May 12, 2026

Copper's Long Game: Why the Metal Beneath the Energy Transition Is Rewriting BHP's Story

There is a particular moment in commodity market history when a structural shift stops being a forecast and starts appearing in financial statements. For most of the past decade, copper's role in the global energy transition was framed as a future story. That moment of transition has now arrived, and it is measurable in ways that matter to investors evaluating BHP shares copper exposure as a long-term thesis rather than a cyclical trade.

Understanding what has changed, why it matters, and what the risks look like from here requires looking at this story from several angles simultaneously: operational, structural, geological, financial, and psychological.

When big ASX news breaks, our subscribers know first

From Iron Ore Giant to Copper-Dominant Earnings Engine

BHP's financial identity was, for decades, synonymous with Australian iron ore. The Pilbara's red dirt delivered extraordinary cash flows that funded dividends, buybacks, and exploration across multiple commodity cycles. That identity is now undergoing a measurable transformation.

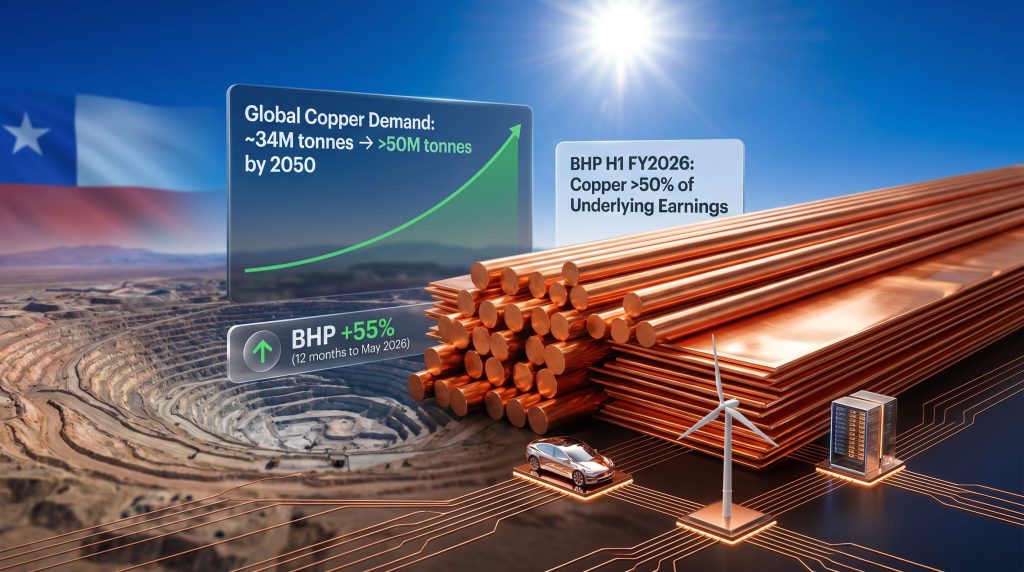

In the first half of FY2026, copper surpassed iron ore to account for more than half of BHP's underlying earnings, marking the first time in the company's modern history that this crossover has occurred. This is not the result of a single copper price spike distorting one reporting period. It reflects a deliberate multi-year capital reallocation strategy, where asset sales of petroleum and thermal coal operations have been systematically redirected toward copper, potash, and nickel.

For investors analysing BHP shares copper exposure as a thesis, this earnings composition shift is the most concrete signal available. It confirms that the portfolio transformation is no longer aspirational. It is already being reflected in reported numbers. Furthermore, understanding the broader copper supply crunch helps contextualise why this repositioning carries such strategic weight.

The Four Forces Reshaping Copper Demand Through 2050

Electrification as the Primary Driver

Copper sits at the physical heart of the global energy transition. Every unit of electricity generated from renewable sources, stored in a battery system, transmitted through an upgraded grid, or consumed by an electric vehicle passes through copper at multiple points along the chain. Unlike many critical minerals whose demand is concentrated in specific technologies, copper is pervasive across the entire electrification ecosystem.

BHP's own demand modelling projects global copper consumption rising from approximately 34 million tonnes annually today to more than 50 million tonnes by 2050, representing an increase of roughly 47% over the period. That projection encompasses four converging demand streams:

- Renewable energy infrastructure: Solar arrays, onshore and offshore wind installations, and grid-scale battery storage all require significantly more copper per megawatt than conventional fossil fuel generation assets.

- Electric vehicle proliferation: An electric vehicle contains roughly three to four times more copper than a conventional internal combustion engine vehicle, with demand concentrated in motors, wiring, charging systems, and battery thermal management.

