May 17, 2026

Understanding Central Bank Gold Accumulation in the Modern Economic Landscape

The global financial architecture has witnessed a fundamental shift in central bank behaviour over the past decade. Where traditional monetary policy once focused primarily on interest rate management and foreign exchange stabilisation, today's central bankers increasingly view gold as an essential component of sovereign wealth preservation. This transformation reflects deeper concerns about currency stability, geopolitical risk, and the long-term viability of fiat monetary systems.

The Strategic Role of Gold in Monetary Policy

Central banks maintain gold reserves as a unique asset class that provides monetary insurance without counterparty risk. Unlike foreign exchange reserves denominated in other nations' currencies, gold represents value that cannot be diluted through external monetary policy decisions or subjected to political manipulation by foreign governments.

Global central bank gold reserves represent approximately 20% of all gold ever mined, totalling over 50,000 tonnes held officially by monetary authorities worldwide. The International Monetary Fund maintains approximately 2,814 tonnes within its Special Drawing Rights basket, establishing gold as a cornerstone of the international monetary framework.

Furthermore, the London Bullion Market Association sets standardised specifications for Good Delivery bars used in official transactions, ensuring consistency across central bank settlements. These specifications require minimum 995.0 fineness and precise weight standards, creating a unified global market for institutional gold trading.

How Central Bank Purchases Differ from Private Investment Flows

Central bank gold acquisition operates on fundamentally different principles than private sector investment. While individual investors may respond to short-term price movements or technical indicators, central banks typically implement systematic accumulation programmes spanning multiple years or decades.

Key Differences in Institutional Purchasing:

• Central banks prioritise physical delivery and storage over paper instruments

• Purchase decisions reflect strategic reserve composition targets rather than profit maximisation

• Acquisition timelines extend across multiple economic cycles

• Storage requirements involve sovereign-grade security infrastructure

• Transactions occur through specialised bullion bank networks rather than retail markets

Moreover, central banks often employ graduated purchasing schedules to minimise market impact and achieve average cost positions over extended periods. This approach contrasts sharply with private sector strategies that may concentrate purchases during specific market conditions.

Currency Diversification as a Geopolitical Tool

Gold accumulation serves as a deliberate strategy to reduce dependence on any single reserve currency, particularly the US dollar. This diversification has gained urgency following recent geopolitical events that demonstrated the vulnerability of traditional foreign exchange reserves to sanctions and asset freezes.

The Russian Central Bank's experience during 2022 sanctions prompted a fundamental reassessment among developing economies regarding USD-denominated asset security. Consequently, many central banks subsequently accelerated gold acquisition programmes as insurance against similar scenarios affecting their own reserves.

When big ASX news breaks, our subscribers know first

Why Are Central Banks Accelerating Gold Purchases in 2026?

Central bank gold purchases reached 1,037 tonnes in 2024, representing the second-highest annual acquisition volume on record. This acceleration reflects multiple converging factors that have fundamentally altered central bankers' risk assessment frameworks.

Inflation Hedging and Monetary Stability Concerns

Gold has demonstrated a 40-year average real return correlation with Consumer Price Index measures exceeding 0.60 during high-inflation regimes. This correlation provides central banks with an effective hedge against persistent inflationary pressures that erode the purchasing power of fiat currency reserves.

Current real interest rates in developed economies hover between 0.5-1.5%, significantly below historical averages. At these levels, the opportunity cost of holding non-yielding gold assets becomes substantially more attractive compared to periods when real rates exceeded 2-3%.

Inflation Protection Mechanisms:

• Gold maintains purchasing power across extended inflationary cycles

• Physical gold cannot be diluted through monetary expansion policies

• Historical price performance during stagflationary periods supports reserve protection

• Cross-currency inflation hedging reduces dependence on single-nation monetary policy

In addition, central banks increasingly recognise that traditional inflation targeting mechanisms may prove insufficient during periods of supply-driven price increases or energy shock scenarios. Gold provides a reserve asset that maintains value independently of policy effectiveness, which aligns with gold prices as inflation hedge strategies.

De-dollarization Trends Among Emerging Economies

Emerging market central banks have accelerated USD exposure reduction following the demonstration of reserve weaponisation capabilities during recent geopolitical conflicts. This process involves systematic replacement of dollar-denominated assets with alternatives including gold, other currencies, and strategic commodities.

