July 28, 2026

Central bank gold buying has reached unprecedented levels as monetary authorities worldwide recalibrate their reserve strategies amid escalating geopolitical tensions and persistent inflation concerns. This surge in institutional demand reflects more than routine portfolio diversification—it represents a fundamental shift in how central banks view currency stability, geopolitical risk, and monetary independence. Furthermore, the historic gold surge demonstrates the market's response to these institutional accumulation patterns.

Traditional portfolio theory emphasised correlation analysis and risk-adjusted returns, yet current accumulation patterns suggest deeper strategic considerations beyond conventional asset allocation models. This transformation reflects mounting concerns about dollar dependency, inflation persistence, and geopolitical fragmentation that challenge established monetary frameworks.

Strategic Reserve Diversification Drives Modern Central Banking

The mechanics of central bank gold buying have evolved significantly from historical precedents. Modern reserve managers apply sophisticated portfolio optimisation techniques that extend beyond traditional foreign exchange holdings. These institutions increasingly recognise that gold serves multiple functions: inflation hedging, counterparty risk elimination, and sanctions-resistant value preservation.

Portfolio theory applications in sovereign wealth management emphasise correlation coefficients between gold and conventional reserve assets. Unlike Treasury securities or currency deposits, gold maintains low correlation with dollar-denominated instruments, providing genuine diversification benefits during monetary stress periods. This mathematical relationship becomes particularly valuable when traditional reserve assets face synchronised devaluation pressures.

Central banks employing modern portfolio theory principles calculate risk-adjusted returns across asset classes while considering unique sovereign requirements. Unlike private investors, central banks must balance yield optimisation with strategic considerations including monetary policy independence and crisis response capabilities.

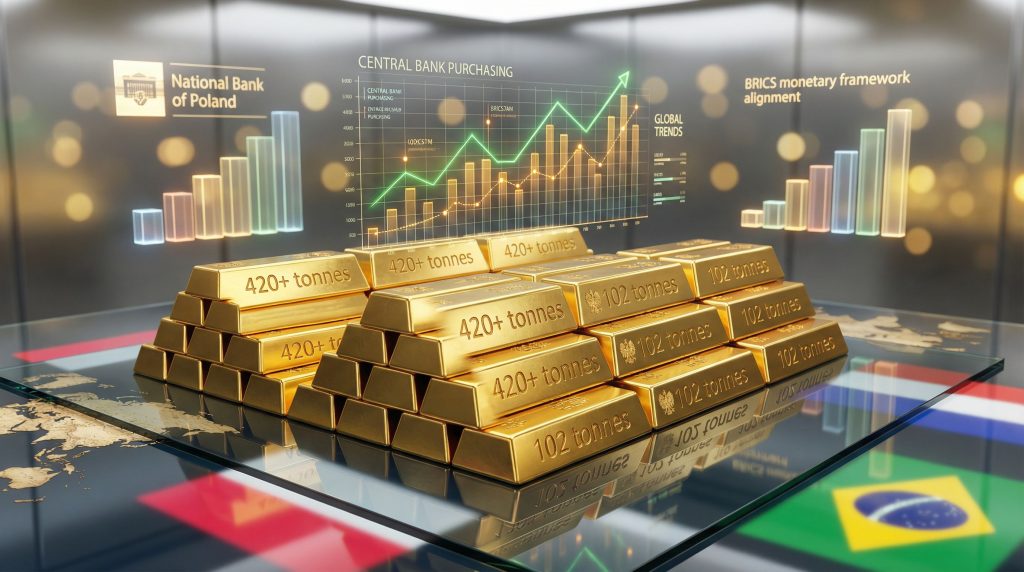

The National Bank of Poland's acquisition of 102 tonnes in 2025 exemplifies strategic diversification beyond pure financial metrics. This accumulation reflects geopolitical hedging strategies where gold provides insurance against potential financial sanctions or currency manipulation. Similarly, the National Bank of Kazakhstan's 57-tonne purchase demonstrates resource-exporting nations' preference for tangible asset backing rather than exclusive reliance on foreign exchange reserves.

Quantitative Easing Impact Mitigation

Unprecedented monetary expansion since 2008 has fundamentally altered central bank reserve strategies. Quantitative easing programmes across major economies created trillions in new currency units, raising legitimate concerns about long-term purchasing power preservation. Consequently, gold accumulation serves as a hedge against the unintended consequences of aggressive monetary stimulus.

