June 19, 2026

The Hidden Economics of Mining at Scale: Why Mega-Projects Almost Always Cost More Than Expected

There is a persistent gap in large-scale resource development between what engineers estimate at the outset and what projects ultimately cost to build. Across the global mining industry, this gap is not an anomaly — it is a pattern so consistent that it has become embedded in how institutional investors price risk into greenfield development assets. The larger and more technically complex the project, the wider that gap tends to be. Underground potash mining in remote geographies represents one of the most capital-intensive, technically demanding categories of resource development on earth, and the economics of BHP Jansen potash project impairment illustrate precisely why that risk premium exists.

The BHP Jansen potash project impairment of approximately US$2.3 billion, announced in June 2026, is not simply a line item in a financial report. It is a window into the structural forces that shape the economics of 21st-century mining at scale: construction inflation, underground engineering complexity, supply chain constraints, and the mathematics of recoverable asset value under revised cost assumptions.

When big ASX news breaks, our subscribers know first

Why Underground Potash Mining Carries a Different Risk Profile

To understand the Jansen impairment, it helps to understand what makes underground potash development fundamentally different from other forms of large-scale mining.

Open-cut mining operations, such as the iron ore operations that form the backbone of BHP's revenue base, involve relatively predictable cost structures. Equipment is accessible, ground conditions are visible during construction, and logistical challenges are manageable compared to deep underground work.

Underground potash mining reverses nearly all of those advantages:

- Shaft sinking to access deep ore bodies requires specialised equipment, extended timelines, and significant engineering precision

- Ground conditions underground cannot be fully assessed until construction is underway, creating scope risk that surface studies cannot eliminate

- Saskatchewan's potash deposits, while among the world's richest in terms of grade, king and permitting considerations, sit at depths typically exceeding 1,000 metres, requiring multi-year shaft development programs before any ore is accessible

- The specialised equipment used in deep underground mine construction has limited global supply, creating procurement bottlenecks that inflate both costs and timelines

- Labour markets in resource-heavy provinces like Saskatchewan tighten considerably during large construction phases, driving wage inflation above general market rates

The Jansen deposit sits within the Williston Basin in Saskatchewan, which hosts one of the largest known concentrations of potash reserves anywhere in the world. The ore body itself is not in question — it is the cost and complexity of accessing, developing, and scaling production that drives the economic sensitivity of the project.

What the Jansen Write-Down Actually Represents

Understanding Non-Cash Impairments in Mining Project Accounting

Before interpreting the significance of the BHP Jansen potash project impairment, it is worth clarifying what a non-cash impairment charge actually means in the context of resource project accounting under International Financial Reporting Standards (IFRS).

An impairment is triggered when the carrying value of an asset on the balance sheet exceeds the estimated recoverable amount of that asset. In mining, recoverable amount is calculated as the higher of an asset's fair value less costs of disposal, or its value in use — essentially, the net present value of expected future cash flows from the project.

When capital cost estimates for a project increase significantly, two things happen simultaneously:

- The total investment required to bring the asset to production rises, increasing the denominator in any return-on-capital calculation

- The net present value of future cash flows declines relative to the increased capital base, compressing the estimated recoverable amount

- If the revised recoverable amount falls below the carrying value on the balance sheet, an impairment must be recognised under IFRS

Critically, this is a non-cash accounting event. No money leaves BHP's accounts as a result of the write-down. Operating cash flow, dividend capacity, and the physical progress of the project are not directly affected. What changes is the reported book value of the asset and, consequently, reported net profit for the period in which the impairment is recognised.

This distinction matters significantly for investors assessing the real-world implications of the charge. Furthermore, understanding cut-off grade economics is essential context for appreciating how revised cost assumptions affect the threshold at which an ore body remains economically viable.

