June 6, 2026

The Metal That Can't Be Melted, Replaced, or Ignored

Few industrial materials carry the weight of genuine irreplaceability. Most metals face at least theoretical substitution pathways, whether through materials science innovation, recycling breakthroughs, or demand-side engineering. Tungsten is different. Its physical profile sits so far outside the range of competing materials that substitution is not merely expensive; it is in most applications technically impossible without sacrificing performance entirely. That irreplaceability, combined with an extraordinary concentration of supply inside a single geopolitical actor, has transformed this once-niche industrial metal into one of the most contested commodities on the planet.

For investors navigating the ASX tungsten stocks landscape, understanding why tungsten commands this position, and which companies are positioned to benefit, is now a genuinely important analytical task. Tungsten's strategic importance has grown considerably in recent years, driven by a confluence of geopolitical, industrial, and defence-related pressures.

When big ASX news breaks, our subscribers know first

Why Tungsten's Physical Properties Create an Economic Moat

Tungsten holds the highest melting point of any element on the periodic table, approximately 3,414 degrees Celsius. To put that in perspective, iron melts at around 1,538 degrees Celsius. The gap between tungsten and its nearest competitors is not marginal; it is enormous, and it explains why there is simply no substitute when extreme thermal stability is a non-negotiable engineering requirement.

When tungsten is combined with carbon to form tungsten carbide, the resulting compound achieves a hardness rating second only to diamond on the Mohs scale. This property underpins roughly 50% of all global tungsten consumption through cemented carbide applications: drill bits, cutting tools, mining equipment, and wear-resistant components used across manufacturing, oil and gas, and construction. These are not luxury applications. They are core industrial infrastructure.

Secondary applications broaden the demand base further:

- High-speed tool steels used in precision machining

- Aerospace turbine components exposed to extreme combustion temperatures

- X-ray tube targets in medical and industrial imaging equipment

- Electrical contacts in high-voltage switching systems

- Radiation shielding in nuclear and medical environments

Across virtually every one of these end uses, the substitution economics are deeply unfavourable. A manufacturer replacing tungsten carbide tooling with a ceramic or steel alternative would face shorter tool life, higher replacement frequency, and reduced machining precision. The cost savings from switching to a cheaper material are routinely overwhelmed by the productivity losses that follow.

The Defence Dependency That Reshapes Procurement Geopolitics

Tungsten's density, approximately 1.7 times that of lead, makes it the dominant material for kinetic energy penetrators, the long rod projectiles used in armour-piercing ammunition. At high velocity, a dense tungsten penetrator can defeat armoured steel that lighter alternatives cannot. The same density advantage applies to missile counterweights, aircraft ballast, and armoured vehicle plating.

The US Department of Defence has formally classified tungsten as a critical defence material. Its procurement framework now includes a binding commitment to eliminate sourcing from Chinese and Russian origins by 2027. European defence procurement has followed a parallel trajectory. Furthermore, the critical military metal demand dynamic playing out across multiple commodities reinforces just how structurally significant these procurement mandates have become. These are not policy aspirations; they are contractual obligations with defined timelines, and they structurally favour producers operating in non-adversarial jurisdictions.

The Clean Energy Vector Most Analysts Underestimate

A less widely understood demand driver is tungsten's role in photovoltaic solar manufacturing. Ultra-fine tungsten wire is used to slice silicon ingots into the thin wafers that form the basis of solar cells. This wire saw technology has now penetrated more than 60% of global photovoltaic production, generating an estimated 4,500+ tonnes of incremental annual tungsten demand. As global solar installation capacity continues to expand, this demand channel deepens alongside it.

Strategic reserve accumulation by several governments adds a further layer. Unlike industrial demand, reserve buying does not respond to price signals in a conventional way. Governments purchasing tungsten for strategic stockpiles are not sensitive to short-term price movements, which means this demand channel can persist even as prices rise sharply.