- Power grid upgrades: The existing electrical grid infrastructure in most developed and developing economies was built for centralised fossil fuel generation, not distributed renewable inputs. Substantial copper-intensive upgrades are required globally to accommodate the energy transition.

- AI data centre buildout: Perhaps the least discussed demand driver in mainstream analysis, BHP projects that copper demand from data centres alone could increase approximately six-fold, reaching close to 3 million tonnes annually by 2050, up from an estimated 500,000 tonnes today.

A Demand Forecast in Context

| Demand Category | Current Estimate | Projected Level (2050) |

|---|---|---|

| Global copper demand (total) | ~34 million tonnes | >50 million tonnes |

| Data centre copper demand | ~500,000 tonnes | ~3 million tonnes |

| BHP annual production target | 1.9-2.0 million tonnes (FY2026) | Expansion underway |

| BHP estimated global market share | ~8.5% | Growing via Escondida expansion |

Source: BHP demand modelling as reported; TradingView analyst consensus data, May 2026. Forecasts represent projections, not guaranteed outcomes.

These figures are drawn from BHP's internal demand forecasting and should be understood as the company's own projections rather than independent third-party research. Investors should consider multiple scenario assumptions when evaluating long-range commodity demand models.

The copper price growth drivers underpinning these projections are consequently attracting significant institutional attention from investors seeking long-duration commodity exposure.

BHP's Copper Production Infrastructure: Scale as a Competitive Moat

Escondida and the Structural Advantage of Tier-One Assets

The single most important fact about BHP's copper production profile is geographic concentration of quality. The Escondida mine in Chile's Atacama Desert is the largest copper mine by production volume on the planet, and it sits within BHP's portfolio as the primary engine of its copper earnings. Ongoing expansion programmes at Escondida are expected to add meaningful incremental production capacity, reinforcing BHP's position as the top copper producer among listed global miners.

BHP's copper production is spread across two primary tier-one jurisdictions:

- Chile: Escondida, alongside associated Chilean operations, represents the bulk of BHP's copper output. Chile hosts the world's largest copper reserves and has been the dominant global copper-producing nation for decades. The Atacama region's high-grade porphyry copper deposits, while facing long-term grade decline challenges, still represent some of the most cost-competitive copper supply globally.

- South Australia: Olympic Dam is a uniquely complex asset that produces copper alongside uranium, gold, and silver as significant byproducts. The uranium component deserves particular attention as a lesser-discussed dimension of Olympic Dam's economics: uranium pricing dynamics and the global nuclear energy renaissance create an additional earnings optionality layer that is rarely factored into headline copper analysis.

Why Ore Grade Matters More Than Reserve Size

A nuance frequently lost in mainstream BHP coverage is the distinction between resource size and resource quality. In copper mining, ore grade — measured as the percentage of copper contained in each tonne of rock mined — is the primary determinant of operating cost, water consumption, energy intensity, and ultimately profit per tonne produced.

As established copper deposits like Escondida mature, the natural geological progression involves accessing lower-grade ore zones deeper within the orebody. Managing this grade decline through blending strategies, processing improvements, and expansion into higher-grade satellite zones is one of the genuine long-term technical challenges facing BHP's copper division. According to BHP's CFO, however, new investors are increasingly buying into copper exposure precisely because of AI-driven demand, which reinforces confidence in long-term capital allocation decisions despite these geological realities.

Frontier Exploration: Serbia and the European Copper Frontier

Beyond its producing assets, BHP has committed up to $35 million toward a copper exploration partnership with Mundoro Capital across a 950 square kilometre exploration package in Serbia, with active drilling programmes extending through 2026. Serbia sits within the Tethyan metallogenic belt, a geological arc stretching across southeastern Europe that hosts several significant copper-gold porphyry deposits.

This exploration commitment is strategically meaningful for two reasons. First, it positions BHP to potentially develop copper supply in Europe at a time when the continent is acutely focused on domestic critical minerals supply chains. Second, it diversifies BHP's exploration pipeline beyond its traditional South American and Australian strongholds.

The "Picks and Shovels" Logic Behind BHP's Expanding Institutional Investor Base

Why Technology Fund Managers Are Looking at a Mining Company

One of the more structurally significant shifts in BHP's investor story is the emergence of a new and broader cohort of international investors entering the BHP register. The composition of this cohort is unusual by historical standards: fund managers whose primary expertise lies in technology and growth equity markets are allocating capital to a diversified mining company.

