June 5, 2026

The Architecture of a Multi-Decade Shift in Sovereign Reserve Strategy

Sovereign wealth management has undergone a quiet but profound transformation over the past decade. Central banks buying gold in April 2026 marked a notable reversal from March's net selling pressure, reflecting a broader, multi-year reassessment of what constitutes a reliable, non-confiscatable reserve asset. This is not a reactionary trend driven by short-term market anxiety. It reflects a fundamental shift in how sovereign institutions view gold in the monetary system amid weaponised financial systems and geopolitical fragmentation.

Understanding this structural shift requires looking beyond any single month's data. The monthly flows of central banks buying gold are best interpreted as chapters within a much longer story, one measured in decades rather than quarters.

When big ASX news breaks, our subscribers know first

April 2026: A Sharp Reversal From March's Selling Pressure

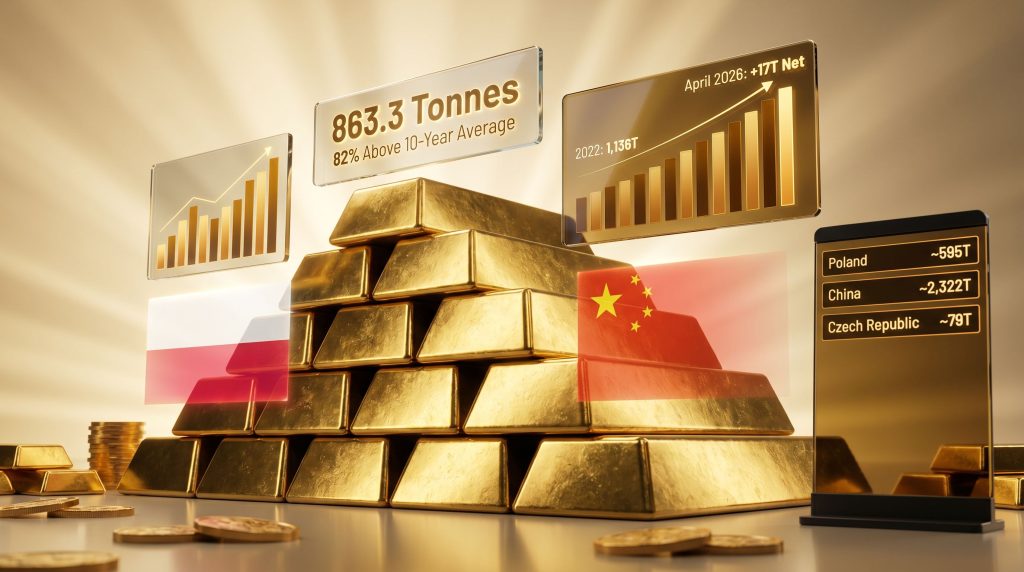

The contrast between March and April 2026 in sovereign gold markets was striking. March saw global central bank gold reserves fall by approximately 27 tonnes, driven primarily by concentrated selling from Turkey and Russia. Within a single month, that dynamic reversed completely. April recorded net central bank gold purchases of 17 tonnes, representing a swing of roughly 44 to 47 tonnes in aggregate positioning.

This kind of month-to-month volatility is not unusual in sovereign gold markets, and it illustrates an important analytical principle: individual monthly data points can be heavily distorted by a small number of large transactions from a handful of institutions. The meaningful signal lies in the trend measured across 12 to 36-month windows, not in any single month's net figure.

