June 16, 2026

Global rare earth markets are experiencing unprecedented transformation as supply chain diversification strategies reshape fundamental economic relationships. Traditional dependencies on single-source production models face mounting pressure from geopolitical tensions, technological advancement requirements, and strategic resource security imperatives across developed economies. Brazil's positioning within this evolving landscape highlights the growing importance of Brazil rare earth project developments in addressing global supply chain vulnerabilities.

The emergence of alternative production pathways, particularly through secondary source processing, represents more than operational innovation—it signals structural realignment of critical mineral supply architecture. These developments occur within broader macroeconomic contexts where resource independence directly correlates with technological sovereignty and national security considerations.

Understanding Brazil's Strategic Position in Critical Mineral Markets

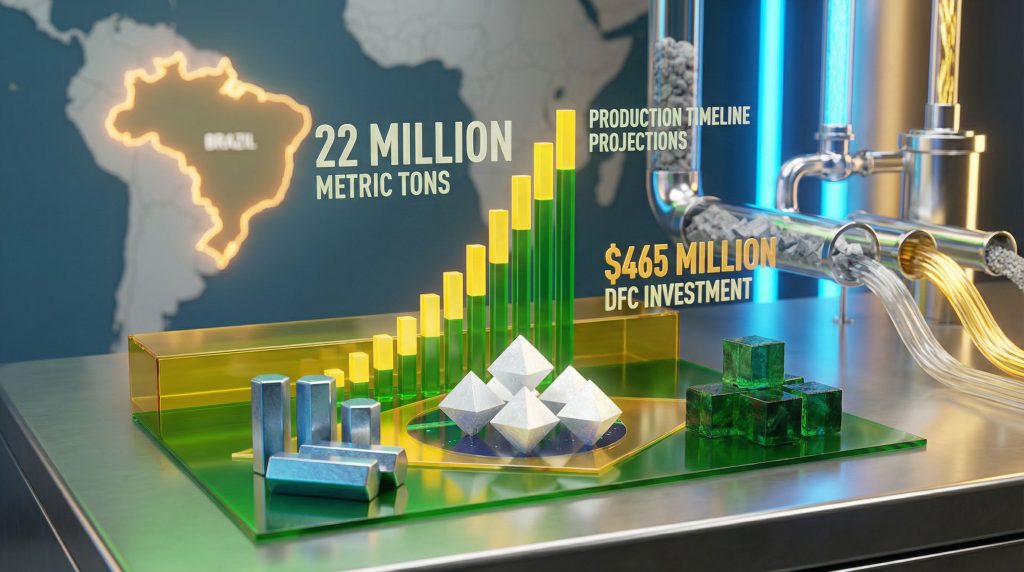

Brazil's position in global rare earth markets stems from geological endowments that place the country among the world's most significant reserve holders. With approximately 22 million metric tons of rare earth element reserves, Brazil controls the world's second-largest reserve base, trailing only China's estimated 44 million metric tons.

This geological advantage occurs within a complex geopolitical landscape where China maintains dominant market positions across the rare earth supply chain. Chinese operations control approximately 70% of global rare earth production and an overwhelming 90% of refining and processing capacity. This concentration creates systemic vulnerabilities for Western economies dependent on rare earth elements for defence systems, renewable energy infrastructure, and advanced manufacturing.

Furthermore, the strategic implications extend beyond simple commodity availability. Rare earth elements encompass 17 elements—15 lanthanides plus scandium and yttrium—that serve critical functions in permanent magnets, phosphors, catalysts, and specialised alloys. Defence applications require rare earth permanent magnets for aircraft engine components, radar systems, and missile guidance systems.

Renewable energy infrastructure depends on rare earth magnets in wind turbine generators, with typical installations requiring 200-600 kg of rare earth permanent magnets per unit. This dependency has intensified focus on energy transition security considerations across Western governments.

Electric vehicle manufacturing represents another demand driver, as EV motors utilise permanent magnets containing neodymium and dysprosium. Global vehicle electrification targets across Europe, North America, and Asia create structural demand growth that existing supply chains struggle to accommodate without Chinese dependencies.

Brazil's emergence as an alternative supplier enables fundamental restructuring of these supply relationships. Western manufacturers can potentially develop integrated supply networks sourcing raw materials from Brazil, processing through allied nations, and manufacturing end products without Chinese supply chain touchpoints. This architecture supports product qualification for government procurement programmes requiring domestic content and supply chain transparency.

When big ASX news breaks, our subscribers know first

What Makes Brazil's Phosphogypsum Processing Model Economically Superior?

