May 12, 2026

When Passive Assets Meet Productive Giants: Rethinking the Gold vs. Equities Debate

There is a deeply rooted assumption in investing circles that gold is the ultimate long-term protector of wealth. During periods of geopolitical turbulence, currency instability, or equity market stress, capital flows reliably into the yellow metal. It has served this function for centuries, and that history carries enormous psychological weight for investors navigating uncertainty.

But history also reveals something less comfortable for gold advocates: over genuinely long investment horizons, assets that generate earnings, reinvest capital, and distribute income to shareholders have consistently outperformed passive stores of value. The compounding mathematics are not subtle. A zero-yield asset that appreciates 40% in a single year can still underperform a dividend-paying, earnings-growing business measured across a decade, because only one of those assets is building value while you wait.

This distinction sits at the heart of why the question of whether BHP shares better than gold long term deserves serious analytical attention rather than a reflexive answer.

When big ASX news breaks, our subscribers know first

Is Gold Still the Ultimate Long-Term Wealth Protector, or Has Its Role Been Overstated?

What Gold Actually Delivers Over Time

Gold's primary function is well understood: it acts as a crisis hedge, a store of purchasing power during inflationary periods, and a low-correlation diversifier within equity-heavy portfolios. Understanding the gold-stock market relationship helps clarify why, during periods of acute stress — whether driven by geopolitical escalation, central bank policy failures, or systemic financial risk — gold's price tends to rise as institutional and retail capital seeks shelter.

Gold's spot price climbed from approximately US$2,618 to US$3,719 across 2025, representing a gain of roughly 40% in USD terms. That is not a trivial return by any measure, and it reflects a genuine risk premium being priced into the market during a period of elevated geopolitical tension and accelerated central bank accumulation of the metal.

However, the critical limitation of gold as a long-term wealth-building vehicle is structural, not cyclical. Gold generates no earnings. It pays no dividends. It produces no operational cash flow. Its price is entirely a function of sentiment, macro conditions, and demand/supply dynamics, with no fundamental earnings floor to provide support during extended downturns.

Gold excels at preserving purchasing power during acute market stress, but for investors with a 10-year horizon, productive assets with earnings growth and dividend capacity have historically delivered superior total returns.

Gold's multi-decade price history also reveals significant volatility that is often understated in popular narratives. The metal spent much of the 1980s and 1990s in a prolonged bear market, losing real purchasing power for investors who allocated heavily at the peak of the previous cycle. Those who held through that period received no dividend income, no earnings growth, and no compounding benefit to offset the drawdown.

Furthermore, while gold as a strategic investment has genuine merit in specific macro environments, its structural limitations become most apparent when measured against earnings-generating assets across full market cycles.

What Productive Assets Offer That Gold Simply Cannot

The compounding advantage of dividend-paying, earnings-generating businesses is not merely theoretical. When a company reinvests earnings into higher-return projects, grows its earnings per share, and distributes capital back to shareholders, it creates a self-reinforcing return engine. A 4% annual earnings growth rate layered on top of a dividend yield produces a total return profile that passive asset ownership structurally cannot replicate.

The distinction between crisis performance and long-term wealth creation is fundamental. Gold wins the crisis performance category with some authority. However, investors building wealth across 10 or more years are not primarily managing crisis risk — they are compounding capital. Those are different objectives requiring different tools.

Why BHP Group (ASX: BHP) Stands Out as a Long-Term Wealth-Building Vehicle

Beyond Iron Ore: Understanding BHP's Evolving Commodity Portfolio

BHP's identity in investor consciousness remains anchored to iron ore, and for understandable reasons. Iron ore has been the company's primary earnings driver for years, generating substantial cash flow that has funded dividends, balance sheet strength, and major capital projects. As of early 2026, iron ore remained a significant contributor to group earnings, with benchmark prices trading around US$111 per tonne.

Consequently, anchoring the entire investment thesis to iron ore misses the more compelling long-term narrative. BHP's management has been deliberate and explicit in signalling a strategic pivot toward what the company describes as "future-facing commodities," specifically copper and potash. This shift is not cosmetic. It reflects a fundamental repositioning of the portfolio toward assets with structural demand tailwinds that extend well beyond the traditional steel-production cycle. For a deeper look at how iron ore demand prospects are evolving, the China demand trajectory remains central to near-term earnings modelling.