The inflation hedging mechanism becomes particularly relevant as central banks navigate between growth support and price stability mandates. Unlike fiat currency reserves, gold maintains intrinsic value independent of any single nation's monetary policy decisions, providing portfolio stability during periods of coordinated global easing.

When big ASX news breaks, our subscribers know first

Emerging Market Leadership in Gold Accumulation

Seven central banks dominated global gold purchases during 2025, with emerging market institutions leading acquisition volumes. The distribution reveals distinct strategic rationales across different economic regions and development stages. Moreover, current gold price forecast models suggest continued upward momentum driven by this institutional demand.

| Central Bank | 2025 Purchases | Strategic Focus |

|---|---|---|

| National Bank of Poland | 102 tonnes | NATO security hedge |

| National Bank of Kazakhstan | 57 tonnes | Resource currency stability |

| Central Bank of Brazil | 43 tonnes | BRICS monetary alignment |

| State Oil Fund of Azerbaijan | 38 tonnes | Petrodollar diversification |

| Central Bank of Turkey | 27 tonnes | Inflation protection |

| People's Bank of China | 27 tonnes | Reserve optimisation |

| Czech National Bank | 20 tonnes | Regional security premium |

The World Gold Council data indicates that twenty-two institutions reported gold reserve increases exceeding one tonne during 2025, demonstrating broad-based institutional interest rather than concentration among a few aggressive purchasers.

Geographic Distribution Analysis

Eastern European central banks exhibit distinct accumulation patterns driven by proximity to geopolitical tensions. The Czech National Bank's 20-tonne acquisition represents proportionally aggressive reserve reallocation for a smaller economy, reflecting regional security concerns that extend beyond traditional monetary policy considerations.

BRICS-aligned institutions pursue gold accumulation as part of broader de-dollarisation strategies. The Central Bank of Brazil's continued purchasing aligns with BRICS monetary initiatives exploring gold-backed alternative currency mechanisms designed to reduce dollar dependency in international settlements.

Resource-exporting nations like Azerbaijan demonstrate petro-state strategies to diversify beyond oil revenues. The State Oil Fund's 38-tonne acquisition reflects recognition of commodity price volatility risks and the strategic value of diversified hard asset reserves.

Geopolitical Risk Amplifies Institutional Demand

Contemporary geopolitical developments create unprecedented safe-haven demand dynamics for institutional gold accumulation. The convergence of multiple conflict zones and economic tensions generates systemic risk premiums that favour non-correlated assets. This environment has contributed to the emergence of record-high gold prices as institutions seek shelter from mounting uncertainties.

Current geopolitical flashpoints as of March 2026 include:

• Ukraine conflict entering its fourth year with sustained military operations

• Iran-US conflict initiated February 28, 2026, creating Middle Eastern instability

• Strait of Hormuz closure disrupting global energy transportation

• Taiwan scenario risks elevated due to potential US military resource constraints

• North Korean provocations through continued missile launch programmes

• Houthi military activities targeting regional shipping and Israeli territory

Sanctions-Resistant Asset Characteristics

The weaponisation of financial systems following Russian asset freezing in 2022 fundamentally altered central bank risk assessment protocols. Traditional reserve assets held as deposits or securities represent counterparty claims that can be frozen during sanctions regimes.

Physical gold holdings eliminate counterparty risk entirely, providing sanctions-proof characteristics that cannot be digitally confiscated or frozen without physical seizure. This distinction has become strategically critical for institutions concerned about potential financial weaponisation, particularly as analysed in comprehensive gold market analyses.

Regional security premiums now factor explicitly into reserve allocation decisions. Eastern European central banks calculate additional value for gold holdings specifically because of geopolitical proximity to potential conflict zones or sanctions-issuing nations.

Energy Crisis Multiplier Effects

The Strait of Hormuz closure demonstrates how geopolitical events create cascading economic effects that reinforce gold's strategic value. The waterway handles 20-30% of seaborne oil globally and one-third of liquefied natural gas, making disruptions systemically significant.

Oil price movements from $67.13 per barrel on February 17 to $103.86 by March 16 represent a 54% increase in less than one month. Such volatility creates immediate commodity price inflation across energy-dependent sectors, supply chain disruption affecting global manufacturing operations, currency stability pressures for energy-importing nations, and increased demand for stores of value independent of specific national currencies.

