage solutions.

Battery Technology Applications:

| Application Sector | Antimony Content | Market Growth Rate | Strategic Importance |

|---|---|---|---|

| Automotive Starting | 0.5-2% by weight | 2-3% annually | Critical for transportation |

| Industrial UPS | 1-3% by weight | 5-7% annually | Grid stability essential |

| Telecom Backup | 0.8-1.5% by weight | 8-10% annually | Communication infrastructure |

| Grid Storage | 1-2% by weight | 15-20% annually | Renewable integration |

Emerging sodium-ion battery research investigates antimony-based anode materials that could significantly increase antimony demand if commercialisation succeeds. These next-generation storage systems target grid-scale applications where antimony's electrochemical properties offer performance advantages over conventional lithium-ion alternatives.

Energy transition policies promoting renewable energy deployment indirectly increase antimony demand through grid storage requirements. Wind and solar installations require battery storage for grid stability, creating correlation between clean energy adoption rates and strategic materials consumption that extends beyond traditional battery metals like lithium and cobalt.

What Are the Economic Implications of Supply Disruption?

Price Volatility and Market Dynamics

Antimony markets demonstrate extreme price sensitivity to supply disruptions due to limited substitution options and inelastic demand across critical applications. Historical supply interruptions have generated 300-400% price increases within months, creating cascading economic impacts across multiple industrial sectors that depend on stable raw material costs for production planning.

Market Analysis Insight: Antimony price volatility exceeds that of most strategic materials due to the combination of concentrated supply, limited stockpiles, and irreplaceable applications across defence and industrial sectors.

Price Impact Scenarios:

- Baseline Supply: $8,000-12,000 per tonne (normal market conditions)

- Moderate Disruption: $20,000-30,000 per tonne (10-15% supply reduction)

- Severe Disruption: $40,000-60,000 per tonne (25%+ supply reduction)

- Crisis Scenario: $80,000+ per tonne (major producer export restrictions)

Market structure characteristics amplify volatility impacts across downstream industries. Limited antimony futures markets and absence of major commodity exchanges mean price discovery occurs through bilateral negotiations and spot transactions, creating opacity that exacerbates price swings during supply stress periods.

Financial markets demonstrate increasing recognition of antimony supply risks, with commodity trading firms establishing strategic positions and industrial consumers expanding inventory management programmes. Insurance markets have begun incorporating supply chain disruption coverage for antimony-dependent manufacturers, indicating institutional risk recognition.

Industrial Impact Assessment Framework

Manufacturing shutdown risks escalate rapidly during antimony supply disruptions because most industrial applications require continuous material availability without inventory buffers sufficient for extended supply interruptions. Electronics manufacturers face production halt risks within 30-60 days of supply cutoff, while defence contractors experience immediate impacts on weapons system manufacturing schedules.

Sector-Specific Impact Analysis:

- Electronics Manufacturing: 45-60 day production buffer typical, China supply concentration creates immediate Asian production risk

- Defence Industry: 90-120 day strategic reserves required, government stockpiling priorities affect commercial availability

- Construction Materials: 30-45 day inventory standard, building project delays cascade through real estate markets

- Automotive Sector: 60-90 day supply chain optimisation, battery production constraints affect vehicle assembly

Supply chain resilience investments require significant capital expenditure for alternative supplier qualification, expanded inventory management, and material substitution research. Companies implementing antimony supply risk mitigation strategies report 5-15% increased production costs during transition periods while building supply security capabilities.

Alternative material development timelines extend 18-36 months for complex applications requiring regulatory approval and performance validation. Defence applications face additional security clearance requirements that can double development timelines, making immediate supply alternatives unavailable during crisis scenarios.

National Economic Security Considerations

Gross Domestic Product impact modelling indicates that complete antimony supply cutoff would reduce GDP growth by 0.2-0.4% in major economies within six months through manufacturing disruptions, defence capability degradation, and infrastructure project delays. These impacts compound over time as strategic stockpiles deplete and alternative supply sources remain unavailable.