Turkey exemplifies this approach through explicit policy directives emphasising national sovereignty in reserve management. Turkish authorities have implemented domestic programmes incentivising private sector gold deposits into official reserves, effectively mobilising household holdings into central bank inventory.

India's Reserve Bank has pursued measured but consistent gold accumulation, increasing holdings from 557.8 tonnes in 2016 to 851.2 tonnes by 2024. This 52.6% expansion reflects deliberate reserve diversification rather than opportunistic purchasing.

Supply Chain Security and Resource Independence

Central banks increasingly view gold accumulation through the lens of resource security rather than purely financial portfolio management. Physical gold represents domestically controlled strategic reserves that cannot be interrupted through supply chain disruptions or international sanctions.

This perspective has gained prominence as global supply chains demonstrate vulnerability to geopolitical tensions and trade conflicts. Gold provides central banks with a reserve asset that requires no ongoing international cooperation for value preservation or access.

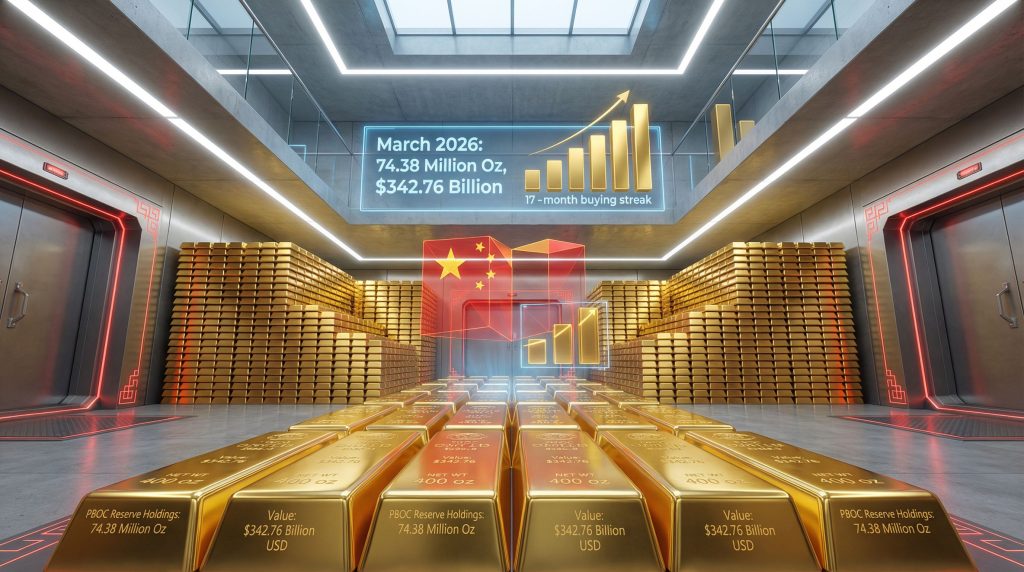

China's Gold Accumulation Strategy: A 17-Month Buying Streak Analysis

The People's Bank of China has maintained consistent gold purchases across 17 consecutive months, demonstrating systematic reserve building that transcends short-term market conditions or price volatility.

Monthly Purchase Patterns and Volume Trends

PBOC Gold Reserve Growth (Recent Quarters)

| Period | Holdings (Million Oz) | Value (USD Billions) | Monthly Change |

|---|---|---|---|

| March 2026 | 74.38 | $342.76 | +0.16 oz |

| February 2026 | 74.22 | $387.59 | +0.03 oz |

| January 2026 | 74.19 | $369.58 | +0.04 oz |

The data reveals several significant patterns in China central bank gold buying behaviour. Monthly acquisition volumes averaged approximately 0.0306 million ounces throughout the 17-month period, indicating systematic rather than opportunistic purchasing decisions.

Volume variations between months (ranging from 0.03 to 0.16 million ounces) suggest either operational constraints in sourcing physical gold or graduated acquisition aligned with fiscal planning cycles. The consistency across 17 months without interruption demonstrates institutional policy commitment rather than discretionary trading.

Reserve Valuation Fluctuations vs. Physical Accumulation

The decline in total USD valuation from February to March 2026 despite continued physical accumulation illustrates gold price volatility impact on reserve calculations. March holdings of $342.76 billion reflected lower per-ounce valuations compared to February's $387.59 billion, despite adding 0.16 million ounces to physical inventory.

This demonstrates that China central bank gold buying prioritises physical quantity accumulation over value timing considerations. The PBOC appears to maintain acquisition targets measured in tonnage rather than dollar amounts, suggesting strategic reserve building objectives transcend short-term price optimisation.

