July 9, 2026

The Quiet Metal Driving the Energy Transition's Biggest Supply Crisis

Every major infrastructure cycle in modern history has been defined by a single commodity bottleneck. In the current energy transition, that bottleneck is copper. While lithium and rare earth elements command headlines, copper underpins every component of the low-carbon economy at a scale those metals cannot match. A single electric vehicle contains roughly 83 kilograms of copper — nearly four times the amount found in a conventional internal combustion engine vehicle. Grid-scale battery storage, offshore wind turbines, and EV charging networks compound this demand exponentially. The structural gap between projected copper demand and currently confirmed supply pipelines is widening in ways that are only beginning to register with mainstream investors.

Against this backdrop, the Central African Copperbelt is undergoing a quiet reassessment. Zambia, in particular, is attracting a new wave of junior exploration capital drawn by the country's geological endowment, its stated production ambitions, and an evolving investment climate that is beginning to prioritise structured foreign partnerships. The Makor Zambia copper plan at African Mining Week, scheduled for Cape Town in October 2026, represents one of the more visible examples of how junior explorers are positioning themselves within this unfolding dynamic.

When big ASX news breaks, our subscribers know first

Zambia's Production Gap: Understanding the Scale of the Ambition

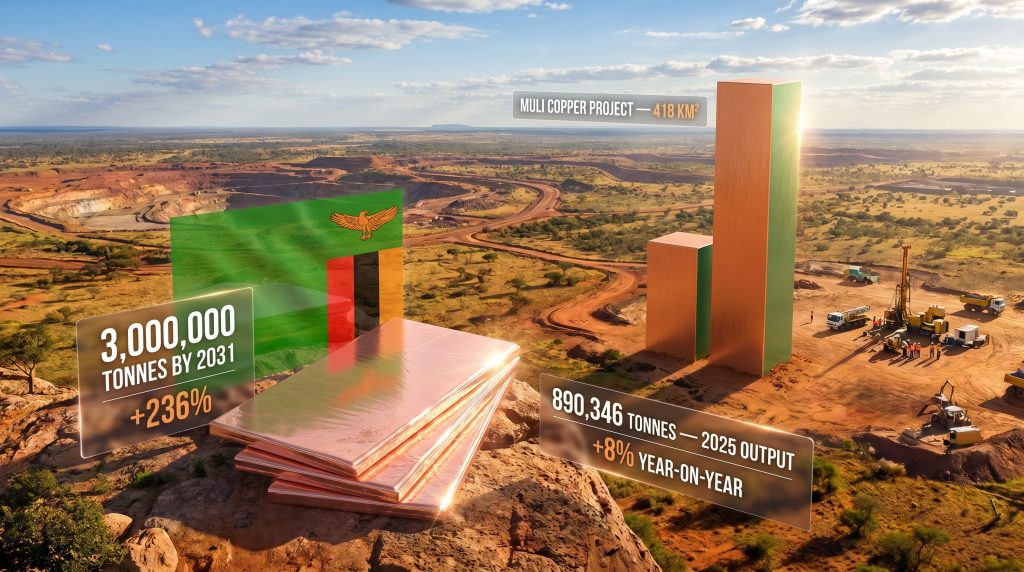

Zambia copper production growth reached 8% in 2025, with total output hitting approximately 890,346 tonnes. That growth rate would be considered impressive in most mining jurisdictions. However, the challenge is that it still fell short of the country's own production targets for the year, and the gap between current output and the government's stated goal of 3 million tonnes per annum by 2031 is measured in the millions of tonnes, not the thousands.

| Metric | Figure |

|---|---|

| 2025 Copper Output | ~890,346 tonnes |

| Year-on-Year Growth (2025) | +8% |

| 2031 Government Production Target | 3,000,000 tonnes |

| Required Increase from 2025 Levels | ~236% |

| Absolute Production Gap | ~2.11 million tonnes |

Achieving this target would require Zambia to roughly triple its current production within six years. For context, Chile, the world's largest copper producer, produces approximately 5.3 million tonnes annually and has done so after decades of sustained capital investment. Zambia's trajectory requires not just new mines but accelerated exploration, infrastructure buildout, labour development, and capital inflows across the entire mining value chain simultaneously.

