June 18, 2026

The Portfolio Gap That Cash-Generative Producers Are Racing to Fill

Across the base metals sector, a structural imbalance has been widening for several years. Cash-generative producers with clean balance sheets sit on one side; proven but underfunded development-stage projects sit on the other. The capital markets that once bridged this gap have tightened considerably, with higher-for-longer interest rates making project finance increasingly inaccessible for pre-feasibility assets that lack the engineering certainty lenders require. The result is a growing universe of stranded development projects whose resource bases are real, whose infrastructure exists, but whose pathway to production has stalled for want of a capable, well-capitalised operator.

This dynamic is precisely the environment in which the Central Asia Metals acquisition of Cygnus Metals was conceived. The transaction is not a speculative bet on an undiscovered resource. It is a calculated move by a producer with established operating cash flow to absorb a brownfield copper-gold development asset that has already cleared the most capital-intensive phase of the mining value chain: proving that the resource is there.

When big ASX news breaks, our subscribers know first

Why Development-Stage Assets Are the Highest-Leverage Position in a Producer's Growth Cycle

The Three-Stage Portfolio Model and the Gap CAML Needed to Address

Central Asia Metals operates two producing mines: the Kounrad copper heap leach operation in Kazakhstan and the Sasa zinc-lead underground mine in North Macedonia. Beyond these, the company holds early-stage exploration interests, including positions in Kazakhstan and a minority stake in Aberdeen Minerals in Scotland. What this portfolio conspicuously lacked was anything occupying the middle ground between exploration-stage optionality and operating cash flow.

That middle ground, the development stage, is precisely where the most significant valuation re-rating occurs. The mining lifecycle re-rating from a preliminary economic assessment (PEA) stage typically sees a project trade at a deep discount to its underlying net asset value (NAV), reflecting the market's uncertainty about execution, permitting timelines, and financing. As successive engineering milestones are achieved and de-risking progresses, that discount narrows, and the asset's market value re-rates upward, sometimes dramatically.

CAML's management has articulated this logic clearly: the company's goal is not to discover a new orebody but to apply its operational expertise and balance sheet strength to accelerate an existing, proven asset through the de-risking curve, capturing that NAV discount compression rather than relying on exploration luck.

Why Brownfield Over Greenfield

The distinction between brownfield and greenfield development is frequently underappreciated by retail investors but is central to how sophisticated mining operators think about capital intensity and risk.

A greenfield project requires:

- Construction of all surface and underground infrastructure from a standing start

- A full environmental assessment and baseline studies conducted without prior regulatory context

- Establishment of a tailings management facility, including permitting from scratch

- Community and First Nations engagement built without any legacy relationships

- Procurement of all access roads, power infrastructure, and processing facilities

A brownfield asset with retained infrastructure eliminates or compresses many of these steps. The capital expenditure profile narrows, the permitting timeline shortens, and the execution risk diminishes because the engineering unknowns have already been partially resolved by whoever operated the site previously.

Chibougamau: What the Asset Actually Represents

A District With Deep Historical Context

The Chibougamau district in northern Québec has a documented mining history stretching back decades. The region's geology is characterised by Archean-age volcanic and sedimentary sequences that host copper-gold mineralisation, a style of deposit that is well understood by both operators and regulators in the province. This geological familiarity reduces the interpretive risk associated with resource modelling and mine planning.

The project as assembled by Doré Copper and subsequently expanded by Cygnus comprises five separate deposits: Corner Bay, Devlin, Joe Mann, Golden Eye, and Cedar Bay. These deposits are connected by a continuous mineralised corridor extending across an 18-kilometre strike length, the majority of which remains untested by modern drilling techniques. This exploration upside is genuinely additive rather than speculative, given that the deposits already defined represent only a fraction of the total prospective strike.