China's Export Controls and the Structural Repricing of Tungsten

Understanding the price trajectory of tungsten over the past two years requires understanding China's dominant position in the global supply chain. China accounts for approximately 80% of global tungsten production, and its domestic mining sector has historically set the floor for international prices through sheer volume. However, that dynamic has reversed, contributing to a broader critical minerals demand surge that is reshaping procurement strategies across Western economies.

A Chronology of Supply Restriction

Beijing's approach to tungsten export controls has been sequential and deliberate:

- February 2025: China introduced a strict export licensing regime covering tungsten products, requiring suppliers to obtain approvals that had not previously been required and that have proven difficult to obtain at scale.

- January 2026: Controls were extended to high-purity tungsten powder under China's dual-use export framework, targeting the most refined and industrially critical forms of the metal.

These measures compounded existing structural pressures within China's domestic mining sector. The 2025 annual mining quota was cut by 6.5% year-on-year. Domestic ore grades are declining as higher-grade deposits are progressively depleted. And mining costs have breached 100,000 yuan per tonne, eroding the cost advantage that historically made Chinese production globally dominant.

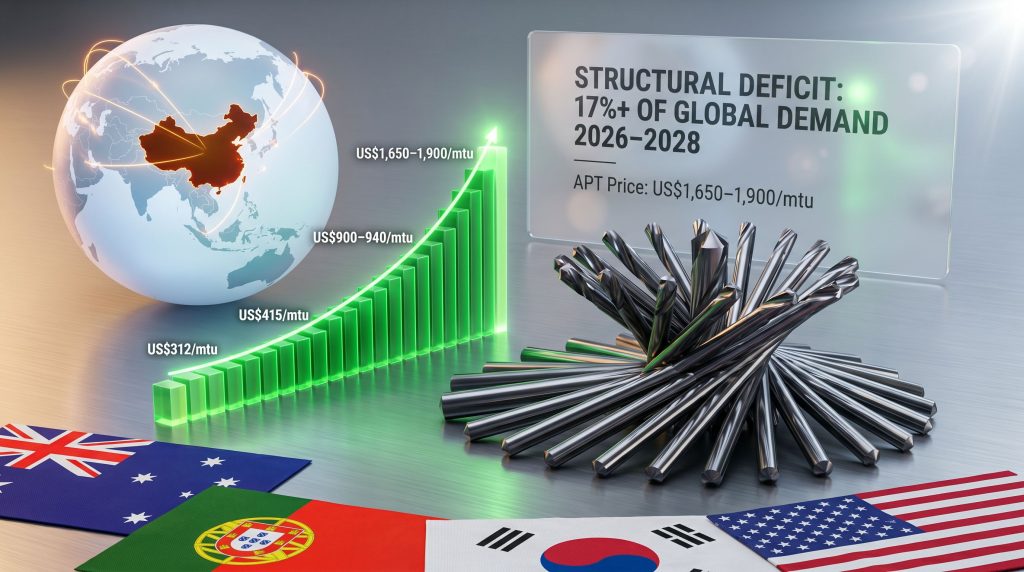

The Price Data That Defines the Moment

The market's response to these supply restrictions has been one of the most rapid repricing events seen in any industrial metal in recent memory.

| Benchmark | 2023 Price | Early 2025 | January 2026 | Mid-February 2026 |

|---|---|---|---|---|

| APT (CIF Rotterdam/Baltimore) | ~US$312/mtu | ~US$415/mtu | US$900-940/mtu | US$1,650-1,900/mtu |

| Tungsten Concentrate | n/a | n/a | n/a | ~US$22,000-24,000/mtu |

| US Spot Tungsten | n/a | n/a | n/a | ~US$111,500/MT |

Source: Fastmarkets; IMARC Group

Ammonium paratungstate, universally referred to as APT, is the primary intermediate product in the tungsten processing chain and serves as the global price benchmark. Producers sell concentrate; processors refine it into APT; manufacturers consume APT to produce tungsten metal, powder, or carbide. Every step in this chain prices off the APT benchmark.

