July 23, 2026

The Quiet Revolution in How Nations Store Wealth

For most of the twentieth century, gold sat at the periphery of modern reserve management. After the collapse of the Bretton Woods system in 1971, central banks gradually shifted their attention toward US Treasury bonds, dollar-denominated instruments, and diversified currency baskets. Gold became, in the eyes of many reserve managers, a relic of a fixed-exchange-rate era. That consensus is now fracturing at a pace that few monetary historians would have anticipated.

The World Gold Council's 2026 Central Bank Gold Reserves Survey documents something genuinely remarkable about central bank gold purchases WGC survey findings: a structural doubling in the pace of sovereign gold accumulation, sustained across four consecutive years, driven not by a single crisis but by the convergence of multiple systemic pressures. Understanding what is actually happening inside these institutions, why they are accelerating their buying, and what it means for the global monetary architecture requires looking well beyond the headline numbers.

When big ASX news breaks, our subscribers know first

Record Survey Participation Signals Institutional Consensus

The 2026 WGC survey attracted responses from 76 central bank institutions, the highest participation count in the survey's nine-year history. That figure is not simply an administrative footnote. Higher participation rates in surveys of this kind typically correlate with heightened institutional engagement with the subject matter. When reserve managers at 76 sovereign institutions feel compelled to articulate their gold strategies in writing, it reflects the degree to which gold has re-entered the core of reserve policy discussions globally.

Data collection ran between February 5 and May 19, 2026, a window that overlapped directly with active military escalation in the Middle East. This timing matters analytically. The responses were not shaped by abstract geopolitical theorising but by live conditions in which sovereign risk premiums were genuinely elevated and the limitations of dollar-denominated instruments were being actively debated. The central bank gold reserves data gathered during this period, therefore, carries particular weight.

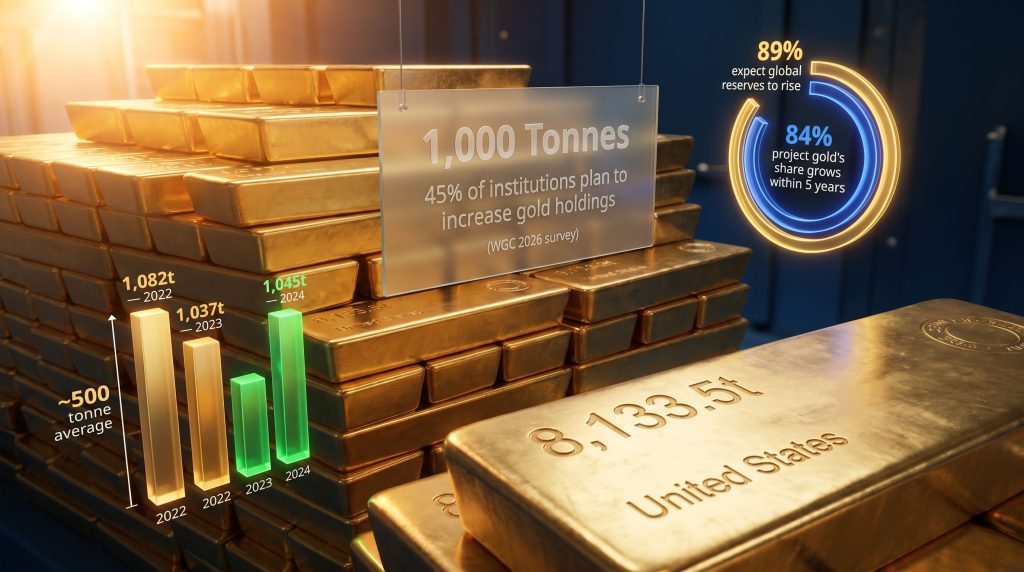

The 1,000-Tonne Threshold: Four Years of Structural Demand

The central empirical finding of the WGC survey is the confirmation that central banks have averaged 1,000 tonnes of gold purchases per year over the past four years. This figure is precisely double the 500-tonne annual average recorded across the preceding decade. The individual yearly totals reinforce the structural rather than cyclical interpretation of this trend:

| Year | Central Bank Gold Purchases |

|---|---|

| Prior Decade Annual Average | ~500 tonnes |

| Four-Year Recent Average | ~1,000 tonnes |

| 2022 | 1,082 tonnes |

| 2023 | 1,037 tonnes |

| 2024 | 1,045 tonnes |

Three consecutive years above 1,000 tonnes eliminates the possibility of a one-off demand spike. Reserve management decisions operate on multi-year planning cycles with substantial institutional inertia. When sovereign institutions sustain this level of acquisition across budget cycles, leadership changes, and shifting market conditions, the conclusion is unambiguous: this is a deliberate, policy-driven reorientation of reserve architecture.

What Is Driving Central Bank Gold Purchases in 2026?

The WGC survey asks reserve managers directly which macro factors are most influential in their allocation decisions. The results across three dominant themes reveal a layered and mutually reinforcing set of pressures. Furthermore, understanding these drivers helps contextualise the central bank gold demand that has reshaped market dynamics since 2022.

Interest Rate Volatility as a Catalyst for Reallocation

92% of survey respondents identified interest rate levels as a relevant factor shaping their reserve allocation decisions. This figure deserves careful interpretation. Conventional thinking holds that gold, as a non-yielding asset, performs poorly in high-rate environments because the opportunity cost of holding it rises. Yet sovereign reserve managers are drawing the opposite conclusion.

The reason lies in the nature of rate volatility itself. When interest rate cycles become unpredictable in both direction and magnitude, the mark-to-market risk of long-duration bond portfolios becomes a more significant concern than the opportunity cost of holding gold. Reserve managers who watched sovereign bond portfolios deteriorate sharply during rapid rate-hiking cycles have adjusted their frameworks accordingly. Gold's lack of yield becomes less relevant when fixed-income instruments are themselves delivering negative real returns or unpredictable capital losses.

Geopolitical Risk at an Unprecedented Premium

An unprecedented 90% of respondents cited gold's historical performance during crisis periods as highly relevant to their current allocation strategy. This is the highest reading ever recorded on this question in the survey's history and reflects the conditions under which the data was collected.

The divergence between institutional categories is analytically significant:

- Advanced economies: 67% identify geopolitical instability as a key allocation driver

- Emerging market and developing economies (EMDEs): 95% identify geopolitical instability as a key driver

This gap is not surprising to those familiar with the differential exposure that EMDE institutions carry. For central banks in geopolitically exposed regions, the weaponisation of dollar-denominated reserve assets through sanctions mechanisms represents an existential risk rather than a theoretical one. The freezing of Russian central bank reserves following the 2022 Ukraine invasion sent a clear signal to reserve managers in dozens of countries: concentration in any single custodial jurisdiction or currency system creates vulnerability. Gold held domestically or in trusted non-aligned vaults does not carry that risk.

Inflation as a Multi-Year Structural Concern

Inflation concerns rank alongside interest rate sensitivity as a top-tier driver of reserve reallocation. The persistence of above-target inflation across major economies throughout 2022 to 2024 has reinforced institutional awareness of gold's purchasing-power preservation characteristics. Reserve managers tasked with maintaining the real value of sovereign wealth over decade-long horizons are recalibrating their frameworks to weight this function more heavily. The compounding effect of simultaneous rate instability, inflationary persistence, and geopolitical fragmentation creates a macro environment that elevates gold's multi-dimensional utility within diversified reserve portfolios.

Forward Intentions: What Reserve Managers Plan to Do Next

The survey's forward-looking data represents some of its most actionable intelligence for analysts monitoring gold market structure. The findings point clearly toward sustained, institutionally committed demand across both near-term and structural timeframes. In addition, these central bank buying trends suggest the pace of accumulation is unlikely to reverse in the near term.

