June 16, 2026

Brazil's strategic position in the global rare earth supply chain revolution reflects mounting concerns about critical minerals energy security and the urgent need for supply chain diversification. Global supply chain vulnerabilities have exposed critical dependencies on single-source suppliers for essential materials that power modern technology. The rare earth elements sector represents one of the most concentrated supply chains in the global economy, creating strategic risks for nations dependent on these materials for defense systems, renewable energy infrastructure, and advanced manufacturing. Brazil emerges as a potential game-changer in this landscape, possessing substantial rare earth deposits that could fundamentally alter global supply dynamics.

Why Brazil Could Reshape Critical Mineral Geopolitics

Brazil's position in the rare earths project in Brazil development represents more than simple resource extraction. The country's vast territorial expanse contains diverse geological formations that host significant rare earth element concentrations, particularly in ionic clay deposits that offer processing advantages over traditional hard rock mining operations. These deposits are distributed across multiple states, reducing single-point-of-failure risks that characterize more geographically concentrated operations elsewhere.

The geopolitical implications extend beyond supply diversification. Brazil's democratic institutions and stable regulatory environment provide investment security that attracts international capital seeking alternatives to politically volatile regions. Furthermore, this stability, combined with the country's established mining infrastructure and experienced workforce, creates conditions favorable for large-scale rare earth development projects.

When big ASX news breaks, our subscribers know first

The Economic Case for Latin American REE Dominance

Economic fundamentals support Brazil's potential emergence as a major rare earth supplier. The country's lower labour costs compared to developed mining jurisdictions, combined with favourable exchange rates, create competitive production cost structures. Additionally, Brazil's extensive transportation infrastructure, including deep-water ports and established logistics networks, facilitates efficient product delivery to global markets.

Domestic demand factors also strengthen the economic case. Brazil's growing renewable energy sector, expanding electric vehicle manufacturing base, and developing defence technology industries create internal markets for processed rare earth materials. Consequently, this domestic consumption potential reduces export dependency and supports higher-value processing activities within the country.

Comparing Brazil's Resource Endowment to Global Competitors

Brazil's rare earth resource base differs significantly from other major producing regions. While traditional producers rely heavily on hard rock deposits requiring energy-intensive processing, Brazil's ionic clay formations offer distinct advantages. These deposits typically contain lower levels of radioactive materials, reducing environmental management complexities and associated costs.

The resource quality comparison reveals favourable characteristics for Brazilian deposits. Higher concentrations of heavy rare earth elements, particularly valuable for advanced technology applications, distinguish Brazilian resources from competitors focused primarily on light rare earth production. This composition profile positions Brazil to serve premium market segments with superior pricing dynamics, supporting the broader critical minerals strategy that many nations are pursuing.

What Makes Brazilian Rare Earth Deposits Uniquely Valuable?

Brazilian rare earth deposits possess distinctive geological characteristics that differentiate them from conventional mining operations worldwide. Understanding these unique properties reveals why international investors view Brazil as a strategic alternative to existing supply sources and how these deposits could reshape global rare earth markets.

Ionic Clay Deposits vs. Traditional Hard Rock Mining

Ionic clay rare earth deposits represent a fundamentally different geological formation compared to hard rock mining operations. In ionic clay systems, rare earth elements exist in an easily extractable form, adsorbed onto clay mineral surfaces rather than locked within crystalline structures. This formation allows for simpler processing techniques that typically require lower energy inputs and generate reduced waste volumes.

The extraction process for ionic clay deposits involves leaching solutions that dissolve the rare earth elements from clay particles, creating a concentrate that undergoes further processing. For instance, this method contrasts sharply with hard rock operations that require crushing, grinding, and complex chemical processing to liberate rare earth elements from host minerals.

Environmental advantages of ionic clay processing include lower water consumption, reduced chemical reagent requirements, and smaller physical footprints compared to traditional hard rock mining operations. These characteristics align with increasingly stringent environmental regulations and corporate sustainability commitments that influence investment decisions in the mining sector.

Grade Advantages and Processing Implications

Grade distribution within Brazilian ionic clay deposits shows consistent rare earth element concentrations across extensive areas, providing operational predictability that supports long-term production planning. Unlike hard rock deposits where grade variations can significantly impact processing efficiency, ionic clay formations typically maintain more uniform composition profiles.