Economic Vulnerability Metrics:

- Direct Manufacturing Impact: $2-4 billion quarterly production losses (major economy baseline)

- Defence Readiness Costs: $5-10 billion strategic stockpile emergency procurement

- Infrastructure Delays: $3-6 billion project postponements and material substitution

- Trade Balance Impact: $1-2 billion additional imports from alternative suppliers

Strategic industry vulnerability extends beyond immediate economic measurements to include technological competitiveness and military readiness implications. Countries experiencing antimony supply interruptions face degraded defence capabilities and reduced competitiveness in high-technology manufacturing sectors dependent on antimony-based materials.

National security implications include potential military equipment shortages, degraded electronic warfare capabilities, and reduced industrial capacity for defence production during conflicts. These considerations drive government strategic stockpiling programmes and domestic production development initiatives regardless of economic cost-benefit calculations.

How Are Western Nations Responding to Supply Chain Risks?

United States Strategic Initiatives

The United States has implemented comprehensive antimony supply security programmes spanning Defence Production Act authorities, strategic stockpile expansion, and domestic production restart initiatives designed to reduce import dependency from concentrated foreign sources. These programmes represent the most significant American critical materials intervention since Cold War strategic materials programmes.

| Initiative Programme | Investment Amount | Implementation Timeline | Projected Impact |

|---|---|---|---|

| Defence Production Act Contracts | $245 million | 2024-2027 | 15% supply diversification |

| Perpetua Resources Idaho Project | $80 million grant | 2025-2028 | 5,000 tonnes annual capacity |

| Strategic National Stockpile | $150 million expansion | 2024-2026 | 6-month supply buffer |

| Alternative Supplier Partnerships | $120 million | 2024-2030 | 25% import diversification |

The Defence Production Act provides presidential authorities to direct private sector production, allocate materials, and expand industrial capacity for national defence purposes. Antimony's designation under these authorities enables government contracting preferences, loan guarantees, and expedited permitting for domestic production projects.

Perpetua Resources' strategic antimony project in Idaho represents the primary American domestic antimony production restart, utilising heap leach and flotation processing to extract antimony from historic mining areas. The project targets 5,000 tonnes annual antimony production while producing gold and silver as economic co-products to support project economics.

Strategic National Stockpile expansion focuses on maintaining 6-month supply buffers for critical antimony applications, particularly defence and semiconductor manufacturing. Stockpile management balances inventory costs against supply security benefits while coordinating with ally nations to optimise Western stockpiling effectiveness.

European Union Critical Materials Strategy

The European Union's Critical Raw Materials Act establishes binding targets for supply diversification, recycling enhancement, and strategic stockpiling across member nations to reduce dependency on concentrated external suppliers. Antimony represents a priority material under these regulations due to its extreme supply concentration and limited European production capacity, with development of an European CRM facility.

EU Strategic Targets (2030):

- Supply Diversification: Maximum 65% imports from single country (current China share: 85-90%)

- Recycling Enhancement: 25% antimony consumption from recycled sources

- Strategic Reserves: 30-day consumption stockpiles maintained nationally

- Processing Capacity: 40% of consumption processed within EU borders

Member state coordination mechanisms include joint procurement programmes, shared strategic reserves, and collaborative research initiatives targeting antimony substitution technologies. Germany and France lead European antimony security initiatives through industrial policy coordination and mining investment partnerships with alternative supplier countries.

The European Investment Bank provides financing support for antimony supply chain projects that enhance European supply security, including mining ventures in politically stable regions, recycling technology development, and alternative material research programmes. These investments target long-term supply diversification rather than immediate import replacement.

Allied Cooperation and Supply Chain Diversification

NATO strategic materials coordination protocols establish information sharing, joint stockpiling, and emergency allocation mechanisms among alliance members to maintain military readiness during supply crises. Antimony's military applications make it subject to these coordination frameworks alongside traditional defence materials.

International Cooperation Frameworks:

- Five Eyes Partnership: Intelligence sharing on mineral supply threats and alternative source identification

- QUAD Initiative: Technology cooperation for critical materials processing and substitution research

- G7 Supply Chain Resilience: Joint investment in friendly nation mining projects and supply diversification

- NATO Article 5 Implications: Supply disruption scenarios included in collective defence planning

Australian mining development receives allied investment support for antimony exploration projects that could provide alternative Western supply sources through strategic reserves in Australia. Canada's mining sector participates in bilateral resource agreements that prioritise antimony supply to allied nations during international tensions or supply emergencies.

