June 14, 2026

The Quiet Metal Making the Loudest Argument for Long-Term Investors

There is a peculiar pattern in commodity markets where the most consequential materials rarely attract the loudest headlines. Gold captures imaginations. Lithium ignites speculative frenzies. Yet copper, the unglamorous workhorse of modern civilisation, is quietly assembling one of the most compelling structural investment cases in the resources sector. For long-term investors tracking the BHP copper growth story, the convergence of forces now bearing down on supply and demand dynamics represents something genuinely rare: a thesis supported by physics, economics, and geology simultaneously.

Understanding why requires moving beyond the surface-level narrative and examining the underlying mechanics of how copper actually flows through an industrialising, electrifying, and increasingly digitised global economy.

When big ASX news breaks, our subscribers know first

Three Demand Forces That Cannot Be Switched Off

Copper's unique physical properties make it effectively irreplaceable across three of the most powerful structural trends of this decade. Its exceptional electrical conductivity, thermal management characteristics, and resistance to corrosion mean that substituting alternative materials typically involves significant performance trade-offs in applications where reliability is non-negotiable.

Electrification and the EV Multiplier Effect

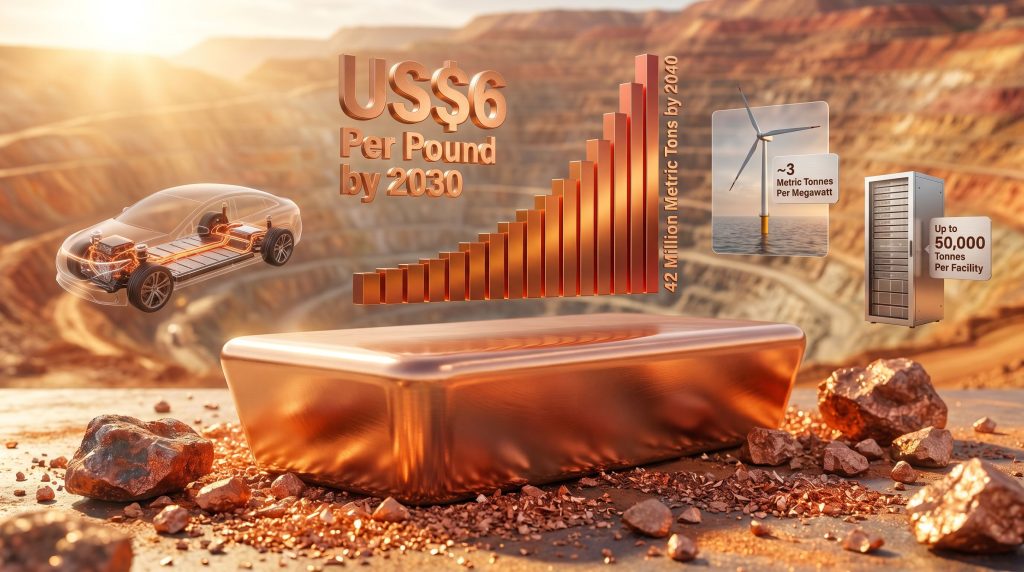

The shift from internal combustion engines to electric vehicles creates a copper demand multiplier that many investors underestimate. A conventional petrol-powered car contains roughly 20 to 25 kilograms of copper. An electric vehicle requires approximately three times that volume, incorporating copper in motors, battery systems, charging infrastructure, and power electronics. As the global EV fleet expands across hundreds of millions of vehicles over the coming decades, the cumulative tonnage requirement becomes staggering.

Wind energy compounds this dynamic. Each megawatt of wind power generation capacity requires approximately three metric tonnes of copper, embedded in turbine generators, cabling, and grid connection infrastructure. Solar installations and grid-scale battery storage systems add further layers of copper intensity to an already demand-heavy picture.

The AI Infrastructure Wildcard

Perhaps the least understood demand vector in copper markets is the explosive growth of artificial intelligence infrastructure. A January 2026 analysis by S&P Global projected that data centre electricity consumption across the United States could climb from roughly 5% of total national power demand to as much as 14% by 2030. That kind of electricity demand growth requires transformative investment in grid infrastructure, cooling systems, and physical wiring at every level of the network.