Valuation Analysis Insights:

• Physical accumulation continues regardless of price movements

• Reserve valuations fluctuate significantly with spot price changes

• Acquisition pace remains consistent across different market environments

• Policy framework emphasises strategic position building over cost averaging

Comparison with Historical Chinese Gold Buying Cycles

Between 2009-2015, China's PBOC reported minimal gold purchases averaging 100-150 tonnes annually. The current acceleration began circa 2016, with recent annual acquisition rates reaching 225-300 tonnes through official channels.

The 17-month consecutive purchasing streak represents unprecedented consistency in Chinese gold accumulation patterns. Previous cycles showed more irregular timing with gaps between reported acquisitions, suggesting evolved policy frameworks prioritising steady reserve building.

China's official contribution of approximately 225 tonnes in 2024 represented 21.7% of total global central bank purchases, establishing the PBOC as the dominant institutional buyer in international gold markets according to Reuters analysis.

How Does China's Gold Strategy Compare to Other Major Central Banks?

Comparative Central Bank Gold Holdings & Recent Acquisition Rates

| Central Bank | Total Holdings (Tonnes) | Recent Annual Pace | Strategic Posture |

|---|---|---|---|

| China (PBOC) | 2,325 | 225-300 | Systematic Accumulation |

| Russia | 2,298 | 150-200 (pre-2022) | Consolidation Phase |

| Turkey | 535.6 | 50-75 | Policy-Driven Growth |

| India | 851.2 | 80-100 | Balanced Diversification |

| Germany | 3,384 | Minimal | Maintenance Mode |

| USA | 8,133.5 | Minimal | Historical Holdings |

Russia's Gold Accumulation Before and After 2022

Russian central bank gold accumulation accelerated dramatically following 2014 geopolitical tensions, averaging over 150 tonnes annually between 2015-2021. This aggressive buying strategy reflected explicit policy objectives to reduce USD exposure and prepare for potential sanctions scenarios.

Post-2022 sanctions implementation, Russia maintained existing gold holdings but moderated new acquisitions due to capital flow constraints and reduced utility of foreign reserves during international isolation. Russian holdings expanded from approximately 1,240 tonnes in 2014 to 2,298 tonnes by 2021, representing 85.3% accumulation over seven years.

Turkey's Aggressive Precious Metals Positioning

Turkish monetary authorities have pursued gold accumulation as a politically significant policy objective, with Presidential directives explicitly emphasising national sovereignty in reserve management. This approach contrasts with more traditional central bank practices focused purely on economic considerations.

Turkey increased holdings from 494.4 tonnes in 2015 to 535.6 tonnes by 2024, maintaining steady acquisition despite economic challenges and currency pressures. The Turkish government implemented innovative programmes encouraging domestic gold deposits into central bank reserves, effectively mobilising private sector holdings for official purposes.

India's Balanced Approach to Reserve Diversification

The Reserve Bank of India has implemented measured but consistent gold accumulation while maintaining sophisticated diversified reserve composition. This balanced approach reflects India's large economy and developed capital markets allowing for complex portfolio management.

India's strategy emphasises gradual diversification rather than aggressive accumulation, with holdings growing from 557.8 tonnes in 2016 to 851.2 tonnes by 2024. This 52.6% expansion over eight years demonstrates sustained commitment without dramatic policy shifts that might signal economic distress or geopolitical concerns.

What Economic Signals Drive Sustained Central Bank Gold Buying?

Interest Rate Environment and Opportunity Cost Analysis

Current global interest rate conditions significantly influence central bank gold acquisition decisions. With US Federal Funds rates at 4.25-4.50% and ECB deposit rates around 3.75% as of early 2026, real interest rates approximate 0.5-1.5% after inflation adjustment.

These relatively low real yields reduce the opportunity cost of holding non-yielding gold assets compared to historical periods when real rates exceeded 2-3%. Central banks increasingly view gold's insurance properties as justifying foregone interest income, particularly given persistent inflation concerns.

Real Rate Impact Factors:

• Lower opportunity costs make gold holdings more attractive

• Inflation expectations reduce real yield appeal of government bonds

• Currency depreciation risks offset nominal yield advantages

• Portfolio insurance value compensates for income foregone

Currency Volatility and Safe Haven Demand

Elevated currency volatility across both developed and emerging markets has increased gold's relative attractiveness as a stable store of value. USD Index volatility remains elevated compared to 2015-2020 baseline periods, while emerging market currencies show increased dispersion and hedging demand.