The processing implications extend beyond simple extraction efficiency. Ionic clay deposits often contain favourable ratios of heavy rare earth elements to light rare earth elements, addressing market demand for specialised materials used in permanent magnets, advanced electronics, and defence applications. This composition advantage allows producers to target higher-value market segments with superior pricing dynamics.

Recovery rates from ionic clay processing typically exceed those achieved in hard rock operations, particularly for heavy rare earth elements. However, higher recovery rates directly translate to improved project economics and reduced resource waste, supporting sustainable development principles that attract environmental, social, and governance-focused investors.

Geographic Distribution Across Key Mining States

Brazil's rare earth deposits are distributed across multiple states, creating geographic diversification that reduces operational risks associated with concentrated production areas. This distribution pattern supports simultaneous development of multiple projects while maintaining supply chain resilience against regional disruptions.

Brazilian REE Resource Distribution by State

| State | Primary Deposit Type | Estimated Resources | Development Stage |

|---|---|---|---|

| Minas Gerais | Ionic Clay | High-grade deposits | Advanced exploration |

| Goiás | Mixed deposits | Large tonnage | Early production |

| Bahia | Ionic Clay | Extensive basins | Exploration phase |

| Amazonas | Undeveloped | Preliminary estimates | Early assessment |

The geographic spread across Brazil's mining-experienced states leverages existing infrastructure, skilled labour pools, and established supply chains. States like Minas Gerais bring decades of mining expertise and developed transportation networks, while regions like Bahia offer access to major port facilities for export operations.

How Will Vertical Integration Transform Brazil's Mining Sector?

Vertical integration strategies within Brazil's rare earth sector represent a fundamental shift from traditional raw material export models toward value-added domestic processing. This transformation aims to capture higher margins while building domestic industrial capabilities that support broader economic development objectives, reflecting broader mining industry trends toward downstream value creation.

From Raw Material Exports to Value-Added Processing

The transition from raw rare earth concentrate exports to processed materials and finished products requires substantial capital investment in specialised processing facilities. These investments include separation plants that purify individual rare earth elements, alloy production facilities, and potentially magnet manufacturing operations that serve end-user markets directly.

Processing infrastructure development creates multiplier effects throughout the regional economy. Specialised technical jobs, supporting service industries, and related manufacturing activities cluster around processing facilities, generating economic benefits that extend beyond direct employment at mining and processing operations.

Technological capabilities required for advanced processing involve ion exchange systems, solvent extraction processes, and precision chemical engineering. These technologies require either domestic development programmes or international technology transfer agreements that bring advanced processing knowledge to Brazilian operations.

The Role of State Development Banks in Industrial Strategy

Brazil's development banking system plays a crucial role in financing rare earth sector development through targeted lending programmes that prioritise domestic processing capabilities. These financial institutions provide patient capital for long-term industrial development projects that private markets might consider too risky or requiring excessively long payback periods.

Brazil's development bank is prioritising rare earth projects that demonstrate domestic processing capabilities, with funding criteria emphasising job creation, technology transfer, and reduced export dependency on raw materials.

Funding criteria established by development banks typically require borrowers to demonstrate clear pathways toward domestic value addition, measurable job creation targets, and technology transfer components that build national industrial capabilities. These requirements align government financial support with broader industrial development objectives.

Loan structures from development banks often include favourable interest rates, extended repayment periods, and flexible collateral requirements that accommodate the unique characteristics of mining project development. These terms enable project developers to pursue more ambitious processing capabilities than conventional commercial financing would support.

Technology Transfer Partnerships with International Players

International partnerships bring critical technological expertise to Brazilian rare earth projects while providing foreign companies with access to Brazilian resources and markets. These arrangements typically involve knowledge sharing agreements, joint venture structures, or licensing arrangements that facilitate technology deployment.

Partnership structures often include training programmes that develop domestic technical capabilities, ensuring that international expertise translates into local knowledge retention. These programmes cover specialised processing techniques, quality control systems, and advanced manufacturing processes that support independent operation over time.

Risk-sharing arrangements within technology partnerships distribute development costs and operational risks between domestic and international partners. This risk distribution makes projects more attractive to both parties while accelerating development timelines through combined resources and expertise.

Which Projects Could Define Brazil's REE Future?