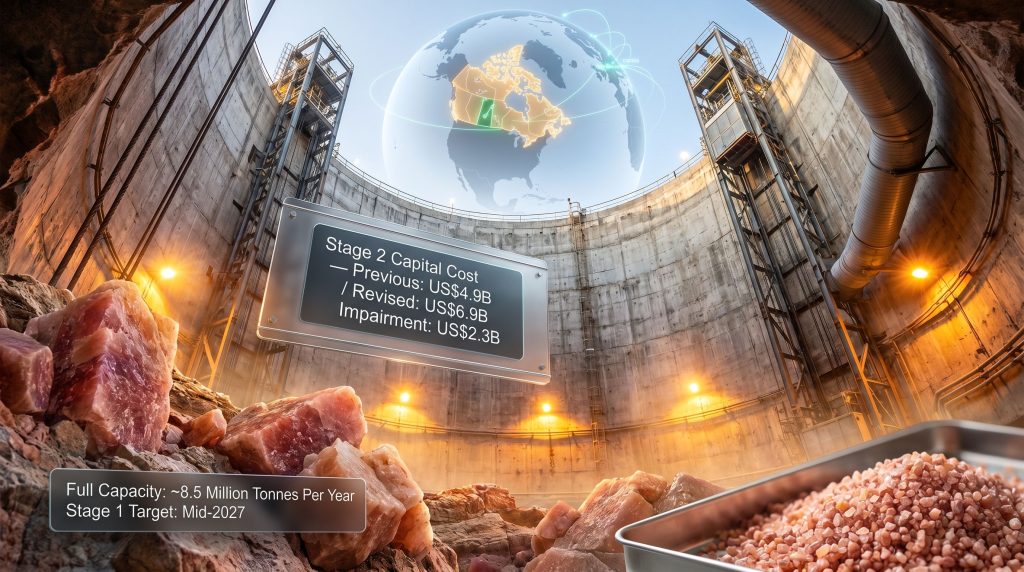

The Revised Numbers in Detail

| Metric | Previous Estimate | Revised Estimate |

|---|---|---|

| Jansen Stage 2 Capital Cost | US$4.9 billion | US$6.9 billion |

| Cost Increase | — | US$2.0 billion (+41%) |

| Impairment Charge | — | US$2.3 billion (non-cash) |

| Stage 1 First Production Target | — | Mid-2027 |

| Stage 2 Revised Timeline | — | 2031 |

| Full Ramp-Up Production Capacity | — | ~8.5 million tonnes per year |

The 41% increase in Stage 2 capital costs from US$4.9 billion to US$6.9 billion is the mechanical driver of the impairment. At this level of cost escalation, the project's revised internal rate of return (IRR) would fall below the threshold used to support the original carrying value, triggering the accounting recognition requirement.

A non-cash impairment does not necessarily signal project abandonment. In large-scale mining, write-downs frequently reflect updated cost modelling rather than fundamental shifts in commodity thesis. The critical question is whether the revised IRR remains above BHP's weighted average cost of capital at long-run potash price assumptions.

What Drove the Stage 2 Cost Escalation?

Several converging factors contributed to the Stage 2 cost revision:

- Construction sector inflation post-2022 materially increased the cost of all major mining construction programs globally, with concrete, steel fabrication, and mechanical installation costs all rising substantially

- Specialised underground mining equipment remains in constrained global supply, with delivery lead times extending significantly and vendor pricing reflecting that constraint

- Engineering scope revisions following updated geotechnical assessments of ground conditions at depth introduced additional support requirements and modified shaft design parameters

- Labour market tightening in Saskatchewan's resource sector, driven by competing large capital projects in the region, pushed construction workforce costs above initial budget assumptions

- Extended development timelines compound all of the above factors by extending the period over which cost inflation applies to ongoing construction expenditure

QC Intel reports that BHP's expected impairment on Jansen reflects precisely this confluence of inflationary and engineering pressures that have characterised large underground mine construction globally since 2022.

Stage 1 vs. Stage 2: Why the Distinction Is Critical for Investors

One of the most important dimensions of the Jansen situation that is frequently conflated in market commentary is the difference between Stage 1 and Stage 2 of the project. These are not simply sequential phases of the same development — they represent materially different risk, capital, and return profiles.

Stage 1 is BHP's primary near-term commitment. It remains on schedule for first production in mid-2027 and represents the project's proof-of-concept phase. Stage 1 will establish Jansen as an operating potash mine, generate initial cash flows, and provide real-world production data against which Stage 2 economics can be calibrated.

Stage 2 is the scaling mechanism that would eventually bring Jansen to its full production capacity of approximately 8.5 million tonnes per year, positioning it as one of the largest individual potash operations in the world. The cost escalation and resulting impairment relate primarily to Stage 2, and BHP's decision to push Stage 2 to a 2031 timeline creates a strategic optionality window for its board.