Brazil's innovative approach to rare earth production centres on extracting valuable elements from phosphogypsum—industrial waste generated during phosphoric acid production for fertiliser manufacturing. This methodology fundamentally alters traditional rare earth economics by eliminating primary mining requirements while addressing environmental waste management challenges.

Global phosphoric acid production generates approximately 280-300 million metric tons of phosphogypsum annually, creating abundant feedstock availability. Brazil's established fertiliser industry produces significant phosphogypsum volumes, providing secure feedstock access without commodity price volatility associated with primary mining operations.

The economic advantages of this processing model include:

- Elimination of exploration and development costs typically ranging $500 million to $2 billion for greenfield rare earth projects

- Reduced environmental liability through processing existing waste streams rather than creating new environmental impacts

- Accelerated project timelines avoiding 3-5 year exploration and permitting phases required for primary mining

- Operational synergies leveraging existing industrial infrastructure and technical expertise

Moreover, this approach represents a significant advancement in mine reclamation innovation, demonstrating how waste streams can become valuable resources. The Uberaba project demonstrates these economic principles through specific operational parameters.

The project targets processing throughput of 2.7 million metric tons annually over an initial 30-year operational life. Feedstock specifications include 0.51% Total Rare Earth Oxide (TREO) content with 57% recovery rates based on collaborative testwork between project partners.

Financial performance metrics highlight the economic advantages:

| Performance Metric | Uberaba Project |

|---|---|

| Post-tax Net Present Value | $916 million |

| Post-tax Internal Rate of Return | 45% |

| Average Annual EBITDA | $217 million |

| Payback Period | 1.7 years |

These financial metrics contrast favourably with traditional rare earth mining projects typically requiring 4-7 year payback periods and generating lower internal rates of return due to higher capital requirements and operational complexity.

The processing methodology involves several integrated steps:

- Phosphogypsum feedstock sourcing from phosphoric acid production residue

- Chemical treatment and cleaning of phosphogypsum stream

- Rare earth element extraction using proprietary intellectual property

- Separation into distinct products: Neodymium-Praseodymium (NdPr) oxide and Samarium-Europium-Gadolinium plus (SEG+)

- Purification to >99.5% specification meeting industrial quality standards

- Cleaned residue return to existing phosphoric acid facilities

This integrated approach eliminates separate tailings management requirements and environmental remediation costs associated with primary mining operations. The partnership model leverages existing industrial infrastructure while applying advanced processing technology to waste streams.

Brazil's Production Capacity Development and Market Integration

Brazil's rare earth production capacity development follows projected growth trajectories that position the country as a significant alternative supplier within global markets. However, this expansion occurs within the broader context of mining industry evolution, where technological advancement and sustainability considerations drive operational decisions.

Current projections indicate progressive capacity expansion through multiple development phases.

Projected Production Milestones:

| Development Phase | Timeline | Annual Capacity (Metric Tons REO) |

|---|---|---|

| Initial Operations | 2024-2025 | 2,000-3,000 |

| Operational Optimisation | 2026-2027 | 4,800-6,500 |

| Expansion Phase | 2028-2030 | 10,000-13,000 |

| Sector Maturation | 2030+ | 20,000+ |

These capacity targets assume successful completion of definitive feasibility studies, financing arrangements, regulatory approvals, and construction execution within anticipated timelines. In addition, the progression reflects typical rare earth project development patterns involving initial production ramp-up, operational optimisation, and potential facility expansion.

Production ramp considerations include:

- Technology transfer efficiency from existing operations to new facilities

- Feedstock supply reliability from established phosphoric acid production

- Market demand growth supporting expanded production volumes

- Regulatory compliance meeting environmental and operational standards

The initial production phase targets 2,000-3,000 metric tons REO annually, reflecting early operational optimisation and feedstock supply establishment. Subsequently, expansion to 4,800-6,500 metric tons indicates full operational startup and initial efficiency improvements.

Medium-term growth projections of 10,000-13,000 metric tons REO reflect potential facility debottlenecking, efficiency improvements, and additional processing modules. The 2030+ sector-wide capacity target of 20,000+ metric tons suggests multiple projects achieving operational status across Brazil's rare earth development landscape.

Market integration factors influencing capacity utilisation include:

- Long-term offtake agreements with major industrial consumers

- Product diversification strategies processing multiple rare earth elements

- Supply chain coordination with downstream manufacturing operations

- Price volatility management through contract structures and inventory policies

Recent rare earth price volatility, including declines of approximately 70% over two years, demonstrates market risk factors requiring strategic management through diversified product portfolios and long-term contract arrangements.