Several significant rare earths project in Brazil development initiatives are advancing through various stages of development, from early exploration to pilot plant operations. These projects collectively represent the foundation of Brazil's emergence as a major global rare earth supplier, with different operators pursuing distinct technological and strategic approaches.

Large-Scale Operations Moving Toward Production

The most advanced projects in Brazil's rare earth pipeline are transitioning from development phases toward commercial production, with operators completing definitive feasibility studies, securing financing, and constructing processing facilities. These operations represent the first wave of Brazilian rare earth production that will establish the country's position in global markets.

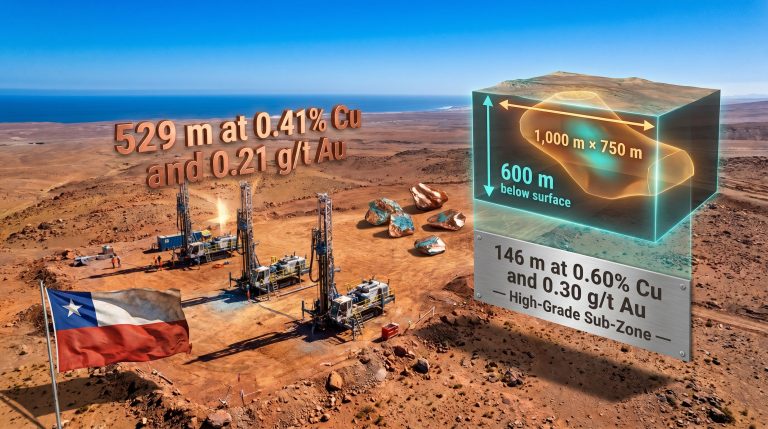

Recent developments include the initiation of pilot plant operations for projects valued at approximately $300 million in total development capital. These pilot facilities serve critical functions in validating processing technologies, optimising recovery rates, and demonstrating commercial viability to investors and off-take partners.

Production capacity targets for near-term operations focus on establishing reliable supply chains while building operational expertise. Initial production volumes are designed to serve specific market segments while providing operational data that supports expansion planning for larger-scale production phases.

Exploration-Stage Projects with High-Grade Potential

Beyond near-term production projects, extensive exploration activities are expanding Brazil's known rare earth resource base through systematic drilling programmes, geochemical surveys, and geological modelling. These exploration efforts focus on identifying deposits suitable for large-scale development while advancing preliminary economic assessments.

Exploration results from various Brazilian states indicate substantial resource potential that could support multiple large-scale operations. The geographic distribution of these exploration projects provides strategic flexibility in selecting optimal development sites based on infrastructure access, environmental considerations, and market proximity.

Integrated Processing Facilities Under Development

Processing infrastructure development represents a critical component of Brazil's rare earth sector evolution, with several operators planning integrated facilities that combine extraction, separation, and value-added processing capabilities. These integrated approaches aim to capture higher margins while serving diverse market requirements.

Key Project Milestones

- Operational Projects: Serra Verde (Minaçu) achieving commercial production in 2024

- Advanced Development: Multiple ionic clay projects targeting mid-2020s production

- Processing Infrastructure: Separation facilities planned for Bahia's industrial complex

- Investment Scale: Projects requiring $300M+ in development capital

Facility planning emphasises modular designs that enable phased capacity expansion based on market demand and operational experience. This approach reduces initial capital requirements while maintaining flexibility to scale operations as markets develop and technology improves.

The next major ASX story will hit our subscribers first

What Are the Environmental and Social Challenges?

Environmental and social considerations represent critical factors in Brazilian rare earth project development, with regulatory requirements, community engagement needs, and environmental protection measures significantly influencing project timelines, costs, and operational approaches. These challenges reflect broader concerns about sustainable mining practices that align with global environmental standards.

Community Impact Assessment and Indigenous Rights

Community consultation processes for rare earth projects involve extensive stakeholder engagement programmes that address local concerns, identify potential impacts, and develop mitigation strategies. These processes are particularly complex in regions with indigenous populations, where constitutional protections require specific consultation protocols.

Indigenous rights considerations include territorial boundary assessments, cultural impact evaluations, and benefit-sharing negotiations that respect traditional land use patterns and community governance structures. These requirements often extend project development timelines but are essential for securing social licence to operate.

