August 2, 2026

The Quiet Revolution in How Sovereign Nations Store Wealth

For most of the twentieth century, the architecture of global reserve management was relatively predictable. Central banks accumulated U.S. dollars, parked capital in Treasury securities, and treated gold as an inherited relic from the Bretton Woods era. That consensus has fractured. Over the past decade, a structural realignment has unfolded at the sovereign level — one that is reshaping the composition of global reserves in ways that carry profound implications for gold markets, currency dynamics, and the long-term credibility of dollar-denominated assets. Central bank gold demand sits at the heart of this transformation.

Understanding this shift requires looking beyond price charts and into the institutional logic driving reserve managers at the world's most consequential financial institutions. Furthermore, examining central bank buying trends provides essential context for anyone seeking to understand where sovereign wealth is being directed.

When big ASX news breaks, our subscribers know first

Gold Overtakes U.S. Treasuries: The Numbers Behind a Historic Inversion

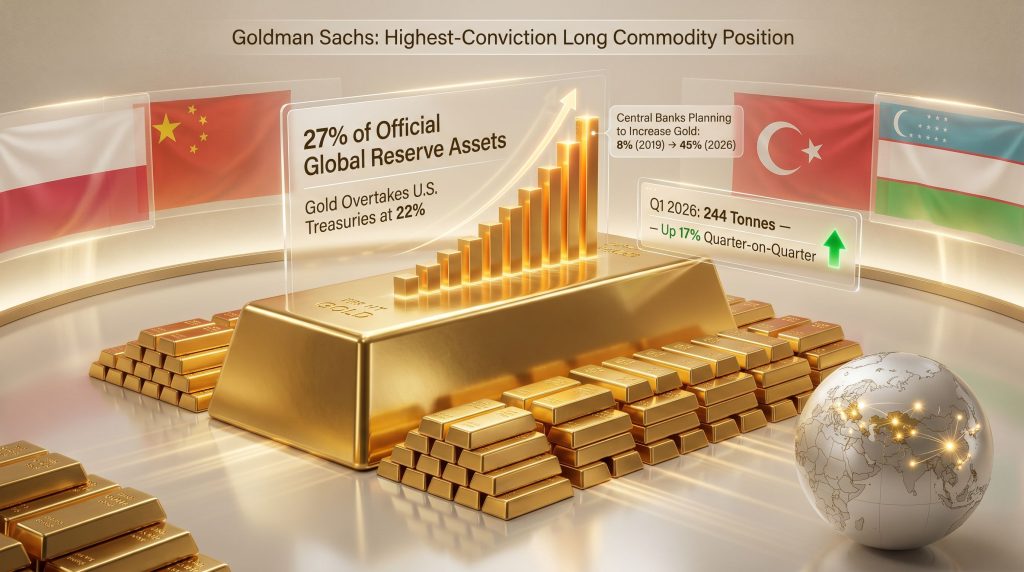

The most striking data point in recent reserve management history is deceptively simple. By the end of 2025, gold represented approximately 27% of official global reserve assets, while U.S. Treasuries had fallen to 22%. This is not a rounding difference. It represents a structural inversion that would have been considered implausible as recently as 2015.

Two forces drove this outcome simultaneously. First, gold's sustained price appreciation substantially increased the mark-to-market value of existing holdings without any additional purchasing required. Second, central banks have been consistent net buyers of gold every single year since 2010, creating cumulative demand pressure that compounded over time.

The scale of recent purchasing activity is difficult to overstate:

| Period | Central Bank Gold Purchases |

|---|---|

| 2022 | 1,000+ tonnes |

| 2023 | 1,000+ tonnes |

| 2024 | 863 tonnes |

| Q1 2026 | 244 tonnes (up 17% quarter-on-quarter) |

Three consecutive years of purchases exceeding 1,000 tonnes annually represents an accumulation cycle with no precedent in the post-Bretton Woods era. The Q1 2026 figure of 244 tonnes, reflecting a 17% increase quarter-on-quarter, suggests institutional conviction has not weakened even as gold prices have reached record highs. According to the World Gold Council's central bank data, this sustained accumulation reflects a fundamental repositioning of sovereign reserves.

Who Is Actually Buying, and How Much?

Emerging Market Central Banks Lead the Charge

The buyer base for central bank gold demand has been dominated by emerging market institutions. Poland, Uzbekistan, Türkiye, and China have been among the most active net purchasers in recent years. Poland's activity in early 2026 was particularly notable, with the National Bank of Poland acquiring 31 tonnes in Q1 2026 alone, placing it at the top of the sovereign buyer ranking for that period.

What is increasingly significant, however, is the broadening of participation beyond developing economies. According to the World Gold Council's Central Bank Gold Reserves Survey 2026, 18% of advanced economy central banks now plan to increase gold holdings over the next 12 months. This participation from wealthier, typically more conservative reserve managers signals a meaningful shift in institutional thinking beyond the emerging world.