Economic Indicators Supporting Continued Accumulation

Stagflation indicators provide fundamental support for continued central bank gold buying strategies. The convergence of persistent inflation with slowing growth creates the precise economic environment where gold historically outperforms traditional financial assets. Additionally, gold rally projections suggest this trend will continue throughout 2026.

Labour Market Deterioration Signals

February 2026 employment data revealed concerning trends that support precious metals allocation strategies:

• 92,000 job losses during February, reversing previous growth trends

• Unemployment rate increase to 4.4%, indicating labour market softening

• Manufacturing employment decline of 12,000 positions, reaching 12.57 million (lowest since January 2022)

• Manufacturing contraction in 23 of the last 25 months, representing the longest losing streak since 2008

Inflation Persistence Metrics

Consumer price inflation remained sticky at 0.3% monthly growth in February, with 2.4% year-over-year increases preceding the energy price surge. The Personal Consumption Expenditures index showed 0.3% January growth following 0.4% December increases.

Energy price transmission effects had not yet appeared in February inflation data, suggesting March figures would reflect substantially higher readings from the oil price surge. According to central banks' gold purchasing strategies, 5% oil price increases add approximately 0.1% to developed-market inflation.

Interest Rate Policy Constraints

Treasury yield movements demonstrate how geopolitical tensions constrain Federal Reserve policy flexibility. The 10-year Treasury climbed to 4.25% while the 30-year reached 4.879%, reflecting market assessment of war-related inflation risks.

Federal Reserve officials face the challenging dynamic where anticipated rate cuts to support employment may be constrained by energy-driven inflation pressures. This creates a policy environment where gold's opportunity cost remains relatively attractive compared to nominal yield instruments.

Furthermore, research indicates the approximately $350 per taxpayer fiscal stimulus from recent legislation risks being absorbed by utility and gasoline cost increases rather than generating economic multiplier effects. This dynamic reduces the effectiveness of both fiscal and monetary stimulus measures.

Interest Rate Cycle Implications for Gold Strategy

Opportunity cost analysis in current monetary policy contexts reveals complex dynamics affecting institutional gold demand. Traditional models assume inverse relationships between interest rates and gold prices, yet recent experience demonstrates that structural factors can override cyclical rate movements.

Real Interest Rate Calculations

Real yield analysis requires adjusting nominal Treasury rates for actual inflation expectations. With energy-driven inflation potentially pushing consumer prices significantly higher throughout 2026, real interest rates may remain negative or marginally positive despite nominal rate increases.

Central bank policy rate forecasting models must now incorporate geopolitical risk premiums that weren't relevant during previous cycles. The Federal Reserve's dual mandate of employment and price stability faces contradictory pressures where supporting employment requires easier policy while controlling inflation demands tighter conditions.

Currency Carry Trade Disruptions

Policy divergence between major central banks creates currency volatility that enhances gold's portfolio stabilisation function. When carry trade strategies face disruption from geopolitical events, institutional investors systematically rotate toward non-correlated assets.

Emerging market central bank rate differentials with developed economies create additional complexity for reserve managers. However, higher domestic rates may support local currencies but also increase the relative attractiveness of non-yielding assets like gold during periods of global uncertainty.

De-Dollarisation Architecture Development

Alternative reserve currency systems represent structural changes in global monetary architecture that extend beyond cyclical dollar strength or weakness. BRICS currency basket initiatives and bilateral swap agreements reflect institutional efforts to reduce dollar dependency in international settlements. The gold reserves by country data reveals how nations are repositioning their reserve portfolios.

Payment System Evolution

SWIFT alternative networks have gained institutional adoption following demonstrated risks of financial system weaponisation. Cross-border transaction cost reduction through alternative payment channels reduces dollar demand for settlement purposes.

Central Bank Digital Currency development increasingly incorporates gold backing mechanisms as central banks explore hybrid monetary systems. These initiatives suggest potential structural shifts toward commodity-backed digital currencies that could dramatically alter reserve composition requirements.

Trade Finance Transformation

Bilateral currency agreements between major trading partners increasingly bypass dollar settlements entirely. Gold collateralisation of trade finance provides neutral settlement mechanisms that neither trading partner can unilaterally manipulate or freeze.

Regional monetary union discussions particularly within BRICS economies explicitly consider gold reserve requirements for alternative currency systems. These developments suggest institutional preparation for monetary architecture changes that would fundamentally alter global reserve asset demand patterns.