12-Month Outlook: Record Accumulation Intentions

| Reserve Manager Forward Intention | Share of Respondents |

|---|---|

| Expect global central bank gold reserves to increase | 89% |

| Plan to increase own institution's gold holdings | 45% (record high) |

| Expect no change to own holdings | 54% |

| Expect a decrease in own holdings | 1% |

The 45% of institutions planning to increase their own gold reserves over the next 12 months represents the highest proportion ever recorded in the survey's history. This is not passive optimism about gold's investment merits; it reflects active institutional capital allocation decisions already embedded in reserve management frameworks.

Five-Year Structural Reallocation: The Dollar Displacement Thesis

Looking across a five-year horizon, the survey data reveals what may be the most consequential monetary trend of the current decade:

- 84% of reserve managers expect gold to represent a moderately or significantly larger share of global reserve portfolios within five years

- 74% of respondents forecast a declining share of US dollar holdings within global reserves over the same period

These two projections, viewed together, constitute a deliberate multi-year displacement of dollar assets by gold within sovereign balance sheets. The scale of this reallocation, when aggregated across dozens of central banks managing trillions of dollars in reserves, represents a structural demand tailwind for gold that operates largely independently of short-term price movements. Sovereign reserve managers are not momentum traders; they are executing decade-scale portfolio transitions.

How Central Banks Actually Buy Gold: The Operational Mechanics

Most market commentary focuses on the volume of central bank gold purchases without examining the mechanisms through which these acquisitions occur. The 2026 WGC survey provides granular operational detail that is rarely available in public sources.

The Two Primary Acquisition Channels

- 50% of respondents fund gold acquisitions through domestic purchase programmes denominated in local currency

- 38% finance purchases through the liquidation of existing reserve assets, including foreign exchange holdings or other sovereign instruments

The domestic programme model is structurally significant for several reasons. Acquisitions denominated in local currency do not require generating foreign exchange flows, do not create upward pressure on the purchasing institution's currency, and do not trigger the kind of international capital movement visibility that foreign market purchases produce. For EMDE institutions in particular, this mechanism allows substantial reserve accumulation below the radar of international financial markets.

EMDE Domestic Programmes: An Expanding Institutional Infrastructure

The expansion of domestic gold purchase frameworks across emerging markets represents an underappreciated structural development in global gold demand:

- 53% of EMDE central banks already operate a formal domestic gold purchase programme

- A further 12% are actively evaluating the establishment of such a framework

If the institutions currently evaluating domestic programmes proceed to implementation, EMDE domestic buying capacity could expand materially within two to three years. This would represent an additional, relatively price-insensitive demand source entering the market.

Refining Standards and Pricing Within Domestic Frameworks

| Domestic Programme Operational Parameter | EMDE Institutions |

|---|---|

| Refine at LBMA Good Delivery List accredited refinery | 12 (down from 14) |

| Pay international spot price for domestically sourced gold | 8 |

| Secure a discount to international spot price | 4 |

The reduction from 14 to 12 institutions using LBMA Good Delivery standard refining is worth noting. LBMA Good Delivery bars represent the globally accepted standard for wholesale gold settlement, meeting minimum purity thresholds and weight specifications recognised across international markets. A decline in adherence to this standard within domestic programmes could indicate that some institutions are prioritising accumulation speed and domestic supply chain integration over international settlement compatibility, potentially creating a bifurcation between domestically held and internationally tradeable gold stocks.

The pricing divergence within EMDE domestic frameworks, where four institutions secure discounts to the international spot price rather than paying spot, reflects the negotiating leverage that sovereign purchasers sometimes exercise over domestic mining operators. This effectively means some governments are acquiring gold at below-market cost while providing a guaranteed offtake channel to local producers.

