June 8, 2026

How Geopolitical Shock Is Redrawing the Global Helium Supply Map

The global helium market was already operating close to its structural limits before conflict reshaped energy geopolitics in the Middle East. Periodic shortages, aging extraction infrastructure, and relentless growth in technology-sector demand had created a market with almost no tolerance for additional disruption. What the escalation of conflict involving Iran has done is not introduce fragility into the helium supply chain — it has exposed fragility that was already deeply embedded within it.

Understanding why the Australia helium extraction and Iran war supply impact story matters requires looking beyond the headlines and into the physical and economic realities of a gas that underpins some of the most strategically important industries on Earth. Furthermore, the helium supply crisis now unfolding is reshaping how governments and investors assess long-term supply security.

The Structural Vulnerabilities That Preceded the Crisis

Helium is unlike virtually every other industrial gas. It is non-renewable in any practical sense, formed through the radioactive decay of uranium and thorium within ancient geological formations over timescales measured in hundreds of millions of years. It cannot be synthesised. Once released into the atmosphere, it escapes Earth's gravitational field entirely and is permanently lost. This irreversibility makes helium supply security categorically different from most commodity markets.

Before the Iran conflict intensified, the global helium supply system was already concentrated among a handful of nations, each carrying its own risk profile:

- United States — historically the world's dominant producer, but output has declined as the Federal Helium Reserve in Texas has wound down, with the reserve formally slated for privatisation

- Qatar — a major exporter whose supply transits through the Persian Gulf, now directly exposed to regional conflict risk

- Russia — Gazprom's Amur helium plant became a significant new source, but geopolitical sanctions and reliability concerns have complicated its role in Western supply chains

- Algeria — a secondary producer with limited capacity to absorb demand from disrupted sources

The concentration of meaningful supply among these four nations created a system with minimal redundancy. Consequently, any disruption to one node cascades quickly across the entire market.

Why Helium Cannot Be Treated Like Other Industrial Commodities

One of the least understood characteristics of helium among non-specialist investors is its near-impossibility to stockpile economically. Unlike oil, which can be held in strategic reserves for years, or lithium, which can be warehoused in various chemical forms, helium in its usable liquid state requires storage at -269 degrees Celsius, just one degree above absolute zero. The infrastructure required to maintain these temperatures is expensive, energy-intensive, and technically complex.

This physical constraint means that supply disruptions translate into market shortages with almost no lag time. When Persian Gulf shipping routes face elevated risk, helium consumers do not draw down strategic reserves because, in most cases, those reserves simply do not exist at scale.

The industries most exposed to this dynamic are precisely those that underpin modern technological civilisation:

- Semiconductor fabrication, where helium functions as a cooling and purging medium in processes that cannot tolerate atmospheric contamination

- Magnetic resonance imaging technology, where liquid helium is used to cool the superconducting magnets that generate diagnostic images

- Fibre optic cable manufacturing, requiring helium atmospheres during the draw process

- Aerospace and defence testing environments

- Quantum computing research, where helium-3 and liquid helium-4 cooling is foundational to qubit stability

Critical Context: Semiconductor manufacturers typically operate on just-in-time supply models, meaning their helium inventories are measured in days rather than weeks. A supply disruption of even short duration can halt production lines that manufacture chips worth billions of dollars annually.

When big ASX news breaks, our subscribers know first

The Iran Conflict's Specific Impact on Helium Markets

How Regional Conflict Tightens an Already Constrained Gas

The Strait of Hormuz carries an estimated 20 to 21 percent of global petroleum liquids trade, and its role as a transit corridor for broader energy and industrial gas exports means that any military escalation in the region reverberates across multiple commodity markets simultaneously. For helium, the consequences flow through several channels:

- Shipping insurance premiums on Persian Gulf routes have increased substantially, raising the landed cost of Qatari helium in Asian and European markets

- Route diversion costs add transit time and expense for vessels avoiding higher-risk corridors

- Supply uncertainty has prompted some technology manufacturers to attempt precautionary purchasing, which itself accelerates price escalation

- Investor caution around Middle Eastern industrial gas infrastructure has suppressed near-term capacity expansion plans

According to reporting from The Conversation, the Iran war is directly threatening global helium supply in ways that extend well beyond short-term price volatility, with long-term structural consequences now being openly discussed by industry analysts.