Commodity diversification across iron ore, copper, and potash reduces BHP's single-cycle dependency and broadens the earnings base in ways that make the company more resilient across the full length of a commodity supercycle.

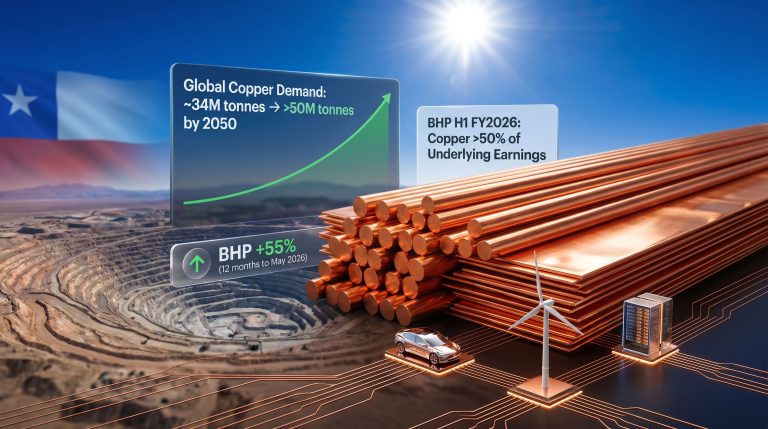

The Copper Supercycle Thesis: BHP's Most Compelling Long-Term Growth Driver

Copper's role in the global economy is expanding in ways that few metals can match. Its electrical conductivity makes it effectively irreplaceable across electricity grid infrastructure, renewable energy systems, electric vehicles, data centres, and industrial machinery. The global electrification transition is not a short-term theme — it is a structural shift measured in decades, and copper sits at the physical centre of it.

BHP's copper segment delivered a 28% increase in first-half profit, demonstrating that operational leverage to rising copper prices is already translating into meaningful earnings growth. This is precisely the kind of earnings acceleration that gold ownership cannot provide, regardless of how well the gold price performs.

The copper supply crunch reinforces the long-term pricing thesis considerably. New copper mines take between 10 and 15 years from discovery to production. Permitting environments across major copper-producing jurisdictions have become increasingly complex and time-consuming. Existing orebodies are progressively declining in grade as the highest-quality deposits are mined first, meaning more ore must be processed to produce the same volume of refined copper. These structural supply constraints create a persistent tension against demand that is forecasted to intensify through the 2030s.

The global electrification transition is not a short-term theme. Copper demand tied to EV infrastructure, grid upgrades, and data centre expansion is forecast to intensify through the 2030s, a timeframe that aligns directly with BHP's long-cycle asset development strategy.

BHP's existing copper asset base, combined with management's stated commitment to expanding future-facing commodity exposure, positions the company to benefit from this dynamic over precisely the long-term horizon where productive assets outperform passive stores of value.

Jansen Potash: The Often-Overlooked Third Pillar of BHP's Long-Term Case

The Jansen potash project in Saskatchewan, Canada, receives considerably less attention from investors than copper or iron ore, but it represents a genuinely differentiated long-duration option within BHP's portfolio. Potash is a critical agricultural fertiliser input, and its demand is structurally linked to global population growth and the intensifying pressure on agricultural productivity.

As global population continues to expand toward a projected 10 billion people by 2050 (United Nations, World Population Prospects), the need to produce more food from a finite base of arable land becomes increasingly acute. Potash is one of the primary inputs that enables higher crop yields on existing farmland, making it a commodity with secular demand support that operates largely independently of the copper or iron ore cycles.

Jansen diversifies BHP's earnings beyond traditional metals cycles and gives the company a third long-term growth pathway that most resource sector peers simply do not possess.

How Does BHP's Financial Profile Compare to Holding Physical Gold?