This staging structure is actually a sophisticated capital allocation feature of Jansen's design. By generating Stage 1 cash flows from 2027 onward, BHP can partially self-fund Stage 2 while also reassessing potash market conditions, construction cost trajectories, and the project's revised IRR before committing the full Stage 2 capital envelope. A definitive feasibility study framework helps contextualise why such staged commitments are considered best practice in managing capital risk across multi-decade mining assets.

The long-cycle nature of potash mining infrastructure means that staged development is not a retreat — it is a rational mechanism for managing capital risk across a multi-decade asset life.

Jansen's Role in the Global Potash Supply Chain

Why Potash Supply Geography Matters

Potash is the third major macronutrient required for crop production, alongside nitrogen and phosphorus. It cannot be manufactured — it must be mined, making geological endowment and geopolitical stability of producing regions directly relevant to global food systems.

The current structure of global potash supply is highly concentrated, creating inherent fragility:

- Canada (primarily Saskatchewan) and Russia/Belarus together account for the majority of global potash production capacity

- The 2022 sanctions imposed on Belarus following its government's actions against civil society created significant disruption to global potash trade flows, with Belarus historically supplying approximately 15-20% of global export volumes

- Russian potash exports have also faced logistics and financing complications stemming from broader geopolitical developments since 2022

- This supply concentration means that any new large-scale production capacity from politically stable, rule-of-law jurisdictions carries strategic value beyond its pure commercial economics

Saskatchewan's Williston Basin potash deposits are characterised by high-grade, consistent ore bodies that have supported decades of production by Nutrien and Mosaic — the world's two largest potash producers. Jansen's ore body sits within this same geological province, with resource quality that justifies the capital intensity of the development. The Saskatchewan School of Public Policy has examined how Jansen fits within the province's broader potash policy framework, highlighting its significance to long-term regional resource strategy.

Food Security as the Long-Run Demand Anchor

The structural demand thesis underpinning BHP's original Jansen investment rationale remains largely intact:

- The global population is projected to exceed 9.7 billion by 2050, requiring significant increases in agricultural productivity from a finite and in many regions deteriorating land base

- Soil potassium depletion is a well-documented phenomenon in intensively farmed agricultural regions, increasing fertiliser application requirements over time

- Emerging market agricultural intensification, particularly across South and Southeast Asia, is expected to drive sustained growth in per-hectare fertiliser consumption over coming decades

- Potash has no synthetic substitute in the fertiliser value chain — it must be mined and applied, making demand inelastic relative to production volumes

These structural forces do not resolve the near-term cost overrun challenge at Jansen, but they do provide the long-run demand framework within which the project's multi-decade production life would operate.

Industry Patterns in Greenfield Cost Escalation

The Jansen Stage 2 cost overrun is significant in absolute terms, but it is not exceptional by the standards of large-scale greenfield underground mining development. Industry analysis consistently shows that cost overruns of 40-80% are common in greenfield underground developments, driven by a combination of structural factors:

- Optimism bias in early-stage feasibility studies, where project proponents systematically underestimate complexity and overestimate productivity

- Front-end loading (FEL) methodology gaps, where insufficient engineering definition at the time of capital commitment leaves scope risk inadequately priced into initial estimates

- Black swan ground conditions that emerge only during shaft sinking and development, requiring design modifications that were not captured in surface-based geological studies

- Inflationary compounding over multi-year construction programs, particularly in periods of elevated materials and labour cost inflation

What differentiates Jansen from projects that face existential cost challenges is the underlying quality of the ore body, the scale of the eventual operation, and the financial strength of the project sponsor. BHP's balance sheet capacity to absorb a US$2.3 billion non-cash charge without operational disruption reflects a company with sufficient scale to weather greenfield development volatility.

The next major ASX story will hit our subscribers first

Situating Jansen Within BHP's Broader Portfolio Strategy

The Commodity Portfolio Transition

| Commodity | Project Type | Risk Profile | Revenue Contribution |

|---|---|---|---|

| Iron Ore | Brownfield expansion | Lower | Core — dominant contributor |

| Copper | Greenfield/brownfield mix | Medium-High | Growth commodity |

| Potash (Jansen) | Greenfield underground | High | Future — pre-revenue |

| Coal (divested) | Operational | Divested | Exited |

BHP's strategic pivot toward what it describes as future-facing commodities — principally copper and potash — represents a deliberate shift away from the lower-risk, high-return profile of its iron ore-dominant past. This transition carries an inherent increase in portfolio risk, as greenfield development in new commodity categories introduces execution uncertainty that brownfield expansions of proven operations do not.