Why Single-Month Snapshots Can Mislead

- Monthly flows are sensitive to large bilateral transactions that may reflect temporary liquidity needs rather than strategic policy shifts

- Domestic producer dynamics, particularly among central banks sourcing gold from national mining output, can cause abrupt directional reversals unrelated to reserve strategy

- Seasonal factors, fiscal cycles, and swap maturity schedules all introduce noise into monthly data

- The more durable signal is the multi-year accumulation trajectory, which has remained structurally elevated since 2022

| Year | Net Central Bank Gold Purchases | Context |

|---|---|---|

| 2022 | ~1,136 tonnes | All-time record since 1950 |

| 2023 | ~1,037 tonnes | Second highest on record |

| 2024 | ~1,045 tonnes (est.) | Sustained elevated demand |

| 2025 | ~863 tonnes | Still 82% above 2010-2021 average |

| April 2026 | +17 tonnes (net) | Recovery after March net selling |

Poland: The World's Most Aggressive Central Bank Gold Buyer

No institution better exemplifies the strategic intent behind central bank buying trends than Poland's Narodowy Bank Polski. In April, the NBP added an estimated 14 tonnes to its reserves, building on the 11 tonnes acquired in March. Year-to-date through April, Poland has accumulated approximately 45 tonnes in 2026 alone.

Total Polish gold reserves now stand at approximately 595 tonnes, representing around 30% of the country's total reserve assets. The NBP's stated ambition is to reach a ceiling of 700 tonnes, a target that NBP Governor Adam Glapiński has described as the threshold that would elevate Poland into the ranks of the world's ten largest sovereign gold holders.

The historical context here is remarkable. In 1996, Poland held just 14 tonnes of gold. Today's reserves represent growth of more than 4,100% over three decades.

Poland's Gold Reserve Growth Trajectory:

| Period | Approximate Holdings |

|---|---|

| 1996 | 14 tonnes |

| Pre-2019 | ~100 tonnes |

| End of 2025 | ~581 tonnes |

| April 2026 (est.) | ~595 tonnes |

| Stated target ceiling | 700 tonnes |

Notably, Poland's accumulation has continued despite persistent market speculation that the country might liquidate gold holdings to finance its sharply elevated defence spending commitments. April's purchase data directly contradicts that theory. Poland already holds more gold than the European Central Bank, a symbolic milestone that underscores how aggressively the country has repositioned its reserve architecture over the past decade.

The Security Logic Behind Poland's Gold Strategy

Poland's accumulation strategy carries a dimension that purely financial analysis can miss. Gold is the only reserve asset that carries no counterparty risk and cannot be frozen, seized, or sanctioned by a foreign government or multilateral institution. For a NATO member bordering an active conflict zone, the appeal of holding a meaningful proportion of national reserves in a fully sovereign, non-confiscatable form is not merely financial — it is strategic.

This distinction between financial assets and sovereign assets is central to understanding why Eastern European central banks have disproportionately driven gold accumulation over the past several years. Furthermore, this logic extends beyond Poland, resonating with sovereign institutions across the broader region.

China's Official Reserves and the Off-Balance-Sheet Question

The People's Bank of China recorded its 18th consecutive month of official gold purchases in April, adding approximately 8 tonnes to disclosed holdings. This was the largest single-month increase in officially reported Chinese gold reserves since December 2024, pushing the PBoC's publicly acknowledged holdings to approximately 2,322 tonnes, equivalent to roughly 9% of total foreign reserves.

The word officially carries significant weight here.

Independent research into Chinese monetary gold flows suggests that officially disclosed PBoC figures represent only a portion of actual holdings. Credible analysis of trade and flow data indicates the Chinese central bank may hold more than 5,000 tonnes of monetary gold in Beijing, a figure more than double the publicly reported total. Mainstream financial media has begun acknowledging this reporting discrepancy, signalling growing institutional awareness of the gap between disclosed and actual Chinese gold reserves.

If the 5,000+ tonne estimate is accurate, China's true gold position could rival or exceed that of the United States, which officially reports approximately 8,133 tonnes. The implications for global reserve architecture and the gold price would be substantial if China ever chose to disclose actual holdings in full.

This off-balance-sheet accumulation is believed to occur through mechanisms that fall outside standard IMF gold reserve reporting channels, including purchases routed through state-owned entities and sovereign wealth vehicles that are not classified as central bank holdings under conventional reporting frameworks.

