June 23, 2026

Central Bank Gold Accumulation Patterns Signal Currency System Transformation

Financial institutions worldwide face unprecedented balance sheet vulnerabilities following decades of quantitative easing policies that expanded monetary supply without corresponding economic productivity growth. Central banks across developed and emerging economies have systematically increased their gold reserves for five consecutive years, with annual purchases exceeding 1,000 tonnes since 2020. This accumulation pattern represents approximately 30% of global gold production annually, creating supply constraints while signaling institutional recognition of fiat currency system limitations that could trigger gold revaluation and the big reset.

The purchasing power erosion affecting major currencies has accelerated beyond historical norms, with the U.S. dollar losing approximately 96-97% of its value since Federal Reserve establishment in 1913. More concerning for policymakers, currency debasement measured against gold has intensified over the past 25 years, with most major currencies declining an additional 90% in purchasing power terms. These metrics suggest systemic monetary instability rather than cyclical economic adjustments.

When big ASX news breaks, our subscribers know first

Structural Weaknesses in Dollar-Based Global Finance

Sovereign Debt Dynamics and Interest Expense Burden

Current U.S. debt-to-GDP ratios have reached 123-128% as of Q3 2024, approaching levels historically associated with fiscal crises in other developed economies. Federal interest expenditures consumed approximately $659 billion in fiscal year 2024, representing roughly 13% of total federal revenue. Unlike previous debt cycles, these obligations occur during periods of suppressed interest rates, suggesting exponential growth potential as monetary policy normalizes.

The European Union faces similar constraints with accumulated sovereign debt exceeding sustainable levels across multiple member states. Italy, Spain, and France maintain debt-to-GDP ratios above 100%, while Germany's fiscal position has deteriorated following energy crisis responses and industrial competitiveness challenges. These structural imbalances limit traditional monetary policy effectiveness and create incentives for alternative reserve strategies.

Central Bank Balance Sheet Vulnerabilities

Post-2008 quantitative easing programs expanded major central bank balance sheets beyond historical precedent:

- Federal Reserve: $900 billion (2007) to $7.4 trillion peak (2022)

- European Central Bank: €1.5 trillion to €8+ trillion expansion

- Bank of Japan: Sustained asset purchases exceeding 100% of GDP

- People's Bank of China: Coordinated yuan liquidity injections supporting domestic growth

These balance sheet expansions created asset price distortions across global markets while reducing central bank policy flexibility. Current attempts at quantitative tightening have proven politically and economically challenging, with most central banks resuming expansionary policies despite persistent inflation concerns.

Regional Currency Arrangement Development

Emerging market economies have accelerated development of dollar-alternative settlement systems following geopolitical tensions and sanctions regime implementation. Furthermore, the BRICS economic bloc has proposed settlement mechanisms utilizing a proposed currency unit with potential 40% gold backing, though final specifications remain under development. China has established bilateral currency swap agreements with over 30 countries, facilitating trade settlements outside traditional dollar channels.

Regional development banks have begun accepting commodity collateral for infrastructure financing, reducing dependence on dollar-denominated debt markets. The New Development Bank, established by BRICS members, has issued bonds in local currencies while maintaining gold reserves as balance sheet stabilization mechanisms.

Gold Revaluation Mechanisms as Economic Policy Tools

Historical Precedents for Monetary Metal Price Adjustments

Government-directed gold revaluations have provided fiscal relief during previous economic crises, offering precedent for contemporary policy applications:

| Year | Country | Previous Price | New Price | Economic Context | Fiscal Impact |

|---|---|---|---|---|---|

| 1934 | United States | $20.67/oz | $35.00/oz | Great Depression recovery | $2.8 billion accounting gain |

| 1971 | Global System | $35.00/oz | Market-determined | Bretton Woods collapse | Fiat currency transition |

| 2024 | Market-driven | $1,200/oz (2020) | $2,600-2,800/oz | Inflation/geopolitical stress | Ongoing price discovery |

The 1934 U.S. gold revaluation generated substantial Treasury accounting gains while strengthening Federal Reserve balance sheet positions during economic recovery efforts. This precedent demonstrates government capacity to adjust official gold valuations for macroeconomic policy objectives without requiring gold sales or physical transfers.