At the facility level, individual hyperscale data centres may require up to 50,000 tonnes of copper each, accounting for power distribution wiring, grounding systems, server interconnects, and thermal management equipment. This single demand vector is reshaping how analysts model copper's long-term price floor, because AI infrastructure spending is being driven by capital-rich technology companies operating largely independently of traditional commodity demand cycles.

Urbanisation in Emerging Markets: The Decades-Long Runway

Beyond electrification and digital infrastructure, the long-arc driver of copper demand remains the urbanisation of emerging economies. Building the electrical grids, transportation networks, and residential infrastructure of rapidly developing cities across Asia, Africa, and Latin America requires enormous volumes of copper. This driver is not tied to any single technology cycle and represents a baseline demand trajectory with decades of momentum remaining.

Demand Projections: What the Numbers Actually Say

S&P Global's modelling projects global copper demand reaching 42 million metric tonnes by 2040, representing a roughly 50% increase from current consumption levels. BHP's internal forecasts carry this further, with the company's own modelling suggesting annual global demand could exceed 50 million tonnes per year by 2050. These figures reflect the copper price drivers that analysts have consistently flagged as durable structural forces rather than cyclical noise.

The table below summarises the primary demand drivers and their copper intensity characteristics:

| Demand Driver | Copper Intensity | Growth Trajectory |

|---|---|---|

| Electric Vehicles | ~3x more copper than ICE vehicles | Global EV fleet expanding rapidly |

| Wind Turbines | ~3 metric tonnes per megawatt | Accelerating globally through 2035 |

| Hyperscale Data Centres | Up to 50,000 tonnes per facility | US power share rising to 14% by 2030 |

| Grid Upgrades and Solar | Substantial ongoing capital requirement | Multi-decade infrastructure cycle |

| Emerging Market Urbanisation | Long-term structural baseline | Decades of runway remaining |

Why Supply Cannot Simply Respond to Demand Signals

The copper supply side is governed by geological and regulatory realities that no amount of capital can quickly overcome. Opening a new copper mine from initial exploration through to sustained commercial production typically takes between 15 and 20 years. That timeline encompasses geological assessment, feasibility studies, environmental permitting, infrastructure development, and the physical construction of processing facilities in often remote locations.

This means the projects needed to meet copper demand beyond 2030 should, by any rational planning horizon, already be in active development today. The available evidence suggests the pipeline is deeply insufficient relative to what future demand will require. Furthermore, the copper supply crunch that analysts have long anticipated is now beginning to materialise in market data.

The International Copper Study Group projects the market will shift from a modest surplus in 2025 to a deficit exceeding 150,000 tonnes by 2026, with that shortfall widening considerably as the decade progresses. S&P Global's modelling adds a further dimension to this concern, estimating that mine output will peak around 2030 before beginning to decline as existing operations move through ageing ore bodies and falling average grades.

Declining Ore Grades: The Geological Headwind

One of the less-discussed structural challenges facing copper supply is the systematic deterioration in ore grade quality across the world's major producing regions. Ore grade refers to the concentration of copper metal within the rock being processed. As mines age, they progressively extract higher-grade ore first, leaving lower-grade material for later years.

This means that processing the same volume of rock produces progressively less metal over time, increasing both the energy and cost per tonne of copper produced. Many of the world's largest operating copper mines are experiencing this grade decline in real time, particularly those highlighted in the Chile copper outlook for 2025 and beyond. The practical consequence is that even with sustained or increased throughput volumes, actual copper production may stagnate or fall.

Analysts note that the combination of grade decline at existing operations and an underdeveloped project pipeline creates a structural supply gap that higher copper prices alone cannot rapidly resolve, given the fixed geological and regulatory timelines involved in bringing new capacity online.

The Price Outlook: Red Cloud Securities' US$6/lb Forecast

Red Cloud Securities has forecast copper averaging US$6 per pound by 2030, compared to current levels near US$5.47 per pound. The directional logic behind this forecast rests on the compounding interaction between structurally rising demand and a supply response constrained by geological, technical, and political factors that capital alone cannot eliminate. The commodity price impact of such a move would be consequential for major producers like BHP.

BHP's Copper Portfolio: Scale, Geography, and Structural Advantage

BHP Group currently produces between 1.9 and 2.0 million tonnes of copper per year, positioning it among the world's largest copper producers by volume. This output is generated across three major asset clusters spanning two continents. BHP's copper growth story is underpinned by this diversified asset base, which provides both scale advantages and geographic resilience.

