June 5, 2026

When Capital Concentration Meets Critical Minerals Scarcity

Across the global mining sector, a structural tension has been building for years between the enormous capital requirements of large-scale project development and the limitations of conventional equity financing. The Canada Nickel Crawford financing strategy represents the most advanced real-world test of whether this tension can be resolved without destroying shareholder value. For junior nickel developers in particular, the path from feasibility to construction has historically been paved with value destruction, as successive equity raises dilute early shareholders to the point where the project's eventual success barely translates into meaningful returns.

What makes the current moment different is the convergence of two forces that rarely align: a supply-constrained commodity market repricing Western nickel assets upward, and an evolving government funding landscape that has created genuine alternatives to open-market equity. Understanding the Indonesian nickel price trends is essential context here, as they have fundamentally altered the calculus for Western developers. For projects with the right combination of scale, economics, and strategic positioning, the traditional dilution trap may no longer be inevitable.

When big ASX news breaks, our subscribers know first

Crawford's Position in a Supply-Concentrated Nickel Market

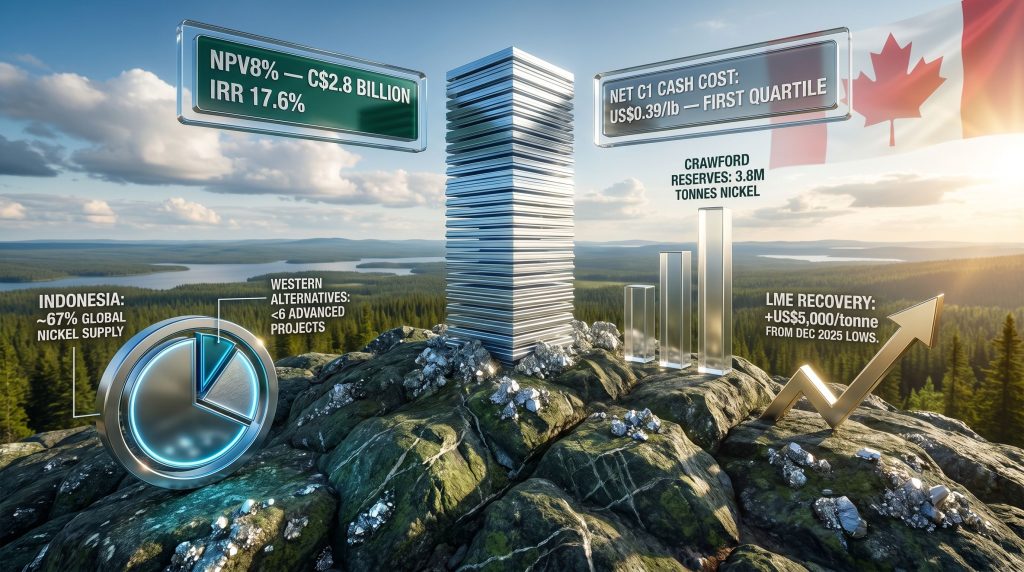

To understand why the Crawford project commands attention beyond its standalone economics, it is necessary to first understand the structural dynamics governing the global nickel market. Indonesia currently controls approximately 67% of global nickel supply, a concentration that, according to data cited in Canada Nickel's May 2026 investor presentation from the U.S. Energy Information Administration and Macquarie, exceeds OPEC's historical peak share of oil production. This is not merely a commodity pricing observation; it represents a systemic vulnerability embedded into the supply chains of every major battery manufacturer and industrial nickel consumer operating outside Indonesian jurisdiction.

How Indonesian Supply Policies Are Reshaping Western Markets

Since late 2025, Indonesia has implemented a sequence of supply-constricting policy measures including ore quota reductions, bans on new nickel pig iron and high-pressure acid leach capacity, and tiered export royalty structures. The Indonesian nickel industry challenges created by these policies have been substantial. The market response has been equally significant: LME nickel prices have risen more than US$5,000 per tonne from December 2025 lows, reflecting a fundamental repricing of Indonesian supply risk.

Within this environment, Crawford's resource scale takes on strategic significance that goes well beyond typical project metrics. The deposit holds 3.8 million tonnes of contained nickel in proven and probable reserves, ranking it second globally behind Russia's Norilsk operation according to Wood Mackenzie data. Furthermore, with fewer than six advanced Western nickel projects having achieved meaningful development progress, the pool of credible non-Indonesian alternatives is critically small.

As Canada Nickel's management has noted, when institutional capital that has been absent from nickel for three to four years returns in volume, there is a large amount of money chasing a very small number of credible stories. The competitive landscape for that capital is asymmetric in Crawford's favour.