Technical Implementation Through Gold Revaluation Accounts

Modern central banks utilise Gold Revaluation Accounts (GRAs) to recognise unrealized gains on gold holdings without requiring physical sales. The European Central Bank system employs these mechanisms extensively, allowing member nation central banks to strengthen regulatory capital positions through accounting adjustments rather than asset liquidation.

U.S. Treasury Gold Certificate System:

- Current statutory gold price: $42.22/ounce (unchanged since 1934)

- Total U.S. gold holdings: 261.5 million ounces (8,133.5 tonnes)

- Market value at $2,700/ounce: ~$706 billion

- Unrealized accounting gain potential: ~$664 billion

Congressional authority under 31 U.S.C. § 5117 permits gold price adjustments for fiscal policy purposes, though such actions require legislative approval rather than executive discretion. Alternative approaches through Treasury certificate revaluation could achieve similar balance sheet effects within existing legal frameworks.

Fiscal Impact Calculations Under Revaluation Scenarios

At current U.S. gold holdings of 261.5 million ounces, a coordinated revaluation from $42.22 to $8,000 per ounce could theoretically generate $2.08 trillion in accounting gains, potentially supporting debt reduction or infrastructure investment programs.

International coordination would amplify these effects across participating economies. The International Monetary Fund holds approximately 2,814 tonnes of gold (90.5 million ounces), providing multilateral institutional capacity for coordinated revaluation initiatives during systemic financial stress.

Gold Price Impact Scenarios:

| Revaluation Level | U.S. Treasury Gain | Global Central Bank Impact | Economic Rationale |

|---|---|---|---|

| $5,000/ounce | $1.3 trillion | $4.2 trillion globally | Partial monetary anchor |

| $8,000/ounce | $2.08 trillion | $6.7 trillion globally | Crisis intervention level |

| $15,000/ounce | $3.9 trillion | $12.6 trillion globally | Full monetary system reset |

Central Bank Physical Gold Accumulation Strategies

Emerging Market Purchase Patterns and Motivations

Central bank gold purchases have maintained momentum above 1,000 tonnes annually for five consecutive years, representing the most sustained accumulation period in modern monetary history. Additionally, this gold strategic investment approach has implications for the broader financial system:

Annual Central Bank Gold Purchases (2020-2024):

| Year | Total Purchases (tonnes) | % of Global Production | Leading Purchasers |

|---|---|---|---|

| 2020 | 1,097 | 31% | China, Russia, Turkey |

| 2021 | 1,037 | 30% | China, Uzbekistan, India |

| 2022 | 1,037 | 29% | Turkey, China, Egypt |

| 2023 | 1,037 | 30% | China, Poland, Singapore |

| 2024 | 1,037 | 30% | China, India, Kazakhstan |

China leads global accumulation with approximately 380 tonnes purchased in 2024, increasing official holdings from ~600 tonnes (2009) to over 2,261 tonnes currently. This strategy aligns with yuan internationalisation efforts and preparation for alternative settlement systems reducing dollar dependency.

Geopolitical Hedging Against Currency Weaponisation

Russia's gold accumulation accelerated following 2014 Crimea sanctions and intensified after 2022 Ukraine invasion sanctions, demonstrating gold's role as sanctions-resistant reserve asset. Russian Central Bank increased holdings from ~600 tonnes (2014) to over 2,332 tonnes (2024) despite international financial restrictions.