International Development Finance and Strategic Resource Access

Development finance institutions increasingly function as strategic tools for securing critical mineral supply chain access rather than traditional development assistance providers. This evolution reflects growing recognition that resource security directly impacts national economic and security interests.

The involvement of development finance institutions in Brazilian rare earth projects demonstrates coordinated Western efforts to diversify supply sources away from Chinese dependencies. These financing mechanisms create direct government exposure to supply chain outcomes while supporting emerging market development objectives.

The U.S. Development Finance Corporation recently announced $465 million in funding for Brazilian rare earth projects, highlighting the strategic importance of these developments. This significant commitment underscores the geopolitical dimension of critical mineral supply chain security.

Development finance characteristics in rare earth projects include:

- Sovereign backing providing enhanced credit quality and political risk mitigation

- Equity participation options creating direct government ownership stakes in strategic operations

- Technology transfer requirements supporting indigenous technical capability development

- Integrated supply chain coordination linking financing to strategic end-user relationships

This financing model contrasts with traditional commercial project finance by incorporating strategic resource access objectives alongside financial returns. Development finance institutions accept potentially lower financial returns in exchange for supply chain security benefits.

Strategic financing mechanisms encompass:

- Direct lending for project development and expansion

- Equity investment creating government ownership participation

- Political risk insurance protecting against regulatory and operational disruptions

- Technical assistance supporting operational capability development

The integration of development finance with strategic mineral projects represents economic diplomacy where capital deployment secures resource access more effectively than traditional trade agreements. This approach creates mutual benefits through emerging market development and developed economy resource security.

Financing terms typically include:

- Offtake agreement requirements linking production to strategic consumers

- Local content mandates supporting domestic economic development

- Environmental compliance standards ensuring sustainable operational practices

- Technology sharing provisions facilitating knowledge transfer and capability building

The Minerals Security Partnership Framework and Supply Chain Architecture

The Minerals Security Partnership represents multilateral coordination mechanisms designed to develop integrated supply chains that provide alternatives to Chinese rare earth dominance. This framework connects resource-rich countries with manufacturing economies through coordinated development finance, technology transfer, and supply chain integration.

Brazil's participation in this framework positions the country as a cornerstone supplier within Western supply chain architecture. The partnership enables coordination between Brazilian production capacity and Western manufacturing demand while establishing quality standards and supply chain transparency requirements.

Framework objectives include:

- Supply chain diversification reducing dependence on single-source suppliers

- Technology standardisation ensuring compatibility across partner nations

- Strategic reserve coordination enabling emergency supply arrangements

- Investment coordination preventing duplication and optimising resource allocation

The partnership structure facilitates development of "allied-source" supply chains that exclude Chinese processing dependencies for strategically sensitive applications. Defence contractors, renewable energy infrastructure developers, and electric vehicle manufacturers can source materials through documented supply chains meeting government procurement requirements.

Supply chain integration benefits include:

- Reduced geopolitical risk through diversified supplier relationships

- Enhanced quality assurance through coordinated standards and certification

- Improved supply reliability via multiple source availability

- Strategic stockpiling coordination enabling emergency response capabilities

This multilateral approach creates regional supply networks spanning raw material extraction, processing and refining, component manufacturing, and end-product assembly. Brazil's role encompasses primary material supply and potentially downstream processing as technical capabilities develop.

Regional integration models include:

- Western Hemisphere networks connecting North and South American suppliers

- Atlantic partnerships linking Brazilian sources with European processors

- Pacific cooperation coordinating with Australian and Japanese partners

- Technology sharing agreements facilitating capability development across partner nations

Economic Impact Analysis and Regional Development

Brazil's rare earth sector development generates significant economic impacts extending beyond direct mining operations. The concentration of development in Goiás, Minas Gerais, and Bahia states creates regional economic clusters around strategic mineral processing infrastructure.

Regional economic transformation includes:

- Industrial ecosystem development supporting industries, logistics networks, and technical services

- High-skilled employment creation in engineering, processing, and research positions

- Export revenue diversification reducing dependence on traditional commodity exports

- Technology transfer benefits through advanced processing techniques and equipment manufacturing

The economic multiplier effects of rare earth development extend throughout regional economies. Infrastructure development, supporting services, and downstream manufacturing create employment and economic activity beyond direct project operations.

Investment multiplier analysis indicates:

Every $1 billion invested in rare earth processing infrastructure typically generates $2.5-3.5 billion in total economic activity through supply chain integration, supporting services, and downstream manufacturing development. This multiplier effect reflects the high-technology nature of rare earth processing and the supporting infrastructure requirements.

