June 6, 2026

The Invisible Resource Quietly Powering the Modern World

Few industrial materials carry the paradox that helium does. It is simultaneously one of the most abundant elements in the universe and one of the most critically scarce resources on Earth. Unlike water, metals, or even rare earth elements, helium cannot be recycled from the environment once it escapes containment. The physics are unforgiving: helium molecules are so light that atmospheric release sends them on a one-way journey upward, eventually beyond Earth's gravitational pull entirely. Every cubic metre vented into the sky is gone from the planet's accessible inventory forever.

This irreversibility places helium in a completely different risk category from virtually every other industrial input. Right now, a convergence of geopolitical disruption, accelerating technology demand, and policy inaction is forcing a reassessment of where future supply will come from. Australia helium extraction, sitting on potentially significant untapped reserves, finds itself at the centre of that conversation, and the helium supply crisis unfolding globally has made that positioning increasingly urgent.

When big ASX news breaks, our subscribers know first

Why Helium Is Not Like Other Industrial Gases

From Radioactive Decay to Pressurised Reservoirs

Understanding why helium is so scarce on Earth requires stepping back into deep geological time. Helium is not manufactured or synthesised. It forms exclusively through the radioactive decay of heavy elements, primarily uranium and thorium, deep within the Earth's crust. This process unfolds across timescales measured in millions of years. The resulting helium migrates slowly upward through permeable rock until it becomes trapped in geological structures, often alongside accumulations of natural gas.

This co-location with natural gas is both helium's greatest discovery opportunity and its most persistent vulnerability. When natural gas fields are developed without dedicated helium recovery infrastructure, the helium contained in what engineers call "tail gases" is simply vented or flared, destroying in seconds what the Earth took geological epochs to produce.

The fact that helium only liquefies at -269 degrees Celsius, making it the coldest known liquid substance, is not merely a scientific curiosity. It is the physical property that makes helium irreplaceable across several of the world's most critical industries.

How Critical Is Helium to the Modern Economy?

The Semiconductor and AI Infrastructure Connection

The global expansion of artificial intelligence infrastructure is quietly intensifying helium demand in ways that most analysts have been slow to factor into supply models. Semiconductor fabrication relies on helium at multiple stages: as a purge gas in diffusion furnaces, as a carrier gas in chemical vapour deposition, and as a leak detection medium due to the exceptionally small size of helium molecules. As AI data centre buildout accelerates, the upstream pressure on chip manufacturing scales with it.

According to Arup George, an engineer at the University of New South Wales, the advanced semiconductor chips underpinning AI systems require extraordinarily complex manufacturing processes, and helium is integral to maintaining the contamination-free environments those processes demand. Its chemically inert nature means it interacts with nothing, contaminates nothing, and can safely purge even the most sensitive fabrication environments (ABC News, May 2026).

Medical Imaging and the Superconducting Magnet Dependency

MRI machines represent perhaps the most visible and non-negotiable application for helium. The superconducting magnets that generate the powerful magnetic fields required for high-resolution imaging must be cooled to temperatures approaching absolute zero, a requirement only liquid helium can meet with current technology. Critically, this is not a one-time fill. Liquid helium evaporates gradually from MRI systems, requiring regular replenishment to maintain operational temperatures.

Brisbane-based medical technology startup Magnetica is among those actively working to reduce this dependency, developing compact MRI systems designed for limb imaging that use helium in gas form rather than liquid form and target substantial reductions in overall helium consumption. While such innovations represent an important directional shift, the global installed base of conventional MRI machines remains overwhelmingly dependent on liquid helium supply chains.

Additional High-Demand Sectors

Beyond semiconductors and medical imaging, helium serves critical functions across:

- Aerospace propulsion – used to purge and pressurize hydrogen rocket fuel systems

- Precision leak detection – the preferred tracer gas for identifying microscopic failures in sealed systems

- Cryogenic research – fundamental to low-temperature physics experiments and quantum computing development

- Fibre optic cable manufacturing – used as a cooling and protective atmosphere during fibre drawing processes

- Nuclear energy – employed as a coolant in certain advanced reactor designs

The convergence of demand from AI infrastructure, healthcare expansion, and emerging quantum technologies means multiple high-growth sectors are simultaneously competing for the same finite, non-substitutable resource, with no viable alternative in sight for most critical applications.