Similar patterns emerge across emerging markets facing potential sanctions risks or seeking reduced dollar exposure:

- Turkey: Increased holdings to 500+ tonnes while managing currency volatility

- India: Strategic purchases supporting rupee internationalisation initiatives

- Kazakhstan: Regional power positioning through hard asset accumulation

- Poland: European Union member diversifying away from ECB-controlled reserves

Western Central Bank Gold Management Evolution

European Central Bank member nations face institutional tensions regarding gold control, exemplified by Italy's political leadership expressing desire to regain national authority over gold reserves currently managed by the ECB system. Italian gold holdings total approximately 2,451.8 tonnes, representing significant sovereign wealth under supranational institutional control.

These tensions reflect broader sovereignty concerns as national governments reconsider centralised monetary authority during economic stress periods. Similar dynamics affect Federal Reserve relationships with U.S. Treasury gold holdings, though institutional frameworks remain more stable than European arrangements.

Basel III Gold Treatment Impact:

The Basel III regulatory framework provides preferential treatment for gold holdings, classifying gold as a zero-risk-weighted asset under specific conditions. This regulatory change creates structural incentives for commercial banks and central banks to hold gold rather than traditional sovereign debt instruments carrying higher risk weightings.

Economic Conditions Triggering Systematic Monetary Reform

Debt Sustainability Thresholds Approaching Critical Levels

Historical precedent suggests that when government interest payments exceed 20% of total revenue, monetary system adjustments become necessary to maintain fiscal stability.

Current U.S. federal interest expenses at 13% of revenue approach concerning levels, particularly given suppressed interest rate environment. Normalisation of interest rates to historical averages would push debt service costs toward crisis thresholds observed in previous monetary system transitions.

Demographic pressures compound fiscal stress through unfunded entitlement obligations. Social Security and Medicare unfunded liabilities exceed $100 trillion in present value terms, creating structural deficits requiring monetary accommodation or system restructuring.

Currency Competition From Alternative Settlement Systems

BRICS Currency Development Progress:

The proposed BRICS settlement unit represents the most significant challenge to dollar hegemony since the euro's introduction. Preliminary specifications suggest:

- 40% gold backing for stability and credibility

- Member nation currency basket for remaining 60%

- Commodity settlement capability for energy and raw materials

- Digital infrastructure supporting cross-border transactions

Implementation remains under development, with China leading technical specification discussions. Success would provide dollar-alternative settlement mechanisms for approximately 40% of global population and 25% of world GDP.

Financial System Stress Indicators

Multiple indicators suggest approaching inflection points requiring monetary system adjustments. However, the current gold price forecast suggests continued upward momentum:

Banking Sector Vulnerabilities:

- Commercial real estate loan defaults increasing across regional banks

- Interest rate risk exposure from duration mismatches

- Credit quality deterioration in leveraged lending markets

- Deposit competition pressuring net interest margins

Market Structure Instabilities:

- Bond market liquidity declining during stress periods

- Derivatives markets concentration creating systemic risks

- Asset price correlations approaching dangerous levels

- Volatility suppression mechanisms showing strain

Gold Price Discovery Under New Monetary Architecture

Market-Driven Versus Policy-Driven Price Formation Dynamics

Current gold price discovery occurs primarily through financial markets including COMEX futures, London Bullion Market Association (LBMA) spot markets, and electronic trading platforms. Physical gold markets represent smaller transaction volumes but provide underlying price support during financial system stress.

Paper Versus Physical Gold Dynamics:

The gold market exhibits significant leverage through derivatives trading, with paper gold contracts exceeding physical gold availability by estimated ratios of 100:1 to 250:1. During monetary system transitions, physical gold scarcity typically drives price premiums above paper gold contract prices, creating delivery stress in financial markets.

Shanghai Gold Exchange and other Asian physical markets increasingly influence global price discovery, reflecting Eastern economies' preference for physical settlement over cash-settled derivatives. This geographic shift in price-setting authority parallels broader monetary system multipolarisation trends.

Supply-Demand Fundamentals in Constrained Production Environment

Global gold mine production averages approximately 3,000-3,500 tonnes annually, with limited expansion capacity due to geological constraints and regulatory restrictions. Major producing regions face increasing extraction costs as easily accessible deposits deplete and environmental regulations intensify.

