June 26, 2026

Why the Global Nickel Supply Gap Is Forcing a Financing Revolution

The mining industry has long operated on a simple but painful financing logic: build the asset, issue the equity, dilute the shareholders. For critical minerals projects requiring billions in capital, that formula has historically transferred enormous value away from early investors at precisely the moment when construction risk is highest. The emergence of government-backed tax incentive frameworks, however, is beginning to disrupt that model in ways most retail investors have not yet fully appreciated.

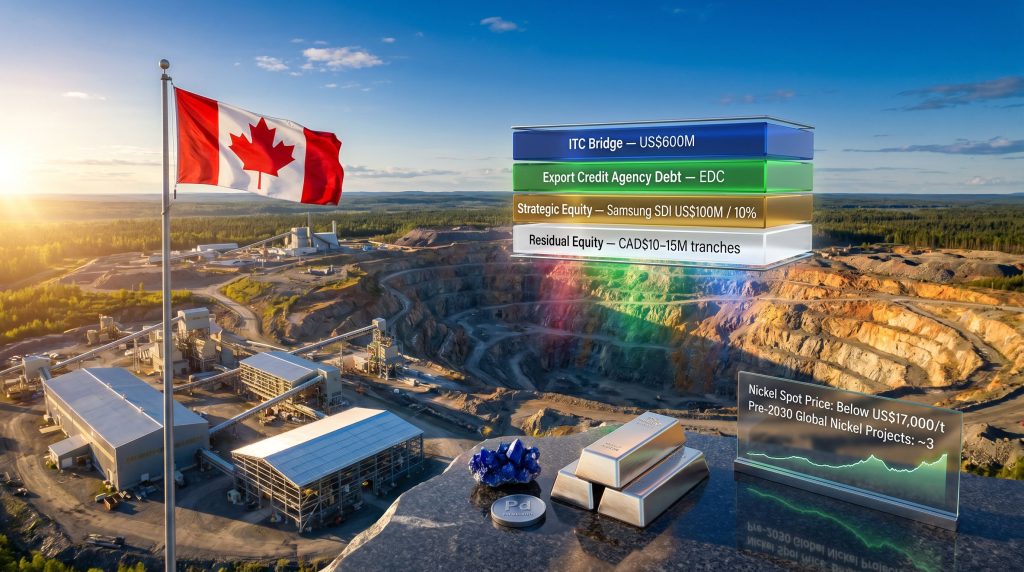

Canada's critical minerals investment tax credit architecture represents one of the most significant shifts in project finance mechanics seen in the sector in a generation. When designed around refundable credits, these instruments do something conventional grants cannot: they create a quantifiable, timing-specific receivable that can be assigned a present value, pledged as collateral, and converted into debt. That transformation, from a future government payment into a current financing instrument, is the central innovation underpinning Canada Nickel Crawford tax credit financing for the Crawford Nickel Project.

When big ASX news breaks, our subscribers know first

The Refundability Distinction Most Investors Miss

Not all tax credits are created equal, and the difference between refundable and non-refundable credits is one of the most consequential distinctions in project finance that rarely receives adequate attention in mainstream coverage.

A non-refundable credit can only offset tax otherwise payable. For a pre-production mining project generating no taxable income, a non-refundable credit has near-zero practical utility during construction. A refundable credit, by contrast, is payable by the government regardless of tax liability, which means it functions as a genuine receivable, a future cash inflow with a defined legal basis, against which debt can theoretically be structured.

Canada's critical minerals ITC framework applies refundable credits to eligible construction expenditures in the critical minerals sector. That design choice transforms the policy from a future tax benefit into a construction-stage financing instrument, provided a lender is willing to bridge the timing gap between expenditure and government reimbursement. That is precisely what the Canada Nickel Crawford tax credit financing facility, targeted at up to US$600 million and being arranged by SB1 Markets AS, is designed to accomplish.

The fundamental innovation here is not the credit itself. It is the ability to monetise that credit before it is received, effectively making government policy a real-time construction funding tool rather than a post-completion reward.

Ontario's Critical Minerals Processing Fund adds a provincial dimension to the federal ITC framework, creating a layered incentive environment that further strengthens the economics of projects like Crawford situated within Ontario's mining corridor near Timmins. Furthermore, the growing critical minerals demand across the energy transition is adding urgency to the development of projects with this kind of robust financing architecture.

Crawford's Position Within a Depleted Global Nickel Pipeline

To understand why lenders and offtake partners are willing to engage seriously with Crawford's capital structure at this stage, it is necessary to appreciate just how narrow the pipeline of credible pre-2030 nickel projects has become globally.

Nickel demand, particularly from the battery supply chain, is structurally long-term bullish even as spot prices have faced pressure in the near term. As of mid-2025, nickel traded below US$17,000 per tonne, a level that has rendered many marginal projects uneconomical and deferred investment decisions across the sector. The paradox this creates is significant: the very price weakness discouraging new supply development is simultaneously strengthening the medium-term supply-demand case for the few projects that can survive at lower prices and still reach production before 2030.

