May 20, 2026

Chile copper projects 2026 are positioned to transform global mining markets as electrification accelerates across industries and renewable energy deployment scales exponentially. These macroeconomic forces create unique supply-demand dynamics that differ fundamentally from traditional commodity cycles. Understanding how major copper-producing regions respond to these pressures provides crucial insights into future market positioning and investment opportunities through the remainder of this decade.

Understanding Chile's Strategic Position in Global Copper Supply Chains

Chile's dominance in global copper markets stems from geological advantages that remain difficult to replicate elsewhere. The nation accounts for approximately 27-28% of global refined copper production, maintaining its position as the world's largest producer with output reaching 5.3 million tonnes in 2023. This compares to Peru's 2.3 million tonnes and China's 1.0 million tonnes, highlighting Chile's substantial market leadership.

Furthermore, the global copper supply forecast indicates Chile's strategic importance in meeting rising demand from energy transition technologies and infrastructure development.

Why Chile Remains the World's Dominant Copper Producer

The Atacama Desert region contains some of the world's highest-grade copper deposits with inherently lower extraction costs. Major operations including Escondida, Collahuasi, Los Pelambres, and Chuquicamata benefit from porphyry copper geology that maintains economic viability even during commodity downturns. These shallow, high-grade ore bodies combined with established infrastructure create competitive advantages that persist across market cycles.

Chile's geological endowment provides structural cost benefits that competitors struggle to match. The country holds approximately 160 million tonnes in proven reserves, representing roughly 36 years of production at current rates. Despite modest grade decline from historical averages of 0.9-1.1% copper content to current levels of 0.65-0.85%, operational costs remain globally competitive at approximately $1.50-$2.00 per pound of copper produced in the largest operations.

The Escondida Mine, operated by BHP as the world's largest copper operation, demonstrates this competitive positioning by producing approximately 1.3 million tonnes annually while successfully integrating advanced desalination technology to address water scarcity challenges. Similarly, Chuquicamata Mine under Codelco management continues its underground conversion project to extend operational life beyond 2040, representing substantial investment in long-term resource management.

The Macroeconomic Drivers Behind 2026 Investment Surge

Global copper demand trajectories are being reshaped by convergent forces that extend far beyond traditional industrial consumption patterns. The International Copper Study Group projects copper demand reaching 25.4 million tonnes in 2025, with medium-term forecasts suggesting continued growth through 2030. Under accelerated decarbonization scenarios, the World Bank's Climate-Smart Mining initiative projects demand could reach 28-30 million tonnes annually by 2030-2035.

Electric vehicle adoption represents a particularly significant demand driver, with global EV sales reaching 14 million vehicles in 2023, representing 18% of total vehicle sales compared to just 10% in 2020. Each battery electric vehicle requires approximately 40-50 kg of copper in electrical systems, wiring, and battery components, compared to only 10-15 kg in conventional internal combustion vehicles. The International Energy Agency projects EV market share could reach 60% of new car sales globally by 2035 under stated policy scenarios.

Renewable energy infrastructure deployment adds another layer of copper intensity to global demand. Wind turbine installations require approximately 4-5 tonnes of copper per 2-3 MW unit, while solar photovoltaic systems need roughly 7-8 kg of copper per kilowatt of capacity. Global renewable energy capacity additions reached 295 gigawatts in 2023, a 50% increase from 2020 levels, with grid modernization investments estimated at $1.5-2.0 trillion through 2035 to support renewable integration.

The copper intensity of energy transition infrastructure significantly exceeds traditional applications. Consequently, the critical minerals energy transition demonstrates copper requirements of 2.5-3.5 kg per megawatt for wind and 3.0-4.0 kg per megawatt for solar farms with integrated storage, compared to 1.2-1.5 kg per megawatt for conventional electrical grid infrastructure.

When big ASX news breaks, our subscribers know first

What Makes 2026 a Pivotal Year for Chilean Copper Development?

Investment climate dynamics are positioning 2026 as a critical milestone for Chile copper projects 2026 initiatives across the country's mining sector. The convergence of capital deployment, operational readiness, and market conditions creates unique opportunities for production capacity expansion during a period of elevated commodity prices and structural demand growth.

Investment Climate Analysis: Capital Deployment Across Chilean Projects

Chilean mining sector capital expenditures averaged $3.8-4.2 billion annually during 2020-2023, with major multinational operators collectively announcing $8-12 billion in medium-term copper project investment between 2023-2025. This investment cycle represents moderate growth compared to the 2010-2015 period, which saw approximately $25-30 billion cumulative investment following the 2008 financial crisis recovery.

The strategic focus on Chile copper projects 2026 reflects risk-adjusted capital allocation, with projects achieving production milestones in 2026 representing lower execution risk compared to longer-duration greenfield developments. This approach provides more predictable returns for institutional investors while supporting Chile's objective of maintaining global market share during the energy transition.

Furthermore, implementing effective copper investment strategies becomes crucial for portfolio optimisation across different project categories and risk profiles:

• Smelting and processing infrastructure receives 28-30% of total allocation, targeting 8-12 year payback periods with stable cash flows

• Brownfield mine expansions capture 45-50% of investment, targeting 5-7 year payback periods with higher operational certainty

• Greenfield operations account for 15-20% of capital, targeting 7-10 year payback periods with elevated geological and execution risk

Geopolitical Factors Accelerating Project Timelines

Supply chain diversification imperatives are fundamentally altering investment timing for Chile copper projects 2026. Following COVID-19 disruptions and rising geopolitical tensions, OECD countries implemented substantial nearshoring and friend-shoring policies. The U.S. CHIPS and Science Act (2022) and European Critical Raw Materials Act (2023) explicitly prioritise copper supply diversification away from single-source dependencies.