Cross-currency basis spreads reflect growing demand for currency hedging instruments, indicating fundamental concerns about exchange rate stability. Gold provides central banks with a reserve asset that maintains value independently of any specific currency relationship, which supports the broader gold-stock market relationship dynamics.

Geopolitical Risk Assessment and Portfolio Insurance

Indices measuring geopolitical tension have remained elevated throughout 2024, contributing to gold's shadow price premium. Central banks increasingly recognise that traditional portfolio theory fails to account for extreme scenarios involving asset freezes, sanctions, or systemic financial disruption.

Gold serves as portfolio insurance against scenarios that could render traditional foreign exchange reserves inaccessible or worthless. This insurance function justifies allocation percentages that might appear suboptimal under conventional risk-return frameworks.

The Hidden Scale of Chinese Gold Accumulation

Off-Balance Sheet Purchases Through State Entities

Analysis of Chinese gold markets suggests actual accumulation may exceed official PBOC reports through purchases by other government entities. The State Administration of Foreign Exchange and various sovereign wealth funds operate independently of central bank reporting requirements.

These parallel accumulation channels reflect China's sophisticated approach to strategic reserve building while maintaining market stability and avoiding excessive transparency regarding total holdings. Multiple agency coordination allows for larger aggregate purchases without concentrated market impact.

Estimated vs. Reported Acquisition Volumes

Industry analysis suggests Chinese government sector gold purchases may exceed PBOC-reported figures by significant margins. While official reports indicate 225 tonnes acquired in 2024, broader government sector accumulation potentially ranges 20-40% higher when including non-central bank purchases.

This estimation reflects analysis of global gold flows, Chinese import statistics, and domestic production allocation patterns. The methodology involves reconciling supply-demand balances with reported institutional holdings across multiple data sources.

Multiple Agency Coordination in Reserve Building

China's approach involves coordinated purchasing across multiple government entities to achieve strategic objectives while minimising market disruption. This distributed strategy allows for larger aggregate accumulation than would be feasible through single-institution purchasing programmes.

Coordination Benefits:

• Reduced market impact through distributed purchasing

• Enhanced operational security through multiple channels

• Flexibility in timing and volume across different institutions

• Strategic ambiguity regarding total accumulation objectives

The next major ASX story will hit our subscribers first

Market Impact and Price Dynamics of Sustained Central Bank Demand

How Institutional Buying Affects Gold Price Floors

Sustained central bank purchasing creates structural demand that provides price support during market downturns. Unlike private sector investors who may liquidate holdings during financial stress, central banks typically maintain acquisition programmes regardless of short-term price movements.

This institutional demand floor has contributed to gold price resilience during recent market corrections. Central bank purchasing represents approximately 15-20% of annual gold demand, providing significant market stability compared to more volatile private sector flows.

Supply-Demand Imbalances in the Physical Market

Central bank demand concentration in physical delivery markets creates periodic supply constraints that affect pricing dynamics. Unlike paper gold markets with virtually unlimited trading capacity, physical markets face logistical limitations in sourcing, refining, and delivering institutional-grade gold bars.

These constraints become particularly evident during periods of elevated central bank activity, when simultaneous purchasing by multiple institutions can strain available supply chains and processing capacity.

Premium Structures Between Paper and Physical Gold

Sustained institutional demand has contributed to periodic premium expansion between physical gold delivery prices and paper contract settlements. Central banks require actual metal delivery rather than cash settlement, creating distinct supply-demand dynamics in physical markets.

These premiums reflect logistical costs, refining capacity constraints, and storage preparation requirements specific to institutional transactions. Premium volatility provides insights into the intensity of central bank purchasing activity and physical market conditions.

Investment Implications for Gold Market Participants

Long-term Price Support from Institutional Demand

Central bank accumulation provides fundamental support for gold prices over extended periods, reducing downside volatility compared to purely speculative markets. This institutional floor creates more predictable risk-reward profiles for other market participants.

The sustained nature of central bank purchasing reduces the likelihood of major price collapses that might occur in markets dominated by short-term speculation. Institutional demand provides stability that benefits both physical gold investors and mining sector participants.

Mining Sector Beneficiaries of Sustained Central Bank Buying

Gold mining companies benefit from both price stability and volume certainty created by predictable central bank demand. This institutional purchasing provides revenue visibility that supports long-term mining investment and development decisions.