The Global Helium Supply Map in 2026: A Concentrated and Fractured Market

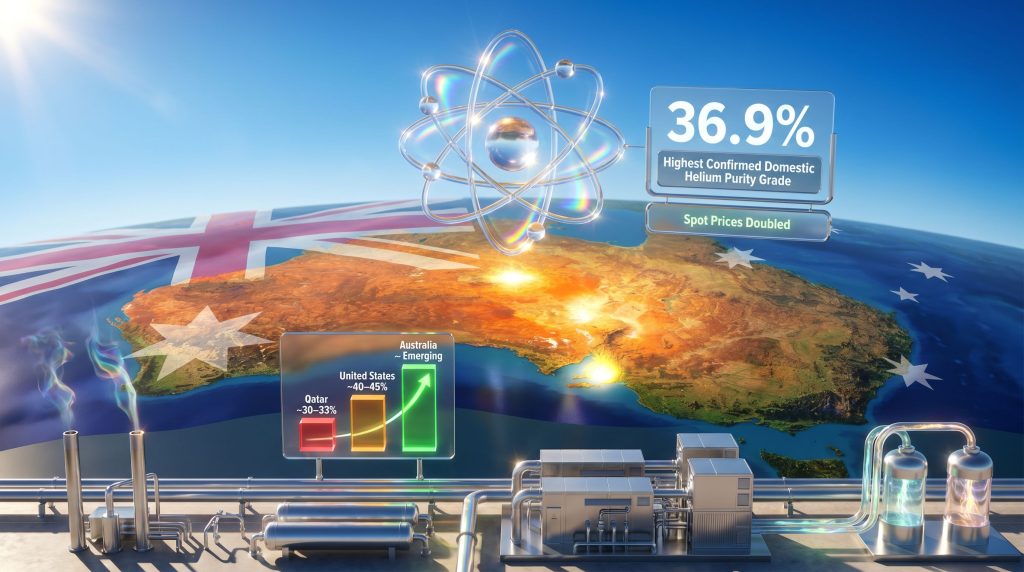

A Shock That Removed One-Third of Global Supply Overnight

In March 2026, Iranian missile strikes on Qatar's Ras Laffan industrial complex caused severe disruption to one of the world's largest helium processing facilities. The consequences for global supply were immediate and severe. Helium spot prices doubled in the aftermath, and long-term contract rates began trending upward as buyers scrambled to secure alternative sources (ABC News, May 2026).

| Supply Region | Approximate Global Share (Pre-2026) | Current Status |

|---|---|---|

| Qatar (Ras Laffan) | ~30-33% | Severely disrupted by missile strikes, March 2026 |

| United States | ~40-45% | Operational but drawing on finite federal reserves |

| Russia | Significant minority share | Constrained by international sanctions |

| Algeria and Others | Smaller contributions | Stable but limited in scale |

What the table above illustrates is a dangerously concentrated market. With Qatar disrupted and Russian output effectively constrained by sanctions, the global helium industry has simultaneously lost its second and third largest producers. The United States, while still operational, has been drawing down its federal helium reserve at Cliffside Field in Texas for decades. That reserve has been progressively sold off under federal legislation, and its long-term availability as a global buffer is inherently limited.

This triple compression of supply creates what supply chain analysts describe as a structural vacuum — a gap in global availability that cannot be filled quickly by any single alternative source, and that is pushing industrial buyers to reassess their geographic diversification strategies. Furthermore, the broader implications for critical minerals energy security are becoming increasingly difficult for policymakers to dismiss.

Where Does Australia Fit? From Producer to Importer and Back Again

The 2023 Darwin Closure and What Australia Lost

Australia's only domestic helium production facility, operated in Darwin in connection with Santos gas supply, ceased operations in late 2023 after its associated gas reserves were exhausted (ABC News, December 2023). With that closure, Australia became entirely dependent on imports for all domestic helium consumption, joining a long list of nations with no domestic production capability.

The timing of that closure, viewed against the supply disruptions of 2026, makes the loss of domestic production capacity particularly acute. Australia is now importing a resource that research suggests it may hold in commercially viable quantities across significant portions of its existing gas processing infrastructure.

The LNG Co-Extraction Opportunity: Billions Being Vented

Research conducted through the Future Energy Export Cooperative Research Centre (FEnEx CRC), led by Professor Eric May, estimates that helium is likely present in commercially meaningful concentrations at up to six of Australia's ten natural gas processing plants (ABC News, May 2026). Under current operations, any helium present in processed gas streams is released with tail gases into the atmosphere. The FEnEx CRC's opportunities report provides a compelling case for why this represents one of Australia's most overlooked industrial opportunities.