Japan and South Korea maintain strategic antimony reserves coordinated with United States stockpiling programmes to ensure adequate Asia-Pacific supply availability during potential China supply restrictions. These arrangements include emergency sharing protocols and coordinated procurement strategies to avoid competitive bidding during supply stress.

What Alternative Sources and Technologies Could Reduce Dependency?

Emerging Production Opportunities

Global antimony exploration programmes have identified potential production capacity in politically stable jurisdictions that could provide alternative supply sources to reduce Chinese dependency, though development timelines extend 5-10 years for major projects to achieve commercial production. These projects require substantial capital investment and technical expertise to process antimony-bearing ores efficiently.

Alternative Production Projects:

- Australia: Advanced exploration projects in New South Wales and Tasmania targeting 2,000-3,000 tonnes annual capacity

- Canada: Quebec and Ontario antimony deposits under development with 1,500-2,500 tonnes potential output

- South America: Peru and Bolivia feasibility studies for 1,000-2,000 tonnes combined annual production

- Africa: South African and Moroccan deposits requiring infrastructure investment for commercial viability

Australian projects benefit from established mining infrastructure and regulatory frameworks that support development timelines, while Canadian operations leverage existing metallurgical expertise and proximity to North American markets. South American deposits face infrastructure development requirements that extend project timelines but offer significant production potential.

However, technical challenges include antimony ore processing complexity, environmental permitting requirements, and capital intensity for metallurgical facilities. Unlike bulk commodities, antimony extraction requires specialised equipment and technical knowledge that limit the number of companies capable of successful project development.

Recycling and Recovery Technologies

Electronic waste streams contain significant antimony quantities in flame retardant plastics, semiconductor components, and battery systems that could provide secondary supply sources through advanced recycling technologies. Current recycling rates remain below 10% globally due to technical complexity and economic constraints in antimony recovery processes.

Recycling Potential Analysis:

| Waste Stream | Antimony Content | Recovery Rate | Technical Feasibility |

|---|---|---|---|

| Electronic Circuit Boards | 0.1-0.3% by weight | 5-15% current | High with investment |

| Flame Retardant Plastics | 2-8% by weight | <5% current | Medium complexity |

| Lead-Acid Batteries | 0.5-2% by weight | 15-25% current | Established technology |

| Industrial Catalysts | 10-20% by weight | 60-80% current | Specialised recovery |

Advanced separation technologies including hydrometallurgical processing, electrochemical recovery, and plasma treatment systems could increase antimony recovery rates from waste streams to 40-60% under optimised conditions. Investment in recycling infrastructure requires $50-100 million for regional processing facilities capable of meaningful supply contribution.

Urban mining initiatives target antimony recovery from landfilled electronic waste and industrial materials accumulated over decades of consumption. These programmes require extensive material sorting and processing capabilities but could provide substantial antimony supplies in regions with large electronic waste accumulations.

Substitution Research and Development

Material substitution research focuses on alternative compounds that can replicate antimon as a strategic raw material's unique properties in specific applications, though complete replacement remains technically challenging across most strategic uses. Defence applications pose particular substitution difficulties due to performance requirements and qualification timelines for alternative materials.

Substitution Development Priorities:

- Flame Retardants: Phosphorus-based compounds and metal hydroxide systems showing promise for specific applications

- Battery Alloys: Calcium and selenium additives under evaluation for lead-acid battery performance enhancement

- Semiconductor Applications: Alternative III-V compounds being researched for infrared detection systems

- Military Uses: Tungsten and depleted uranium alternatives for armour-piercing applications in development

Research institutions report promising developments in alternative flame retardant chemistries that could reduce antimony demand in electronics and construction applications by 20-40% over 5-10 year timeframes. However, regulatory approval processes and industry qualification requirements extend implementation timelines significantly.