The Czech Republic: 38 Months of Disciplined Accumulation

While Poland and China attract the bulk of market attention, the Czech Republic deserves recognition for one of the most consistently executed sovereign gold accumulation programmes in the world. The Czech National Bank added another 2 tonnes in April, extending an unbroken buying streak to 38 consecutive months.

Current holdings stand at approximately 79 tonnes, with official policy targeting 100 tonnes by 2028. That leaves roughly 21 tonnes of planned purchases over the next two years.

The Czech approach embodies a deliberate, low-volatility accumulation methodology:

- Purchases are made consistently regardless of short-term price movements

- The strategy prioritises reserve diversification over market timing

- The 38-month streak demonstrates institutional commitment that survives changes in market conditions, gold price levels, and geopolitical context

This kind of steady-state accumulation is arguably more strategically significant than large sporadic purchases, as it reflects embedded policy rather than opportunistic positioning.

The Sellers: Russia's Fiscal Drain and Uzbekistan's Supply-Side Dynamics

Russia: Gold Reserves Under Fiscal Siege

Russia recorded net gold sales of approximately 6 tonnes in April, its fourth consecutive month of selling. The drawdown reflects the compounding fiscal pressure of sustained military expenditure against a backdrop of international sanctions that restrict access to conventional external financing.

Russia had previously positioned its gold reserves as a strategic financial buffer, deliberately insulated from Western financial system exposure. The fact that this buffer is now being drawn upon signals that the fiscal cost of ongoing conflict has reached a threshold where even hard-asset reserves are being liquidated.

Uzbekistan: Production Flows, Not Strategy Shifts

Uzbekistan reduced its holdings by approximately 1 tonne in April, reversing a strong accumulation trend that had seen the country add 25 tonnes year-to-date through March. Prior to this reversal, Uzbekistan held approximately 416 tonnes, with gold comprising roughly 88% of total reserve assets — one of the highest gold-to-reserves ratios of any sovereign institution globally.

The reversal is best understood through a supply-side lens rather than a strategic policy change. Central banks that source gold directly from domestic mining production, including Uzbekistan and Kazakhstan, regularly oscillate between buying and selling as domestic output flows vary. These directional reversals are artefacts of production scheduling and concentrate-to-reserve conversion timing rather than changes in long-term reserve strategy.

The next major ASX story will hit our subscribers first

The Geographic Architecture of Sovereign Gold Demand

The regional pattern of central banks buying gold over the past three years reveals a clear structural shift in global reserve architecture. In addition, this geographic concentration offers important context for understanding the durability of long-term demand.

Comparative Regional Central Bank Gold Buying (36-Month Average):

| Region | Average Monthly Net Purchases |

|---|---|

| Asia | ~12 tonnes/month |

| Eastern Europe | ~11 tonnes/month |

| Middle East / Central Asia | Variable (includes net sellers) |

| Western Europe / Americas | Minimal net accumulation |

The concentration of buying in Asia and Eastern Europe is not coincidental. Both regions share a common strategic motivation: reducing exposure to dollar-denominated reserve assets that can be subject to sanctions, asset freezes, or unilateral restrictions by Western governments or multilateral institutions.

The 2022 freezing of Russian sovereign assets held in Western financial systems functioned as a pivotal inflection point. Dozens of sovereign institutions that had previously treated dollar-denominated reserves as unambiguously safe suddenly confronted the reality that those assets could be rendered inaccessible through political decisions. Gold, held physically within a sovereign's own borders, carries no such vulnerability, reinforcing its role as gold as a safe haven in an era of geopolitical uncertainty.

Price Sensitivity vs. Strategic Mandate: How Central Banks Actually Buy Gold

A common misconception in retail gold analysis is that central banks are indifferent to price. The World Gold Council's assessment of 2025 data challenges this view, noting that elevated gold prices contributed to a more measured pace of accumulation, with the annual total falling 21% year-on-year to 863.3 tonnes.