Mining Sector Advantages:

• Reduced price volatility supports project economics

• Predictable demand volumes justify capacity expansion

• Long-term purchasing contracts possible with institutional buyers

• Operational planning benefits from stable demand outlook

Investors interested in exposure to this trend might consider a comprehensive gold mining stocks overview to understand various opportunities within the sector.

Portfolio Allocation Strategies in a Central Bank-Driven Market

Private investors should consider the structural demand changes created by sustained central bank accumulation when developing gold allocation strategies. Traditional portfolio optimisation models may underweight gold when failing to account for institutional demand floors.

The presence of price-insensitive institutional buyers creates different risk-return characteristics than historically existed in gold markets. Portfolio allocation should reflect these evolved dynamics and the reduced probability of sustained bear markets, as outlined in effective gold investment strategy approaches.

Future Outlook: Will China's Gold Buying Streak Continue?

Economic Indicators That Could Influence Policy Changes

Several economic factors could influence the sustainability of China's 17-month gold buying streak. Currency stability pressures, fiscal constraints, and evolving geopolitical relationships may affect accumulation priorities and available resources for reserve building.

Key Monitoring Indicators:

• Chinese foreign exchange reserve levels and composition

• USD-CNY exchange rate stability requirements

• Fiscal policy priorities and government spending allocation

• International trade balance trends affecting reserve accumulation capacity

Potential Saturation Points for Central Bank Reserves

Central banks face practical limitations in gold allocation percentages within overall reserve portfolios. While gold provides valuable diversification and insurance properties, excessive concentration could limit operational flexibility and liquidity management.

International best practices suggest gold allocations typically range 5-15% of total reserves for large economies. China's current allocation remains below these thresholds, suggesting continued accumulation potential before reaching saturation points.

Alternative Reserve Assets and Diversification Strategies

Future Chinese reserve strategy may incorporate additional diversification beyond gold, potentially including strategic commodities, other precious metals, or alternative currency arrangements. This evolution could affect the pace and duration of current gold accumulation programmes.

The development of central bank digital currencies and alternative international payment systems may also influence traditional reserve asset preferences and allocation decisions over time. However, current gold price forecast trends suggest continued institutional demand remains likely.

Frequently Asked Questions About Central Bank Gold Purchases

How Do Central Banks Store and Manage Physical Gold?

Central banks employ specialised storage infrastructure including underground vaults, multi-jurisdictional custody arrangements, and sophisticated security protocols. Major storage locations include Federal Reserve facilities in New York, Bank of England vaults in London, and domestic central bank installations.

Storage management involves regular auditing, insurance arrangements, and coordination with international bullion banks for transaction settlement. Many central banks maintain gold holdings across multiple locations to reduce concentration risk and ensure access during various scenarios.

What Percentage of Global Gold Demand Comes from Central Banks?

Central bank purchases represented approximately 23% of global gold demand in 2024, based on total annual demand of approximately 4,500 tonnes. This percentage has increased significantly from historical averages of 10-15%, reflecting the recent acceleration in institutional accumulation.

This demand share makes central banks the second-largest source of gold demand after jewellery manufacturing, and significantly larger than investment demand from exchange-traded funds or individual investors.

Can Central Bank Buying Patterns Predict Gold Price Movements?

Central bank purchasing patterns provide valuable insights into long-term price trends and support levels, though short-term price prediction remains challenging due to multiple market influences. Sustained institutional buying typically creates price floors and reduces downside volatility over extended periods.

However, gold prices remain subject to various factors including currency movements, interest rate changes, geopolitical events, and speculative trading activity that can override central bank influence in shorter timeframes.

The combination of sustained China central bank gold buying and broader institutional accumulation trends suggests continued structural support for gold markets, though investors should consider multiple factors when making allocation decisions. Central bank demand provides important market stability while reflecting evolving monetary policy priorities in an uncertain global economic environment, as detailed in the latest Gold Demand Trends report.

Please note: This analysis is for informational purposes only and should not be considered investment advice. Gold investments involve risks including price volatility and market fluctuations. Past performance does not guarantee future results. Consult with qualified financial professionals before making investment decisions.

Looking to Capitalise on Central Bank Gold Demand Trends?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. With central banks driving unprecedented institutional demand for gold, begin your 14-day free trial today and secure your market-leading advantage in the evolving precious metals landscape.