Management at Canada Nickel estimates that Crawford is among approximately three nickel projects globally positioned to reach production before 2030. That is an extraordinarily narrow field, and it concentrates the attention of battery manufacturers, offtake counterparties, and export credit agencies on a very short list of viable assets.

| Metric | Detail |

|---|---|

| Crawford project location | Timmins, Ontario, Canada |

| Estimated pre-2030 global nickel projects | Approximately 3 |

| Nickel spot price context (mid-2025) | Below US$17,000/t |

| Samsung SDI equity commitment | US$100 million for approximately 10% |

| ITC bridge facility target | Up to US$600 million |

| SB1 Markets transaction volume (prior 12 months) | Approximately US$70 billion |

Crawford itself is a large-tonnage, low-grade sulphide deposit with meaningful nickel, cobalt, and palladium byproduct credits. The sulphide classification is important. Unlike laterite nickel deposits, which dominate Indonesia's production base and require high-pressure acid leach processing, sulphide deposits can be processed via conventional flotation and smelting routes to produce Class 1 nickel, the battery-grade material that EV supply chains specifically require.

That geological distinction makes Crawford directly relevant to Western battery manufacturers seeking to build supply chains outside of Chinese-controlled Indonesian nickel supply. In addition, the diverging processing economics between sulphide and laterite deposits continue to widen Crawford's competitive advantage at current nickel price levels.

How the ITC Bridge Facility Actually Works

The structural logic of the Canada Nickel Crawford tax credit financing can be broken down into a clear sequence:

- Federal permit issued – construction authorisation confirmed under Canada's 2019 Impact Assessment Act.

- Eligible construction expenditures incurred – capital is deployed during the build phase.

- Investment tax credits accrue – refundable credits attach to those expenditures under the critical minerals ITC framework.

- Lender advances debt – SB1 Markets AS, acting as arranger, sources institutional lenders willing to advance funds against the present value of the anticipated credit stream.

- Government reimburses credits post-completion – the refundable payment flows to Canada Nickel.

- Debt is repaid from the government receipt – the lender recovers principal from the credit reimbursement, not from project operating cash flow.

This structure is mechanically elegant for one specific reason: the repayment source is a government receivable, not a commodity-price-dependent cash flow. That meaningfully changes the risk profile for lenders compared to conventional project finance debt, where repayment depends entirely on the project generating sufficient operating revenue.

The critical prerequisite is confirmed construction authorisation. Without the federal permit, eligible construction cannot commence, credits cannot accrue, and the facility cannot be formally sized. That dependency is why the pending federal permit issuance, targeting early summer 2026, is the most consequential near-term catalyst in Crawford's entire development timeline.

Why This Structure Protects Existing Shareholders

In a conventional greenfield financing model, the developer raises a large equity contribution through share issuances. For a project of Crawford's scale, that could mean hundreds of millions of dollars in dilutive equity raises, compressing the ownership percentage of shareholders who backed the project in its earlier stages.

The ITC bridge replaces equity as the primary funding vehicle for more than half of Canada Nickel's equity contribution to Crawford. The residual equity component shrinks to manageable tranches of approximately CAD$10 to $15 million, used to bridge gaps between incoming financing tranches rather than fund the bulk of the project. That is a structurally different dilution profile, and it is one of the more underappreciated aspects of the Canada Nickel Crawford tax credit financing structure for long-term shareholders. Consequently, this approach also aligns well with the broader battery metals investment landscape, where minimising dilution is increasingly a differentiating factor for institutional capital.

SB1 Markets AS and What the Mandate Signals

The appointment of SB1 Markets AS as exclusive arranger carries meaningful signal value beyond the mechanics of the facility itself. SB1 Markets AS is a Nordic investment bank with approximately US$70 billion in transactions arranged in the preceding 12-month period, with demonstrated expertise in natural resource project finance and established relationships within export credit agency networks.

That last point is particularly relevant. Crawford's broader capital stack includes Export Development Canada debt and expressions of interest from two additional export finance groups. SB1 Markets operates in precisely the institutional ecosystem where those counterparties are active, which means the arranger appointment is not incidental to the broader financing architecture but directly complementary to it.

It is important to distinguish between a mandate and a binding commitment. An exclusive mandate authorises SB1 Markets to arrange the facility and compresses the timeline between permitting and financing close. It does not constitute a signed facility agreement, nor does it guarantee that lenders will be identified and terms finalised by year-end 2026. Investors should treat this as a material advancement, not a completed transaction.

The deliberate sequencing of the mandate, awarded in anticipation of the federal permit rather than after its receipt, reflects management's assessment that the published draft permit conditions represent the substantive conclusion of the permitting process. That sequencing choice shortens the window between permit receipt and financing close, compressing what is otherwise a lengthy institutional engagement process.

