July 10, 2026

Why the World's Next Great Copper District May Already Be Permitted

The global mining industry is entering one of its most consequential decades in generations. As electrification accelerates across transport, energy storage, and grid infrastructure, the supply pipeline for copper, cobalt, and high-grade iron ore has failed to keep pace with demand projections. Most analysts tracking the copper supply crunch now point to a structural deficit emerging between 2025 and 2035, driven not by a lack of known deposits but by a chronic shortage of fully permitted, investment-ready projects capable of reaching production within the decade.

This is precisely the context in which the Capstone Santo Domingo project in Chile deserves serious attention. Not because of a single announcement or milestone, but because of what it represents at a systems level: a rare convergence of geological diversity, completed environmental permitting, anchored institutional co-investment, and a district-scale integration strategy that few greenfield copper projects anywhere in the world can match at this stage of development.

When big ASX news breaks, our subscribers know first

Understanding the Geological Foundation: IOCG Deposits and Why They Matter

Most copper projects discussed in financial media are porphyry-type deposits, where copper is disseminated through large volumes of intrusive rock at relatively low grades. The Capstone Santo Domingo project in Chile belongs to an entirely different geological category: the iron oxide-copper-gold (IOCG) deposit class, hosted within Chile's Cretaceous Iron Belt along the Atacama fault zone. Our IOCG deposits guide provides further context on what makes this classification commercially significant.

IOCG deposits are geologically distinctive for several reasons that carry direct economic consequences:

- They tend to produce multiple revenue-generating commodities simultaneously, rather than a primary metal with minor by-products

- Magnetite iron ore in IOCG systems is often of high purity, making it attractive to steelmakers pursuing direct reduced iron (DRI) processes for lower-emissions steel production

- Cobalt mineralisation frequently occurs alongside copper and iron in IOCG systems, creating a multi-critical-mineral output profile from a single orebody

- The structural controls that form IOCG deposits in fault zones can create significant lateral and depth extensions, supporting long mine lives

Santo Domingo sits at an elevation of 1,000 to 1,280 metres above sea level, approximately 130 km north-northeast of Copiapó in Chile's Atacama Region (Region III). Its position 35 km northeast of Capstone's operating Mantoverde mine is not incidental: both assets share the same Cretaceous Iron Belt geology, which is the fundamental underpinning of the district integration thesis.

The IOCG classification separates Santo Domingo from conventional single-metal copper porphyry projects. Its multi-commodity architecture means production revenue is diversified across copper, magnetite iron ore, cobalt, and gold simultaneously, reducing unit cost sensitivity to fluctuations in any single commodity price.

Production Architecture: What the Numbers Actually Mean

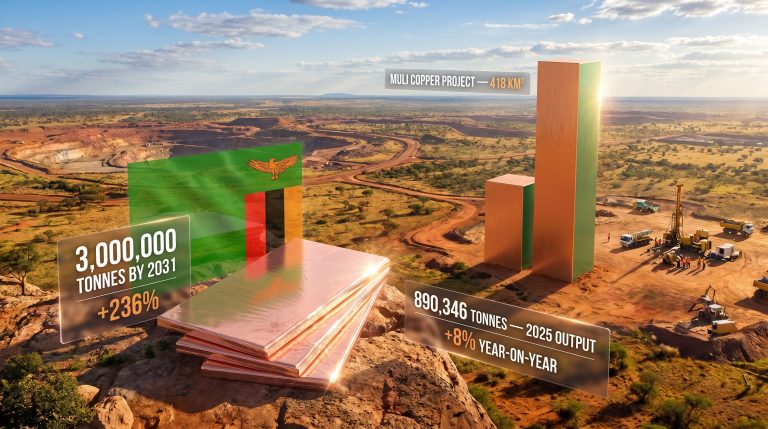

The Capstone Santo Domingo project in Chile is designed around a copper-iron concentrator plant rated at 72,000 tonnes per day, one of the larger throughput rates among greenfield copper developments currently approaching a construction decision in Latin America. Understanding what this throughput translates into at the commodity level requires looking at the full output matrix.

| Commodity | Projected Annual Output | Production Context |

|---|---|---|

| Copper | ~106,000 tonnes | First 7 years of operation |

| Magnetite iron ore | 5.4 million tonnes | Port throughput capacity |

| Cobalt (district-wide) | 4,500 to 6,000 tonnes | Across integrated Mantoverde-Santo Domingo district |

| Gold | By-product | Supplementary revenue contribution |

Several figures in this table warrant closer examination than they typically receive in coverage of this project.

The cobalt production range of 4,500 to 6,000 tonnes per annum across the district is particularly strategically significant. For context, global cobalt production has historically hovered between 150,000 and 200,000 tonnes annually, with a dominant share originating from the Democratic Republic of Congo. A single integrated district in Chile producing up to 6,000 tonnes of cobalt per year would represent a meaningful diversification of supply for battery manufacturers and Western governments seeking alternatives to DRC-sourced cobalt. Capstone's own assessment indicates this volume would rank the district among the world's largest cobalt producers.