Supply Constraints:

- Declining ore grades across major gold mining districts

- Increased extraction costs from deeper, more complex deposits

- Regulatory restrictions limiting new mine development

- Geopolitical risks affecting major producing regions

- Energy cost pressures impacting mining economics

Demand Acceleration:

Central bank purchases consuming 30% of annual production create structural supply deficits for private markets. Investment demand through exchange-traded funds (ETFs) and direct purchases compounds scarcity effects, while industrial applications require steady gold supplies regardless of price levels.

Monetary Gold Pricing Models and Valuation Frameworks

Traditional Valuation Approaches:

| Methodology | Current Estimate | Revaluation Scenario | Underlying Assumptions |

|---|---|---|---|

| Money Supply Backing | $8,000-12,000/oz | 25% reserve backing | M2 money supply coverage |

| Debt Monetisation | $15,000-20,000/oz | Sovereign debt backing | Government liability coverage |

| Currency Crisis | $25,000+/oz | Fiat system collapse | Flight-to-quality scenarios |

| Historical Purchasing Power | $3,000-5,000/oz | Inflation-adjusted pricing | Long-term currency debasement |

Advanced Modelling Considerations:

Monetary economist analyses suggest gold pricing under renewed monetary system integration would reflect currency stability requirements rather than traditional supply-demand dynamics. Countries implementing gold-backed settlement systems would require gold reserves proportional to trade volumes and monetary base coverage ratios.

Financial historians identify approximately 80-year cycles in international monetary system restructuring, with the current cycle suggesting major changes beginning around 2020-2025.

The next major ASX story will hit our subscribers first

Investment Implications During Monetary Transition Periods

Portfolio Allocation Strategies for Currency Regime Change

Historical analysis demonstrates precious metals funds consistently outperform general equity markets by 200-400% during monetary transition periods. The 1970s dollar devaluation cycle, 2000s commodity supercycle, and current gold rally demonstrate this pattern across different economic environments.

Asset Class Performance During Monetary Stress:

- Physical precious metals: Positive correlation with currency debasement

- Mining equities: Leverage to underlying commodity price movements

- Real estate: Inflation hedge with financing risk considerations

- Bitcoin: Digital alternative with adoption volatility

- Traditional bonds: Negative correlation with inflation expectations

- Growth equities: Valuation compression during discount rate adjustments

Hard Asset Positioning Versus Financial Securities

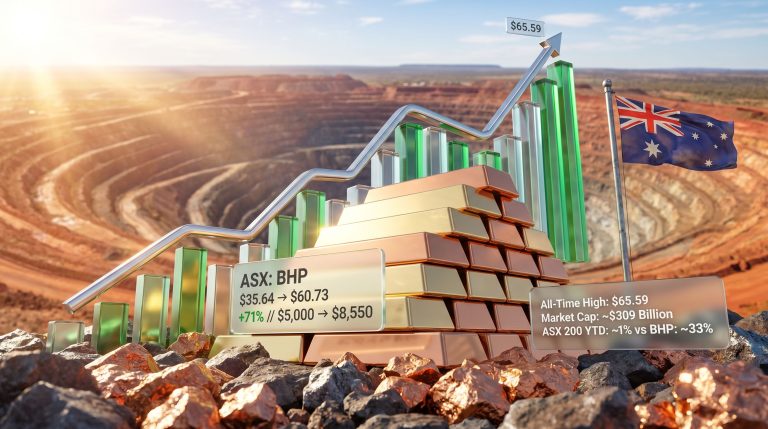

Current precious metals mining companies trade at significantly lower valuations than technology companies despite comparable or superior growth prospects. Major gold producers like Newmont and Barrick Gold maintain price-to-earnings ratios around 10-12, while technology companies with similar market capitalisations trade at 25+ P/E ratios.