Where Is the Gold Being Stored? The Custody Diversification Trend

Current Vaulting Preferences

- Bank of England: cited by 57% of respondents as their primary external vaulting location

- Domestic storage: utilised by 49% of respondents, a figure that has been growing

The Bank of England's dominant position reflects London's historical role as the global hub of the wholesale gold market, where proximity to the LBMA trading infrastructure provides liquidity access that domestically stored gold cannot easily replicate. However, the steady growth in domestic storage reflects a deliberate risk management posture: institutions are reducing dependency on any single custodial jurisdiction while maintaining operationally necessary overseas holdings for liquidity and trading purposes.

The Repatriation Movement in Numbers

Over the past 12 months:

- 9% of institutions increased domestic storage allocations, up from 5% in the prior period

- 10% diversified their overseas storage arrangements beyond existing locations

Looking forward over the next 12 months:

- 7% plan to expand domestic storage capacity

- 9% plan to further diversify overseas vaulting arrangements

The repatriation trend accelerated meaningfully between survey cycles, with domestic storage expansion nearly doubling from 5% to 9% of institutions year-on-year. This trajectory reflects the broader theme of jurisdictional risk reduction that is also visible in reserve currency diversification data.

The next major ASX story will hit our subscribers first

The Global Gold Reserve League Table: Where Sovereign Holdings Stand

Largest Holders as of Q1 2026

| Rank | Country | Gold Reserves |

|---|---|---|

| 1 | United States | 8,133.5 tonnes |

| 2 | Germany | 3,350.3 tonnes |

| 3 | Italy | 2,451.8 tonnes |

| 4 | France | 2,437.0 tonnes |

| 5 | China | 2,313.4 tonnes |

The concentration of reserves among the top ten sovereign holders, who collectively manage approximately 70% of all officially reported global gold stockpiles, reflects historical accumulation patterns rooted in the Bretton Woods era, when gold convertibility made large holdings a functional monetary necessity. The United States' position as the dominant holder by a significant margin partly explains the global reserve system's dollar dependency. Consequently, the role of gold in the monetary system is being actively reassessed by the 74% of survey respondents expecting dollar share to decline.

Net Movement Leaders: Who Bought and Who Sold in 2025

| Country | Net Reserve Change | Direction |

|---|---|---|

| Poland | +101.98 tonnes | Increase |

| Kazakhstan | +56.99 tonnes | Increase |

| Brazil | +42.79 tonnes | Increase |

| China | +26.75 tonnes | Increase |

| Turkey | +26.70 tonnes | Increase |

| Singapore | -26.41 tonnes | Decrease |

| Ghana | -11.93 tonnes | Decrease |

| Russia | -6.22 tonnes | Decrease |

| Germany | -1.28 tonnes | Decrease |

| Mexico | -0.17 tonnes | Marginal Decrease |

Poland's +101.98-tonne expansion stands as the largest single-country increase recorded in 2025 and warrants specific attention. Poland's accumulation strategy is not opportunistic; it reflects a deliberate policy of building sovereign financial resilience in a geographically exposed position. The country has publicly articulated targets of holding gold equivalent to 20% of its total foreign exchange reserves, a benchmark that implies continued substantial purchasing in future years.

Kazakhstan's +56.99 tonnes and Brazil's +42.79 tonnes reflect different but complementary logics. Kazakhstan, as a significant gold producer, is channelling domestic mine output directly into national reserves, reducing foreign exchange dependency while monetising extractive sector output. Brazil's accumulation reflects a broader BRICS-aligned reserve diversification strategy.

Singapore's -26.41-tonne reduction stands as the largest net liquidation in 2025. As a sophisticated reserve manager with well-established active management capabilities, Singapore's reduction likely reflects tactical rebalancing rather than a structural shift away from gold, potentially capturing liquidity for other asset class opportunities at elevated gold price levels.

Active Gold Management: Beyond Passive Storage

An often-overlooked dimension of central bank gold strategy is the growing practice of active reserve management, deploying gold as a return-generating instrument rather than purely as a static store of value.