Resource Growth and Grade Profile

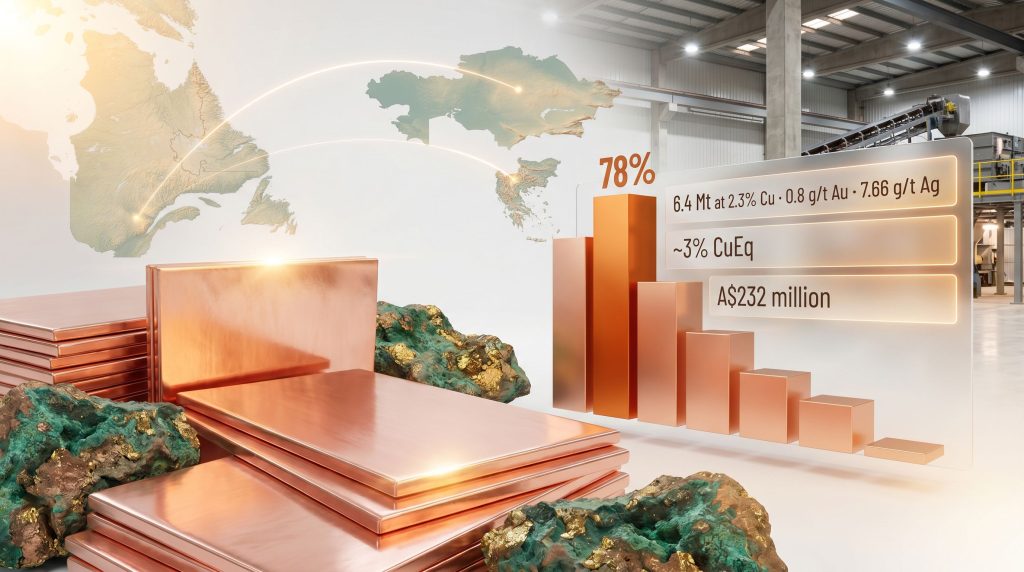

Under Cygnus's stewardship, the measured and indicated resource base at Chibougamau grew by 78% to 6.4 million tonnes at a grade of 2.3% copper, 0.8 grams per tonne gold, and 7.66 grams per tonne silver, equating to approximately 3% copper equivalent on a combined basis. The inferred resource category adds a further 8 million tonnes, representing significant conversion potential through continued drilling.

To put this grade profile in context, the global weighted average head grade for copper mines has been declining for decades, with many large-scale operations now processing material below 0.5% copper. Understanding grade and permitting is essential here — Chibougamau's approximately 3% copper equivalent places it firmly in the high-grade category, a characteristic that materially improves unit economics and reduces the tonnage required to generate meaningful metal output.

Grade matters more than resource size in today's capital environment. High-grade copper-gold deposits demand less processing throughput to achieve the same metal output, reducing both capital expenditure requirements and operating costs per tonne of refined metal. Chibougamau's 3% copper equivalent compares favourably with most advanced-stage copper development projects currently seeking financing globally.

The Copper Rand Mill: A Refurbishable Processing Asset

One of the least-discussed but most financially significant features of Chibougamau is the Copper Rand processing facility, a mill that operated until 2008 and remains in a refurbishable condition. For a development project, inheriting an existing processing facility rather than constructing one from scratch can represent a capital saving of tens to hundreds of millions of dollars depending on scale, even after accounting for refurbishment costs.

The mill's prior operation also means that much of the process engineering thinking for the deposit has already been done. Metallurgical flowsheets, reagent consumption profiles, and equipment specifications from the prior operating period provide a meaningful head start on the feasibility study process that CAML intends to advance post-acquisition.

How the Central Asia Metals Acquisition of Cygnus Metals Is Structured

Transaction Terms at a Glance

The Central Asia Metals acquisition of Cygnus Metals is structured as an all-share scheme of arrangement under Australian law, with CAML issuing 0.06 new shares for every Cygnus share held. The implied price of approximately A$0.176 per Cygnus share represents a premium of roughly 60% to Cygnus's closing price immediately prior to the announcement.

| Deal Parameter | Detail |

|---|---|

| Transaction Type | All-share scheme of arrangement |

| Exchange Ratio | 0.06 CAML shares per Cygnus share |

| Implied Price Per Cygnus Share | ~A$0.176 |

| Premium to Last Close | ~60% |

| Total Deal Value | ~A$232 million |

| Post-Completion CAML Ownership | ~70% |

| Post-Completion Cygnus Ownership | ~30% |

| Target Completion | September 2026 |

Major Cygnus shareholders controlling approximately 29% of the register have indicated their intention to vote in favour of the scheme, subject to standard conditions, providing an early signal of institutional support for the transaction.

The Logic of Paying in Shares, Not Cash

The all-share structure is not simply a financing convenience. It is a deliberate balance sheet decision. CAML enters this transaction carrying no meaningful debt, with only a minor overdraft facility of approximately US$1 million drawn at present. Paying in cash or taking on debt to fund the acquisition would have consumed the very financial capacity that makes CAML a credible development partner for Chibougamau.

By issuing shares, CAML preserves:

- Its full cash flow for sustaining capital expenditure at Kounrad and Sasa

- Ongoing exploration funding in Kazakhstan and Scotland

- The continuation of its 30 to 50% of free cash flow dividend policy throughout the integration period

- The balance sheet headroom to finance Chibougamau's development through a combination of operating cash flow and conservative debt, targeting a leverage ceiling of approximately 2x net debt to EBITDA

This structure also means Cygnus shareholders are not being cashed out at a fixed point in time. Instead, they become CAML shareholders, retaining exposure to both the development upside at Chibougamau and the ongoing cash flow from Kounrad and Sasa.