The Dilution Problem That Has Defined Junior Mining

The conventional junior mining development model operates through a repeating cycle of equity issuance. A developer raises capital through successive placements at progressively larger amounts as the project advances through permitting, feasibility, and toward construction. By the time a construction decision is reached, it is common for aggregate equity dilution to have reached 50% to 100% of the share count that existed at earlier development stages.

This model is not simply suboptimal from a shareholder value perspective; it creates a structural incentive to move quickly at the expense of financing discipline. Developers under cash pressure accept whatever terms the equity market offers, and the market, recognising this leverage, prices the capital accordingly.

How Crawford Breaks the Conventional Mould

Canada Nickel has explicitly rejected this model as a governing constraint on the Canada Nickel Crawford financing strategy. Management has made clear that the company intends to take the time necessary to assemble a financing package that minimises equity issuance, even if that extends the development timeline relative to a conventional approach. The stated target is approximately 2% or less in new equity issuance, a figure that would be genuinely exceptional for a project requiring approximately C$2.0 billion in initial capital expenditure.

Deconstructing the Four-Pillar Financing Architecture

The Canada Nickel Crawford financing strategy rests on four interconnected components, each designed to reduce reliance on the next by contributing non-dilutive or low-dilution capital.

Project Debt Through Export Development Canada

Export Development Canada serves as the central arranger of the project debt layer. EDC's mandate encompasses support for Canadian companies engaged in export-oriented or strategically significant domestic projects, making it structurally suited to critical minerals demand contexts with national supply chain implications. Canada Nickel has re-entered negotiations with EDC for the next phase of debt structuring following the satisfactory completion of an independent engineer review, a critical gating requirement that lenders typically impose before progressing to binding commitment discussions.

Government-backed project debt from an institution like EDC differs from conventional commercial project finance in cost of capital, covenant flexibility, and the institutional signalling effect it creates for other capital providers. EDC's involvement effectively validates the project's technical and economic credentials in a language that other institutional lenders and government funders understand.

The Refundable Tax Credit Bridge Facility

The most structurally innovative element of the financing stack is the refundable tax credit bridge facility, which management has characterised as potentially covering approximately 60% of the required equity capital component. Understanding why this matters requires understanding what "refundable" means in this context.

How a Refundable Tax Credit Bridge Works:

- A refundable tax credit is payable by government regardless of whether the project is profitable, unlike non-refundable credits that only offset tax payable

- This characteristic transforms the credit from a contingent benefit into a near-certain government-backed receivable

- A bridge facility allows a developer to borrow against these future receivables before they are formally received

- Because lenders treat government-backed refundable credits as highly predictable cash flows, they can be financed at rates far below what open-market equity would cost

- Consequently, this replaces a substantial equity raise with structured debt against a government-backed asset

Management has targeted the bridge facility announcement for September or October 2026, positioning it as the third major financing milestone following federal permit issuance and the first government funding tranche.

Government and Strategic Partner Capital

The third pillar encompasses government funding programmes and strategic partner contributions. Crawford has been designated under Natural Resources Canada's Major Projects Office and included within Ontario's One Project, One Process framework, which coordinates provincial review processes. These designations improve funding eligibility and reduce the administrative friction associated with government programme applications, though they do not constitute confirmed government funding commitments.

Strategic shareholders already embedded in the capital structure include Agnico Eagle, Samsung SDI, Anglo American, and the Taykwa Tagamou Nation. The Indigenous partnership dimension is particularly notable because it introduces a category of capital that carries both financial and social licence value, directly supporting the regulatory credibility required for government funding applications.

Targeted Flow-Through Equity

The fourth pillar is deliberately narrow: targeted flow-through share issuances directed at district-level exploration rather than construction capital. The C$4.97 million placement announced on May 21, 2026, comprising up to 2,400,000 flow-through shares at C$2.07 per share and closing on or around June 10, 2026, exemplifies this approach. Proceeds fund eligible exploration expenses across the Timmins Nickel District, with qualifying expenditures renounced to purchasers with an effective date no later than December 31, 2026.

The separation of district exploration capital from construction capital is strategically deliberate. Flow-through structures provide tax advantages that allow the company to raise exploration capital at an effective cost below standard equity, while keeping the non-dilutive construction financing model structurally intact.