National economic implications encompass:

- Foreign exchange earnings from high-value exports to developed markets

- Technology sector development through advanced processing capabilities

- Industrial diversification beyond traditional mining and agricultural exports

- Strategic resource positioning enhancing Brazil's geopolitical influence

Based on current rare earth pricing and projected production capacity, Brazil's rare earth sector could potentially generate $2-4 billion annually in export revenues by 2030, representing significant foreign exchange contributions to the Brazilian economy.

Employment creation patterns include:

- Direct operations employment in processing facilities and supporting infrastructure

- Indirect employment through supply chain integration and supporting services

- Induced employment from regional economic activity generated by project operations

- Technology sector employment in research, development, and technical services

The next major ASX story will hit our subscribers first

Environmental and Social Considerations in Economic Viability

Brazil's rare earth development faces complex environmental and social challenges that directly impact long-term economic sustainability. Current development applications indicate potential conflicts with existing land uses that could disrupt operations and increase regulatory compliance costs.

Mining applications reportedly overlap with 96 rural settlements, creating stakeholder management challenges requiring comprehensive community engagement and potentially costly mitigation measures. These social factors directly influence operational continuity and regulatory approval timelines.

Risk mitigation strategies encompass:

- Community engagement protocols including stakeholder consultation and benefit-sharing agreements

- Environmental impact minimisation through focus on waste processing rather than primary extraction

- Regulatory compliance investment in proactive environmental and social governance measures

- Technology innovation developing lower-impact processing techniques and waste management

The phosphogypsum processing model provides inherent environmental advantages compared to primary mining by processing existing waste streams rather than creating new environmental impacts. This approach exemplifies mining sustainability transformation principles that prioritise environmental stewardship alongside economic development.

This approach reduces environmental liability while addressing existing industrial waste management challenges.

Environmental management considerations include:

- Waste stream processing converting industrial byproducts to valuable commodities

- Residue management ensuring cleaned phosphogypsum meets environmental standards

- Water management minimising freshwater consumption and wastewater generation

- Air quality protection controlling emissions from processing operations

Social licence maintenance requires ongoing community engagement addressing concerns about industrial development impacts on local communities and traditional land uses. Successful project execution depends on maintaining stakeholder support through transparent communication and benefit sharing.

Stakeholder management approaches include:

- Early engagement with affected communities and indigenous groups

- Economic benefit sharing through employment, procurement, and community investment

- Cultural preservation respecting traditional land uses and cultural sites

- Ongoing consultation maintaining dialogue throughout project lifecycles

Long-term Market Dynamics and Competitive Positioning

Global rare earth demand projections indicate sustained growth driven by technological advancement and clean energy transition requirements. Industry analysts forecast 7-10% annual demand growth through 2030, substantially exceeding historical consumption patterns.

Primary demand drivers include:

- Electric vehicle manufacturing requiring permanent magnet motors

- Renewable energy infrastructure utilising wind turbine generator magnets

- Consumer electronics incorporating rare earth elements in smartphones, laptops, and appliances

- Defence applications demanding advanced electronics and guidance systems

This demand growth occurs within volatile pricing environments that create both opportunities and risks for new production capacity. Recent price declines demonstrate market cyclicality requiring strategic management through diversified product portfolios and long-term supply agreements.

Several companies are positioning themselves strategically within this market, including Australian miners exploring Brazilian opportunities to capitalise on the country's geological advantages. However, this expansion requires careful consideration of market timing and project execution capabilities.

Brazil's competitive advantages include:

- Lower labour costs compared to developed markets while maintaining technical expertise

- Abundant energy supply from hydroelectric power providing low-cost electricity for processing

- Established infrastructure including port facilities and transportation networks

- Regulatory framework with established mining regulatory processes and clear permitting procedures

Technology and innovation capabilities encompass:

- Research institution partnerships with universities and government research facilities

- International collaboration with Western technology providers and development partners

- Process optimisation focusing on continuous improvement in extraction and processing efficiency

- Environmental technology development emphasising cleaner processing techniques and waste management

Brazil's cost structure advantages position the country favourably within global production cost curves. The elimination of primary mining costs through phosphogypsum processing creates structural cost advantages compared to traditional rare earth operations.