The China Underreporting Problem

One of the least appreciated complexities in understanding true central bank gold demand involves the opacity of Chinese reporting. IMF coverage of global central bank gold transactions has declined sharply, from approximately 90% of transactions to roughly one-third in recent years. Analysis of available data suggests that China's actual gold accumulation may be substantially larger than officially disclosed figures, potentially by a factor of up to ten.

This matters enormously for supply-demand modelling. If true sovereign demand is being systematically underreported, the effective demand floor supporting gold prices is likely far higher than headline figures suggest. Investors and analysts relying solely on disclosed purchase data may be materially underestimating structural demand. In addition, the role of central bank gold reserves in underpinning price floors deserves far greater attention from market participants.

Four Structural Reasons Central Banks Are Accumulating Gold

The motivations behind sustained central bank gold demand are not monolithic. They reflect a convergence of distinct strategic imperatives that have intensified simultaneously.

1. Reserve Diversification Away from Single-Currency Dependency

In a multipolar geopolitical environment, overexposure to any single reserve currency carries concentration risk that was once considered acceptable but is now viewed with growing caution. Gold provides a non-correlated asset class that does not depend on the fiscal or monetary policy decisions of any single sovereign issuer.

2. Counterparty Risk Elimination

This is perhaps the most technically important driver. Every other major reserve asset class, including U.S. Treasuries, UK Gilts, and foreign currency deposits, carries inherent counterparty exposure. The issuer could default, restructure, or in extreme circumstances, restrict access. Gold held domestically carries zero counterparty risk. It is not a claim on any institution. It simply exists.

3. The 2022 Sanctions Precedent

The decision by the United States and its allies to freeze Russian sovereign foreign exchange reserves in 2022 fundamentally altered the risk calculus for reserve managers globally. For many central banks, particularly those in jurisdictions with geopolitical complexity, the event demonstrated that assets previously considered safely liquid could be rendered inaccessible through political action.

Jurisdiction matters as much as asset class. Gold stored domestically carries no freeze risk. Gold held in foreign custody does. This distinction is now central to how reserve managers evaluate their portfolios.

The practical response has included accelerated gold repatriation programmes. India, Germany, and most recently France have all taken steps to bring gold reserves back within domestic jurisdiction, reflecting a preference for assets that cannot be subject to third-party custodial intervention. Consequently, the role of gold in the monetary system has been fundamentally reassessed at the highest levels of sovereign finance.

4. Crisis Mobilisation Capability

Gold's universal liquidity profile — recognised simultaneously by sovereign institutions, commercial banks, and retail markets — makes it uniquely deployable during systemic stress events. Historical precedent, including major commodity price shocks, demonstrates that gold can be mobilised when other asset classes face liquidity constraints. This property is particularly valued by reserve managers who must plan for scenarios that conventional financial models struggle to anticipate.

Sentiment Data: A Decade-Long Transformation in Reserve Manager Thinking

Perhaps the most revealing indicator of structural change comes from longitudinal survey data tracking how central bankers themselves think about gold.

| Survey Year | % of Central Banks Planning to Increase Gold Reserves |

|---|---|

| 2019 | 8% |

| 2020 | 20% |

| 2025 | 43% |

| 2026 | 45% |

The trajectory from 8% in 2019 to 45% in 2026 is one of the most dramatic sentiment reversals in the history of reserve management. Critically, only 1% of central banks expect to reduce gold holdings over the next 12 months, according to the World Gold Council's 2026 survey. This near-universal directional alignment is historically unusual.

The shift in how reserve managers categorise gold is equally telling:

| Classification | 2024 | 2026 |

|---|---|---|

| Strategic Asset | 64% | 75% |

| Historical Legacy Asset | 62% | 44% |

The decline in legacy classification from 62% to 44% in just two years indicates that gold is being actively repositioned within institutional frameworks. When 75% of reserve managers explicitly classify gold as a strategic asset rather than an inherited holding, it redefines the demand floor. This is not cyclical allocation driven by price momentum. It is deliberate, forward-looking portfolio construction at the sovereign level.

Furthermore, 89% of reserve managers expect global central bank gold holdings to increase over the next 12 months, a figure that suggests near-universal conviction in the continuation of this accumulation cycle.

Why High Gold Prices Are Not Deterring Sovereign Buyers

A natural question arises: if gold prices are at historic highs, why are central banks still buying aggressively? The answer reveals a fundamental difference between sovereign reserve management and conventional investment logic.

Retail and institutional investors typically optimise for entry price, seeking to acquire assets at attractive valuations relative to expected returns. Central banks, however, operate within entirely different mandates. They are managing reserve adequacy across multi-decade time horizons, with primary objectives around inflation hedging, portfolio diversification, and crisis preparedness rather than short-term return maximisation.