Valuation Comparison Analysis:

| Sector | Average P/E Ratio | Revenue Growth | Asset Tangibility | Inflation Sensitivity |

|---|---|---|---|---|

| Gold Mining | 10-12x | 15-25% | High (reserves) | Positive |

| Technology | 25-35x | 10-20% | Low (intangible) | Negative |

| General Market | 18-22x | 5-15% | Mixed | Mixed |

This valuation disparity suggests significant appreciation potential for commodity-related investments as traditional financial assets experience multiple compression during inflation adjustment periods. Furthermore, record-high gold prices continue to support this investment thesis.

Geographic Diversification and Regulatory Considerations

Precious metals ownership regulations vary significantly across jurisdictions, creating opportunities and risks for international investors:

Favourable Jurisdictions:

- Switzerland: Traditional precious metals banking infrastructure

- Singapore: Growing precious metals storage and trading hub

- Canada: Stable mining jurisdiction with resource expertise

- Australia: Major producer with established mining finance sector

Regulatory Risk Considerations:

- Potential ownership restrictions during currency crises

- Import/export controls on precious metals

- Tax treatment changes affecting investment returns

- Confiscation risks under emergency economic powers

Silver's Dual Role in Monetary System Evolution

Industrial Demand Versus Monetary Demand Dynamics

Silver faces unique supply-demand characteristics combining monetary investment demand with essential industrial applications. Approximately 70-80% of annual silver production serves industrial uses including solar panels, electronics, and automotive applications, limiting supply available for investment purposes.

Critical Industrial Applications:

- Solar panel manufacturing: Approximately 130-150 million ounces annually

- Electronics production: Every smartphone contains ~1 gram silver

- Automotive industry: Electric vehicles require 25-50 grams per unit

- Medical applications: Antimicrobial properties drive healthcare demand

- 5G infrastructure: Enhanced connectivity requirements increase silver consumption

Supply Deficit Projections and Market Stress Indicators

Silver markets have experienced production deficits for approximately 50 years, with above-ground silver inventories gradually depleting through industrial consumption. Historical silver coin supplies from pre-1965 U.S. coinage and similar programs in other countries have been largely consumed by industrial applications over recent decades.

Supply-Demand Imbalance Factors:

- Annual mine production: ~850-900 million ounces

- Industrial consumption: ~600-650 million ounces

- Investment demand: ~150-200 million ounces

- Central bank purchases: Minimal but increasing

- Recycling supply: ~180-200 million ounces

Net deficit: Approximately 100-150 million ounces annually

Gold-Silver Ratio Reversion Potential

Geological surveys indicate silver occurs in earth's crust at approximately 10 times the abundance of gold, suggesting long-term price ratios should reflect this natural relationship.

Current gold-silver ratios fluctuate between 70:1 and 90:1, significantly above the historical 15:1 ratio maintained for centuries and well above the geological abundance ratio of 10:1. Monetary system changes incorporating both metals could drive ratio normalisation toward historical precedents.

Silver Price Scenario Analysis:

| Gold Price | 10:1 Ratio | 15:1 Ratio | Current ~80:1 |

|---|---|---|---|

| $5,000/oz | $500/oz | $333/oz | $63/oz |

| $10,000/oz | $1,000/oz | $667/oz | $125/oz |

| $20,000/oz | $2,000/oz | $1,333/oz | $250/oz |

These calculations assume gold-silver ratio reversion during monetary system transitions when both metals resume monetary functions rather than serving primarily as investment vehicles.

Regional Monetary Experiments and Comparative Analysis

Eastern Versus Western Hard Money Integration Approaches

Asian economies demonstrate significantly higher cultural acceptance of precious metals as wealth preservation mechanisms compared to Western financial markets. China, India, and Southeast Asian nations maintain multi-generational traditions of gold and silver ownership transcending government monetary policies.