The Brownfield Advantage in Practice: Infrastructure, Tailings, and Operational Overlap

What Survives from the Prior Operating Period

Beyond the Copper Rand mill, the Chibougamau site retains civil engineering works, concrete foundations, and administrative infrastructure from its operational era. These are not trivial assets. In remote northern Québec, establishing basic operational infrastructure — from roads and power connections to buildings capable of withstanding sub-Arctic conditions — represents a meaningful capital and time cost that Chibougamau has already absorbed.

The tailings facility carries particular regulatory significance. Under Québec's environmental framework, the tailings storage area retains classification as an active deposition site, meaning CAML does not face the prospect of initiating a new tailings permitting process from scratch. For context, the establishment of a new tailings facility in a Canadian jurisdiction typically requires a comprehensive environmental assessment that can add years to a project's timeline. This existing classification compresses that risk substantially.

Why CAML's Operational DNA Transfers Directly

A detail that receives insufficient attention in most coverage of this transaction is the degree to which Chibougamau's technical requirements mirror what CAML already does at Sasa. The Sasa mine operates a dry-stack tailings system, and critically, the operation involves depositing dry-stack tailings over legacy historical tailings — a technically demanding process that requires precise geotechnical management and regulatory co-ordination.

This is not a common operational skill set. Many mining companies have never managed this specific challenge. CAML has already navigated it at Sasa, and Chibougamau's requirements are described as closely analogous. This, consequently, reduces what would otherwise be a significant execution risk to a largely known engineering problem for CAML's team.

The transferability of tailings management expertise is a key but underappreciated risk mitigant in this transaction. Dry-stack tailings over legacy impoundments requires geotechnical modelling, staged deposition planning, and ongoing regulatory engagement that CAML has already developed institutional competence in.

The Development Pathway: From PEA to Construction Decision

A Step-by-Step Progression

CAML's stated development roadmap for Chibougamau following completion of the acquisition is structured and sequential:

- Finalise the updated PEA: Cygnus had already commenced updating the 2022 Doré Copper PEA to incorporate the expanded resource base. CAML will complete this work, providing the foundational economic framework for subsequent study stages.

- Advance directly to feasibility study: Rather than conducting an intermediate pre-feasibility study, CAML intends to move from the updated PEA directly into a full feasibility study, compressing the timeline.

- Progress environmental baseline work: Environmental monitoring programmes already underway will continue, building the dataset required for Québec's environmental assessment process.

- Deepen First Nations engagement: The existing relationship with the Cree Nation of Oujé-Bougoumou, established by Doré Copper and continued by Cygnus, will be maintained and expanded. Social licence is increasingly recognised as a rate-determining constraint on mining project development timelines in Canada.

- Target a construction decision within approximately four to five years of transaction completion, contingent on feasibility outcomes and permitting progress.

Why Cygnus Could Not Have Done This Alone

The structural position of junior copper developers in the current market deserves direct analysis. A company at the PEA stage, seeking to advance a project to a construction decision, typically faces the following capital requirements:

- One to two further equity raises to fund feasibility study work and environmental baseline programmes, each dilutive to existing shareholders

- The organisational challenge of building an in-house project management and construction capability, which requires years of hiring and institutional knowledge development

- Access to project finance markets that, in 2025 and 2026, have become demonstrably more selective, with lenders concentrating capital in assets that have achieved pre-feasibility or better

By combining with CAML, Cygnus shareholders bypass all three constraints simultaneously. They gain access to CAML's established balance sheet, its institutional relationships with lenders and capital markets, and its existing construction and operational expertise, without the dilution associated with funding these capabilities independently.

The next major ASX story will hit our subscribers first

Existing Operations: The Cash Engine Behind the Strategy

Kounrad and Sasa Performance

CAML's ability to execute the Central Asia Metals acquisition of Cygnus Metals without compromising shareholder returns depends critically on the continued performance of its operating assets. The signals here are positive. Kounrad delivered slightly above-expected copper production in the first quarter of 2026, with seasonal output typically increasing through the warmer summer months as the heap leach operation benefits from improved solution kinetics. Kazakhstan exploration drilling results are anticipated in Q3 2026.

At Sasa, the mine is reported to be recovering from previously disclosed operational challenges. Across the first five months of 2026, CAML's combined operations are tracking ahead of the prior corresponding period across all three metals simultaneously — copper, lead, and zinc — a position that reinforces confidence in the sustainability of the dividend through the Chibougamau integration period. Half-year results are scheduled for September 2026.