Escondida, Chile: The World's Largest Copper Mine

Escondida, located in Chile's Atacama Desert at high altitude, is the world's single largest copper operation by output. The mine's scale provides cost advantages and processing efficiencies that smaller operations cannot replicate, though it also faces the grade decline challenges characteristic of a mature, large-scale operation. Chile as a jurisdiction carries both advantages and risks, including periodic political and regulatory uncertainty that investors in BHP should monitor.

Olympic Dam and Carrapateena: South Australia's Copper Heartland

Olympic Dam is one of the most geologically complex and strategically significant mining operations in the world. It is simultaneously a copper, uranium, gold, and silver operation hosted within a single giant ore body. The polymetallic nature of Olympic Dam creates revenue diversification that pure copper mines cannot offer, but also adds metallurgical and processing complexity.

In October 2025, BHP committed more than US$550 million to expand Olympic Dam, a capital commitment that signals genuine long-term conviction in the asset's future contribution. Carrapateena, a newer underground copper-gold operation also in South Australia, adds a higher-grade complementary asset to BHP's Australian copper portfolio.

Resolution Copper: A Generational Asset on the Horizon

BHP holds a 45% stake in Resolution Copper alongside Rio Tinto (ASX: RIO), an asset that represents one of the largest undeveloped copper deposits in the world. The deposit is estimated to be capable of producing approximately 40 billion pounds of copper across a 40-year mine life, a volume roughly equivalent to one quarter of projected US copper demand over that same period.

Resolution remains in development, navigating a complex permitting environment in Arizona. It is not a near-term production contributor, but its long-term optionality value is genuinely significant for investors evaluating BHP's copper exposure over a 10 to 20-year time horizon.

Copper Overtaking Iron Ore as BHP's Primary Earnings Engine

Perhaps the most strategically significant internal shift within BHP over recent years has been copper's rise relative to iron ore as an earnings contributor. For most of BHP's modern history, iron ore generated the dominant share of group profit, largely reflecting the extraordinary margins available during China's infrastructure construction boom.

As iron ore price dynamics have moderated and BHP's copper volumes and prices have improved, copper has emerged as the more dynamic earnings driver. The leveraged relationship between copper price movements and free cash flow is a critical feature of this transition. Because BHP's existing copper operations carry relatively fixed cost structures, incremental price improvement flows disproportionately into margin, creating significant earnings leverage to copper price appreciation.

BHP is targeting copper-equivalent production growth of 3% to 4% per year through 2035, a compounding rate that becomes increasingly powerful as the pricing environment improves toward the upper end of analyst forecasts. According to recent reporting, this copper surge has already begun powering record results for the company.

The next major ASX story will hit our subscribers first

Scenario Analysis: Mapping the Range of Outcomes

No investment thesis exists without uncertainty, and the BHP copper growth story carries meaningful risks alongside its structural tailwinds. The table below maps three plausible price scenarios and their implications:

| Scenario | Copper Price Range | Implication for BHP | Key Risk Factor |

|---|---|---|---|

| Bear | US$3.50–US$4.50/lb | Compressed margins, slower expansion capex | Demand slowdown, faster supply response |

| Base | US$5.50–US$6.00/lb | Strong free cash flow, full expansion proceeds | Moderate supply growth, stable demand |

| Bull | US$6.50–US$8.00/lb | Exceptional earnings leverage, accelerated M&A optionality | Supply deficit deepens, AI demand exceeds forecasts |

The bear case is not implausible. A sharper-than-expected slowdown in Chinese economic activity, a technology-driven substitution in specific applications, or a faster-than-anticipated supply response from new jurisdictions could pressure prices below the levels currently embedded in consensus forecasts. Investors should treat any copper price projection as a probabilistic range rather than a fixed outcome.

Capital Deployment: Organic Growth and Acquisition Optionality

BHP's management has been consistent in articulating a preference for organic growth as the primary driver of copper volume expansion, with acquisitions viewed as supplementary rather than essential. The company is estimated to hold approximately US$10 billion in redeployment capacity, providing meaningful optionality to pursue bolt-on acquisitions if appropriately priced opportunities emerge without requiring M&A to validate the growth thesis.