Cultural and Economic Factors:

- Family wealth transfer traditions utilising physical precious metals

- Government credibility concerns driving private hard asset accumulation

- Limited social safety net access requiring individual wealth preservation

- Banking system maturity gaps favouring tangible asset storage

Western economies emphasise financial asset ownership through institutional intermediaries including exchange-traded funds, mutual funds, and retirement account structures. This institutional mediation creates concentrated ownership patterns and potential systemic risks during financial stress periods.

European Union Monetary Integration Pressures

European Central Bank governance structures create tensions between national sovereignty and supranational monetary control, particularly regarding gold reserve management. Member nations transferred significant gold holdings to ECB authority during euro adoption, reducing national government flexibility during economic crises.

ECB Gold Holdings by Member State:

| Country | Gold Holdings (tonnes) | % of Reserves | ECB Control Level |

|---|---|---|---|

| Germany | 3,355 | 75% | Partial |

| Italy | 2,451 | 68% | Substantial |

| France | 2,436 | 65% | Substantial |

| Spain | 281 | 18% | Full |

| Netherlands | 612 | 55% | Substantial |

Recent political developments in Italy, Germany, and France suggest growing pressure for national governments to regain control over gold reserves held within the ECB system. These tensions reflect broader EU fragmentation pressures and sovereignty concerns during economic stress periods.

Emerging Market Currency Stability Mechanisms

Turkey's Crisis Management Model:

Turkey implemented Gold Revaluation Accounts during 2018 currency crisis, allowing the central bank to recognise unrealized gains on gold holdings for balance sheet strengthening without requiring physical sales. This mechanism provided fiscal flexibility while maintaining gold reserves for future monetary policy applications.

Turkish Central Bank increased gold holdings from approximately 200 tonnes (2014) to over 500 tonnes (2024), demonstrating sustained accumulation strategy despite economic volatility. In addition, gold-backed trade agreements with regional partners reduced foreign exchange vulnerability while supporting currency stability.

Bilateral Trade Settlement Innovations:

Emerging market economies increasingly utilise bilateral currency arrangements and commodity-backed settlements to reduce dollar dependency:

- Russia-China: Yuan-ruble trade settlements with gold backing provisions

- India-Iran: Rupee-rial oil trade with gold settlement options

- Brazil-Argentina: Local currency trade agreements

- Saudi Arabia-China: Yuan-denominated oil contracts

These arrangements create precedents for broader monetary system changes reducing reliance on dollar-denominated international trade, supporting the concept of gold revaluation and the big reset.

Timeline Scenarios for Global Monetary System Reform

Gradual Transition Versus Crisis-Driven Change Models

Incremental Integration Pathway:

Gradual gold integration into existing monetary frameworks would likely progress through voluntary adoption phases:

- Phase 1: Increased central bank gold accumulation (currently occurring)

- Phase 2: Gold-backed trade settlement pilot programs

- Phase 3: Regional currency arrangements with precious metals components

- Phase 4: Major economy gold standard adoption or gold-backed currency units

- Phase 5: International coordination of gold-integrated monetary systems

This timeline could extend over 10-20 years, allowing market adaptation and institutional preparation for monetary system changes.

Crisis-Driven Implementation:

Financial system stress could accelerate monetary reset processes within 2-5 year timeframes:

- Trigger events: Sovereign debt crisis, currency collapse, or geopolitical conflict

- Emergency measures: Coordinated central bank gold revaluation

- System stabilisation: Gold backing for currency confidence restoration

- Long-term structure: New international monetary arrangements

Policy Implementation Requirements and Institutional Coordination

G20 Coordination Mechanisms:

Major monetary system changes require coordination among G20 economies representing approximately 80% of global GDP. Historical precedents including Bretton Woods (1944) and Plaza Accord (1985) demonstrate institutional capacity for coordinated monetary policy adjustments.