37% of central bank respondents report practising active management of their gold reserves. The objectives driving these frameworks have shifted meaningfully:

- Enhancing portfolio returns: cited by 85% of active managers

- Risk mitigation: cited by 42% of active managers, up sharply from 22% in 2025

The near-doubling of risk-focused active management objectives in a single year is a notable behavioural shift. Active gold management typically involves mechanisms such as gold lending, where central banks lend physical gold to commercial institutions for a lease rate return, and gold swaps, where gold is exchanged temporarily for currency with an agreement to reverse the transaction. These instruments allow institutions to generate yield from their gold holdings while maintaining long-term reserve exposure.

The rise in risk-mitigation as a stated objective suggests that active management frameworks are increasingly being used not just to enhance returns but to dynamically adjust portfolio risk profiles, using gold's low or negative correlation with other asset classes as a portfolio construction tool rather than simply an insurance position.

The EMDE vs. Advanced Economy Divide: Diverging but Converging

| Strategic Dimension | Advanced Economies | EMDE Central Banks |

|---|---|---|

| Geopolitical instability as key driver | 67% | 95% |

| Domestic purchase programme operational | Lower adoption rate | 53% in place |

| Currently evaluating domestic programme | Not specified | 12% considering |

| Planning to increase own gold holdings | 18% | Significantly higher proportion |

| Crisis performance rated highly relevant | High | Very High |

The 28-percentage-point gap in geopolitical risk sensitivity between advanced and EMDE institutions is one of the most analytically revealing findings in the entire survey. It reflects fundamentally different threat models. Advanced economy central banks operate within multilateral institutional frameworks that provide implicit protections; their dollar-denominated reserves have historically been safe from unilateral seizure. EMDE institutions cannot rely on these protections with the same confidence, creating a structurally higher reservation price for gold's sovereignty-preserving characteristics.

Yet despite the gap in intensity, the direction of travel is consistent across both categories: more gold, more diversification, less dollar concentration. The convergence of strategy, even if at different speeds and from different starting points, reinforces the structural nature of the current demand cycle. Furthermore, central banks influencing gold price formation is becoming an increasingly important dynamic for analysts to monitor.

What This Means for the Gold Market: Price Structure and Supply Dynamics

Official Sector as a Price-Forming Force

A critical development of the past four years is the transition of central bank purchases from a marginal demand category into a primary price-forming variable. When official sector buying consistently absorbs 1,000 tonnes annually, representing roughly 25% of annual global mine production, it creates a structural demand floor that persists through price cycles.

Unlike ETF flows, which are highly price-sensitive and can reverse rapidly, or speculative futures positioning, which oscillates with momentum, sovereign accumulation is inherently long-duration and largely price-insensitive. Reserve managers do not liquidate gold holdings because the spot price declines 10% in a quarter. This demand characteristic introduces asymmetric support into the gold market structure that was largely absent in prior decades.

The Supply Side Constraint

What the WGC survey does not capture directly but which is essential context is the supply-side reality that official sector demand is meeting. Global gold mine production has grown only marginally over the past decade, constrained by declining average ore grades at existing mines, rising development costs, permitting timelines, and the depletion of high-grade near-surface deposits. The combination of structurally elevated demand from sovereign institutions and constrained supply growth creates a fundamental market dynamic that supports sustained price appreciation over multi-year horizons.

Analytical Limitations: What the Survey Cannot Tell Us

Intellectual honesty requires acknowledging the boundaries of survey-based analysis. According to Reuters reporting on the WGC survey findings, stated intentions do not always translate directly into confirmed transactions, and several important caveats apply:

- Survey data captures stated intentions at a specific moment, not confirmed transaction commitments

- Geopolitical developments, gold price levels, and domestic political changes can alter actual purchase execution significantly

- The 1% of institutions expecting reserve reductions serves as a reminder that the dominant accumulation thesis is not universal

- Intra-year tactical adjustments are not captured by annual survey snapshots

- Reporting of gold reserve levels by some central banks, particularly China, involves acknowledged transparency limitations

The World Gold Council's research indicates that central banks continue to recognise gold's portfolio benefits and that demand from the official sector is likely to remain robust for the foreseeable future. This institutional commitment, sustained across multiple years and diverse geopolitical contexts, represents one of the most durable demand foundations the gold market has seen in modern monetary history.