The near-doubling of APT prices in approximately six weeks following the January 2026 powder controls was not an overreaction. It reflected a genuine recognition that the available non-Chinese supply simply cannot fill the gap left by restricted Chinese exports in the near term. Market participants have characterised the resulting price regime as one in which prices rise easily and fall with great difficulty. The structural reasons for this assessment are compelling.

Disclaimer: All price data and market forecasts referenced in this article are drawn from third-party sources including Fastmarkets and IMARC Group. Past price movements are not indicative of future performance. This article does not constitute financial advice.

The Supply-Demand Gap Through 2028: Structural, Not Cyclical

The distinction between a structural and a cyclical supply deficit matters enormously for how investors should evaluate tungsten exposure. Cyclical deficits resolve themselves as prices rise and new supply enters the market. Structural deficits persist because the barriers to new supply are not primarily economic.

In tungsten's case, the barriers are geological, jurisdictional, and temporal. Tungsten deposits of sufficient grade and scale outside China are rare. Bringing a new mine into production typically requires five to ten years from discovery through feasibility studies, permitting, construction, and commissioning. No price signal, however strong, can compress that timeline significantly.

CICC has forecast that the global supply-demand gap will exceed 17% of total demand annually from 2026 through 2028. Global new production capacity additions expected in 2026 total less than 5,000 tonnes, which is insufficient to materially alter the deficit picture. Automotive sector demand, if it aligns with continued industrial recovery in the second half of 2026, could provide a secondary price catalyst on top of the defence and clean energy demand already in play.

| Market Metric | 2026 Estimate | 2032 Projection | CAGR |

|---|---|---|---|

| Global Tungsten Market Value | ~US$7.6bn | ~US$9.65bn | 8.14% |

Source: IMARC Group

The principal risk to this outlook is US dollar strength, which reduces the purchasing power of international tungsten buyers priced in other currencies. However, given the scale of the supply shortfall and the inelastic nature of demand across defence and industrial applications, most analysts view currency headwinds as insufficient to meaningfully reverse the price trend.

ASX Tungsten Stocks: A Framework for Evaluation

The ASX provides access to the tungsten theme across the full project development spectrum. Before examining individual companies, investors benefit from applying a consistent evaluation framework. In addition, Australia's critical minerals push has created a policy environment increasingly supportive of domestic tungsten development.

| Company | ASX Code | Stage | Key Asset | Notable Feature |

|---|---|---|---|---|

| EQ Resources | EQR | Producer | Mt Carbine (QLD) + Barruecopardo (Spain) | Two producing mines |

| Tungsten Mining NL | TGN | Developer | Mt Mulgine (WA) | 175Mt JORC resource |

| Almonty Industries | AII | Producer/Developer | Panasqueira (Portugal) + Sangdong (South Korea) | Multi-jurisdiction portfolio |

| Thor Mining | THR | Developer | Molyhil (NT) + Bonya JV (NT) | Dual tungsten-molybdenum exposure |

| Arafura Resources | ARU | Explorer/Developer | Bonya tungsten deposit (NT) | JV with Thor; secondary asset |

| Antipa Minerals | AZY | Explorer | Adjacent to O'Callaghans (WA) | Early-stage, no defined resource |

Key variables that differentiate these exposures:

- Production status: Revenue-generating operations versus pre-production assets carry fundamentally different risk profiles

- Resource quality: JORC-compliant resource size, WO3 grade, and the ratio of resources already converted to economically mineable reserves

- Jurisdiction: Australian, European, and North American projects each carry different regulatory, logistical, and geopolitical risk characteristics

- Offtake and partnerships: Existing sales agreements with Western industrial or defence buyers provide revenue certainty that exploration-stage assets cannot offer

- Funding pathway: The distance between current capital position and first production cash flow is a critical differentiator for development-stage companies

EQ Resources (ASX: EQR): Direct Revenue Leverage to the Price Cycle

EQ Resources is the most operationally mature tungsten producer among ASX tungsten stocks, with revenue exposure to current spot prices through two producing operations. Mt Carbine in Far North Queensland and the Barruecopardo mine in Spain's Salamanca province together give EQR a geographic diversification that few small-cap miners can claim. Barruecopardo has been described as Europe's largest tungsten operation, positioning EQR as a natural offtake candidate for European industrial buyers seeking to reduce exposure to Chinese supply.