The Jansen impairment is, in part, a visible manifestation of that strategic risk materialising. It does not invalidate the underlying commodity thesis, but it does underscore the execution premium that investors should factor into greenfield development timelines and capital estimates for large-scale mining projects. In addition, commodity prices and mining performance remain closely linked, and any sustained weakness in potash pricing would further compress the revised IRR calculations that underpin BHP's Stage 2 decision framework.

BHP's South Flank iron ore project in the Pilbara stands as a reference point for successful large-scale project delivery within the company's portfolio — a brownfield expansion that leveraged existing infrastructure and operational expertise to deliver within more predictable cost parameters. Jansen, as a greenfield underground development in a commodity where BHP has no prior operational history, carries a fundamentally different execution risk profile.

Frequently Asked Questions: BHP Jansen Potash Project Impairment

What is the BHP Jansen potash project impairment?

BHP has recorded a non-cash impairment charge of approximately US$2.3 billion against its Jansen potash project in Saskatchewan, Canada. The write-down reflects a reduction in the project's recoverable value following a significant increase in the Stage 2 capital cost estimate, which has risen from US$4.9 billion to US$6.9 billion, an increase of approximately 41%.

Does the impairment mean BHP is abandoning Jansen?

No. BHP has reaffirmed its commitment to Jansen Stage 1, which remains targeted for first production in mid-2027. The impairment relates primarily to the revised economics of Stage 2, which has been rescheduled to a 2031 timeline. The project retains full-capacity production potential of approximately 8.5 million tonnes per year once both stages are operational.

Why did Jansen Stage 2 costs increase so significantly?

The Stage 2 cost increase from US$4.9 billion to US$6.9 billion reflects a combination of post-2022 construction sector inflation, specialised underground equipment cost increases, labour market tightening in Saskatchewan, and engineering scope revisions following updated geotechnical assessments.

How does a non-cash impairment affect BHP shareholders?

A non-cash impairment reduces reported net profit and earnings per share for the period but does not directly affect BHP's operating cash flow or its capacity to sustain dividend distributions. Sophisticated institutional investors typically assess underlying business performance metrics separately from impairment-adjusted reported earnings.

What is potash and why is it strategically important?

Potash is a critical agricultural input used primarily as a potassium fertiliser to support crop yields and soil health. Its strategic importance is tied to global food security, as it has no synthetic substitute in the fertiliser value chain and must be mined from geologically specific deposits. Demand is expected to grow over the long term in line with population growth and agricultural intensification across developing economies.

Key Takeaways: Reading the Jansen Impairment Strategically

- The US$2.3 billion write-down is a non-cash accounting event driven by a 41% increase in Stage 2 capital costs, not evidence of a fundamental project failure or abandonment decision

- Stage 1 remains on schedule for mid-2027 first production, preserving BHP's near-term pathway to establishing Jansen as a cash-generating asset

- Stage 2's deferral to 2031 is a capital allocation decision that creates a board-level optionality window, not a permanent suspension of the scaling strategy

- The cost escalation reflects sector-wide greenfield development dynamics rather than Jansen-specific engineering failures, consistent with industry-wide patterns of 40-80% overruns in underground mining projects

- BHP's long-term potash thesis, anchored in food security demand and geopolitical supply concentration risk, remains structurally intact despite the near-term cost revision

- Investors should contextualise the impairment against BHP's total balance sheet scale, where a US$2.3 billion non-cash charge represents a manageable adjustment within a company of its financial depth

- The strategic optionality embedded in Jansen's staged design means that Stage 1 cash flows from 2027 can inform and partially fund Stage 2 decisions, reducing the binary risk that a fully committed single-stage development would carry

This article contains forward-looking statements and analysis based on publicly available information. It does not constitute financial advice. Readers should conduct their own independent research and seek qualified financial advice before making any investment decisions. Past performance and project estimates are not reliable indicators of future outcomes.

Readers seeking further coverage of BHP's Jansen project developments and broader Australian mining sector news can explore ongoing reporting at australianminingreview.com.au, which provides regular updates on major ASX-listed resource companies, project economics, and commodity market developments.

Want to Identify the Next Major Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex mineral data into actionable insights for both short-term traders and long-term investors — explore historic discoveries and their exceptional returns to understand the opportunity at stake, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.