July 21, 2026

The Capital Discipline Reckoning: Why the World's Biggest Energy Companies Are Returning to Their Roots

Across the global energy industry, a quiet but consequential correction has been underway. The post-pandemic era briefly convinced investors, policymakers, and corporate boardrooms that the energy majors could simultaneously fund large-scale renewable transitions while sustaining the upstream productivity that built their balance sheets over decades. That experiment, for several of the world's largest oil and gas producers, has not delivered the returns that justified the capital deployed. The result is a generational recalibration of investment priorities, and no company illustrates this more starkly than BP.

The BP pivot back to oil and gas is not simply a story about one company changing direction. It is a window into the structural tension at the heart of the global energy transition: the gap between long-term decarbonisation ambitions and the near-term financial realities that govern trillion-dollar enterprises.

When big ASX news breaks, our subscribers know first

From Green Ambition to Hydrocarbon Realism: How BP Lost Its Way and Found It Again

When Bernard Looney took over as chief executive in early 2020, BP launched what was widely considered the most aggressive renewable energy strategy of any major oil and gas company in the world. The plan involved cutting hydrocarbon production by approximately 40% from 2019 levels by 2030 and deploying billions annually into wind, solar, hydrogen, and carbon capture technologies. At the time, it was heralded as a blueprint for how legacy fossil fuel companies could reinvent themselves for a net-zero world.

What followed was a painful lesson in the difference between strategic aspiration and financial execution. BP's renewable investments consistently generated returns that lagged behind its upstream hydrocarbon operations. As capital flowed toward lower-yielding clean energy assets, the company's financial performance deteriorated relative to peers who had maintained tighter discipline over capital allocation. BP's share price from the start of 2022 to early 2025 was essentially flat, while Shell's shares rose approximately 72% over the same period, according to reporting by City A.M.

The underperformance created an opening for activist investors. Elliott Management, one of the world's most aggressive hedge funds, acquired approximately a 5% stake in BP valued at around $3.8 billion, and used that position to intensify pressure on the board to simplify the business and refocus on fossil fuel value creation. The arrival of Elliott shifted the governance dynamic decisively, accelerating a strategic reset that was already quietly underway under Looney's successor, Murray Auchincloss.

Leadership Transitions and the Architecture of Change

BP's recent history is defined by rapid chief executive turnover. Four leaders have passed through its Surrey headquarters in fewer than three years, each one moving the strategic needle further in the same direction: away from renewables-led ambition and toward hydrocarbon-centred discipline.

The trajectory can be summarised as follows:

-

Bernard Looney established the green energy ambitions and aggressive renewable targets that defined BP's early 2020s identity.

-

Looney's departure triggered a period of internal review that exposed the financial underperformance of those commitments.

-

Murray Auchincloss initiated the first substantive pivot, cancelling $10 billion in planned renewable energy investments and redirecting that capital into BP's petrochemicals division.

-

Meg O'Neill, appointed as the first female chief executive of a major British energy company and a former executive at Woodside Energy, accelerated the transformation upon taking the helm in 2026.

O'Neill's first communication to BP's approximately 100,000 employees made clear that the company was operating under conditions of significant geopolitical market complexity, and that her leadership would prioritise clarity and consistency. Her actions backed those words almost immediately.

The New Corporate Architecture: Simplicity as Strategy

One of O'Neill's first structural decisions was to dismantle BP's historically complex organisational design and replace it with a straightforward two-division framework. The logic was as much financial as operational: a simpler structure reduces overhead, accelerates decision-making, and allows capital to flow more efficiently toward the highest-returning assets.

| Division | Primary Function | Strategic Priority |

|---|---|---|

| Upstream | Exploration and production of oil and gas | Volume growth, capital efficiency |

| Downstream | Refining, trading and distribution | Margin optimisation, cash generation |

This back-to-basics architecture echoes the corporate structures that defined BP's most profitable decades in the late twentieth century. The implicit message is that the diversified, multi-business model that accumulated renewable assets, hydrogen projects, and carbon capture ventures alongside traditional upstream operations created complexity without commensurate returns.