This balance sheet depth is itself a competitive advantage. Developing tier-one copper assets requires sustained capital commitment across multi-year timelines. Few companies can underwrite that level of expenditure without balance sheet distress. Consequently, well-considered copper investment strategies that account for this dynamic tend to favour producers with both scale and financial resilience.

Risks Investors Should Weigh Carefully

The BHP copper growth story is compelling, but intellectual honesty requires acknowledging its vulnerabilities:

- Execution risk in long-lead development projects is real. Olympic Dam's expansion and Resolution Copper's eventual development both involve technical complexity at scale.

- Geopolitical exposure in Chile, which hosts Escondida and contributes the largest share of BHP's copper output, warrants monitoring. Periodic shifts in Chilean mining taxation and environmental regulation have historically created uncertainty for operators.

- Production growth timelines are long. Targeting 2.5 million tonnes per year by the mid-2030s is credible but not guaranteed, and investors should expect variability along the path.

- Iron ore revenue has not fully disappeared from BHP's earnings mix, meaning macro headwinds to Chinese steel demand continue to influence overall group performance even as copper grows in relative importance.

Frequently Asked Questions: BHP Copper Growth Story

How much copper does BHP currently produce per year?

BHP produces approximately 1.9 to 2.0 million tonnes of copper annually across its Escondida, Olympic Dam, and Carrapateena operations.

What is BHP's copper production target for 2035?

BHP is targeting approximately 2.5 million tonnes of copper-equivalent production by the mid-2030s, supported by a 3% to 4% annual growth rate in copper-equivalent output.

Why is copper demand expected to increase so significantly?

Three converging forces are driving demand: the electrification of transportation and energy systems, AI-driven data centre infrastructure investment, and the long-term urbanisation of emerging economies. Each of these demand vectors is structurally durable and largely independent of the others.

What is Resolution Copper and why does it matter?

Resolution Copper is a large undeveloped copper deposit in Arizona, held 45% by BHP and 55% by Rio Tinto. The deposit is estimated to contain approximately 40 billion pounds of producible copper across a projected 40-year mine life, representing roughly 25% of projected US copper demand over that period.

How does BHP's copper exposure compare to other ASX-listed miners?

BHP's copper production scale is materially larger than any other ASX-listed mining company, with its 1.9 to 2.0 million tonne annual output dwarfing what other domestic peers produce. Rio Tinto has meaningful copper exposure through Oyu Tolgoi in Mongolia, but BHP's diversified copper portfolio across three major asset clusters gives it a broader production base.

What copper price is needed for BHP's expansion projects to be economically viable?

BHP has not publicly specified a single price threshold for project viability, but analyst modelling generally suggests its expansion capital remains economically justified at prices above approximately US$4.00 to US$4.50 per pound, providing a meaningful buffer below current spot levels.

Key Takeaways

- Global copper demand is projected to rise approximately 50% to 42 million metric tonnes by 2040, driven by electrification, AI infrastructure, EVs, and grid modernisation.

- New copper mines take 15 to 20 years to develop, and the current project pipeline is insufficient to close the post-2030 deficit without accelerated development activity.

- BHP produces approximately 1.9 to 2.0 million tonnes of copper annually and is targeting 2.5 million tonnes by the mid-2030s through primarily organic growth.

- Copper has emerged as BHP's primary earnings driver alongside iron ore, creating significant leverage to rising prices given the fixed-cost structure of existing operations.

- Resolution Copper alone represents approximately 40 billion pounds of production potential over 40 years, equivalent to roughly 25% of projected US copper demand over the same period.

- Red Cloud Securities forecasts copper averaging US$6 per pound by 2030, representing meaningful upside from current levels near US$5.47 per pound.

- BHP holds an estimated US$10 billion in redeployment capacity, providing disciplined acquisition optionality without depending on M&A to deliver on the copper growth thesis.

This article contains general information only and does not constitute personalised financial advice. Copper price forecasts cited represent third-party analyst projections and involve inherent uncertainty. Past performance of commodity prices and mining equities is not indicative of future returns. Investors should conduct independent research and consider their personal financial circumstances before making any investment decision.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights across copper and more than 30 other commodities. Explore how historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.