Side-by-Side Comparison: BHP Shares vs. Physical Gold

| Investment Attribute | BHP Shares (ASX: BHP) | Physical Gold |

|---|---|---|

| Earnings Growth | Forecast ~4.62% annual EPS growth; copper segment delivered 28% H1 profit increase | No earnings, price appreciation only |

| Dividend Income | Variable dividend linked to commodity earnings; rebound potential as copper scales | Zero yield, no income generation |

| Valuation Entry Point | ~12-14x forward FY27 earnings; analyst fair value ~A$52.50 | No earnings multiple, priced on sentiment and macro fear |

| Growth Catalysts | Copper electrification demand, Jansen potash ramp, iron ore cash generation | Geopolitical tension, inflation expectations, USD weakness |

| Downside Risk | Commodity cycle exposure; iron ore price sensitivity | Lower operational risk; no upside leverage in bull markets |

| 12-Month Performance (to April 2026) | ~50% gain; ~20% recovery from April lows | ~40% gain in USD terms |

| Analyst Consensus | Buy-to-hold for a decade; copper and potash thesis cited by multiple analysts | Effective short-term hedge; limited long-term total return advantage |

| Crisis Hedging | Moderate; balance sheet strength provides resilience | High; primary safe-haven function |

What the Valuation Gap Reveals About Long-Term Opportunity

Trading at approximately 12 to 14 times forward FY27 earnings, with analyst consensus placing fair value at approximately A$52.50 per share, BHP offers a fundamentally different value proposition than a zero-yield commodity asset priced purely on fear and macro sentiment.

The earnings multiple framework matters because it reveals something gold pricing cannot: an implied growth rate. With earnings per share forecasts of approximately A$4.43 for FY27 and annual EPS growth projections of roughly 4.62%, BHP's valuation reflects a business whose intrinsic value is expected to expand over time. Every dollar of earnings growth compounds the share's fundamental value in a way that no amount of gold price appreciation can structurally replicate.

BHP's balance sheet strength is an additional structural advantage. The company's ability to sustain capital investment through commodity downturns, fund major projects like Jansen, and maintain dividend payments during challenging periods reflects a financial resilience that smaller resource companies — and gold bars — simply cannot offer. Understanding how commodity prices and mining performance interact over cycles is essential context for evaluating this resilience properly.

What Do the Numbers Actually Say? Performance Data Decoded

Short-Term Price Action: 2025 and Early 2026 Context

Gold's 40% USD price surge across 2025 attracted significant short-term capital, driven by a combination of geopolitical risk premium, central bank accumulation (particularly from emerging market central banks diversifying away from USD reserves), and genuine inflation anxiety among retail investors.

Notably, gold mining ETFs significantly outperformed physical gold during this period. The iShares Gold Producers ETF and comparable instruments gained between 96% and 110%, illustrating a principle that sophisticated commodity investors understand well: when commodity prices rise, companies with operational leverage to that commodity can generate returns far exceeding the commodity price gain itself, because their margins expand dramatically. This is operational gearing at work.

BHP shares gained approximately 50% over the 12 months to April 2026, with approximately a 20% recovery from April lows reflecting broader market stabilisation. Critically, BHP's gains were not purely sentiment-driven. They reflected actual operational performance, particularly the copper segment's strong profit growth, and genuine commodity demand fundamentals rather than a fear-driven macro premium. According to analysis from The Motley Fool Australia, BHP's sustained run raises legitimate questions about whether the valuation remains attractive at current levels — a consideration long-term investors should weigh carefully.

Long-Term Return Framework: Why the 10-Year Lens Changes the Comparison

The compounding arithmetic of dividend reinvestment fundamentally changes the total return comparison over multi-year periods. An investor who reinvests BHP dividends during periods of strong commodity earnings is effectively purchasing additional shares at prevailing market prices, compounding both income and capital growth simultaneously.

Layered on top of this dividend compounding is BHP's earnings growth trajectory. At approximately 4.62% annual EPS growth, the intrinsic value of the business expands meaningfully over a decade. A physical gold allocation over the same period generates no dividends, no earnings growth, and no compounding — making the 10-year return comparison structurally asymmetric in favour of productive assets under most commodity cycle scenarios.

BHP's commodity cycle exposure requires a genuine long-term orientation. Investors seeking short-term capital preservation may find gold more suitable, but those building wealth over a decade or more face a structurally different return calculus.