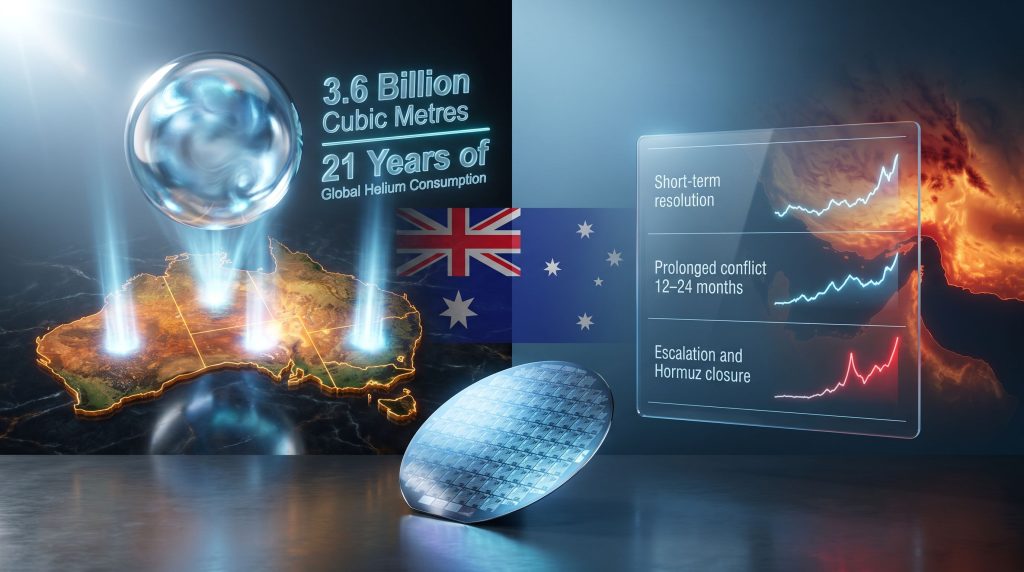

Scenario Modelling: Three Possible Trajectories for Helium Supply

| Scenario | Conflict Duration | Helium Supply Impact | Price Trajectory |

|---|---|---|---|

| Short-term resolution | Under 6 months | Moderate tightening, recovers with lag | Initial spike, gradual stabilisation |

| Prolonged conflict | 12 to 24 months | Sustained shortage, demand rationing likely | Structurally elevated across all grades |

| Escalation with Hormuz closure | Indefinite | Severe global shortage across tech and medical sectors | Extreme volatility, potential allocation-based supply |

The middle scenario is arguably the most instructive for long-term strategic planning. A sustained conflict of 12 to 24 months would not merely create temporary price spikes. It would accelerate the structural repositioning of helium supply chains away from Middle Eastern sources, a trend that was already gaining momentum before the current crisis.

Australia's Helium Endowment: A Resource Base With Global Significance

What the Numbers Actually Represent

Research from the Future Energy Exports Cooperative Research Centre (FEnEx CRC) estimates that Australia contains approximately 3.6 billion cubic metres of helium within its natural gas resource base. To contextualise that figure, this volume is equivalent to roughly 21 years of total global helium consumption at current demand levels, though not all of it is necessarily extractable under current economic conditions.

This resource estimate positions Australia not as a marginal opportunity at the edges of the global helium market, but as a potential foundational supplier capable of materially reshaping the global supply geography over the next two to three decades. In addition, the broader critical minerals demand surge of recent years has intensified focus on assets precisely like this.

The helium-prospective geology is distributed across three primary regions:

- South Australia occupies the most active exploration focus, with Precambrian basement geology that has generated helium through radioactive decay over geological timescales measured in the hundreds of millions of years

- Northern Territory offers a different pathway, with existing gas processing infrastructure that could support helium co-extraction from conventional natural gas streams

- Western Australia hosts large natural gas reserves within which extractable helium concentrations may be present, though exploration in this context remains at an earlier stage

The Geology That Makes South Australia Stand Out

The geological rationale for South Australia's prominence in helium exploration is worth examining in detail, as it illustrates a mechanism that is not widely understood outside specialist geoscience circles.

Helium accumulates in subsurface traps through a process called radiogenic helium generation. Uranium and thorium atoms embedded within ancient crustal rocks undergo radioactive decay, releasing alpha particles that capture electrons to become helium-4 atoms. Over geological timescales, these atoms migrate upward through permeable rock and, where an impermeable cap rock exists, accumulate in the same structural traps that hold natural gas.

South Australia's geology is dominated by Proterozoic-age basement rocks, some exceeding 1.5 billion years in age, which have had an exceptionally long period to generate and accumulate radiogenic helium. This is why projects in this region are reporting helium concentrations that are, in some cases, among the highest documented globally.