Production Targets: The Numbers That Define the New BP

The revised production ambitions are the clearest quantitative expression of BP's new direction:

-

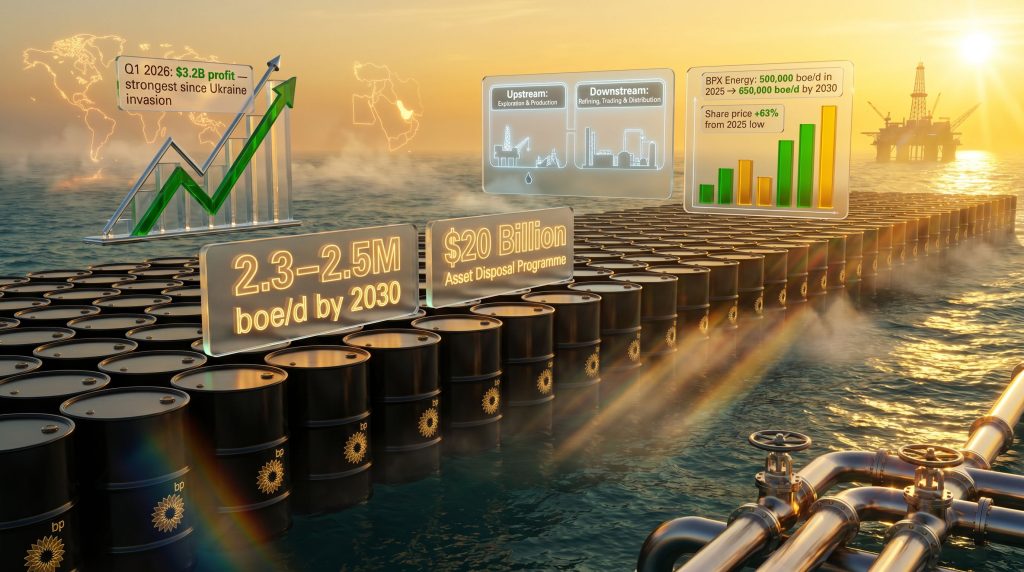

A target of 2.3 to 2.5 million barrels of oil equivalent per day (boe/d) by 2030, replacing the prior plan that had envisioned deep production cuts.

-

BPX Energy, the company's U.S. shale operation, is targeting 500,000 boe/d in 2025, scaling to 650,000 boe/d by 2030.

-

Projected shale output growth of approximately 8% annually, underpinned by the capital efficiency advantages of unconventional plays where repeat drilling programmes and established infrastructure allow production growth at lower incremental cost.

The shale angle is particularly notable from an investment perspective. U.S. unconventional production offers a faster capital cycle than conventional offshore or deepwater projects, meaning BP can deploy capital and realise returns on shorter timeframes, improving cash conversion and balance sheet metrics more rapidly than multi-year greenfield developments would allow.

Q1 2026 Earnings: The Financial Inflection Point

The results that BP reported for the first quarter of 2026 validated the strategic repositioning in the most direct way possible: through financial performance that far exceeded expectations.

Key metrics from the quarter include:

-

Trading division profit before tax reached $3.2 billion, the strongest quarterly result since Russia's invasion of Ukraine.

-

Overall quarterly profit more than doubled, significantly beating internal guidance and external analyst forecasts.

-

Production held broadly flat despite the closure of the Strait of Hormuz, a critical maritime corridor that historically accounts for approximately one-fifth of all seaborne oil and gas traffic globally.

-

BP's share price rose nearly 3% on the day of the earnings announcement, according to City A.M.

Quilter Cheviot global energy analyst Maurizio Carulli described the Q1 results as both positive and ahead of expectations, while XTB analyst Kathleen Brooks characterised them as stunning, according to reporting by City A.M.