This is precisely the environment in which well-structured junior explorers can establish meaningful positioning. The window between geological discovery and large-scale production typically spans seven to fifteen years, meaning exploration activity initiated today is directly relevant to whether Zambia hits its 2031 targets or falls further behind.

Why the Copperbelt Still Has Room to Surprise

A common misconception among non-specialist investors is that the Central African Copperbelt has been thoroughly explored and that major new discoveries are unlikely. The geological reality is considerably more nuanced. The Copperbelt is a sediment-hosted stratabound copper system that stretches across Zambia and the Democratic Republic of Congo, and large portions of it remain either minimally explored or assessed only with legacy geophysical methods that lacked the resolution of modern techniques.

Stratabound copper deposits in this geological setting are particularly significant because they tend to be large-tonnage, lower-grade systems amenable to bulk mining methods, rather than the high-grade but geometrically complex vein deposits more common in other copper provinces. This geological characteristic favours district-scale exploration strategies, where identifying the broader mineralised system is as valuable as locating a single ore body.

Furthermore, advances in airborne electromagnetic (AEM) surveying, induced polarisation (IP) geophysics, and deep-penetrating gravity methods have materially improved the probability of discovering new mineralisation beneath cover sequences that previously obscured prospective geology. Junior explorers employing these modern tools across large licence areas are not simply repeating historical exploration approaches with higher budgets; they are accessing geological information that was structurally unavailable to previous generations of explorers.

Makor Resources: District-Scale Thinking in a Single-Target World

Most junior mining companies operating in competitive jurisdictions default to a single-target exploration model for a straightforward reason: it is cheaper, faster, and easier to communicate to retail investors. The downside is that it concentrates all geological and capital risk on one outcome. If the target disappoints, the entire investment thesis collapses.

Makor Resources has pursued a structurally different approach. The Perth-based company has assembled a portfolio of exploration licences across multiple Zambian districts, prioritising large anomaly systems over isolated drill targets. Its flagship asset, the Muli Copper Project in the Mumbwa district, covers 418 square kilometres of greenfield tenure hosting geochemical and geophysical anomalies consistent with sediment-hosted copper mineralisation. The Kangili Copper Project in the Mkushi district represents a secondary target within the same strategic framework.

Additional licence holdings in the Ndola, Kitwe, and Kasempa areas extend Makor's footprint further into the Copperbelt corridor, creating a portfolio structure that can absorb individual exploration setbacks without fatally compromising the broader investment thesis.

| Project | District | Scale | Stage |

|---|---|---|---|

| Muli Copper Project | Mumbwa | 418 km² | Greenfield anomaly |

| Kangili Copper Project | Mkushi | Early-stage | Geochemical targeting |

| Additional Licences | Ndola, Kitwe, Kasempa | Various | Copperbelt extensions |

Key Geological Consideration: A 418 km² greenfield anomaly is a genuinely large exploration footprint for a junior company. For comparison, many Tier 1 copper deposits occupy surface footprints of just 5 to 50 km² at the ore body level. The scale of Muli suggests either a very large mineralised system, multiple stacked targets, or a combination of both — all of which represent significant upside if validated by systematic geophysics and drilling.

Dissecting the $30 Million Copper Investment Plan

The headline figure attached to Makor's Zambia strategy is a US$30 million total investment commitment, but the architecture of that commitment is as important as the number itself. Rather than front-loading capital into a high-risk single drilling campaign, the company has structured its expenditure into two distinct phases separated by a clear decision gate. In this respect, Makor's approach reflects broader copper investment strategies that emphasise phased capital discipline over speculative early commitment.

Phase 1: Building the Geological Foundation (2026)

- Budget allocation: US$2 to US$3 million

- Key activities include systematic airborne and ground geophysical surveys to map subsurface conductors, multi-element soil geochemical sampling programs to define anomaly footprints, geological mapping to interpret structural controls on mineralisation, and target ranking to prioritise the most compelling drill locations

- Primary objective: Generate sufficient geological data to make an informed and defensible drilling decision

Phase 2: Drill-Out and Resource Definition (Post-2026)

- Budget allocation: US$20 to US$30 million

- Key activities include diamond and reverse circulation drilling across ranked targets, metallurgical testwork on representative samples, resource estimation to JORC or NI 43-101 standard, and preliminary scoping assessments