Historical patterns from prior commodity cycles reinforce this point. Investors who maintained BHP exposure through the iron ore price downturn of the mid-2010s and held patiently into the subsequent recovery period were rewarded with returns that substantially exceeded what equivalent capital sitting in gold would have produced over the same window.

What Are the Real Risks of Choosing BHP Over Gold?

Commodity Cycle Volatility: The Honest Assessment

Iron ore price sensitivity remains BHP's most significant near-term earnings risk. China's steel production trajectory, property sector health, and infrastructure investment levels all influence iron ore demand and pricing in ways that BHP cannot control. A sustained decline in iron ore prices can compress group earnings and dividend capacity materially.

The key risks for long-term BHP investors include:

- Iron ore price sensitivity driven by Chinese steel demand cycles

- Copper demand timing uncertainty, as the electrification transition plays out over years rather than quarters

- Jansen's extended capital deployment timeline, with potash production ramping gradually over multiple years

- Permitting and regulatory complexity across multiple operating jurisdictions

- Currency fluctuations affecting AUD-denominated returns from USD-priced commodities

Why BHP's Risk Profile Remains Manageable for Long-Term Investors

BHP's scale and balance sheet strength mean that it can absorb commodity cycle downturns in ways that smaller resource companies cannot. The company has the financial capacity to continue investing in Jansen, sustaining copper development, and maintaining operational efficiency even during periods when iron ore prices weaken.

Diversification across three major commodity streams — iron ore, copper, and potash — means that weakness in any single market is partially offset by performance elsewhere. A Morningstar comparison of BHP and Rio Tinto highlights how this multi-commodity structure distinguishes BHP's investment proposition from single-commodity peers. This structural advantage is something no single-metal holding, including gold, can replicate.

Gold's Hidden Risks That Investors Often Underestimate

Physical gold carries its own risk profile that is frequently understated in popular investment commentary:

- No earnings floor: gold's price is entirely sentiment and macro-driven, with no fundamental support during sustained bear phases

- Significant opportunity cost: holding a zero-yield asset over a decade means forgoing compounding dividend income that could have been reinvested at prevailing market prices

- Storage and insurance costs for physical gold reduce net returns in ways that are not always factored into superficial performance comparisons

- Gold mining ETF performance (96-110% gains during the 2025 gold bull market) demonstrates that operational leverage, not the metal itself, drives the strongest commodity-linked returns

The next major ASX story will hit our subscribers first

BHP vs. Gold: Which Is Right for Your Investment Strategy?

Investor Profile Matching: A Framework for Decision-Making

BHP Shares May Suit Investors Who:

- Prioritise total returns combining income and capital growth over a 7 to 10-year or longer horizon

- Want exposure to structural demand themes including electrification, EV infrastructure, and global food security

- Are comfortable with commodity cycle volatility in exchange for earnings growth and dividend income

- Seek a diversified resource platform rather than a single-commodity position

Physical Gold May Suit Investors Who:

- Prioritise capital preservation during periods of acute geopolitical or financial market stress

- Want a low-correlation asset to balance an equity-heavy portfolio

- Have a shorter investment horizon or lower tolerance for earnings-linked volatility

- Are specifically hedging against currency devaluation or systemic financial risk

Can Both Coexist in a Long-Term Portfolio?

The most sophisticated approach to this debate is not binary. Gold and BHP shares better than gold long term as the sole portfolio answer is perhaps the wrong framing entirely. Gold and BHP can serve complementary functions within a well-constructed long-term portfolio: gold as a crisis buffer that preserves capital during acute stress events, and BHP as the long-term growth engine that compounds wealth through earnings growth, dividends, and structural commodity demand exposure.

The risk for long-term wealth builders is over-allocating to gold at the expense of productive, earnings-generating assets. A portfolio that is heavily weighted toward zero-yield assets may preserve capital effectively during downturns, but it structurally impairs the compounding return that converts savings into genuine long-term wealth.

Position sizing between productive assets and safe-haven holdings should be calibrated to the investor's specific time horizon, income needs, and risk tolerance — ideally in consultation with a licensed financial adviser.

Frequently Asked Questions: BHP Shares vs. Gold as a Long-Term Investment

Is BHP a better long-term investment than gold?