Benefit-sharing arrangements typically include direct financial payments, infrastructure development commitments, and employment opportunities for local community members. These agreements aim to ensure that local populations receive tangible benefits from resource development activities in their territories.

Conservation Area Overlaps and Biodiversity Concerns

Environmental protection requirements in Brazil include comprehensive biodiversity assessments, habitat preservation commitments, and restoration obligations that address potential ecological impacts from mining activities. These requirements are particularly stringent in regions with high biodiversity value or proximity to protected areas.

Conservation area overlaps require careful site planning to avoid protected zones while maintaining viable project economics. Alternative site selection processes often involve extensive environmental surveys and geological assessments to identify optimal development locations that minimise ecological impacts.

Regulatory Framework and Licensing Requirements

Brazilian environmental licensing processes involve multiple regulatory agencies and require detailed environmental impact assessments, public consultation periods, and monitoring plan development. These processes typically require 18-36 months to complete, depending on project complexity and environmental sensitivity.

Environmental and Social Risk Factors

| Risk Category | Primary Concerns | Mitigation Strategies |

|---|---|---|

| Community Impact | Rural settlement displacement | Stakeholder consultation programmes |

| Environmental | Conservation area overlap | Alternative site selection |

| Regulatory | Complex licensing process | Early engagement with authorities |

| Legacy Issues | Historical contamination | Comprehensive environmental assessment |

Regulatory compliance strategies emphasise early engagement with environmental agencies, comprehensive baseline studies, and adaptive management approaches that respond to changing environmental conditions and regulatory requirements.

How Does International Investment Drive Development?

International investment flows into Brazil's rare earth sector reflect global supply chain diversification strategies and the search for alternatives to concentrated production sources. These investment patterns involve diverse funding sources, partnership structures, and strategic objectives that collectively support sector development while helping mitigate trade war impacts on global supply chains.

Australian Mining Companies Leading Exploration

Australian mining companies bring significant technical expertise and financial resources to Brazilian rare earth projects, leveraging their experience in developing similar deposits in other jurisdictions. These companies often serve as project operators while partnering with Brazilian entities to navigate local regulatory requirements and market conditions.

Investment strategies from Australian operators typically emphasise rapid development timelines, proven processing technologies, and established off-take relationships that provide market access for Brazilian production. These capabilities complement Brazilian resource endowments and regulatory knowledge.

Operational expertise from Australian companies includes specialised mining techniques, environmental management systems, and safety protocols that meet international standards while complying with Brazilian regulatory requirements. This expertise transfer supports sector development while building domestic capabilities.

Strategic Partnerships with Technology Providers

Technology partnerships involve specialised engineering companies, equipment manufacturers, and process technology developers that provide critical capabilities for rare earth processing. These partnerships often include licensing agreements, equipment supply contracts, and technical support services.

Foreign investment in Brazilian rare earth projects reflects global supply chain diversification strategies, with Australian, European, and Japanese entities providing both capital and technical expertise for integrated development models.

Partnership structures typically include performance guarantees, technology warranties, and ongoing technical support that ensure processing systems operate according to design specifications. These arrangements reduce technical risks while ensuring access to proven technologies.

Government-to-Government Cooperation Frameworks

Bilateral cooperation agreements between Brazil and rare earth-importing nations create frameworks for investment promotion, technology transfer, and trade facilitation. These agreements often include government financing support, investment protection measures, and preferential procurement arrangements.

Diplomatic support for private sector investment includes trade promotion activities, regulatory cooperation initiatives, and joint research programmes that support sector development while strengthening bilateral economic relationships.

Capital Requirements and Financing Structures

Capital requirements for Brazilian rare earth projects typically range from $100 million to $500 million, depending on production scale, processing complexity, and infrastructure requirements. These capital needs require diverse funding sources including equity investment, project financing, and development bank support.

Financing structures often combine multiple funding sources to optimise capital costs and risk distribution. Common structures include senior debt facilities, subordinated financing, equity partnerships, and off-take prepayment arrangements that provide capital while securing market access.

Risk mitigation strategies within financing arrangements include political risk insurance, currency hedging programmes, and commodity price protection mechanisms that address key risks associated with international mining investment in emerging markets.

What Timeline Should Investors Expect for Production Ramp-Up?