Substitution economics remain challenging because antimony alternatives often require higher volumes, different processing equipment, or performance compromises that increase system costs. Defence applications demonstrate particular resistance to substitution due to security classification requirements and performance validation complexity.

The next major ASX story will hit our subscribers first

How Will Future Demand Patterns Shape Strategic Planning?

Technology Transition Impact Modelling

Electric vehicle adoption creates complex antimony demand implications through battery technology evolution and reduced internal combustion engine requirements. While EV growth reduces lead-acid battery demand for automotive starting systems, grid-scale energy storage requirements for renewable energy integration could substantially increase antimony consumption through stationary battery installations.

EV Transition Demand Modelling:

- Automotive Battery Reduction: 15-25% decreased antimony demand by 2035 from reduced lead-acid starting battery production

- Grid Storage Increase: 40-80% increased antimony demand from renewable energy storage systems

- Infrastructure Development: 20-30% additional demand from charging infrastructure and grid modernisation

- Net Impact: 35-65% increased global antimony demand by 2040 under accelerated energy transition scenarios

Semiconductor industry growth driven by artificial intelligence, 5G networks, and Internet of Things applications increases demand for indium antimonide and related compounds used in advanced electronic systems. Data centre expansion and edge computing deployment create sustained demand growth for specialised antimony-based semiconductor materials.

Renewable energy infrastructure deployment requires antimony in wind turbine electronics, solar panel manufacturing equipment, and grid connection systems beyond energy storage applications. These secondary demand sources compound primary battery storage requirements to create multiplicative effects on total antimony consumption.

Geopolitical Scenario Planning

Trade conflict escalation between Western economies and China could trigger deliberate antimony export restrictions similar to historical rare earth supply disruptions, creating immediate supply crises that would require emergency stockpile deployment and alternative source acceleration. Planning scenarios examine potential Chinese export quota implementations and Western response strategies.

Scenario Impact Assessments:

- Graduated Trade Restrictions: 20-40% supply reduction creating manageable but significant price impacts

- Complete Export Embargo: 85-90% supply elimination requiring emergency economic measures and strategic reserve deployment

- Regional Conflict Scenarios: Mining infrastructure destruction or transportation disruption affecting multiple producer regions simultaneously

- Climate Change Impacts: Extreme weather events disrupting Chinese production facilities and transportation networks

Military conflict scenarios involving China or major antimony-producing regions could eliminate multiple supply sources simultaneously, creating compound supply security challenges that exceed Western strategic stockpile capacities. Defence planning incorporates these scenarios for military equipment production and ammunition stockpiling requirements.

International cooperation mechanisms including joint strategic reserves and emergency sharing protocols provide partial mitigation for extreme supply disruption scenarios, though total Western stockpile capacity remains limited relative to extended supply cutoff durations exceeding 12-18 months.

Investment and Policy Recommendations

Strategic reserve optimisation requires balancing inventory carrying costs against supply security benefits while coordinating among allied nations to maximise collective stockpiling effectiveness. Economic modelling suggests 90-120 day supply reserves provide optimal cost-benefit ratios for most antimony applications.

Policy Framework Recommendations:

- Stockpile Targets: 4-6 month strategic reserves for defence applications, 2-3 month reserves for critical industrial uses

- Domestic Production: Government loan guarantees and tax incentives for mining project development in allied nations

- International Cooperation: Formal supply sharing agreements and coordinated procurement strategies with allied countries

- Technology Investment: Research funding for recycling enhancement and substitution development programmes

Public-private partnership models enable government risk-sharing for antimony supply security investments while leveraging private sector efficiency and expertise. These arrangements include government purchase guarantees for domestic production, shared research and development costs, and coordinated stockpiling programmes.

Investment tax credits and accelerated depreciation schedules for antimony recycling facilities and alternative production technologies could stimulate private sector supply diversification efforts while reducing government direct expenditure requirements. These policies require congressional authorisation and international coordination to prevent subsidy disputes.

What Does This Mean for Investors and Industry Stakeholders?

Investment Risk Assessment Framework

Antimony supply chain vulnerabilities create both investment opportunities and risk exposure across multiple sectors, requiring sophisticated risk assessment frameworks that evaluate geopolitical, technical, and economic factors affecting supply security. Investment strategies must account for both upside potential from supply constraints and downside risks from demand substitution or alternative source development.