Implementation Challenges:

- National sovereignty concerns regarding gold reserve control

- Competitive devaluation risks during transition periods

- Market stability maintenance during system restructuring

- Developing economy inclusion in new monetary arrangements

International Monetary Fund Reform:

IMF Special Drawing Rights (SDR) modifications could incorporate gold components, providing multilateral framework for monetary system evolution. Current SDR composition includes U.S. dollar, euro, Chinese yuan, Japanese yen, and British pound, but excludes commodity backing.

Gold-backed SDR modifications would require consensus among IMF member nations and could provide transition mechanism toward broader monetary system changes incorporating precious metals backing. For instance, detailed gold market analysis suggests this transition could create significant market opportunities.

Strategic Positioning for Monetary System Evolution

Key Indicators for System Change Monitoring

Primary Warning Signals:

- Central bank gold purchase acceleration beyond current 1,000+ tonne levels

- Government debt-to-GDP ratios exceeding 150% in major economies

- Interest expense ratios approaching 20% of government revenues

- Alternative payment system adoption in international trade

- Currency volatility increases among major trading partners

Secondary Indicators:

- Precious metals ETF inflows accelerating beyond historical patterns

- Mining company valuations reaching extreme premiums to book value

- Gold lease rates increasing above 2-3% levels

- Central bank coordination meetings increasing frequency

- Legislative discussions regarding gold standard restoration

Individual and Institutional Investor Positioning

Core Allocation Framework:

- 5-15% precious metals allocation for conservative portfolios

- 10-25% allocation for moderate risk tolerance

- 20-40% allocation for aggressive positioning

Implementation Vehicles:

- Physical ownership: Direct possession with secure storage

- Mining equities: Leveraged exposure to metal price movements

- Precious metals ETFs: Liquid exposure without physical storage

- International diversification: Multi-jurisdiction precious metals exposure

Risk Management Considerations:

Monetary system transitions create both opportunities and risks requiring careful position sizing and diversification. Furthermore, gold miners' insights provide valuable guidance for investment decisions:

- Regulatory changes affecting precious metals ownership

- Tax treatment modifications during monetary system evolution

- Liquidity considerations during market stress periods

- Storage and insurance costs for physical precious metals

- Currency exposure risks for international investments

Long-Term Wealth Preservation During Currency Transitions

Historical precedents suggest precious metals ownership provides superior wealth preservation during monetary system changes compared to traditional financial assets. The 1970s gold performance during dollar devaluation, post-2000 commodity supercycle, and current precious metals rally demonstrate consistent patterns across different economic environments.

Wealth Preservation Strategies:

- Geographic diversification across multiple jurisdictions

- Asset class diversification beyond precious metals alone

- Income generation through dividend-paying mining companies

- Inflation hedging through real asset exposure

- Liquidity maintenance for tactical opportunities

Educational Preparation:

Understanding monetary history and precious metals markets becomes increasingly important as traditional financial relationships change during system transitions. Investors benefit from studying previous monetary system changes, central bank operations, and gold standard economics to navigate coming changes effectively.

The convergence of unsustainable sovereign debt levels, persistent currency debasement, and accelerating central bank gold accumulation suggests approaching inflection points in the international monetary system. While specific timing remains uncertain, the structural forces driving change appear increasingly inevitable. Moreover, the concept of gold revaluation and the big reset gains credibility as traditional monetary mechanisms face unprecedented challenges. Prudent preparation through precious metals exposure, geographic diversification, and monetary system education positions investors for potential opportunities while providing portfolio protection during transition uncertainties.

Disclaimer: This analysis involves speculation about future monetary system changes and precious metals valuations based on historical patterns and current trends. Actual developments may differ significantly from scenarios discussed. Investment decisions should consider individual circumstances, risk tolerance, and professional financial guidance.

Ready to Position Yourself for the Next Major Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping subscribers identify actionable opportunities ahead of the broader market during this unprecedented period of monetary transformation. With central banks accumulating over 1,000 tonnes of gold annually and potential currency system changes on the horizon, understanding historic discovery returns becomes crucial for capitalising on the precious metals sector's evolution.