The economic modelling around LNG co-extraction retrofits is compelling. Academic analysis suggests that adding nitrogen rejection units capable of capturing helium from existing gas processing streams could achieve a discounted payback period of approximately 2.4 years under current price conditions. That figure, always subject to site-specific variation and capital cost assumptions, nonetheless points to a potentially high-return infrastructure investment.

Professor May has argued publicly that Australia could extract substantially greater value from its natural gas assets if operators invested in helium recovery infrastructure. Without financial incentives, however, LNG operators have no commercial reason to make those capital investments, meaning the helium continues to be systematically destroyed through routine venting operations (ABC News, May 2026).

Australia's Active Helium Exploration Landscape

South Australia: World-Leading Purity Grades

The most striking geological development in Australian helium extraction has come from the Yorke Peninsula in South Australia. Gold Hydrogen, an ASX-listed company focused on natural hydrogen and helium discovery, has reported helium concentrations of 36.9 percent purity at its exploration sites, a figure described by managing director Neil McDonald as a world-leading discovery (ABC News, May 2026).

Crucially, this resource is described as "green helium," meaning it exists independently of any natural gas or LNG formation. This distinction matters commercially because it allows production without the infrastructure, regulatory complexity, and emissions profile associated with fossil fuel co-extraction. Gold Hydrogen is targeting commercial production within approximately two years, though achieving that timeline requires hundreds of millions of dollars in capital investment for extraction and processing infrastructure.

Other Australian Basins With Helium Potential

-

Northern Territory (Amadeus Basin): Prior drilling programs have intersected helium grades reported as high as 9 percent in subsalt geological zones. Companies including Central Petroleum are re-examining historical well data specifically through a helium-focused lens, recognising that earlier exploration was conducted with hydrocarbon economics as the primary objective.

-

Western Australia: Georgina Energy is progressing evaluation of its Hussar and Mt Winter project areas, which have been identified as hosting a large prospective helium resource footprint. These projects remain at an assessment stage.

-

Tasmania: Natural Helium Tasmania is developing a production model built around helium deposits independent of fossil fuel infrastructure, with renewable-powered processing as a core design principle. The company has flagged a commercialisation target of 2026 to 2027.

The next major ASX story will hit our subscribers first

The Onshore Refining Multiplier: Raw Gas Is Only the Beginning

One of the least discussed but most financially significant aspects of Australia's helium opportunity lies not in extraction itself but in downstream processing. Raw helium extracted from the ground requires purification to reach the high-purity grades demanded by semiconductor manufacturers and medical device producers.

As Dr Arup George of the University of New South Wales has noted, the real value in the helium supply chain sits at the refined end. Possessing the raw material is a starting point, but delivering a highly processed, application-ready product is where margins and strategic value are maximised (ABC News, May 2026). An Australian industry that stops at wellhead extraction captures only a fraction of the available economic opportunity. Onshore refining to export-grade purity transforms helium from a bulk commodity into a precision industrial input, commanding substantially higher pricing and stronger long-term offtake relationships with technology sector customers.

The Critical Minerals Listing Debate: The Policy Lever That Determines Everything

Why Australia Removed Helium From the List in 2023

Australia's federal government removed helium from its critical minerals list in 2023. At the time, the government stated the decision aligned with its strategic partnership frameworks. Critics of the decision argue it effectively removed the commercial incentives — including federal tax concessions and investment support eligibility — that would have encouraged LNG operators to invest in co-extraction equipment precisely during the period when global supply was tightest. This decision sits awkwardly alongside the broader critical minerals policy direction being pursued by major trading partners, particularly the United States.

Policy gap: Australia's removal of helium from its critical minerals list in 2023 eliminated the financial incentives that could have driven LNG operators toward co-extraction investment. The window that decision closed coincides almost exactly with the global supply crisis that emerged in 2026.

What Reinstatement Would Actually Provide

Critical minerals listing in Australia delivers a specific set of commercial enablers:

- Eligibility for federal tax concessions under the critical minerals production tax incentive framework

- Access to government-backed financing support through institutions such as Export Finance Australia

- Strategic signalling to international capital markets that the resource carries sovereign priority

- Potential inclusion in bilateral supply agreement discussions with technology sector partners in Asia and North America

The Resources Minister's office, responding to questions in May 2026, indicated the government would continue monitoring supply chain disruptions but stopped short of committing to any policy change, noting that the United States also produces helium as a partial offset to global supply concerns (ABC News, May 2026).