In the fourth quarter of 2025, EQR delivered 38,292 MTU of tungsten across its operations, representing a 33% quarter-on-quarter increase. The APT benchmark price at the start of 2026 stood at approximately US$900/mtu. Given that prices have since more than doubled, the revenue implications of that production ramp are significant.

The Mt Carbine Reserve Conversion Opportunity

The most consequential near-term catalyst for EQR is the reserve conversion program at Mt Carbine. Currently, only 23% of the total Mt Carbine mineral resource has been classified as economically mineable reserve. That gap between resource and reserve is not a negative signal; it is an opportunity. The company commenced a 28-hole, 7,700-metre drilling campaign in early 2026, a four-month program specifically designed to support resource-to-reserve conversion and underpin a comprehensive update expected in late 2026.

In March 2026, EQR also gained initial access to a higher-grade in-situ orebody at Mt Carbine, supporting a production step-up that carries through to the remainder of the year. If the drilling program achieves its objectives, a significant re-rating of the reserve base would materially alter the long-term production profile and valuation metrics.

Investor Note: EQR's share price appreciated approximately fourfold in the first four months of 2026. Investors assessing entry at current levels should carefully evaluate whether this re-rating has already captured the near-term production upside, or whether the reserve conversion program and ongoing price appreciation represent unpriced optionality. This is not a recommendation to buy or sell.

The next major ASX story will hit our subscribers first

Tungsten Mining NL (ASX: TGN): Development-Stage Torque at a Conservative Price Assumption

Tungsten Mining NL offers a fundamentally different risk-return proposition. Mt Mulgine in Western Australia hosts a JORC-compliant Mineral Resource of 175 million tonnes, positioning it among the most significant tungsten deposits outside Chinese jurisdiction by volume. The project is not yet in production, which means TGN carries development-stage risk, but it also means investors are not paying for a project that has already been re-rated on current commodity prices.

Scoping Study Economics and the Gold Sequencing Strategy

The November 2025 Scoping Study is notable for two reasons. First, the economics: the preferred 6 million tonne per annum development scenario generated a pre-tax NPV of A$1.0 to A$1.4 billion and an IRR of 30 to 45%. A larger 15 million tonne per annum scenario carried NPV of A$1.7 to A$2.3 billion. Second, and critically, these numbers were modelled using a tungsten price assumption of US$425/mtu, a figure that is now materially below prevailing spot prices. The sensitivity of these economics to current pricing is substantial.

TGN's decision to sequence near-surface oxide gold extraction ahead of full-scale tungsten production reflects sound capital risk management. Generating cash flow from gold during the pre-stripping phase offsets a portion of the capital required to expose the tungsten orebody, reducing the funding gap that would otherwise need to be bridged through equity or debt markets.

The development timeline milestones are:

- Pre-Feasibility Study (PFS): Targeted for completion in the current quarter

- Definitive Feasibility Study (DFS): Targeted for the second half of 2027 — a definitive feasibility study of this scale will be a pivotal de-risking event for the project

- First tungsten production: Targeted for Q3 2029, subject to positive study outcomes

TGN has also received a A$1 million Federal Critical Minerals Development Program grant and is actively exploring a potential NASDAQ listing to broaden access to international capital markets. Investors should recognise that the multi-year timeline between current study work and eventual production represents both the primary risk and the primary source of long-term value creation opportunity. For broader context on TGN's market position, ASX company data provides useful reference points for investors monitoring the stock.

Almonty Industries (ASX: AII): Multi-Jurisdiction Scale Across Three Continents

Almonty Industries brings a level of geographic and operational diversification that distinguishes it from other ASX tungsten stocks. The company's Panasqueira mine in Portugal is one of the longest continuously operating tungsten mines in the world, providing a track record of production that exploration and development-stage companies cannot replicate.