Crawford's Economics: The Numbers That Make Non-Dilutive Financing Achievable

The feasibility of a non-dilutive financing approach depends fundamentally on the underlying project economics being strong enough to satisfy the stringent requirements of government lenders and institutional debt providers. Crawford's completed FEED study, delivered in 2025, provides lender-grade technical validation across every dimension that matters.

| Metric | Value |

|---|---|

| NPV8% (base case) | C$2.8 billion |

| NPV8% (including CCUS credits) | ~C$2.9 billion |

| Internal Rate of Return (base) | 17.6% |

| IRR (including CCUS credits) | ~18.9% |

| Initial Capital Expenditure | ~C$2.0 billion |

| Life-of-mine net C1 cash cost | US$0.39/lb |

| Global cost curve position | First quartile (Wood Mackenzie) |

| Contained nickel in reserves | 3.8 million tonnes |

The cost positioning is particularly significant for debt serviceability analysis. At US$0.39 per pound on a net C1 basis, Crawford occupies the first quartile of all global nickel producers on the Wood Mackenzie cost curve. This means the project remains economically viable across a wide range of nickel price scenarios, providing debt providers with substantial margin of safety in their downside stress testing.

The CCUS credit component also deserves specific attention. Crawford's ultramafic host rock has particularly high carbon sequestration potential through natural mineral carbonation processes, allowing the project to generate carbon capture, utilisation, and storage credits that improve project economics beyond what conventional nickel projects can access. This is a genuinely distinctive geological characteristic, and it adds an additional layer of economic resilience while simultaneously aligning with government environmental objectives.

Management has stated unambiguously that from a technical standpoint, Crawford is construction-ready. The capacity to order long-lead items exists today; the constraint is capital sequencing rather than engineering readiness. This distinction matters for financing negotiations because it shifts negotiating leverage toward the developer.

Federal Permitting: The Structural Trigger for the Entire Financing Stack

Crawford is currently one step away from receiving its federal permit under Canada's 2019 Impact Assessment Act. The Impact Assessment Agency of Canada has published draft permit conditions following the completion of its impact assessment report. A 30-day public consultation period on those conditions precedes their finalisation, after which a recommendation is referred to the responsible minister, with permit issuance targeted for early summer 2026.

The significance of this milestone extends well beyond regulatory compliance. Crawford would become the first mining project in Canada to receive a permit under the 2019 legislation, completing a process that has taken approximately four years and involved the submission of more than 20,000 pages of documentation.

The permit is not merely a checkbox in the development sequence. For government funding programmes, EDC debt facilities, and institutional lenders, federal environmental approval is typically a prerequisite before capital commitment discussions can proceed to binding stages. The permit issuance is therefore the structural key that activates the entire non-dilutive financing stack.

The regulatory environment itself has evolved materially during Crawford's permitting timeline. Federal regulators have moved toward a more collaborative working posture, focused on reaching rigorous outcomes efficiently. This does not represent a lowering of standards; it reflects a growing recognition within regulatory institutions that the process of achieving rigorous outcomes can be streamlined without compromising their quality.

The next major ASX story will hit our subscribers first

Three Milestones That Will Define the 2026 to 2027 Construction Timeline

| Milestone | Target Timing | Strategic Significance |

|---|---|---|

| Federal permit issuance | Early summer 2026 | Activates government funding eligibility and EDC debt negotiations |

| First government funding tranche | Before end of Q2 2026 | Unlocks subsequent tranches; validates non-dilutive thesis |

| Tax credit bridge facility announcement | September to October 2026 | Covers ~60% of equity capital component |

| Final construction decision | Mid-2027 | Commits capital; initiates long-lead procurement |

Scenario Analysis: What Happens If Milestones Slip?

Responsible analysis requires examining not just the base case but the range of plausible outcomes.

Scenario A: On-Schedule Execution

- Federal permit received early summer 2026

- Government funding tranche confirmed Q2 2026

- Bridge facility announced Q3/Q4 2026

- Construction decision mid-2027

- Outcome: Crawford enters construction with minimal equity dilution, full financing stack intact, long-lead items ordered on schedule

Scenario B: Permit Delay of Three to Six Months

- Downstream financing milestones shift accordingly

- Bridge facility announcement pushed toward Q1 2027

- Construction decision delayed to late 2027 or early 2028

- Outcome: Dilution risk increases marginally as corporate costs require bridging through additional small placements; project economics remain fully intact

Scenario C: Government Funding Tranche Delayed Beyond Q2 2026

- Subsequent tranches delayed, creating sequencing uncertainty in the financing stack

- Mitigation: Samsung SDI offtake relationship and strategic shareholder base provide alternative capital pathways; EDC negotiations continue independently

- Outcome: Timeline pressure increases but structural non-dilutive model remains viable if permitting is confirmed