Frequently Asked Questions: Central Bank Gold Purchases and the WGC Survey

What is the WGC Central Bank Gold Reserves Survey?

The World Gold Council's annual survey gathers responses from reserve managers at central banks globally to understand gold holding strategies, purchase intentions, and reserve composition views. The 2026 edition received responses from 76 institutions, the highest participation in the survey's nine-year history.

How much gold are central banks buying annually through 2026?

Central bank gold purchases WGC survey data confirms an average of 1,000 tonnes per year over the past four years, precisely double the 500-tonne average of the preceding decade, with individual years reaching 1,082 tonnes in 2022, 1,037 tonnes in 2023, and 1,045 tonnes in 2024.

What are the primary drivers of central bank gold purchases?

The three dominant drivers identified in the WGC survey are interest rate volatility (92% of respondents), gold's historical crisis performance (90%), and inflation concerns. For EMDE institutions specifically, geopolitical instability is cited by 95% as a key driver.

Which country holds the most gold as of 2026?

The United States leads with 8,133.5 tonnes, followed by Germany at 3,350.3 tonnes, Italy at 2,451.8 tonnes, France at 2,437.0 tonnes, and China at 2,313.4 tonnes.

Which country increased its gold reserves the most in 2025?

Poland recorded the largest single-country expansion, adding 101.98 tonnes to its sovereign gold holdings in 2025, followed by Kazakhstan at +56.99 tonnes and Brazil at +42.79 tonnes.

Are central banks moving gold to domestic storage?

Yes. 9% of institutions increased domestic storage allocations over the past 12 months, up from 5% in the prior period, while 10% diversified their overseas vaulting arrangements.

Key Takeaways: The 2026 WGC Central Bank Gold Survey

- Central bank gold accumulation has structurally doubled, averaging 1,000 tonnes annually over four years versus approximately 500 tonnes in the prior decade

- 45% of institutions plan to increase their own gold holdings in the next 12 months, a record high in the survey's nine-year history

- 84% of reserve managers expect gold's share of global reserves to rise within five years; 74% expect the dollar's share to fall

- Geopolitical risk is the dominant driver in EMDE markets (95%), while interest rate sensitivity (92%) is the universally top-ranked factor across all institution types

- 53% of EMDE central banks operate formal domestic gold purchase programmes, with 12% more actively evaluating their establishment

- Storage diversification is accelerating, with domestic storage expansion nearly doubling year-on-year and overseas vaulting diversification growing in parallel

- Active gold management objectives are shifting: risk mitigation as a driver nearly doubled from 22% to 42% in a single year

- The official sector has evolved from a passive reserve holder into an active, price-forming participant in the global gold market, absorbing roughly one quarter of annual mine supply

This article is intended for informational purposes only and does not constitute financial or investment advice. All data referenced is sourced from the World Gold Council's 2026 Central Bank Gold Reserves Survey and associated institutional reporting. Readers should conduct their own research and consult qualified financial advisers before making any investment decisions. Survey data reflects stated institutional intentions at a specific point in time and does not guarantee future reserve management behaviour.

Want to Know When the Next Major Gold Discovery Hits the ASX?

While central banks quietly accumulate thousands of tonnes of gold, individual investors can position ahead of the market by acting on significant ASX gold discoveries the moment they are announced — Discovery Alert's proprietary Discovery IQ model scans every ASX announcement in real time, delivering actionable alerts directly to subscribers. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to secure a genuine market-leading edge.