Gold Hydrogen's South Australian exploration program has reported corrected helium concentrations of up to 36.9 percent in certain gas samples. For reference, the threshold for commercial helium production from natural gas is generally considered to begin at concentrations around 0.3 percent. A concentration approaching 37 percent represents a resource quality roughly 100 times above the commercial minimum threshold, which has significant implications for extraction economics.

The Darwin Closure and Its Strategic Consequences

A Poorly Timed Exit From Domestic Production

Australia's only operational helium production facility, based in Darwin, ceased operations in late 2023 following the depletion of its feed gas supply from the offshore Bayu-Undan field. The closure eliminated the country's only source of domestically produced helium at precisely the moment when global supply chains were entering a period of compounding stress.

The strategic irony is significant. Australia now sits atop one of the largest estimated helium resource bases in the world while simultaneously importing all of the helium it consumes domestically. This gap between geological endowment and production reality is the central challenge and opportunity that the current wave of exploration activity is attempting to address.

Other companies active in Australia's emerging helium sector include Georgina Energy in the Northern Territory, Central Petroleum which is assessing helium co-extraction potential using existing gas infrastructure, as well as earlier-stage participants including Thor Energy, D3 Energy, and Prominence Energy. However, Australia's resource exports more broadly face mounting structural pressures that make the pace of helium sector development all the more consequential.

Project Economics: What the Financial Models Show

The Numbers Behind Australian Helium Viability

A 2022 academic case study modelling helium recovery from Australian natural gas streams produced financial metrics that deserve attention from resource investors:

| Financial Metric | Base-Case Result |

|---|---|

| Discounted payback period | 2.4 years |

| Discounted cash flow rate of return | 39.9 percent |

These figures were generated under base-case assumptions, meaning they do not incorporate the elevated helium prices that the current Iran conflict scenario would produce. Under the prolonged conflict scenario outlined above, project economics would improve materially beyond even these already compelling returns.

Investment Consideration: A sub-3-year discounted payback period combined with a nearly 40 percent DCF return positions Australian helium extraction favourably against most critical minerals development opportunities currently available to resource investors. These are base-case figures generated before the current supply disruption, not optimistic projections.

It is important to note that these are modelled projections based on academic research and should not be treated as financial advice or guaranteed outcomes. Resource project economics are subject to capital cost escalation, regulatory delays, market price volatility, and offtake agreement uncertainties.

Barriers That Could Delay the Opportunity From Being Realised

Infrastructure, Regulation, and Market Structure

The barriers to scaling Australian helium production are real and should not be minimised. Several structural challenges must be resolved before Australia can become a meaningful exporter.

Technical and infrastructure challenges:

- Helium extraction from natural gas requires cryogenic separation equipment operating at extreme temperatures, infrastructure that does not currently exist at commercial scale in Australia following the Darwin closure

- Greenfield processing facility construction requires substantial upfront capital, and project financing typically requires committed offtake agreements before banks will advance funds

- For co-extraction from existing gas streams, integration with operating gas processing facilities adds technical complexity and regulatory coordination requirements across multiple jurisdictions

Regulatory gaps:

- Helium is not formally classified as a critical mineral within Australia's national framework, which limits access to concessional finance mechanisms available through bodies such as Export Finance Australia and the Critical Minerals Facility

- Exploration licensing for helium-specific activities varies across state jurisdictions, creating inconsistency for companies operating multistate programs

- Policy discussions around reclassifying helium as a critical mineral are understood to be ongoing, and formal reclassification would represent a material positive for the sector's development timeline

Market structure challenges:

- The global helium distribution system is dominated by a small number of large industrial gas companies including Air Products, Linde, and Air Liquide, which control significant portions of the offtake and logistics chain

- Helium pricing does not occur on public commodity exchanges, making price discovery complex and contract negotiation more opaque than in most mineral markets

- Emerging Australian producers will need either to negotiate with incumbent distributors or develop direct long-term relationships with end-users in the semiconductor and medical sectors

The next major ASX story will hit our subscribers first

Potential Export Markets and Australia's Competitive Positioning

Where Australian Helium Would Flow

Australia's existing trade architecture provides a meaningful head start in identifying and developing export relationships for helium. The most strategically aligned potential markets are:

| Market | Primary Helium Demand Driver | Australia's Strategic Advantage |

|---|---|---|

| Japan | Semiconductor manufacturing, medical MRI | Deep LNG trade relationship, bilateral trust |

| South Korea | Advanced chip fabrication | Strong bilateral trade ties, proximity |

| Taiwan | Global semiconductor hub, TSMC and peers | Critical supply chain alignment |

| United States | Aerospace, defence, medical technology | Five Eyes security partnership |

| European Union | Industrial manufacturing, scientific research | Diversification from Russian supply |

Taiwan's semiconductor industry warrants particular attention. Companies like TSMC operate fabrication facilities that collectively consume enormous volumes of helium annually. Supply diversification away from Middle Eastern and Russian sources is a strategic imperative for these manufacturers, and a stable, high-quality Australian supply source would represent a compelling alternative. The geopolitical resource pressure reshaping global supply chains is, furthermore, directly accelerating these diversification conversations.