The Sangdong mine in South Korea represents the company's most significant growth asset. Phase 1 is in production, while Phase 2 is targeting annual output exceeding 460,000 MTU, equivalent to approximately 7% of current global tungsten supply. Achieving that target would make Sangdong one of the largest tungsten mining operations outside China in the world.

AII is also advancing the Gentung Browns Lake project in the United States, with a planned launch in the second half of 2026. If developed as planned, this would represent the first commercial tungsten mining operation in the United States in decades, a milestone with obvious strategic relevance given the US Department of Defence's 2027 deadline to eliminate Chinese-origin procurement.

Almonty's multi-jurisdictional production footprint spans three continents, positioning the company as a natural offtake partner for Western buyers seeking supply chain diversification. However, investors should conduct independent due diligence on the company's capital structure, funding requirements, and execution timelines before drawing investment conclusions.

Smaller ASX Tungsten Exposures Worth Monitoring

Thor Mining (ASX: THR) and the Bonya Joint Venture

Thor Mining's Molyhil project in the Northern Territory holds a 3.5 million tonne reserve grading 0.29% WO3, providing a defined resource base with dual-commodity exposure through associated molybdenum mineralisation. Thor also holds a 40% interest in the Bonya tungsten-copper joint venture in the Northern Territory, alongside Arafura Resources which holds the remaining 60%.

The combination of tungsten and molybdenum at Molyhil is a differentiating feature. Molybdenum is itself a critical mineral used in high-strength steel alloys and in the catalysts that process petroleum, and its price dynamics can provide additional revenue support independent of the tungsten market.

Arafura Resources (ASX: ARU) and Antipa Minerals (ASX: AZY)

Arafura Resources holds its 60% interest in the Bonya tungsten deposit primarily as an optionality asset. The company's strategic focus remains the Nolans rare earth project, and Bonya should be evaluated as a secondary exposure rather than a primary tungsten investment thesis.

Antipa Minerals holds exploration tenure adjacent to the O'Callaghans tungsten deposit in Western Australia's Paterson Province. No JORC-compliant resource has been defined at this stage. Antipa represents early-stage geological prospectivity rather than defined project economics, and should be assessed accordingly.

Key Risks Facing ASX Tungsten Stocks in 2026

| Risk Category | Description | Severity |

|---|---|---|

| Price Reversal | Chinese export controls relaxed or global demand weakens | Medium-High |

| USD Strength | Stronger dollar reduces international purchasing power | Low-Medium |

| Development Execution | Cost overruns, permitting delays, or funding gaps | Medium-High |

| Reserve Conversion Failure | Drilling programs underperform resource conversion targets | Medium |

| Equity Market Sentiment | Risk-off environment compresses small-cap valuations | Medium |

| Geopolitical Escalation | Broader trade conflict disrupts supply chains in multiple directions | Medium |

Structural factors that support price durability work against these risks:

- The projected supply-demand gap exceeding 17% of total demand through 2028 provides a durable floor

- Western procurement mandates create binding, price-insensitive demand for non-Chinese supply

- The thin global project pipeline limits how quickly new supply can enter the market

- Strategic reserve accumulation programs create demand that does not respond to conventional price signals

A Risk-Tiered Approach to Investing in ASX Tungsten Stocks

No single ASX tungsten stock is universally appropriate for all investors. The right entry point depends on risk tolerance, time horizon, and portfolio objectives.

- Near-term cash flow focus: Operational producers with direct revenue exposure to current APT benchmark prices offer the most immediate commodity sensitivity

- Development-stage upside: Projects with large, well-defined resource bases and compelling feasibility study economics offer greater long-term return potential but require acceptance of multi-year development timelines and capital funding risk

- High-torque speculative exposure: Exploration-stage companies adjacent to known deposits offer maximum leverage to a positive outcome at lower absolute capital commitment, with commensurately higher binary risk

Due Diligence Checklist for ASX Tungsten Stocks

- Is the mineral resource JORC-compliant, and what percentage has been converted to economically mineable reserve?