The investment logic driving this rotation is genuinely elegant from a risk-adjusted perspective. Constructing AI infrastructure exposure through semiconductor manufacturers, cloud platform operators, or hyperscale data centre builders requires taking a binary view on which technology architecture, commercial model, or company will prevail in a rapidly evolving competitive landscape. These are difficult questions with expensive failure modes.

Copper removes that binary risk entirely. Regardless of which AI company dominates the next decade, regardless of whether one chip design or another wins, the physical infrastructure enabling that outcome requires copper in large quantities. BHP, as the world's largest listed copper producer with approximately 8.5% of global supply, is a form of technology infrastructure exposure with the valuation characteristics of a commodity producer rather than a software company trading at elevated growth multiples.

The investor psychology at work here reflects a sophisticated application of the upstream exposure framework: when uncertain about which companies will win a technology race, own the scarce physical inputs that all competitors need. This is conceptually similar to the gold rush analogy of selling shovels rather than mining gold, but applied to twenty-first century infrastructure buildout.

What This Capital Rotation Means for BHP's Long-Term Valuation

The expansion of BHP's potential investor universe has implications beyond near-term share price performance. A broader and more diverse institutional shareholder base can structurally reduce the cyclicality of BHP's valuation multiple, because technology-oriented investors tend to apply longer-duration discounting frameworks than traditional resources fund managers. In addition, exploring copper investment strategies that leverage this dynamic can help investors position effectively for what may be a multi-year rerating of BHP's earnings quality.

If BHP begins to be valued, even partially, as a structural beneficiary of technology infrastructure growth rather than purely as a copper price proxy, the multiple expansion potential is material. This remains a speculative observation rather than a confirmed valuation shift, but it represents an underappreciated dimension of what the changing investor base could mean over a multi-year horizon.

Multi-Division Performance and Balance Sheet Architecture

Diversification as an Earnings Stabiliser

The copper transformation story exists alongside, rather than instead of, strong performance across BHP's other major business segments. This multi-stream earnings architecture is central to the investment case for BHP shares copper exposure, providing a resilience buffer that pure-play copper companies cannot offer.

BHP's key operating divisions and their current status:

| Division | Current Performance | Strategic Role |

|---|---|---|

| Western Australian Iron Ore (WAIO) | Recently achieved record production levels | Primary cash flow generator; funds copper growth capex |

| Copper | Tracking toward upper half of FY2026 guidance (1.9-2.0M tonnes) | Primary earnings contributor in H1 FY2026 |

| Steelmaking Coal | Retained exposure | Commodity cycle diversification; optionality on steel demand |

| Potash (Jansen, Canada) | Long-dated development stage | Multi-decade agricultural demand optionality |

The interplay between these divisions is strategically important. Iron ore cash flows fund copper expansion capital expenditure during periods when copper prices are under pressure. During periods of iron ore softness, copper earnings provide compensatory contribution. This internal hedging mechanism creates earnings stability that is genuinely difficult to replicate through external diversification alone.

Balance Sheet Positioning

BHP's financial flexibility has been materially enhanced through a disciplined portfolio reshaping programme over the preceding several years. The divestiture of petroleum operations and certain coal assets generated substantial proceeds that have been redeployed toward copper, nickel, and potash. Furthermore, understanding the broader commodity price impact on diversified miners like BHP illustrates why this reallocation strategy has been so consequential for long-term earnings resilience.

This balance sheet management allows BHP to simultaneously pursue organic growth at Escondida and Olympic Dam, maintain dividend distributions to shareholders, fund frontier exploration commitments in Serbia, and retain capacity for opportunistic mergers and acquisitions during periods of commodity market weakness.

The next major ASX story will hit our subscribers first

BHP Share Price Performance and Analyst Positioning

Twelve-Month Returns in Context

BHP shares have delivered a 55% total return over the twelve months to May 2026, measured against an S&P/ASX 200 Index gain of approximately 6% over the same period. Year-to-date performance stands at 28%, with a 6% gain recorded in the five trading sessions immediately preceding the May 12, 2026 publication of the source analysis. Notably, BHP shares up 55% in a year has prompted many analysts to reassess whether current valuations still represent compelling entry points.

At a prevailing share price of $58.33, BHP is trading materially above the consensus analyst price target, a configuration that historically signals the market has run ahead of fundamental valuation models.