Production timeline expectations for Brazilian rare earth projects reflect the complex development requirements, regulatory processes, and market development activities required to establish commercial operations. Understanding these timelines helps investors and market participants plan for supply availability and investment returns.

Near-Term Production Targets (2025-2027)

The immediate timeline for Brazilian rare earth production focuses on projects that have completed feasibility studies, secured financing, and initiated construction activities. These near-term operations will establish Brazil's initial market presence while building operational expertise for subsequent expansion phases.

Pilot plant operations currently underway provide critical operational data that validates processing technologies and economic assumptions. These pilot facilities typically operate for 6-12 months before transitioning to commercial-scale production, assuming successful demonstration of technical and economic viability.

Production ramp-up schedules for near-term projects typically involve gradual capacity increases over 12-18 months as operators optimise processing parameters, train personnel, and establish supply chain relationships. This gradual approach reduces operational risks while building market confidence.

Medium-Term Processing Capability Development

Processing infrastructure development for medium-term production requires 3-5 years for design, construction, and commissioning of separation facilities and value-added processing capabilities. These timelines reflect the technical complexity of rare earth processing and the need for specialised equipment and expertise.

Technology deployment strategies often involve phased implementation approaches that begin with basic separation capabilities before adding advanced processing functions. This staging reduces initial capital requirements while enabling operators to optimise each processing stage before adding complexity.

Long-Term Supply Chain Integration Goals

Long-term development objectives for Brazilian rare earth operations include full supply chain integration from mining through finished product manufacturing. These ambitious goals require substantial additional investment and technology development over 7-10 year timeframes.

Production Timeline Analysis

- Phase 1 (2025-2026): Existing operations scaling production

- Phase 2 (2027-2028): New mines entering production phase

- Phase 3 (2029-2030): Integrated processing facilities operational

- Phase 4 (2030+): Full value chain from mining to magnet production

Supply chain integration strategies involve downstream processing investments, end-user market development, and technology partnerships that support finished product manufacturing. These strategies aim to capture maximum value from Brazilian rare earth resources while serving global market demand.

How Will Brazil Navigate Geopolitical Supply Chain Pressures?

Geopolitical considerations significantly influence Brazil's rare earth sector development as the country positions itself as an alternative supplier in increasingly complex global supply chains. Understanding these dynamics reveals how Brazil can leverage its resources for strategic advantage while managing international relationships.

Reducing Global Dependence on Single-Source Suppliers

Supply chain diversification imperatives drive international interest in Brazilian rare earth development as consuming nations seek alternatives to concentrated production sources. This diversification demand creates market opportunities for Brazilian producers while supporting premium pricing for reliable, politically stable supply sources.

Strategic positioning as a reliable alternative supplier requires Brazil to demonstrate long-term production capability, consistent quality standards, and stable political environments that support sustained supply relationships. These factors influence international investment decisions and off-take agreement structures.

Market positioning strategies emphasise Brazil's democratic institutions, stable regulatory environment, and established mining sector experience as differentiating factors that provide supply security for strategic materials consumers.

Strategic Alliances and Technology Transfer Agreements

International alliance formation enables Brazil to access advanced processing technologies, secure market access, and obtain development financing while maintaining domestic control over resource development. These alliances typically involve mutual benefit structures that serve both Brazilian development objectives and international supply security needs.

Technology transfer arrangements within strategic alliances ensure that Brazil develops domestic capabilities while accessing proven processing technologies. These arrangements support independent operational capabilities over time while reducing technological dependence on international partners.

Diplomatic engagement supports private sector alliance formation through bilateral investment treaties, trade agreements, and regulatory cooperation frameworks that reduce investment risks and facilitate technology transfer.

Balancing Export Revenue with Domestic Industrial Development

Export strategy development must balance immediate revenue generation from raw material sales against longer-term industrial development objectives that capture higher value-added activities. This balance influences investment incentives, regulatory policies, and market development strategies.

Domestic market development for processed rare earth materials supports industrial diversification while reducing export dependence. Growing domestic demand from renewable energy, electronics manufacturing, and defence sectors provides market foundations for value-added processing capabilities.

What Are the Key Risk Factors for Project Success?

Risk assessment for Brazilian rare earth projects encompasses technical, regulatory, market, and operational factors that could impact project development timelines, costs, and ultimate success. Understanding these risks enables better investment decision-making and risk management strategies.

