July 15, 2026

The Uranium Equation: Why Supplying India Tests Every Assumption in Australia's Export Policy

The global energy transition has quietly rehabilitated nuclear power from pariah to priority. Governments across Europe, Asia, and North America are either extending reactor lifespans, commissioning new builds, or both. Underpinning this shift is a simple arithmetic problem: uranium demand is rising structurally, supply chains remain concentrated and fragile, and the nations that hold the ore are finding themselves at the centre of increasingly complex geopolitical negotiations.

Nowhere is that complexity more visible than in the Australia India uranium deal, formalised through an administrative arrangement signed in July 2026 during Prime Minister Narendra Modi's visit to Melbourne. The agreement activates a legal framework that has existed in principle since 2014 but remained effectively dormant for over a decade. What changed is not the law, but the political will to operationalise it, and the consequences of that decision ripple far beyond any single bilateral trade relationship.

When big ASX news breaks, our subscribers know first

A Deal Over a Decade in the Making

The bilateral nuclear cooperation agreement between Australia and India was originally signed in September 2014 and entered into force in 2015. At that point, it established the legal scaffolding for uranium trade but left the actual mechanics of implementation undefined. Australian governments of different political persuasions spent the following years wrestling with an unresolved tension: India is not a signatory to the Nuclear Non-Proliferation Treaty (NPT), and that status has never changed.

The July 2026 administrative arrangement resolves the implementation impasse by establishing the bilateral procedures required to actually move uranium from Australian mines to Indian reactors. Furthermore, understanding the broader uranium market dynamics helps contextualise why this moment carries such strategic weight. The core terms of the arrangement are structured as follows:

| Element | Detail |

|---|---|

| Announcement Date | July 9, 2026 |

| Occasion | PM Modi's visit to Melbourne alongside PM Albanese |

| Legal Foundation | 2015 Australia-India Nuclear Cooperation Agreement |

| Safeguards Mechanism | IAEA oversight under India-specific safeguards agreement |

| Declared Purpose | Civilian energy generation only |

| Separation Requirement | Verifiable separation of civilian and military nuclear programs |

| Commercial Terms | No specific volumes, values, or timelines disclosed |

Notably, no commercial contracts have been announced. The administrative arrangement is an enabling instrument, not a purchase order. The path from signed framework to delivered uranium still requires bilateral nuclear material accounting procedures, export approvals under the Australian Safeguards and Non-Proliferation Office (ASNO), and individually negotiated supply agreements between Australian producers and Indian buyers.

Understanding Australia's Unique Export Tracking System

One aspect of this deal that receives insufficient attention in mainstream coverage is the mechanics of how Australia actually monitors its uranium after it leaves the country. All Australian uranium exports are classified as Australian Obligated Nuclear Material (AONM), a chain-of-custody designation that travels with the material through processing, conversion, enrichment, and final use in a reactor.

This is more stringent than what many other uranium exporters require. The AONM system means that:

- Australian uranium must be used only in facilities explicitly approved under bilateral agreements

- Any re-transfer of AONM to a third country requires Australia's prior consent

- Physical inventories of AONM must be reported to ASNO at regular intervals

- Any deviation from approved use triggers a formal bilateral consultation process

In theory, this creates a robust chain of accountability. In practice, the system's effectiveness depends entirely on the accuracy of India's self-reporting and the capacity of IAEA inspectors to verify declared inventories at civilian facilities. This is where the architecture meets its practical limits.

The Non-NPT Problem: Why India Is a Special Case

India's nuclear status is genuinely unique in the international system. It is one of only four states known to possess nuclear weapons that never signed the NPT, alongside Pakistan, Israel, and North Korea. Unlike North Korea, which withdrew from the treaty after joining it, India simply never acceded to the NPT framework at all.

This creates a structural asymmetry. NPT member states in good standing are subject to comprehensive safeguards, meaning the IAEA has the right to inspect and verify the entire nuclear fuel cycle. India, by contrast, operates under an India-specific safeguards agreement negotiated following the landmark 2008 U.S.-India Civil Nuclear Agreement (the 123 Agreement). Under this arrangement, India designates certain facilities as civilian and subjects them to IAEA inspection, while retaining a separate, unsafeguarded military programme.

The critical vulnerability in this structure is what non-proliferation analysts call fuel cycle fungibility. Even if Australian uranium is physically directed to a declared civilian reactor, that reactor's operation frees up India's domestically mined uranium for other applications, including its weapons programme. The uranium atoms are different, but the net effect on India's total nuclear fuel budget is the same.

This fungibility argument was the central contested point during U.S. Congressional debate over the 123 Agreement in 2008, and it has never been satisfactorily resolved. Australia is now navigating the same unresolved terrain.