The Strait of Hormuz dimension deserves particular attention. The waterway connecting the Persian Gulf to the Arabian Sea is one of the most strategically sensitive chokepoints in global energy logistics. When it is disrupted, energy trading desks that can navigate price volatility and reroute supply flows gain significant commercial advantage. BP's trading operation, which performs best in exactly this kind of volatile environment, delivered accordingly.

Balance Sheet Repair: The Metric That Matters Most

Beyond the headline profit number, institutional investors and analysts focused most closely on BP's balance sheet progress during the Q1 2026 reporting period. The company had been spending more than $1.3 billion annually on debt interest alone, making deleveraging a top-tier operational priority.

Key balance sheet actions during the period included:

-

Retirement of $4.3 billion in corporate bonds without reissuance, funded by redirecting cash previously earmarked for share buybacks.

-

The quarterly share buyback programme was trimmed to a range of $750 million to $1 billion, down from prior commitments, reflecting the deliberate prioritisation of debt reduction.

-

The term "balance sheet" was referenced more than a dozen times during BP's Q1 2026 analyst call, underscoring the institutional focus on financial repair over shareholder distributions.

The retirement of hybrid debt instruments without refinancing is a particularly important signal. Hybrid bonds sit in a grey area between equity and debt on corporate balance sheets, and their elimination reduces not only interest costs but also the structural complexity that rating agencies and institutional investors scrutinise closely.

The Asset Disposal Programme: $20 Billion by 2026

Alongside production growth and balance sheet repair, BP has committed to generating $20 billion through asset sales by 2026 as the third pillar of its financial recovery. Progress to date includes:

-

Sale of the Castrol lubricants business to a U.S. private equity firm for $10.1 billion.

-

Divestment of a German refinery to Klesch Group for an undisclosed consideration.

-

Cancellation of $10 billion in planned renewable energy investments, with capital redirected into petrochemicals.

-

Reduction of hydrogen and carbon capture project commitments from approximately 30 initiatives to between 5 and 7 by 2030.

The Castrol transaction is strategically significant beyond its headline price. Lubricants represented one of BP's highest-margin downstream businesses, with strong brand equity and relatively stable cash flows. Selling it at a premium to private equity signals a willingness to sacrifice quality assets in pursuit of balance sheet objectives, which reflects the depth of the financial pressure BP has been navigating.

The next major ASX story will hit our subscribers first

Elliott Management and the Activist Investor Effect

Elliott Management's intervention warrants examination as a case study in how activist capital can reshape strategy at a corporation generating approximately $192.5 billion in annual revenue. The hedge fund's acquisition of a 5% stake gave it both the economic weight and the boardroom leverage to demand accelerated action on portfolio simplification and hydrocarbon refocus.

Sources familiar with Elliott's position indicated to City A.M. that chair Albert Manifold's early tenure had been viewed as encouraging, and that he had already functioned as a constructive force for change. However, the same sources characterised the transformation as still in early stages, suggesting ongoing scrutiny rather than uncritical satisfaction.

BP's stock recovery of approximately 63% from its 2025 low reflects market endorsement of the direction Elliott pushed for. That said, the relationship between activist investors and corporate management rarely settles into permanent alignment. As BP's financial metrics improve, the internal governance dynamics will likely evolve.

The Shareholder Divide: Governance Friction Beneath the Surface

Strong financial results did not prevent a degree of shareholder unrest at BP's 2026 Annual General Meeting. The board lost two separate votes, covering climate reporting disclosure and a proposal to shift the gathering to a virtual format. More significantly, nearly one-fifth of shareholders voted against the reelection of chair Albert Manifold, an unusually high dissent figure by the standards of major listed companies, where board chairs typically receive close to unanimous support.

Quilter Cheviot's Maurizio Carulli, as reported by City A.M., characterised the AGM rebellion as representing dissatisfaction beyond the specific governance questions on the agenda, rather than a fundamental objection to BP's strategic direction. The distinction matters for investors trying to interpret what the voting data actually signals.