The Re-Rating Investment Thesis and Macro Context

NAV Discount Compression as the Core Opportunity

The investment logic underpinning this transaction is grounded in a well-established feature of junior mining markets. PEA-stage development assets structurally trade at deep discounts to their underlying NAV because the market prices in execution risk, financing risk, permitting risk, and the time value of capital tied up before first production. As each of these risk factors is systematically addressed through engineering progress and regulatory milestones, the discount narrows and the market value of the asset re-rates toward its theoretical NAV.

CAML is essentially purchasing that re-rating optionality at a price that reflects Cygnus's current discount, then applying its operational and financial capabilities to accelerate the de-risking process. This is a fundamentally different value creation mechanism from organic resource discovery and one that is far more predictable in its inputs, if not its outcomes.

Macro Tailwinds Reinforcing the Case

Several macro conditions are converging to make this transaction particularly timely. Furthermore, broader copper market trends are reinforcing the strategic rationale at precisely the right moment:

- Copper prices near record levels in 2025 and 2026 are directly improving the economic returns modelled in project studies, widening the NPV of development assets like Chibougamau at any given discount rate

- Junior financing conditions have tightened materially, concentrating development capital in the hands of cash-generative producers and lenders rather than standalone explorers

- Geographic diversification into Canada reduces CAML's single-country and currency concentration risk relative to its current Kazakhstan and North Macedonia portfolio

- A planned TSX or TSX Venture Exchange listing will expose CAML to North American institutional and retail investor capital, potentially expanding the shareholder base and improving liquidity

In addition, the broader wave of mining M&A activity across the sector suggests that CAML is far from alone in recognising the strategic value of well-positioned brownfield development assets at this point in the cycle.

Key Near-Term Catalysts

| Catalyst | Expected Timing |

|---|---|

| Kazakhstan exploration drilling results | Q3 2026 |

| Cygnus transaction completion | September 2026 |

| CAML half-year financial results | September 2026 |

| TSX / TSX-V listing decision | Alongside or post-completion |

| Updated Chibougamau PEA | Post-completion (timeline TBC) |

| Sasa operational recovery confirmation | H2 2026 half-year results |

Frequently Asked Questions

What is the Central Asia Metals acquisition of Cygnus Metals?

Central Asia Metals, a London-listed copper, zinc, and lead producer, has proposed an all-share acquisition of ASX-listed Cygnus Metals, valued at approximately A$232 million. The transaction adds the Chibougamau copper-gold development project in Québec to CAML's portfolio and is structured as a scheme of arrangement under Australian law, targeting completion in September 2026.

What premium are Cygnus shareholders receiving?

The implied price of approximately A$0.176 per Cygnus share represents a premium of roughly 60% to Cygnus's closing price immediately before the announcement. Consideration is paid entirely in CAML shares at an exchange ratio of 0.06 CAML shares per Cygnus share held.

Will CAML take on significant debt to fund Chibougamau's development?

CAML has indicated a conservative leverage ceiling of approximately 2x net debt to EBITDA for the development phase, governed by a five-year balance sheet planning framework. The company enters the transaction with no meaningful debt, and the all-share deal structure ensures the acquisition itself does not consume cash reserves.

Why is the tailings facility classification significant?

The existing tailings storage area at Chibougamau retains an active deposition site classification under Québec regulations, meaning CAML does not need to initiate a new tailings permitting process from scratch. Establishing a new tailings facility in a Canadian jurisdiction can add multiple years to a project's regulatory timeline; this existing classification materially reduces that risk.

What happens to Cygnus's management team after completion?

CAML has indicated that Cygnus's in-country operational team in Canada, including project leadership, will remain in place following completion. A former Cygnus director is also expected to be nominated to the CAML board, providing continuity across technical, regulatory, and community engagement functions.

Is CAML considering further acquisitions after this deal?

Management has indicated that near-term focus will be concentrated on closing and integrating the Cygnus transaction. The balance sheet is described as remaining capable of supporting opportunistic transactions, but no additional M&A activity is being actively pursued, with limited bandwidth expected over the following six to twelve months.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, timelines, and development targets discussed herein are forward-looking statements subject to material risks and uncertainties. Readers should conduct their own due diligence before making any investment decisions. Past operational performance does not guarantee future results.

Want to Identify the Next Major Copper-Gold Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly converting complex mineral data across 30+ commodities into a single, actionable gold-equivalent metric — so subscribers can identify high-potential opportunities like significant copper-gold discoveries the moment they are announced. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.