The mine life of more than 19 years is equally important from an investor perspective. Long mine lives provide the cash flow duration required to justify large-scale infrastructure investment and attract project finance from institutional lenders who typically require 15-plus year asset lifetimes to underwrite debt facilities of this magnitude.

The Ownership and Financing Structure: De-Risking Through Strategic Partnership

The financial architecture of the Capstone Santo Domingo project reflects a carefully structured approach to sharing capital risk without surrendering operational control.

| Stakeholder | Ownership Interest | Key Financial Terms |

|---|---|---|

| Capstone Copper | 75% | Majority operator and decision-maker |

| Orion Resource Partners | 25% | Up to US$360 million consideration |

The Orion Resource Partners transaction, agreed in October 2025, is structured so that US$225 million of the total consideration becomes payable upon a positive final investment decision (FID). This is not a trivial structural detail. It means that the moment Capstone declares a positive FID, a substantial capital injection is triggered automatically, providing immediate balance sheet reinforcement precisely when construction spending begins to ramp.

Orion Resource Partners is a specialist critical minerals investment firm with deep expertise across battery metals and copper. Its decision to acquire a 25% stake validates the project's technical and commercial credentials from a financially sophisticated counterparty perspective, which carries weight beyond the headline capital figure.

The total initial capex estimate of US$2.3 billion places Santo Domingo among the largest greenfield copper construction commitments under active advancement in Latin America. For comparison, the adjacent Mantoverde mine required approximately US$870 million in capital investment and now produces between 89,000 and 102,000 tonnes of copper annually since commencing operations in 2024. Mantoverde's delivery track record provides a meaningful operational credibility reference for Santo Domingo's development approach.

The project already holds full environmental approval, which eliminates what is consistently the most unpredictable timeline risk in Chilean mining development. Environmental permitting processes in Chile can extend over multiple years and have historically derailed or significantly delayed major projects. Santo Domingo's fully approved status means the primary pathway-blocking risk has already been resolved.

What the First Blast Actually Signals: Reading Pre-FID Technical Milestones

In mid-2026, Capstone conducted the first blasting activity at the Santo Domingo site. This event has been widely noted, but its specific technical purpose is frequently mischaracterised in market commentary.

The blast was not a construction commencement event. Its purpose was narrow and technically specific: to obtain ballast material for testing the physical properties required for the thickened tailings deposit infrastructure. Tailings management is one of the most technically demanding and environmentally sensitive components of any large copper concentrator operation, and characterising the material behaviour of thickened tailings deposits requires actual rock samples from the site.

Thickened tailings technology, which increases the solids content of tailings slurry before deposition, is increasingly preferred over conventional tailings storage facilities because it reduces water consumption, lowers the risk of liquefaction failures, and decreases the physical footprint of the tailings impoundment. For an Atacama Region operation where water scarcity is a fundamental constraint, the tailings management design choice has direct cost and environmental implications.

What the blasting event does signal is that Capstone is actively advancing technical de-risking activities across multiple workstreams simultaneously ahead of its targeted Q4 2026 FID. Offshore port construction studies at Punta Roca Blanca are underway. Tailings materials characterisation is progressing. The Orion partnership is in place. Each of these parallel workstreams reduces the technical uncertainty that a lender or equity investor would need to price into the project at the point of FID. Furthermore, a completed definitive feasibility study underpins the technical rigour behind these advancement milestones.

The District Integration Model: Three Assets, One Economic System

The most analytically underappreciated dimension of the Capstone Santo Domingo project in Chile is what it enables at the district level, rather than what it achieves as a standalone operation.

The Mantoverde-Santo Domingo district strategy integrates three separate assets under shared infrastructure:

- Santo Domingo (Capstone 75%, Orion Resource Partners 25%) – the anchor greenfield development targeting first production around 2028

- Mantoverde (Capstone 70%, Mitsubishi Materials 30%) – the operating mine 35 km away, producing since 2024 at 89,000 to 102,000 tonnes of copper per year

- Sierra Norte (formerly Diego de Almagro, 100% Capstone) – an advanced exploration asset with potential to route ore through Santo Domingo's concentrator, extending reserve life without duplicating processing infrastructure

The combined district production target upon full integration exceeds 250,000 tonnes of copper per year, supplemented by the cobalt and magnetite iron ore streams described above. Achieving this through three co-located assets sharing infrastructure represents a fundamentally different economic model than building three independent mines.

The infrastructure sharing thesis rests on a principle well-established in mining economics: co-located operations sharing port access, desalination capacity, and power transmission infrastructure achieve materially lower unit operating costs than standalone developments of equivalent scale. Industry analysis consistently supports this conclusion, and Ausenco Chile's vice president of minerals and metals, Marcelo Henríquez, has noted publicly that projects combining such synergies improve commercial outcomes for all participants while simultaneously reducing environmental footprint. This observation is directly applicable to the Santo Domingo district model.