How Crawford's Model Compares to the Conventional Junior Developer Playbook

| Dimension | Traditional Junior Model | Crawford Non-Dilutive Model |

|---|---|---|

| Primary capital source | Open-market equity raises | Government funding + debt + tax credit bridge |

| Typical dilution at construction | 50 to 100% of pre-construction shares | Target: ~2% or less |

| Financing timeline | Faster but value-destructive | Longer but value-preserving |

| Lender/government requirements | Minimal | Requires FEED, independent engineer review, permitting |

| Strategic partner involvement | Limited | Agnico Eagle, Samsung SDI, Anglo American, TTN |

| Risk profile for shareholders | High dilution, lower per-share value | Lower dilution, higher per-share value retention |

| Cost curve positioning required | Not applicable | First quartile essential for debt serviceability |

The non-dilutive model is not universally replicable. It demands a specific combination of characteristics that most junior developers simply do not possess. In addition, the broader battery metals investment landscape must be receptive to the project's strategic positioning for the financing stack to function effectively. Crawford satisfies all the necessary criteria. Most junior developers satisfy none of them.

Samsung SDI, Offtake Dynamics, and the Battery Sector's Urgency

One dimension of the Canada Nickel Crawford financing strategy that carries significant forward-looking importance is the Samsung SDI relationship. As one of the world's leading battery manufacturers, Samsung SDI has maintained a strategic interest in securing non-Indonesian nickel offtake, with Crawford identified as one of the few projects capable of delivering meaningful production before 2030.

Offtake-linked financing structures represent a potential pathway that bridges the gap between a battery manufacturer's procurement needs and a developer's capital requirements. When an offtaker commits to purchasing production at defined price terms over a multi-year period, that commitment can serve as the revenue certainty underpinning project debt. The stronger and more creditworthy the offtaker, the more favourably lenders treat that revenue stream in their debt sizing calculations.

Samsung SDI's position as a globally significant battery manufacturer means that a formalised offtake agreement carries substantial financing weight. The company's continued engagement with Crawford, against a backdrop of Indonesia's tightening supply policies, reflects a procurement urgency that aligns directly with Canada Nickel's financing timeline objectives. Furthermore, the broader prospects for nickel market recovery add additional momentum to this dynamic.

Frequently Asked Questions

What is Canada Nickel's target dilution level for the Crawford financing?

Management has established a target of approximately 2% or less in new equity issuance, a figure that stands in sharp contrast to the 50 to 100% dilution events that have historically characterised large junior mining project financings at the construction stage.

What is the refundable tax credit bridge facility and why is it central to the strategy?

The bridge facility allows Canada Nickel to borrow against future government tax credit receivables before those credits are formally received. Because the credits are refundable regardless of project profitability, lenders treat them as near-certain government-backed cash flows. Management has indicated this mechanism could cover approximately 60% of the equity capital component required for Crawford's construction.

What role does Export Development Canada play in the Crawford financing?

EDC is the central arranger of the project debt layer. Canada Nickel re-entered negotiations with EDC following the satisfactory completion of an independent engineer review, a prerequisite for binding debt commitment discussions. EDC's involvement brings government-backed lending terms and signals institutional confidence in the project's viability to other capital providers.

Why is the federal permit the critical gating event for the financing timeline?

Government funding programmes, EDC debt facilities, and institutional lenders typically require federal environmental approval before committing capital. The permit, expected in early summer 2026, is the structural trigger that activates the non-dilutive financing stack across all four pillars.

What happens to the financing strategy if nickel prices fall from current levels?

Crawford's life-of-mine net C1 cash cost of US$0.39 per pound places it in the first quartile of global nickel producers on the Wood Mackenzie cost curve. This positioning provides significant downside protection and maintains debt service viability across a wide range of price scenarios, including those well below current LME spot levels.

Who are Canada Nickel's strategic shareholders and how do they support the financing?

Strategic shareholders include Agnico Eagle, Samsung SDI, Anglo American, and the Taykwa Tagamou Nation. These relationships provide potential pathways for offtake-linked financing, Indigenous partnership capital, and the institutional credibility that supports government funding applications and EDC debt negotiations.

What is Crawford's CCUS credit advantage and why is it geologically unusual?

Crawford's ultramafic host rock has exceptionally high carbon sequestration potential through natural mineral carbonation. This geological characteristic allows the project to generate carbon capture credits that improve base-case economics by approximately C$100 million in NPV terms, a benefit not available to most conventional nickel sulphide or laterite deposits and one that directly supports government environmental funding objectives.

Disclaimer: This article contains forward-looking statements and scenario analysis involving forecasts, timelines, and financial projections that are subject to material risks and uncertainties. Financing milestones, permit timelines, and project economics may differ materially from those described. This article does not constitute financial advice. Readers should conduct their own due diligence before making investment decisions.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into actionable investment insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.