The next major ASX story will hit our subscribers first

Market Dynamics and Price Discovery Mechanisms

Supply-demand equilibrium shifts reflect the growing influence of institutional accumulation on gold market structure. Annual mine production of approximately 3,000-3,500 tonnes faces increasing competition from central bank purchases that exceeded 1,000 tonnes annually in recent years.

Institutional vs. Private Demand

Central bank purchase timing tends to be less price-sensitive than private investment flows, creating more consistent demand regardless of short-term price volatility. This institutional buying pattern provides price floor support during market corrections.

Exchange-traded fund flows demonstrate correlation with central bank activity, suggesting private investors recognise institutional accumulation as a positive signal for long-term gold allocation strategies.

Over-the-counter transaction patterns indicate that central banks often transact outside public markets, reducing immediate price impact while creating persistent demand pressure over longer time horizons.

Forward Curve Implications

Sustained institutional demand affects gold forward curves by reducing available supply for lending markets. When central banks accumulate and hold physical gold rather than leasing reserves, it constrains supply available for forward transactions.

Market transparency considerations arise when sovereign institutions transact with immunity from typical disclosure requirements. This creates information asymmetries where institutional demand may not be immediately visible to private market participants.

Long-Term Financial System Architecture Changes

Monetary system evolution toward increased gold backing represents potential structural shifts comparable to historical monetary regime changes. Academic discussions of "Bretton Woods III" scenarios reflect growing institutional recognition that current fiat currency systems face sustainability challenges.

Systemic Risk Distribution

Concentration risk in dollar-denominated reserves creates systemic vulnerabilities when geopolitical tensions threaten dollar-based settlement systems. Geographic diversification through gold accumulation spreads systemic risk across multiple asset classes and jurisdictions.

Financial contagion pathways may be modified when central banks hold significant gold reserves that remain valuable independent of any single nation's financial system stability. This could potentially provide more effective crisis response mechanisms during future systemic stress events.

Hybrid System Development Scenarios

Central bank independence under potential gold standard constraints represents a fundamental policy trade-off between monetary flexibility and currency credibility. Hybrid systems that partially back currencies with gold reserves could provide middle-ground approaches.

Digital currency integration with gold backing mechanisms suggests potential technological solutions for combining gold's stability characteristics with modern payment system efficiency requirements.

Investment Strategy Positioning

Portfolio construction implications for continued central bank demand suggest strategic allocation adjustments across multiple asset classes. Gold mining equity exposure provides leveraged participation in sustained institutional demand while physical gold allocation offers direct exposure to reserve asset accumulation trends.

Market Timing Considerations

Central bank purchase seasonality tends to be less pronounced than private investment flows, creating more consistent demand patterns throughout annual cycles. Geopolitical event correlation with institutional buying activity suggests that crisis periods may accelerate rather than delay accumulation programmes.

Economic data release impact on central bank purchasing appears limited compared to private investor reactions, indicating that institutional demand may provide market stability during volatile periods. Policy announcement timing often coincides with increased gold accumulation, suggesting central banks may anticipate monetary policy changes that haven't yet been publicly communicated.

Risk Assessment Framework

Scenario analysis for potential demand disruption includes geopolitical tension resolution, alternative store-of-value asset development, and international monetary system reforms. However, structural drivers appear more persistent than cyclical factors.

Economic recovery impact on risk asset preferences could reduce safe-haven demand, though institutional diversification strategies may continue independent of cyclical economic conditions. In addition, the current trajectory suggests sustained momentum in precious metals markets.

The confluence of persistent inflation, geopolitical fragmentation, and monetary system evolution creates a structural environment supporting continued central bank gold buying. Unlike cyclical precious metals demand driven by investor sentiment, institutional accumulation reflects fundamental changes in how sovereign entities manage reserve portfolios and strategic risk. These structural shifts suggest that gold's role in global monetary architecture may be entering a new phase of increased prominence, with implications extending far beyond traditional commodity market dynamics.

Want to Capitalise on the Next Major Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, converting complex geological announcements into actionable investment insights before the broader market reacts. With central banks driving unprecedented gold demand, positioning yourself ahead of major discoveries through Discovery Alert's dedicated discoveries page could provide the strategic advantage needed to benefit from this institutional momentum—start your 14-day free trial today at discoveryalert.com.au.