Market positioning strategies include:

- Long-term contract development securing stable pricing and demand relationships

- Product quality differentiation meeting stringent specifications for high-value applications

- Supply chain integration developing downstream processing capabilities

- Strategic partnerships with major industrial consumers and technology providers

Investment Opportunities and Risk Assessment Framework

Brazil's rare earth sector presents multiple investment themes spanning infrastructure development, technology innovation, downstream manufacturing, and supporting services. Each investment category offers distinct risk-return profiles requiring specialised analysis and due diligence approaches.

For investors seeking exposure to this sector, understanding comprehensive investing guide strategies becomes essential for navigating the complexities of critical mineral markets.

Primary investment opportunities include:

Infrastructure Development: Processing facilities, transportation networks, port capacity expansion, and power supply systems require substantial capital investment with long-term payback periods but stable cash flow characteristics.

Technology Innovation: Advanced separation techniques, environmental remediation systems, and automation technologies offer high returns but carry technical execution risks and intellectual property considerations.

Downstream Manufacturing: Magnet production, alloy manufacturing, and component assembly create value-added opportunities with shorter payback periods but require market access and technical expertise.

Supporting Services: Engineering, logistics, financial services, and equipment supply provide stable revenue opportunities with lower capital requirements but face competitive pressures.

Comprehensive risk assessment framework:

| Risk Category | Specific Risk Factors | Mitigation Strategies |

|---|---|---|

| Market Risk | Price volatility, demand fluctuations, competitive dynamics | Long-term contracts, product diversification, market research |

| Regulatory Risk | Environmental compliance, permitting delays, policy changes | Proactive engagement, compliance investment, legal analysis |

| Operational Risk | Technical challenges, supply disruptions, quality issues | Technology partnerships, redundancy planning, quality systems |

| Geopolitical Risk | Trade disputes, sanctions, diplomatic tensions | Diversified market access, diplomatic engagement, contingency planning |

Investment timing considerations reflect:

- Project development phases requiring different capital commitments and risk profiles

- Market cycle positioning optimising entry timing relative to price cycles

- Technology maturation balancing early-mover advantages with execution risks

- Regulatory evolution considering changing environmental and social requirements

Successful investment strategies require thorough due diligence addressing technical, commercial, regulatory, and financial factors. The complexity of rare earth markets demands specialised expertise in geology, metallurgy, chemistry, and industrial applications.

Due diligence priorities encompass:

- Resource verification confirming feedstock availability and quality specifications

- Technology validation ensuring processing techniques achieve target recoveries and product specifications

- Market analysis validating demand projections and pricing assumptions

- Regulatory assessment confirming permitting status and compliance requirements

- Financial modelling stress-testing assumptions and scenario analysis

Future Outlook and Strategic Implications

Brazil's rare earth sector development represents a strategic inflection point in global supply chain architecture. The country's emergence as a major supplier enables fundamental restructuring of critical mineral dependencies while creating new economic opportunities and geopolitical relationships.

Success in this transformation depends on maintaining competitive cost structures while addressing environmental and social challenges that could undermine long-term sustainability. The integration of Brazilian production into Western supply chains will likely accelerate over the next decade, driven by geopolitical considerations and technological advancement requirements.

Strategic success factors include:

- Operational excellence maintaining cost competitiveness and production reliability

- Environmental stewardship ensuring sustainable practices and community support

- Technology advancement developing innovative processing techniques and product specifications

- Market integration establishing long-term relationships with strategic customers

The transformation positions Brazil as a critical partner in global efforts to reduce dependence on Chinese rare earth supplies while meeting growing demand for clean energy and advanced technology applications. This role creates both opportunities and responsibilities requiring careful strategic planning and execution.

Long-term strategic implications encompass:

- Geopolitical influence through strategic resource control and supply chain participation

- Economic development via high-technology industries and export revenue generation

- Environmental leadership demonstrating sustainable resource extraction and processing

- Technology advancement building indigenous capabilities in critical mineral processing

The next decade will determine whether Brazil successfully transforms geological endowments into sustainable competitive advantages within global rare earth markets. Success requires coordinated efforts across government, industry, and civil society to build the technical capabilities, infrastructure, and institutional frameworks necessary for long-term leadership in this strategically critical sector.

This analysis is provided for educational purposes and should not be considered as investment advice. Potential investors should conduct thorough due diligence and consult with qualified professionals before making investment decisions in the rare earth sector or related markets.

Looking to Capitalise on Brazil's Rare Earth Revolution?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant critical mineral discoveries across the ASX, helping investors identify actionable opportunities in the rapidly evolving rare earth sector before they hit mainstream markets. Start your 14-day free trial today and gain the market-leading edge you need to navigate this transformative period in global supply chains.