How Australia Compares to Other Uranium Exporters

A common response to non-proliferation concerns is to point out that Australia is not breaking new ground. Multiple nations already supply uranium to India under comparable safeguard arrangements. However, the uranium supply and demand pressures shaping this landscape make Australia's entry into the market particularly consequential.

| Exporting Country | Framework | India Supply Status |

|---|---|---|

| Canada | Strict NPT and safeguards conditions | Active supplier |

| Kazakhstan | Less restrictive export policies | Active supplier |

| Russia (Rosatom) | State-directed; geopolitical factors | Active supplier and reactor constructor |

| France | EU framework; civilian-use conditions | Active supplier |

| Uzbekistan | Bilateral arrangements | Active supplier |

| Australia | AONM tracking; IAEA safeguards | Active as of 2026 |

The counterargument is straightforward: if Australia refuses to supply India, other nations with considerably less stringent tracking requirements will simply fill the gap. Australia's participation at least brings AONM accountability into the supply chain. Whether this logic holds under sustained scrutiny depends on how one weighs the normative function of non-proliferation norms against their practical enforcement capacity.

How Does the Russian Uranium Situation Factor In?

Geopolitical disruption has also reshaped the global supply picture. The Russian uranium import ban introduced by the U.S. Senate has accelerated the search for alternative supply sources. This dynamic, consequently, strengthens the strategic case for Australia expanding its role as a reliable, transparent uranium exporter to allied and partner nations, including India.

India's Nuclear Ambitions and the Scale of Demand

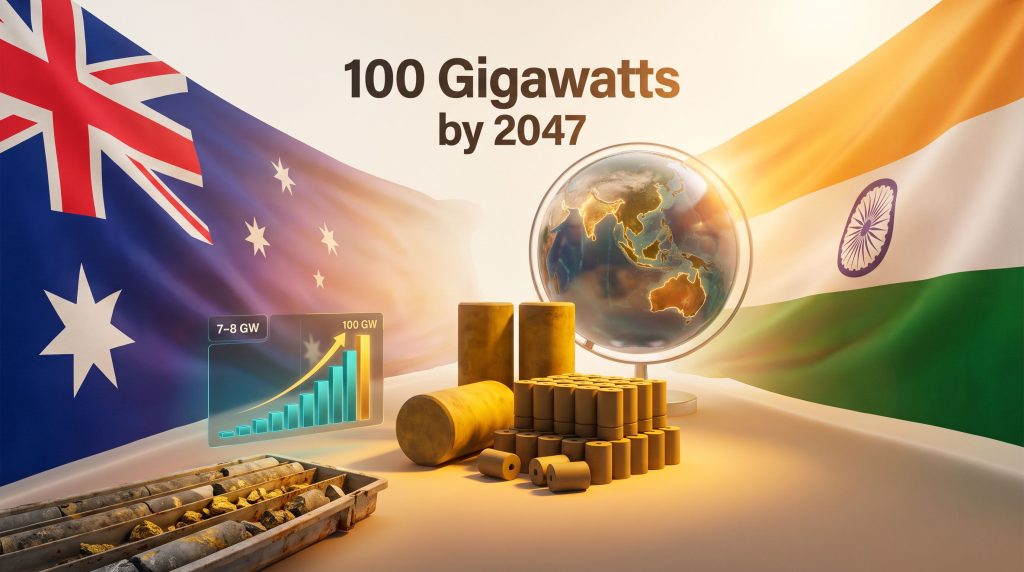

To understand why this deal matters economically, it helps to appreciate the extraordinary scale of India's nuclear energy plans. India has committed to reaching 100 gigawatts of installed nuclear capacity by 2047, timed to coincide with the centenary of its independence.

The gap between ambition and current reality is staggering:

| Metric | Figure |

|---|---|

| Target nuclear capacity (2047) | 100 GW |

| Current installed capacity (approx. 2025) | 7-8 GW |

| Required expansion multiplier | More than 10x |

| New reactors required | Dozens of large units over 20+ years |

Achieving this target would require India to sustain one of the most aggressive nuclear construction programmes in history. Every reactor added to that fleet requires a continuous supply of uranium fuel. Australia, holding approximately 28% of the world's known uranium reserves, represents a tier-one potential source for that supply chain. Global uranium reserves of this magnitude give Australia considerable leverage in shaping the terms of long-term supply relationships.

The scale of India's ambition also means that demand certainty, if contractually locked in, could justify capital investment in expanding Australian uranium production capacity. Olympic Dam in South Australia, operated by BHP, contains the world's largest known uranium deposit, though its uranium output has historically been constrained by the ore's polymetallic nature and processing bottlenecks. A long-term offtake relationship with India could change the economic calculus for expansion investment.

The next major ASX story will hit our subscribers first

What the Deal Means for Australia's Strategic Trade Posture

The uranium arrangement is not an isolated transaction. It fits within a deliberate recalibration of Australia's resource export relationships, reducing concentration risk associated with over-reliance on any single trading partner. According to the AFR, uranium miners are already positioning to capitalise on the deal's commercial opportunities. India's rapid economic expansion and the scale of its long-term energy needs make it a strategically significant destination for Australian resource exports across multiple commodity categories.