The evidence supports price inelasticity at the sovereign level. Purchase volumes remained robust through 2022, 2023, and 2024 even as gold prices climbed to levels that would have previously triggered profit-taking from conventional investors. This behavioural pattern suggests that the structural drivers of central bank gold demand are sufficiently powerful to override short-term valuation concerns.

Goldman Sachs has maintained gold as its highest-conviction long commodity position, with central bank purchasing identified as the primary structural demand driver. The firm's thesis centres on geoeconomic uncertainty rather than rate differentials as the dominant variable — a framing that aligns with why sovereign demand has remained elevated even during periods of higher real yields. The Brookings Institution's analysis of central bank gold holdings further underscores this structural shift in reserve management thinking.

The next major ASX story will hit our subscribers first

Gold's Reserve Asset Properties: The Framework That Matters

Understanding why gold maintains its appeal requires comparing it systematically against competing reserve asset classes across the dimensions that matter most to reserve managers.

| Asset Class | Liquidity | Counterparty Risk | Freeze Risk | Inflation Hedge |

|---|---|---|---|---|

| Gold (domestic) | High | None | None | Strong |

| U.S. Treasuries | Very High | Low-Medium | Possible | Weak |

| Foreign Currency | High | Medium | Possible | Weak |

| Gilts/Sovereign Bonds | High | Low-Medium | Possible | Weak |

Gold held domestically occupies a genuinely unique position in this matrix. No other commonly held reserve asset combines the absence of counterparty risk, the elimination of freeze risk, and meaningful inflation protection within a single instrument. This combination is not replicable through any financial engineering or synthetic structure. Consequently, central banks influencing gold prices through sustained purchasing have created a dynamic that market participants cannot afford to overlook.

Supply Context and the Structural Demand Floor

Global gold mine production runs at approximately 3,500 tonnes per year. Against this backdrop, central bank net purchasing at 800 to 1,000+ tonnes annually represents a significant and sustained claim on available supply — approximately 25 to 30% of annual mine output flowing directly into sovereign vaults.

This dynamic creates what analysts describe as a structural demand floor: a price support mechanism that operates independently of speculative positioning, ETF flows, or retail sentiment. Even in scenarios where other demand categories contract, sovereign accumulation provides a baseline that constrains downside price risk.

The scenarios under which central bank demand could meaningfully moderate are limited and, based on current survey data, considered unlikely in the near term:

- A fundamental reduction in perceived geopolitical risk and sanctions threat

- A structural strengthening of confidence in dollar-denominated reserve frameworks

- A significant expansion in global mine supply altering the supply-demand balance

- Coordinated multilateral reserve framework reforms reducing gold's strategic premium

None of these conditions appear imminent. The trajectory of reserve manager sentiment, the persistence of geopolitical fragmentation, and the continued underperformance of dollar-denominated assets as inflation hedges all point toward sustained central bank gold demand through 2026 and into 2027.

Frequently Asked Questions: Central Bank Gold Demand

Why are central banks buying so much gold right now?

Central banks are accumulating gold primarily to diversify away from dollar-denominated assets, eliminate counterparty exposure, and hedge against geopolitical and inflationary pressures. The 2022 event demonstrating that sovereign foreign exchange reserves could be frozen materially accelerated this trend across multiple jurisdictions.

Has gold really surpassed U.S. Treasuries as the world's largest reserve asset?

Yes. As of end-2025, gold represented approximately 27% of official global reserve assets compared to 22% for U.S. Treasuries, driven by both price appreciation and sustained net purchasing since 2010.

Which countries are buying the most gold?

Emerging market central banks have led accumulation, with Poland, China, Türkiye, and Uzbekistan among the most active. Poland purchased 31 tonnes in Q1 2026 alone. Advanced economy participation is also increasing, with 18% of institutions in developed markets planning to expand holdings.

Does China buy more gold than it reports?

Analysis of IMF reporting data suggests actual Chinese central bank gold purchases may substantially exceed publicly disclosed figures, potentially by a factor of up to ten. Declining reporting coverage — from approximately 90% to roughly one-third of global transactions — creates significant opacity in understanding true demand levels.

Will central bank gold demand continue through 2026 and beyond?

Survey data indicates 45% of central banks plan to increase gold reserves over the next 12 months, with only 1% planning reductions. Structural drivers including geopolitical risk, reserve diversification mandates, and the erosion of confidence in single-currency reserve frameworks remain firmly in place.

This article contains forward-looking statements, projections, and analysis based on publicly available data and industry survey results. It does not constitute financial or investment advice. Readers should conduct independent research and consult qualified advisers before making investment decisions. Past performance of any asset class does not guarantee future results.

Further context on global gold reserve trends and central bank purchasing behaviour can be found at miningweekly.com, which covers precious metals market developments across major producing and consuming regions.

Want to Stay Ahead of the Next Major Gold Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into clear, actionable insights for both short-term traders and long-term investors. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.