What the Analyst Consensus Is Actually Telling Investors

| Rating Category | Analyst Count | Percentage of Coverage |

|---|---|---|

| Buy or Strong Buy | 5 of 21 | 24% |

| Hold | 14 of 21 | 67% |

| Sell | 2 of 21 | 9% |

| Average 12-month price target | $54.30 | ~7% below $58.33 |

| Most bullish scenario | Implies ~18% upside | Minority view |

| Most bearish scenario | Implies ~33% downside | Minority view |

Source: TradingView analyst consensus data, May 2026. Analyst forecasts are opinions, not guarantees of future performance.

The 67% hold weighting among covering analysts is the most informative signal in this table. It does not represent bearishness on BHP's long-term copper thesis. Rather, it reflects a valuation discipline: the average target of $54.30 sitting approximately 7% below the current trading price indicates that consensus models have already incorporated the copper growth narrative at a lower entry point and are now flagging that near-term return expectations should be tempered.

The 51-percentage-point spread between the most bullish and most bearish individual price targets reveals significant divergence in fundamental assumptions, likely reflecting different views on copper price trajectory, Chinese economic activity, and the pace of electrification infrastructure buildout.

This article contains general information only and does not constitute financial advice. Past performance is not indicative of future results. Investors should consider their own circumstances and seek independent financial advice before making investment decisions. All analyst price targets and forecasts represent opinions, not guarantees, and may change without notice.

Key Risks Every BHP Investor Must Understand

Labour Relations at Escondida

The Escondida mine has a documented history of union-related work stoppages and industrial action. Given Escondida's outsized contribution to BHP's total copper output, any significant labour disruption carries direct earnings consequences. This remains the most operationally proximate near-term risk to BHP's copper production guidance.

Copper Price Cyclicality

Structural demand arguments do not eliminate price volatility. Copper prices remain highly sensitive to Chinese manufacturing and construction activity, US dollar movements, and global inventory cycle dynamics. A sustained period of weaker copper prices would compress margins even as production volumes grow, and this cyclical sensitivity should not be obscured by the long-term structural narrative.

Ore Grade Decline as a Geological Reality

A less-discussed but genuinely material long-term consideration is the natural grade decline trajectory of established porphyry copper deposits like Escondida. As higher-grade ore near the surface is progressively mined, accessing deeper, lower-grade material increases unit operating costs. Managing this geological reality through processing technology investment and operational efficiency gains is an ongoing challenge that directly affects BHP's long-term copper cost position.

Regulatory and Tax Environment in Chile

Chile's mining royalty framework and broader regulatory environment for large-scale copper extraction have been the subject of ongoing policy debate. Any material increase in mining taxes or operational restrictions would affect the economics of the Escondida expansion programmes and potentially alter the attractiveness of further Chilean capital investment.

Execution Risk Across Multiple Growth Fronts

BHP is simultaneously managing expansion at Escondida, development at Jansen in Canada, exploration in Serbia, and ongoing investment at Olympic Dam. Allocating capital effectively across multiple long-lead-time projects in different jurisdictions and commodity segments introduces genuine portfolio complexity risk.

A Framework for Evaluating BHP Shares Copper Exposure Today

For investors approaching BHP with a long-term horizon, the evaluation framework should consequently address five dimensions:

- Copper price sustainability: Is the current price environment reflecting genuine structural demand, or does it incorporate speculative premium that may reverse cyclically?

- Production growth execution: Is the Escondida expansion tracking to timeline and budget, and is the grade profile of expansion ore consistent with guidance assumptions?

- Valuation versus consensus: With the average analyst price target sitting approximately 7% below the May 2026 trading price, does the current entry point reflect the copper thesis at a reasonable margin of safety?

- Dividend sustainability: Can BHP maintain distributions to shareholders while simultaneously funding multi-billion-dollar copper growth capital expenditure commitments?

- Portfolio quality trajectory: Are the ongoing asset sales and capital reallocation decisions genuinely improving the quality and duration of BHP's earnings mix, or simply concentrating commodity risk?

BHP's transition from an iron ore-dominated earnings profile to a copper-led business represents one of the most significant portfolio transformations in the company's history. The structural demand forces underpinning this repositioning are multi-decade in nature, well-supported by independent energy transition analysis, and converging across multiple technology and infrastructure megatrends simultaneously.

The central analytical tension for investors today is not whether the copper demand thesis is credible. It is whether $58.33 per share, following a 55% twelve-month rally, represents an entry point that still offers adequate compensation for the operational, cyclical, and execution risks that accompany even the most compelling long-term commodity investment case.

Want to Catch the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant copper and critical mineral discoveries and delivering actionable alerts to subscribers ahead of the broader market — explore the historic returns major discoveries have generated and begin your 14-day free trial to position yourself at the forefront of the next major find.