Frequently Asked Questions: Australia Helium Extraction and the Iran War Supply Impact

Why is helium irreplaceable in semiconductor manufacturing?

Helium's role in chip fabrication stems from its unique physical properties, specifically its extremely low boiling point of -269 degrees Celsius and its chemically inert nature. It is used to maintain ultra-clean, ultra-cold environments during critical process steps including lithography and ion implantation. No commercially viable substitute currently exists for these specific applications. The consequences of supply disruption for semiconductor manufacturers are therefore not merely economic — they are operational.

How has the Iran conflict created direct helium supply pressure?

The Persian Gulf region is a critical transit corridor for Qatari helium exports destined for Asian and European markets. Conflict escalation has introduced shipping risk, elevated insurance premiums, and route diversion costs that raise the landed price of helium across import-dependent markets. Because helium cannot be economically stockpiled, even moderate supply disruptions translate rapidly into market tightness. The 2025 commodity outlook highlights how this dynamic is now being priced into longer-term resource investment frameworks.

What helium purity levels make a project commercially viable?

Commercial helium extraction from natural gas typically becomes viable at feed gas concentrations above approximately 0.3 percent helium. Projects reporting concentrations significantly above this level, particularly those approaching the figures cited by some South Australian explorers, represent exceptional resource quality that substantially improves extraction economics by reducing the volume of gas that must be processed to recover a unit of helium product.

When could Australian helium exports realistically begin?

Based on exploration timelines, capital requirements for processing infrastructure, and regulatory approval pathways, early-stage Australian helium projects are broadly targeting production commencement within a 3 to 7 year window. South Australian projects with high-purity helium concentrations and simpler extraction profiles may be positioned toward the earlier end of that range, while projects requiring greenfield processing infrastructure face longer development timelines.

Does Australia currently produce any helium?

As of late 2023, Australia has no active domestic helium production following the closure of the Darwin extraction facility. All helium consumed domestically is currently sourced through imports, a situation that creates a strategic vulnerability across healthcare infrastructure and technology manufacturing supply chains within the country.

The Larger Picture: A Generational Reorientation of Helium Supply Geography

Geopolitical disruption has a documented historical pattern of permanently accelerating supply chain diversification. The 1970s oil shocks produced lasting changes in energy infrastructure investment that reshaped global production geography over the following two decades. The Iran conflict's impact on helium supply appears to be following a similar dynamic, compressing timelines for investment decisions that might otherwise have been deferred.

Australia's combination of factors is unusual in the global resource landscape. A large estimated resource base, ancient geology with documented helium-generating capacity, existing export infrastructure from the LNG sector, stable governance, and established trade relationships with the world's largest helium-consuming nations create an alignment of opportunity that is genuinely rare. As noted by Stockhead's analysis of Iranian conflict chokepoints, the companies and countries with credible alternative supply solutions are increasingly well-positioned to capture long-term market share.

The primary risk is not geological or commercial. The financial modelling suggests compelling economics even under base-case assumptions. The primary risk is the pace of policy and capital mobilisation. Geopolitical disruption creates windows of strategic opportunity, but those windows do not remain open indefinitely. Nations and industries that move decisively during supply crises tend to capture long-term market positions that prove durable even after the immediate crisis resolves.

Final Strategic Assessment: The Australia helium extraction and Iran war supply impact story ultimately comes down to timing. Australia holds an estimated 3.6 billion cubic metres of helium, equivalent to roughly 21 years of global consumption. The Iran conflict has compressed the timeline for global buyers to seek non-Middle Eastern alternatives. Whether Australian policy frameworks and private capital mobilise quickly enough to convert that geological endowment into export reality will determine whether Australia captures a generational economic opportunity or watches it migrate to competing jurisdictions.

This article contains forward-looking analysis, financial modelling references, and scenario projections that involve inherent uncertainty. The financial metrics cited are derived from academic modelling and do not constitute financial advice. Readers should conduct their own due diligence before making investment decisions related to any company or sector discussed herein.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical and emerging commodities like helium — instantly translating complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the broader market.