Crawford's Full Capital Stack Architecture

The ITC bridge does not exist in isolation. It is one layer within a multi-instrument capital structure specifically designed to minimise the equity contribution and therefore minimise dilution.

| Financing Layer | Provider | Function |

|---|---|---|

| ITC Bridge Facility | SB1 Markets AS (arranging) | Funds majority of equity contribution |

| Senior Project Debt | Export Development Canada + 2 export finance groups | Primary debt financing for construction |

| Government Contributions | Federal and provincial programs | Targeted capital contributions alongside debt |

| Strategic Equity | Samsung SDI (US$100M / ~10% stake) | Anchor equity and offtake alignment |

| Residual Equity | Public markets | Approximately CAD$10-15M tranches as required |

The re-engagement with EDC following a successful independent engineer review is a notably positive signal for the project's bankability. Independent engineering reviews serve as a foundational due diligence step for export credit agency participation. A successful outcome means the project's technical assumptions have withstood institutional-grade scrutiny, opening the pathway for formal credit discussions that might otherwise remain hypothetical.

The fact that two additional export finance groups have expressed independent interest in participating alongside EDC suggests that institutional appetite for Crawford's risk profile, at this stage of development, is broader than a single bilateral relationship.

The next major ASX story will hit our subscribers first

The Permitting Timeline and Its Cascading Dependencies

Crawford holds a historically significant position in Canadian mining regulation. It is the first mining project advancing through the permitting process under Canada's 2019 Impact Assessment Act, which replaced the previous Canadian Environmental Assessment Act with a more comprehensive framework. Navigating this process successfully would set procedural precedents for future mining projects operating under the same legislation.

The current status involves the Impact Assessment Agency of Canada having issued its impact assessment report along with draft permit conditions. A 30-day public consultation period is underway, after which conditions are finalised and the permit issued. The company is targeting permit receipt in early summer 2026.

The sequencing dependencies cascade from that single event:

- Permit issuance confirms construction authorisation and establishes ITC entitlement basis.

- ITC entitlement confirmed allows the bridge facility to be formally sized.

- First government contribution tranche validates the non-dilutive architecture.

- Facility arrangement completed by year-end 2026 positions the project for FID.

- Final Investment Decision targeting 2027 is the culmination of the entire sequence.

Any material modification to permit conditions during the consultation period introduces residual uncertainty, both for project economics and for lender appetite in a structure where credit quality is partially a function of construction cost assumptions.

Key Risks Every Investor Should Evaluate

Serious engagement with Crawford's financing story requires honest acknowledgment of the risks that sit alongside the opportunity.

Financing execution risk is primary. The exclusive mandate is a meaningful milestone but represents the beginning of institutional engagement rather than its conclusion. Lender identification, credit assessment, and term finalisation remain ahead. The critical minerals ITC framework itself is subject to legislative change, and any policy modification could alter the credit stream against which the facility would be sized.

Permitting risk remains live until the consultation period concludes and final conditions are published. Draft conditions published does not mean final conditions confirmed.

Commodity price risk is a persistent backdrop. Nickel spot prices below US$17,000 per tonne at the time of writing create a challenging environment for project economics, even if the medium-term fundamental case for Class 1 nickel remains constructive. However, the nickel market recovery thesis continues to attract institutional attention, particularly given the EV demand trajectory and the structural shortage of sulphide-based nickel supply outside of existing operations. Furthermore, monitoring Indonesian nickel price trends provides important context for understanding how Crawford's sulphide-based economics compare against the dominant laterite supply base.

Disclaimer: This article contains forward-looking analysis based on publicly available information. It does not constitute financial advice. Readers should conduct their own due diligence and consult a qualified financial adviser before making investment decisions. Past performance and project milestones do not guarantee future outcomes.

Why Crawford's Model Could Reshape Canadian Critical Minerals Finance

If the Canada Nickel Crawford tax credit financing is successfully arranged and executed at scale, it would represent a structural template that other Canadian critical minerals developers will almost certainly study and attempt to replicate. The core innovation, using a government policy instrument as a real-time construction financing lever rather than a post-completion reward, is applicable to any project with sufficient eligible construction expenditures under the critical minerals ITC framework.

Comparisons to the US Inflation Reduction Act's advanced manufacturing credits are instructive. American developers have similarly begun structuring debt against IRA tax credit streams, a practice now commonly described as tax credit monetisation in the US project finance community. Canada's refundable ITC framework offers a structurally analogous mechanism, and Crawford's execution, if successful, would validate the approach within the Canadian jurisdictional context.

The broader implication for the critical minerals financing landscape is substantial. Export credit agency participation, strategic equity from end-users, and targeted government contribution programs are already standard components of institutional-grade critical minerals capital stacks. The ITC bridge adds a fourth instrument that could become a defining feature of Canadian project finance in the sector, fundamentally changing the dilution calculus for early-stage shareholders in projects with sufficient scale to access it.

For investors tracking the Crawford story, the milestone sequence through 2026 and into 2027 is now clearly defined. The federal permit is the trigger. Everything downstream, from bridge facility sizing through to FID, depends on that single regulatory outcome landing on the timeline management has guided toward.

For further analysis of Canada Nickel's Crawford project development and financing milestones, institutional-grade coverage is available through Crux Investor at cruxinvestor.com.

Want to Track the Next Major Mineral Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable investment insights — explore historic examples of exceptional discovery returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.