- Trigger condition: Positive Phase 1 results confirming a viable and scalable mineralised system

| Phase | Budget | Status | Key Deliverable |

|---|---|---|---|

| Phase 1 | US$2 to US$3 million | Committed for 2026 | Drill-ready targets |

| Phase 2 | US$20 to US$30 million | Milestone-contingent | Resource estimate |

| Total | Up to US$30 million | Progressive | Full project definition |

This phased structure is not merely a financing convenience. It reflects a sophisticated understanding of exploration risk management. By requiring Phase 1 data before committing Phase 2 capital, Makor preserves the ability to redirect, scale back, or accelerate based on actual geological evidence rather than initial assumptions.

Investor Insight: Junior explorers that commit large drilling budgets without adequate preliminary geophysical and geochemical work frequently waste capital on poorly targeted holes. The Phase 1 investment in systematic data acquisition is often where the most critical value is created, even though it generates fewer headline announcements than drilling results.

African Mining Week 2026: Why Cape Town Is the Right Stage

African Mining Week, held annually in Cape Town, functions as one of the continent's most concentrated gatherings of mining capital, expertise, and policy influence. The October 14 to 16, 2026 edition will bring together exploration companies, institutional fund managers, development finance institutions, equipment suppliers, and government representatives from across the African mining landscape.

For a junior explorer like Makor, AMW provides access to a quality of audience that is difficult to replicate through standard investor roadshows. Attendees include professionals who understand the specific risk profile of early-stage African exploration, the regulatory nuances of sub-Saharan jurisdictions, and the commercial structures used to advance projects from greenfield anomaly to operating mine.

The ASM Formalisation Panel: Commercial Strategy Disguised as Policy Advocacy

Makor CEO Brooke Bibeault is scheduled to participate in a dedicated panel on accelerating the formalisation of artisanal and small-scale miners (ASM). While this might appear to be a corporate social responsibility gesture, the commercial logic behind this focus is considerably more sophisticated.

Artisanal and small-scale mining in Zambia and across sub-Saharan Africa represents a paradox for large-scale operators. On one hand, ASM activity provides livelihood income for millions of workers and their families and often predates formal exploration in identifying mineralised areas. On the other hand, unregulated ASM creates overlapping tenure conflicts, environmental liabilities, community tensions, and supply chain traceability problems that can delay or derail formal mining projects.

Bibeault's AMW presentation is expected to address how Makor's MineHive program approaches this challenge not as a compliance obligation but as a commercial opportunity. The program aims to integrate artisanal operators into traceable, structured supply chains that satisfy downstream copper buyers' increasingly rigorous responsible sourcing requirements.

The downstream demand for supply chain transparency is accelerating rapidly. The European Union's Corporate Sustainability Due Diligence Directive and the United States Uyghur Forced Labor Prevention Act have established precedents for import-linked traceability requirements. Battery manufacturers supplying European and North American automotive OEMs are already facing contractual obligations to demonstrate that copper inputs are sourced through verifiable, responsible supply chains.

Emerging Commercial Logic: Mining companies that can offer buyers a traceable, formally structured copper supply chain sourced from ASM-integrated operations are positioned to command supply chain premium from downstream purchasers who would otherwise face regulatory exposure from opaque sourcing. This transforms the cost of ASM formalisation into a revenue-enhancing asset rather than a purely philanthropic expenditure.

Structural Risks That Capital Allocators Must Quantify

A balanced assessment of the Makor Zambia copper plan at African Mining Week must acknowledge the structural challenges that accompany any exploration investment in sub-Saharan Africa, regardless of the quality of the geological thesis.

Zambia-Specific Risk Factors

- Fiscal regime variability: Zambia has a documented history of adjusting mining royalty structures. The country moved to a variable royalty rate linked to copper prices, then subsequently modified the framework again. Long-duration capital commitments are sensitive to royalty rate changes that alter project economics materially.

- Infrastructure deficits in exploration corridors: Remote licence areas such as those in the Mumbwa and Mkushi districts often lack sealed road access, reliable water infrastructure, and grid power connectivity. These gaps add capital requirements and timeline risk to early-stage programs.

- Currency and sovereign risk exposure: Zambia experienced a sovereign debt default in 2020 and subsequently completed a restructuring process. While the macroeconomic situation has stabilised, kwacha volatility remains a consideration for USD-denominated investment budgets.