Can Emerging Technologies Reduce Helium Demand?

Conservation Measures and Their Structural Limits

Several technological developments are gradually reducing per-unit helium consumption across key sectors:

- Closed-loop helium recycling systems in industrial and laboratory settings can recover and reuse a meaningful proportion of helium that would otherwise be vented

- Low-helium MRI designs, such as those being developed by Magnetica, reduce the ongoing coolant requirements for new installations

- Semiconductor process optimisation has improved helium utilisation efficiency at some fabrication nodes

However, these efficiency improvements are unlikely to offset the structural demand growth being driven by AI infrastructure expansion and global healthcare system development. The installed base of existing MRI machines alone represents a multi-decade ongoing demand commitment. As semiconductor fabrication scales to meet AI chip demand, the aggregate consumption trajectory points upward even with per-unit efficiency improvements factored in. In addition, the surging critical minerals demand across adjacent sectors only compounds the challenge.

Australia vs. The World: A Comparative Supply Framework

| Country | Primary Source | Reserve Status | Strategic Advantage |

|---|---|---|---|

| United States | Cliffside Field and LNG co-extraction | Large but declining federal reserve | Established infrastructure and domestic demand base |

| Qatar | North Field LNG | Massive reserves; currently disrupted | Scale and cost efficiency when operational |

| Russia | East Siberia LNG | Significant but sanctions-constrained | Large untapped upside; geopolitically isolated |

| Tanzania | Dedicated helium fields | Emerging; early-stage development | Non-hydrocarbon origin; long-term potential |

| Australia | LNG co-extraction and standalone plays | Unproven at commercial scale; high-grade deposits confirmed | Geographic proximity to Asian technology supply chains |

Australia's geographic position relative to the Asia-Pacific technology corridor is an underappreciated strategic asset. South Korea, Japan, Taiwan, and increasingly Southeast Asian semiconductor hubs all represent high-volume helium consumers with a direct interest in supply chain diversification away from Middle Eastern and Russian sources. Furthermore, Australia's resource exports framework already provides established trade relationships that an emerging helium industry could leverage. An Australian helium export industry would offer those buyers a politically stable, geographically proximate alternative that no current major producer can match.

Three Scenarios for Australia's Helium Industry to 2030

Scenario 1: Policy Activation

Critical minerals reinstatement triggers LNG operator investment in co-extraction infrastructure. First commercial volumes reach market within three to four years. Australia re-establishes domestic production and begins modest exports to Asia-Pacific buyers.

Scenario 2: Market-Led Development

Sustained elevated spot prices make standalone helium projects like those in South Australia economically viable without policy support. Development timelines extend to five to seven years due to the absence of concessional financing. Australia returns to domestic self-sufficiency but misses the early export window.

Scenario 3: Structural Inaction

Without policy incentives or sustained price signals, LNG operators continue venting helium and greenfield projects fail to attract sufficient capital. Australia remains a pure importer while global supply gradually rebuilds through Qatar's recovery and emerging producers in Tanzania and North America.

Key Takeaways: Australia's Helium Extraction Opportunity at a Glance

| Factor | Current Status | Potential Upside |

|---|---|---|

| Domestic production | Zero (fully imported) | Up to six LNG plants with commercial co-extraction potential |

| Highest confirmed purity | 36.9% in South Australia | World-leading grade for standalone extraction |

| Critical minerals status | Delisted in 2023 | Reinstatement could unlock investment and tax incentives |

| LNG co-extraction payback | 2.4-year model estimate | Scalable across existing infrastructure network |

| Global price environment | Spot prices doubled post-March 2026 | Sustained elevation supports project economics |

| Research and technical readiness | Early-stage; frameworks under development | CSIRO and FEnEx CRC actively building knowledge base |

The arithmetic of Australia helium extraction is increasingly difficult to ignore. A non-renewable, strategically critical resource is being permanently destroyed through venting at existing gas facilities, while the global supply environment has shifted dramatically in favour of new producers. Whether the policy and capital frameworks align quickly enough to convert geological potential into commercial reality remains the central question for the industry over the next three to five years.

This article is intended for informational purposes only and does not constitute financial or investment advice. Statements involving future production timelines, project economics, price forecasts, and regulatory outcomes are inherently uncertain and subject to change. Readers should conduct independent research before making any investment decisions.

Want to Track ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across 30-plus commodities — including the emerging helium and critical minerals sector — ensuring subscribers can identify actionable opportunities the moment they are announced. Explore historic discoveries and the substantial returns they have generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.