The shareholder divide at BP reflects a broader tension within institutional investment:

-

ESG-mandated funds face structural pressure to reduce exposure to companies that are actively expanding fossil fuel production.

-

Return-focused investors are rewarding BP's financial recovery and the discipline of its capital reallocation programme.

-

Governance-focused shareholders are registering discomfort with the pace and transparency of the strategic transition regardless of financial outcomes.

Furthermore, a 113% jump in quarterly profit ultimately dominated the conversation despite the governance friction, but the underlying tension between these investor constituencies will persist.

BP vs. Shell: The Supermajor Valuation Gap

The comparison between BP and Shell over the period from early 2022 to mid-2025 is instructive. Shell's approximately 72% share price gain versus BP's flat performance over the same window reflects the valuation premium that capital markets assign to early and decisive strategic clarity. Shell moved toward hydrocarbon capital discipline before BP, avoided the most aggressive renewable overcommitments, and harvested the rerating benefit that BP is only now beginning to capture.

| Company | Strategic Posture | Approximate Capex Mix |

|---|---|---|

| BP (post-reset) | Hydrocarbon pivot underway | ~$10 billion oil and gas, $1.5-2 billion low-carbon |

| Shell | Disciplined hybrid approach | Higher upstream allocation, selective clean energy |

| TotalEnergies | Diversified supermajor model | Balanced upstream and LNG with maintained renewables exposure |

Note: Capex figures represent approximate disclosed or reported ranges. Investors should verify current allocations via each company's investor relations materials.

Key Risks Investors Should Monitor

The BP pivot back to oil and gas carries a compelling near-term financial rationale, but several risk categories deserve careful consideration.

Oil Price Sensitivity. BP's restructured earnings base is heavily leveraged to crude prices, and its commodity price exposure has increased materially as a result of the strategic reset. The geopolitical tailwind from Middle East disruption that inflated Q1 2026 trading profits is inherently temporary, and a sustained price correction would expose the underlying earnings leverage of the new model.

Regulatory and Policy Headwinds. The UK government's decision to extend the North Sea windfall tax following BP's Q1 2026 profit announcement illustrates the political sensitivity of supermajor earnings. Carbon pricing mechanisms and evolving net-zero legislation represent structural long-term risks to hydrocarbon demand. Consequently, BP's reduced clean energy footprint does little to hedge against these risks, particularly as the broader renewable energy transition accelerates across global markets.

Decarbonisation Economics. By narrowing its clean energy portfolio so aggressively, BP reduces its exposure to decarbonisation economics that could reshape competitive dynamics over the medium term. The asymmetry between the speed of divestment and the time required to rebuild strategic capability in low-carbon technologies is a structural constraint worth monitoring closely.

Execution Risk. Managing a $20 billion divestment programme while simultaneously growing upstream production to 2.3 to 2.5 million boe/d by 2030 is an operationally complex undertaking. Furthermore, portfolio simplification at scale creates integration and sequencing risks that can erode value if asset sales are poorly timed or structured. In addition, market volatility impacts from tariff regimes and geopolitical disruption add further uncertainty to the execution timeline.

Strategic Optionality. BP's aggressive reduction of its clean energy portfolio limits its capacity to pivot again if regulatory conditions or demand dynamics shift materially in the years ahead. However, for now, the market has rewarded the focus and clarity that the BP pivot back to oil and gas has delivered.

This article is for informational and educational purposes only and does not constitute investment advice. All financial data, production targets, and analyst commentary referenced are drawn from publicly available reporting. Past performance is not indicative of future results. Readers should conduct their own due diligence before making any investment decisions.

Want to Stay Ahead of Major Energy and Commodity Discoveries?

While BP's strategic pivot back to hydrocarbons signals where the smart capital is flowing, Discovery Alert's proprietary Discovery IQ model scans the ASX daily to deliver real-time alerts on significant mineral discoveries — explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself at the forefront of the next major find.