Technical Challenges in Processing Technology

Processing technology risks include equipment performance uncertainties, recovery rate variations, and product quality consistency challenges that could impact project economics. These technical risks are particularly relevant for projects utilising newer processing technologies or operating with complex ore compositions.

Technology validation through pilot plant operations provides critical risk mitigation by demonstrating processing performance under actual operating conditions. Pilot results inform final design decisions while reducing technical uncertainties that affect project financing and development timelines.

Technical support arrangements with technology providers include performance guarantees, troubleshooting assistance, and upgrade pathways that address potential processing challenges. These arrangements reduce operator risk while ensuring access to technical expertise.

Infrastructure Development Requirements

Infrastructure constraints including transportation access, power supply availability, and water resource access can significantly impact project development costs and timelines. Remote project locations may require substantial infrastructure investments that affect project economics.

Infrastructure development strategies often involve partnerships with government agencies, utility providers, and transportation companies to develop shared infrastructure solutions. These partnerships can reduce individual project costs while supporting regional development objectives.

Market Demand Volatility and Price Risk

Commodity price volatility represents a significant risk factor for rare earth projects, with prices subject to demand fluctuations, supply disruptions, and geopolitical influences. Price volatility can impact project financing, development decisions, and operational profitability.

Market risk mitigation strategies include long-term off-take agreements, price hedging arrangements, and diversified product portfolios that reduce exposure to individual rare earth element price volatility. These strategies provide revenue stability while maintaining upside exposure to favourable market conditions.

Demand forecasting challenges reflect rapid technological changes in end-user markets, evolving environmental regulations, and shifting geopolitical preferences that influence rare earth consumption patterns. These uncertainties complicate long-term planning and investment decisions.

Future Outlook: Brazil's Path to REE Supply Chain Leadership

Brazil's trajectory toward rare earth supply chain leadership depends on successful execution of current development projects, continued investment in processing capabilities, and effective navigation of international market dynamics. The rare earths project in Brazil represents a transformative opportunity for the nation to establish itself as a critical player in global supply chains.

Production Capacity Projections Through 2030

Production capacity development scenarios suggest Brazil could achieve significant global market share by 2030 through successful execution of current project pipelines and continued exploration success. These projections assume favourable market conditions, successful project execution, and continued international investment flows.

Capacity expansion potential beyond initial projects could position Brazil among the top three global rare earth producers, depending on market demand growth and competitive responses from other producing regions. This potential requires sustained investment and successful project development over the remainder of the decade.

Market share objectives for Brazilian producers emphasise reliable supply, consistent quality, and competitive pricing that establish long-term customer relationships. Achieving these objectives requires operational excellence and continued investment in processing technology and capabilities.

Technology Development and Innovation Hubs

Innovation ecosystem development around rare earth processing could establish Brazil as a centre of excellence for ionic clay processing technologies and related applications. This technological leadership would support sustained competitive advantages while attracting continued international investment and partnership.

Research and development initiatives linking universities, government research institutions, and private companies create knowledge networks that support continued technological advancement and innovation in rare earth processing and applications through partnerships with companies like Brazilian Rare Earths.

Regional Economic Impact and Job Creation Potential

Economic impact projections for Brazil's rare earth sector development include direct employment in mining and processing operations, indirect employment in supporting industries, and induced economic activity from increased regional income levels. These impacts support broader economic development objectives while creating political support for continued sector development.

Regional development strategies emphasise sustainable economic growth, environmental protection, and community benefit-sharing that create lasting positive impacts from rare earth resource development. Furthermore, these strategies are essential for maintaining social licence to operate and political support for sector growth, as highlighted in industry analysis of Brazil's emerging role in global critical minerals supply.

Please note: This analysis is based on publicly available information and involves forward-looking projections that are subject to various risks and uncertainties. Investment decisions should be based on comprehensive due diligence and professional financial advice. Market conditions, regulatory environments, and project execution capabilities may differ from current expectations, potentially affecting outcomes discussed in this analysis.

Ready to Capitalise on Critical Minerals Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities in the critical minerals sector ahead of the broader market. Explore how major mineral discoveries have generated substantial returns by visiting Discovery Alert's dedicated discoveries page and begin your 30-day free trial today to position yourself at the forefront of the next mining breakthrough.