The broader Australia-India partnership framework now encompasses:

- Critical minerals supply chain cooperation

- Green hydrogen development pathways

- Renewable energy technology collaboration

- Defence and security engagement

- Nuclear fuel supply as a newly operationalised element

Within this architecture, the uranium deal carries symbolic as much as commercial weight. It signals that Australia is prepared to extend its resource partnership with India into strategically sensitive territory, reflecting a deepened level of bilateral trust.

Three Scenarios for How This Plays Out

Given the complexity of the implementation pathway, projecting outcomes requires acknowledging genuine uncertainty across multiple dimensions.

Scenario 1: Smooth implementation and deepened bilateral ties

IAEA safeguards function as designed, civilian-military programme separation holds, and Australian uranium becomes an established component of India's reactor fuel supply chain. Commercial contracts are progressively negotiated, providing demand certainty for Australian producers. This scenario requires sustained political commitment in both capitals and stable IAEA oversight capacity over a multi-decade horizon.

Scenario 2: Implementation stalls due to administrative and regulatory friction

The pattern of the previous decade repeats itself. ASNO approval processes, political sensitivity in Australia, and the complexity of bilateral nuclear material accounting procedures combine to delay commercial flows for years. The deal remains diplomatically significant but delivers limited near-term benefit to the Australian uranium sector.

Scenario 3: Non-proliferation backlash reshapes the policy environment

A regional nuclear escalation event or credible evidence of fuel diversion triggers renewed global scrutiny of uranium supply arrangements with non-NPT states. Australian domestic political pressure forces a policy review. The deal becomes a liability in Australia's diplomatic positioning rather than an asset, particularly if it is perceived as having weakened non-proliferation norms during a period of elevated risk.

The Investment Dimension: What ASX Uranium Investors Should Consider

The following section involves forward-looking analysis and should not be construed as financial advice. Investors should seek independent professional advice before making investment decisions.

The formalisation of the Australia India uranium deal introduces a new demand signal into the Australian uranium investment narrative. In addition, broader uranium investment trends suggest that structural demand growth is already reshaping how capital is being allocated across the sector. Key considerations for market participants include:

- Production concentration risk: Australia's uranium output remains concentrated at a small number of operating assets. Expanded demand from India does not automatically translate to expanded production without capital investment and regulatory approvals.

- Long-term contract versus spot exposure: India's nuclear utilities have historically sought long-term supply agreements rather than spot market purchases. This favours producers capable of guaranteed delivery over extended contract terms.

- Junior explorer sensitivity: ASX-listed uranium explorers and developers may see renewed investor interest as the strategic case for Australian uranium production strengthens, though this sentiment-driven movement may precede commercial reality by years.

- Processing bottlenecks: The conversion of uranium ore to the yellowcake (uranium oxide) form required for export involves processing constraints that are independent of reserve size. Investment in processing infrastructure may be as important as resource base expansion.

- Uranium spot price dynamics: Formalised large-scale supply arrangements between Australia and India, once operationalised, would represent a structural addition to long-term contract demand. This has historically been supportive of uranium price stability, though spot price movements are driven by multiple global factors simultaneously.

The Deeper Question: What Norms Are Being Set?

Perhaps the most significant aspect of the Australia India uranium deal is not what it does now, but what it signals for the future. Nuclear governance relies heavily on norms — the shared expectations about what is acceptable behaviour that operate alongside formal treaty obligations.

The NPT architecture was built on the premise that access to civilian nuclear technology would be conditional on non-proliferation commitments. The various exceptions made for India, beginning with the 2008 123 Agreement and now including Australia's administrative arrangement, collectively erode the conditionality that gives the NPT its normative force.

World Nuclear News reports that the agreement is broadly seen as a landmark step in civilian nuclear cooperation, though its long-term non-proliferation implications remain actively debated. At a time when global nuclear risk is being assessed more seriously than at any point since the Cold War, the question of whether economic and strategic logic can routinely override non-proliferation principle is not abstract.

Australia is a mid-sized power with an outsized role in global non-proliferation diplomacy relative to its size. How it manages its uranium export relationships contributes to the normative environment in which those norms either hold or gradually dissolve.

The yellowcake question — whether Australia can export uranium to India while maintaining the credibility of its non-proliferation commitments — does not have a clean answer. What it has is a set of trade-offs that will play out across decades of reactor operation, diplomatic engagement, and global nuclear risk management. The July 2026 administrative arrangement is not the end of that conversation. It is the moment Australia formally chose a side in it.

Want to Track ASX Uranium Opportunities as Australia's Nuclear Export Story Unfolds?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including uranium — instantly translating complex market developments into actionable insights for investors at every level. Explore historic examples of major discovery returns and begin your 14-day free trial today to position yourself ahead of the market.