Key Shared Infrastructure Components

Puerto Santo Domingo at Punta Roca Blanca

A purpose-built greenfield port is planned for Punta Roca Blanca to handle both 5.4 million tonnes per annum of magnetite iron ore and 0.72 million tonnes per annum of copper concentrate. Port construction is a long-lead infrastructure item, and offshore studies have already commenced, indicating the level of pre-FID advancement across the project's critical path components.

Desalination Plant

Water supply in the Atacama Region is not merely a logistical challenge; it is an existential operational constraint. All large-scale mining operations in the region require dedicated water supply solutions, and the Santo Domingo district's desalination facility will serve multiple assets, distributing both the capital cost and the environmental footprint of water extraction across the district rather than requiring each operation to develop independent solutions.

Power Transmission Infrastructure

Shared power corridors reduce per-unit energy infrastructure costs across district assets and, crucially, position the district to integrate renewable energy sources. Northern Chile has some of the highest solar irradiance levels recorded anywhere globally, and the buildout of renewable power capacity in the Atacama Region is progressing rapidly, creating a realistic pathway toward lower-carbon energy supply for operations of this type.

The next major ASX story will hit our subscribers first

Pipeline Projects Reinforcing the Long-Term Vision

Three development-stage initiatives form the strategic pipeline behind the primary Santo Domingo build:

- Santo Domingo Óxidos: targeting oxide copper mineralisation adjacent to the primary sulphide deposit, potentially extending the resource base

- Sierra Norte Integración: routing Sierra Norte ore through Santo Domingo's concentrator, extending reserve life without duplicating capital-intensive processing infrastructure

- Mantoverde Phase II: expanding throughput and extending mine life at the operating Mantoverde asset

Each of these pipeline projects is premised on infrastructure that Santo Domingo's construction would bring into existence. This creates a compounding optionality structure where the economic case for each successive project strengthens as shared infrastructure is built out, rather than each project standing or falling independently.

Critical Minerals Context: Copper, Cobalt, and the Steel Decarbonisation Angle

The Capstone Santo Domingo project in Chile sits at the intersection of three distinct demand narratives that are each accelerating independently.

Copper and electrification: Copper demand forecasts from major investment banks and commodity research firms consistently project significant volume growth through 2040, driven by electric vehicle manufacturing, transmission grid expansion for renewables, and industrial electrification. Santo Domingo's 106,000 tpa copper output during peak early production years represents a meaningful contribution to addressing the projected supply shortfall.

Cobalt and battery supply chain security: G7 nations and the European Union are actively working to reduce dependence on DRC-sourced cobalt, which accounts for the majority of global supply. A fully permitted, ESG-compliant Chilean cobalt source from a stable jurisdiction with established mining infrastructure represents a differentiated supply chain option that could attract strategic offtake interest from battery manufacturers and their automotive customers.

Magnetite iron ore and green steel: High-purity magnetite is increasingly sought by steelmakers developing hydrogen-based direct reduced iron processes as a lower-emissions pathway to steel production. In addition, the green steel trends emerging across global markets are reinforcing demand for exactly the type of high-purity magnetite that IOCG deposits like Santo Domingo naturally produce as a primary co-product, adding a steel decarbonisation dimension that is not available from conventional copper porphyry operations.

Risk Framework: What to Monitor Ahead of the Q4 2026 FID

| Risk Category | Current Status | Key Mitigation Factor |

|---|---|---|

| Permitting risk | Resolved | Full environmental approval secured |

| Technical risk | Partially mitigated | Tailings characterisation progressing via 2026 blasting program |

| Financing risk | Partially mitigated | Orion transaction reduces Capstone's equity exposure |

| Execution risk | Moderate | Mantoverde delivery track record provides credibility reference |

| Market risk | Ongoing | 19-plus year mine life provides commodity cycle averaging |

The Q4 2026 FID is the pivotal binary event for project advancement. A positive decision triggers the US$225 million Orion payment, initiates the concentrator plant build program, and formally commits the port and desalination infrastructure construction schedules. The Wheaton Precious Metals portfolio page also reflects the level of institutional interest tracking this project closely. Beyond the FID itself, the following milestones warrant close monitoring:

- Tailings materials characterisation results from the mid-2026 blasting program

- Offshore port construction study outcomes at Punta Roca Blanca

- Sierra Norte exploration results, which could expand the district resource base

- Cobalt offtake discussions, given growing institutional interest in non-DRC supply

- Copper price trajectory, which directly influences the economics underpinning FID confidence

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, timelines, and production estimates cited are based on company guidance and publicly available data and are subject to material change. Investors should conduct their own due diligence and consult qualified financial advisers before making investment decisions.

Want to Know When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including copper, cobalt, and iron ore — so subscribers can act ahead of the broader market. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial to secure a genuine market-leading edge.