However, the same analysis confirms that long-term strategic interest in gold accumulation remained firmly intact despite this moderation. The nuance is important:

- Price sensitivity affects the pace of central bank accumulation, not the direction

- Central banks are executing multi-year reserve allocation mandates, not attempting to optimise entry prices

- The moderation from 2022 to 2025 levels reflects both price-driven caution and the normalisation of post-2022 emergency diversification programmes

Even at 2025's moderated pace, the 863.3 tonne annual figure represented the fourth-largest expansion of central bank gold reserves on record, sitting 82% above the 2010 to 2021 annual average of 473 tonnes. The structural demand baseline remains historically elevated, and central bank gold demand shows no meaningful signs of abating.

Key Risk Factors and What Investors Should Monitor

Disclaimer: The following observations involve forward-looking analysis and should not be construed as investment advice. Gold markets involve significant risk, and past purchasing patterns by sovereign institutions do not guarantee future price outcomes.

Several variables could meaningfully alter the central bank gold buying trajectory through the remainder of 2026:

- Gold price escalation could intensify the cautious approach dynamic observed in 2025, further moderating the pace of accumulation

- Geopolitical resolution in Eastern Europe could reduce the urgency of reserve diversification for some regional institutions

- IMF reporting standard changes could increase transparency around off-balance-sheet holdings, potentially altering disclosed reserve figures materially

- Fiscal deterioration in sanctioned economies could accelerate Russian gold sales beyond current levels

- Chinese disclosure decisions remain a wildcard with potentially large market implications

Investors tracking sovereign gold demand should monitor the following data points in coming months:

- Monthly World Gold Council reserve data releases for May and June 2026

- Polish NBP reserve updates as holdings approach the 700-tonne policy ceiling

- PBoC official reserve disclosures for any acceleration or deceleration in acknowledged purchases

- The trajectory of Russian gold sales as a proxy for fiscal stress within sanctioned economies

- Turkish central bank positioning, given its outsized influence on recent monthly swings

Frequently Asked Questions: Central Banks Buying Gold in April 2026

How much gold did central banks buy in April 2026?

Net central bank gold purchases totalled approximately 17 tonnes in April 2026, reversing the prior month's net selling of roughly 27 tonnes. Poland led buying at an estimated 14 tonnes, followed by China at approximately 8 tonnes, with Russia and Uzbekistan recording modest offsetting sales.

Why did central bank gold buying slow in 2025?

The World Gold Council attributed the 21% year-on-year moderation in 2025 net purchases, which totalled 863.3 tonnes, partly to elevated gold prices prompting a more measured pace of accumulation. Despite this, 2025 still ranked as the fourth-largest year of central bank gold reserve expansion on record and remained 82% above the 2010 to 2021 annual average. Consequently, the long-term structural case for accumulation remained robust.

Why might China's official gold reserve figure be understated?

China's officially reported 2,322 tonnes reflects only holdings formally disclosed through standard IMF reporting channels. Credible independent analysis of monetary gold flow data suggests actual PBoC holdings may exceed 5,000 tonnes when accounting for accumulation routed through mechanisms outside conventional reserve reporting frameworks. For further context, Brookings Institution research explores how central bank gold holdings function within broader reserve management strategy.

Is Russia selling its gold reserves?

Yes. Russia has been a net gold seller for at least four consecutive months as of April 2026, with monthly sales of approximately 6 tonnes. This reflects the compounding fiscal pressure of sustained military spending and the effects of international economic sanctions on Russia's external financing capacity.

Further analysis on sovereign gold reserve trends and structural demand dynamics is available through the World Gold Council's central bank gold statistics and through ongoing precious metals market commentary at Gold-Eagle.com.

Want to Track the Next Major Gold Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including gold — so subscribers can identify actionable opportunities the moment they emerge. Explore how historic discoveries have generated extraordinary returns for early investors, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.