- What tungsten price assumption underpins the feasibility economics, and how does that compare to current spot?

- Does the company hold existing offtake agreements with Western industrial or defence buyers?

- What is the fully funded pathway to production, and has sufficient capital been secured or identified?

- Is the project jurisdiction eligible for Western defence or critical minerals procurement programs?

- Does the management team have a track record of taking projects through to production?

Frequently Asked Questions About ASX Tungsten Stocks

What is APT and why does it matter to investors?

Ammonium paratungstate is the primary intermediate chemical compound in the tungsten processing chain. Tungsten ore is processed into concentrate, which is then refined into APT, which is subsequently reduced to produce tungsten metal or powder. APT prices serve as the global benchmark for tungsten transactions and directly influence the revenue and margins of every tungsten producer. When APT prices move, producer economics move with them.

Why is tungsten classified as a critical mineral?

The US, European Union, and Australia have all formally classified tungsten as a critical mineral. The classification reflects three converging factors: the metal's irreplaceable role across defence and industrial applications, the extreme concentration of global supply within a single geopolitical actor, and the historical thinness of the non-Chinese project development pipeline. Critical mineral status does not automatically confer project-specific government support, but it shapes the policy environment within which projects are developed and evaluated.

How do China's export controls affect ASX-listed tungsten companies?

Beijing's export licensing regime, introduced for tungsten products in February 2025 and extended to high-purity powder in January 2026, has directly reduced the volume of Chinese-origin tungsten available to Western buyers. This creates a procurement imperative for Western industrial and defence customers to source from alternative suppliers. ASX-listed producers and developers operating in Australia, Europe, and North America are natural beneficiaries of this redirection of demand, provided they can demonstrate supply reliability and product quality.

Is tungsten a sound long-term investment theme?

The structural supply-demand imbalance, Western procurement mandates with binding timelines, and the thin non-Chinese project pipeline collectively support a durable long-term investment thesis. Individual company outcomes, however, will depend heavily on execution capability, funding access, commodity price sustainability, and geological outcomes from ongoing exploration and development programs. Investors should treat sector-level analysis as a starting point, not a conclusion.

Tungsten's Transformation From Industrial Input to Geopolitical Asset

The convergence of forces that has repositioned tungsten over the past two years reflects broader structural shifts in how Western economies think about supply chain security. A metal that once attracted attention primarily from materials engineers and procurement specialists is now the subject of defence department mandates, government reserve programs, and active investor interest across multiple capital markets.

The ASX occupies a distinctive position in this landscape, offering access to the full spectrum of tungsten exposure, from operational producers generating revenue at current record prices, to large-scale developers with globally significant resource bases, to early-stage explorers with high-torque optionality. Each entry point carries a different risk profile and demands a different investment framework.

The 2026 to 2028 window, defined by a projected supply gap exceeding 17% of total demand and a project pipeline too thin to close it quickly, represents the most acute phase of the structural imbalance. How individual ASX tungsten stocks perform within that window will depend less on the macro thesis, which appears well supported, and more on the operational and financial execution of each company's specific development program.

For further analysis and market commentary on the ASX tungsten investment landscape, readers can explore additional perspectives at Stocks Down Under.

This article is intended for informational purposes only and does not constitute financial advice. All statistics, price data, and forecasts referenced are sourced from third-party providers including Fastmarkets, IMARC Group, and CICC. Investors should conduct their own independent research and consult a licensed financial adviser before making investment decisions. Past performance and price movements are not indicative of future results.

Want To Be First When The Next Major ASX Mineral Discovery Hits?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across tungsten, gold, and 30+ other commodities — transforming complex geological data into actionable investment insights the moment they're announced. Explore historic examples of exceptional discovery returns and start your 14-day free trial at Discovery Alert to position yourself ahead of the market.