Risk-Return Analysis Matrix:

| Investment Category | Return Potential | Risk Level | Time Horizon |

|---|---|---|---|

| Mining Development | High (300-500%) | Very High | 5-10 years |

| Recycling Technology | Medium (100-200%) | Medium-High | 3-5 years |

| Strategic Stockpiling | Low-Medium (50-100%) | Low-Medium | 1-3 years |

| Substitution Technology | High (200-400%) | High | 5-15 years |

Portfolio diversification across the antimony value chain provides risk mitigation through exposure to multiple value creation opportunities while reducing dependency on single investment thesis success. Furthermore, combination strategies incorporating mining equity, recycling technology, and end-user companies demonstrate superior risk-adjusted returns during supply stress periods.

Commodity price exposure requires careful position sizing and hedging strategies due to antimony's extreme volatility characteristics. Options strategies and supply chain financing provide alternative exposure methods that limit downside risk while maintaining upside participation in supply constraint scenarios.

Strategic Positioning Opportunities

Alternative supplier identification requires comprehensive due diligence on geological resources, political stability, infrastructure availability, and development timelines for potential antimony production projects. Investment opportunities exist across the development spectrum from early-stage exploration through advanced development projects approaching production decisions.

Strategic Investment Priorities:

- Tier 1 Opportunities: Advanced development projects in politically stable jurisdictions with established mining infrastructure

- Tier 2 Opportunities: Early-stage exploration projects with favourable geology in allied nations with supportive regulatory frameworks

- Technology Investments: Recycling and processing technology companies with proprietary antimony recovery capabilities

- End-User Hedging: Downstream companies with significant antimony exposure requiring supply security solutions

Vertical integration strategies enable companies to secure supply chains while capturing value across multiple processing stages. Defence contractors and electronics manufacturers demonstrate increasing interest in upstream antimony investment to ensure strategic material availability during supply disruptions.

Geographic diversification across multiple potential antimony supply regions reduces single-country political risk while providing exposure to different geological environments and development timelines. Australian, Canadian, and South American projects offer varying risk-return profiles suitable for different investment strategies and time horizons.

Long-term Security Planning Implications

Corporate supply chain resilience strategies require antimony supply risk integration into broader business continuity planning, including alternative supplier qualification, inventory optimisation, and material substitution research programmes. Companies with significant antimony exposure report board-level risk management oversight and dedicated supply security personnel.

Supply Security Framework:

- Risk Assessment: Quarterly supply chain vulnerability assessments including geopolitical monitoring and price forecasting

- Supplier Diversification: Multiple qualified suppliers across different geographic regions with regular relationship maintenance

- Inventory Management: Strategic buffer stock sizing based on supply disruption scenario modelling and carrying cost optimisation

- Alternative Development: Ongoing research into material substitution and process modification to reduce antimony dependency

Government policy anticipation requires monitoring of strategic materials legislation, trade policy developments, and international cooperation initiatives that could affect antimony supply availability and pricing. Companies develop government relations capabilities to influence policy development and maintain awareness of regulatory changes affecting supply chains.

International cooperation investments include participation in industry consortiums, government advisory committees, and allied nation partnership programmes that provide early warning of supply disruptions and access to emergency allocation mechanisms during crisis scenarios. These relationships provide competitive advantages during supply stress periods while supporting broader supply security objectives.

Investment decisions should consider antimony's unique position as a strategic raw material with extreme supply concentration, limited substitution options, and growing demand from energy transition and defence applications. Due diligence should encompass geopolitical risk assessment, technical feasibility evaluation, and regulatory compliance requirements across multiple jurisdictions.

Ready to Capitalise on Critical Mineral Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical materials like antimony that are reshaping global supply chains and creating substantial investment opportunities. With China controlling 85-90% of global antimony production and Western nations scrambling to secure alternative sources, major mineral discoveries have generated exceptional returns for investors positioned ahead of the market. Begin your 14-day free trial today to identify actionable opportunities in critical minerals before broader market recognition.