- ASM conflict potential: Without effective community engagement and formalisation programs, artisanal activity within or adjacent to formal licence areas can generate operational disruptions and reputational complications.

Comparison of Junior Explorer Risk Profiles in the Copperbelt

| Risk Category | Single-Target Explorer | District-Scale Explorer |

|---|---|---|

| Geological concentration risk | High | Diversified across targets |

| Capital efficiency at early stage | Higher per target | Lower per target initially |

| Discovery upside | Limited to one outcome | Multiple potential discoveries |

| ASM and community complexity | Localised | Broader stakeholder footprint |

| Government relationship importance | Moderate | Elevated due to scale |

The next major ASX story will hit our subscribers first

The Bigger Picture: Copper Supply Chains and the Battery Economy

The investment thesis underpinning exploration activity in Zambia's Copperbelt is ultimately a derivative of the copper supply crunch that materials scientists and energy economists have been modelling for several years. Global copper demand is projected by multiple independent research bodies to reach somewhere between 30 and 35 million tonnes per annum by 2035, compared to current annual production of approximately 22 million tonnes. The gap between those figures represents one of the most consequential supply chain challenges of the coming decade.

Zambia sits in a geologically privileged position to contribute to closing that gap. The country's Copperbelt extends into some of the least explored portions of the broader sediment-hosted copper system, and its relatively stable governance environment compared to neighbouring DRC gives it a structural advantage in attracting long-duration exploration capital. In addition, the broader critical minerals demand driven by the global energy transition continues to place copper at the forefront of strategic investment priorities.

The Makor Zambia copper plan at African Mining Week is best understood not as a single company announcement but as a data point within a much larger pattern of junior capital mobilisation toward African copper. The companies that establish credible geological footprints, defensible community relationships, and structured ASM formalisation programs in this current exploration cycle are positioning themselves for the value inflection point that typically arrives when a district-scale exploration program transitions from anomaly identification to confirmed mineralisation.

Furthermore, the growing prevalence of majors and junior partnerships in the Copperbelt signals that large producers are increasingly looking to junior explorers to replenish their project pipelines — a dynamic that could provide significant exit or joint venture optionality for well-positioned early movers like Makor.

Speculative Consideration: If even one of Makor's large-footprint Zambian licence areas delivers a discovery comparable in scale to other Copperbelt sediment-hosted systems, the capital appreciation potential relative to current exploration-stage valuations could be substantial. However, it bears emphasising that greenfield exploration success rates globally average well below 10% at the prospect-to-discovery conversion stage. Investors should treat all exploration-stage outcomes as inherently speculative and calibrate position sizing accordingly.

Key Takeaways for Investors and Industry Observers

- Makor's phased capital deployment model limits early downside exposure while preserving the option to scale significantly if Phase 1 data supports it

- The 418 km² Muli Copper Project represents a genuinely large exploration target by industry standards, with district-scale potential requiring systematic modern geophysical assessment before its true discovery probability can be assessed

- CEO Brooke Bibeault's AMW panel role on ASM formalisation is strategically significant beyond its surface optics, linking directly to supply chain traceability demands from downstream copper consumers

- Zambia's 2031 production target of 3 million tonnes creates a compelling national context for copper exploration investment, though the gap between ambition and execution remains considerable

- The MineHive ASM integration program positions Makor at the intersection of responsible sourcing regulation and community development, which is increasingly a prerequisite for securing social licence and attracting ESG-aligned capital

- All exploration-stage investments carry material speculative risk, and the geological thesis underlying Makor's Zambia portfolio will require systematic validation through phased field programs before any resource-level conclusions can be drawn

Investors and industry participants seeking further context on Zambia's copper sector and African mining investment trends can access relevant reporting and analysis through Mining.com, which covers developments across the global mining industry including African copper exploration. This article does not constitute financial advice. All forward-looking statements and projections should be treated as speculative in nature.

Want to Track the Next Major Copper Discovery the Moment It Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper exploration plays positioned to benefit from the global supply crunch — ensuring subscribers can act on actionable opportunities ahead of the broader market. Explore historic discoveries and their returns to understand the scale of what early positioning can mean, then begin your 14-day free trial at Discovery Alert to secure your market-leading advantage.