For growth-oriented investors with a 7 to 10-year or longer horizon, BHP's combination of earnings growth, dividend income, and exposure to structural commodity demand themes provides a total return profile that physical gold cannot replicate. Gold remains a superior short-term hedge during acute market stress but offers no operational leverage, no dividends, and no earnings growth capability.

What makes BHP shares a compelling long-term investment?

BHP's long-term investment case rests on three pillars: copper demand driven by global electrification and EV infrastructure growth; potash exposure through the Jansen project linked to long-term agricultural productivity demand; and iron ore cash generation funding capital returns and balance sheet resilience through commodity cycles.

How has BHP performed compared to gold recently?

Over the 12 months to April 2026, BHP shares gained approximately 50%, while gold surged approximately 40% in USD terms over 2025. Gold mining ETFs carrying operational leverage to gold prices gained between 96% and 110%, illustrating that earnings-linked commodity exposure consistently outperforms passive metal ownership during commodity bull market conditions.

What is BHP's forward earnings valuation?

BHP was trading at approximately 12 to 14 times forward FY27 earnings, with analyst estimates placing fair value at approximately A$52.50 per share. EPS forecasts of approximately A$4.43 for FY27, combined with annual EPS growth projections of roughly 4.62%, underpin the long-term buy-and-hold thesis cited by multiple market analysts.

Does BHP pay dividends?

Yes. BHP's dividend is variable and linked to commodity prices and earnings performance. While not a fixed income stream, BHP has demonstrated a consistent commitment to returning capital to shareholders during periods of strong cash generation. For long-term investors, the combination of dividend income and capital growth creates a compounding total return advantage over non-yielding assets such as gold.

What are the biggest risks of investing in BHP over gold?

The primary risks include iron ore price sensitivity, copper demand timing uncertainty, and the extended capital deployment timeline of the Jansen potash project. Commodity cycle downturns can compress earnings and dividends significantly. However, BHP's balance sheet strength and diversified commodity exposure provide structural resilience that smaller resource companies cannot match.

The Long-Term Verdict: Productive Assets vs. Passive Stores of Value

Why the Structural Argument Favours BHP Over a Multi-Decade Horizon

The fundamental argument for why BHP shares better than gold long term comes down to the mathematics of compounding. Earnings growth, dividend reinvestment, and structural commodity demand create a return engine that zero-yield assets are structurally incapable of matching over periods measured in decades rather than quarters.

BHP's positioning across copper, iron ore, and potash gives it multiple pathways to shareholder value creation. It is not a single macro bet on sentiment or fear — it is a diversified industrial operation with cash flow, capital return capability, and exposure to some of the most compelling structural demand themes of the coming decades.

The electrification transition, agricultural productivity pressure, and expanding global infrastructure investment are decade-long structural demand drivers. BHP is among the best-positioned ASX companies to translate those macro themes into tangible, measurable shareholder returns.

Final Framework: Matching Asset Selection to Investment Objectives

| Investment Objective | Preferred Asset |

|---|---|

| Long-term wealth compounding (10+ years) | BHP Shares |

| Crisis hedging and capital preservation | Physical Gold |

| Income generation and dividend growth | BHP Shares |

| Inflation protection (short-term) | Physical Gold |

| Exposure to electrification and EV demand | BHP Shares |

| Portfolio diversification (low correlation) | Physical Gold |

| Total return maximisation over a commodity supercycle | BHP Shares |

Editorial Disclaimer: This article provides general financial analysis and educational commentary only. It does not constitute personalised financial advice. Investors should consider their individual financial circumstances, objectives, and risk tolerance carefully. Consultation with a licensed financial adviser is strongly recommended before making any investment decisions. Past performance is not indicative of future returns. All financial figures and performance data referenced are based on publicly available information at the time of writing and may have changed.

Want to Uncover the Next Major ASX Mineral Discovery Before the Broader Market Does?

While BHP offers compelling long-term compounding through copper, potash, and iron ore, the most dramatic early-stage returns in the resources sector often emerge from significant new mineral discoveries — and Discovery Alert's proprietary Discovery IQ model delivers real-time ASX discovery alerts the moment they are announced, turning complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page to see what is possible, then begin a 14-day free trial to position yourself ahead of the market.