Strategic mineral security frameworks elevate Chilean copper to national defence importance. The U.S. Department of Defense classified copper as a critical material in December 2023, while the EU identified copper as requiring secure supply chains with Latin American production cited as strategically preferable to China-dependent sourcing. China controls approximately 60-65% of global copper refining capacity, creating supply chain vulnerabilities that Western governments actively seek to address.

Trade policy evolution provides additional acceleration factors. USMCA provisions incentivise North American mineral sourcing with preferential tariff treatment, while Chilean copper exported to North America faces fewer barriers than Chinese or Russian alternatives. The U.S.-Chile Critical Minerals Cooperation agreement, formalised in 2023, specifically targets acceleration of Chilean copper, lithium, and molybdenum projects through coordinated development support.

Which Projects Will Define Chile's Production Capacity Through 2030?

Production capacity expansion across Chile's copper sector involves multiple project categories with distinct timelines, risk profiles, and capital requirements. Understanding these developments provides insight into how Chilean production will evolve through the remainder of this decade.

Tier-1 Development Projects Reaching Critical Milestones

| Project Category | Investment Value | Expected Production Impact | Timeline to First Copper |

|---|---|---|---|

| Smelting Infrastructure | $4.2B | +30% domestic processing | 2032-2033 |

| Mine Expansions | $6.8B | +400,000 tonnes annually | 2026-2028 |

| Greenfield Operations | $3.8B | +250,000 tonnes annually | 2027-2029 |

Smelting infrastructure development represents a strategic shift toward domestic value-added processing. The Codelco-Glencore partnership, formalised in 2023, created a joint venture targeting 1.5 million tonnes annual smelting capacity through combined existing operations and expansion programmes. Capital expenditure for these improvements reaches $1.8-2.1 billion through 2028, with production ramp beginning in 2027-2029.

Environmental compliance upgrades within smelting operations require $400-600 million for particulate filters and SO2 capture systems. These investments ensure long-term operational sustainability while meeting increasingly stringent environmental standards across the Chilean mining sector.

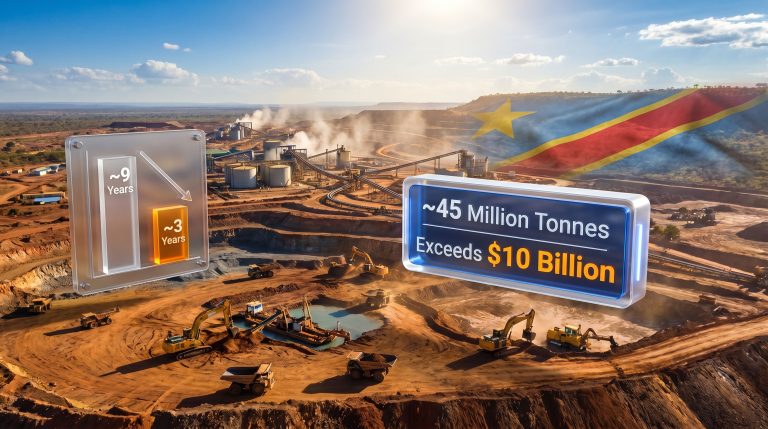

Major mine expansion projects include several significant operations targeting Chile copper projects 2026 milestones:

• Los Pelambres (Antofagasta PLC): $2.9 billion capital programme targeting +170,000 tonnes by 2026-2027

• Escondida (BHP): Brownfield expansion targeting +150,000 tonnes through processing capacity enhancement, $1.7 billion capital with 2026-2028 production ramp

• Chuquicamata (Codelco): Underground transition and capacity optimisation, $1.2 billion with production ramp during 2026-2028

Technology Integration and Operational Efficiency Gains

Autonomous mining systems deployment across major Chilean operations represents significant technological advancement. These systems improve productivity while reducing operational costs by 15-20% through optimised equipment utilisation and reduced labour requirements in hazardous environments.

Water recycling technologies address critical resource scarcity in Chile's arid mining regions. Advanced desalination integration, particularly at coastal operations like Escondida, enables sustained production expansion despite regional water constraints. These systems require substantial capital investment but provide long-term operational security in water-stressed environments.

Digital supply chain optimisation reduces delivery timeframes and improves inventory management across the Chilean copper sector. Integration of predictive maintenance systems and real-time operational monitoring enhances equipment availability while minimising unplanned downtime.

How Will Production Scaling Impact Global Copper Markets?

Chilean production capacity expansion occurs within broader global supply-demand dynamics that will determine market equilibrium through 2030. Understanding these interactions provides insight into pricing trends and market share evolution across major copper-producing regions.

Supply-Demand Equilibrium Projections for 2026-2030

Chile's contribution to global copper markets extends beyond absolute production volumes to include processing capacity and supply chain reliability. The country's expansion programmes target closure of projected supply deficits that could reach 4.7 million tonnes under accelerated electrification scenarios.

Price stability implications of increased Chilean capacity depend on concurrent demand growth from renewable energy and electric vehicle sectors. Base case scenarios project copper trading at $8,500-9,500 per tonne, while sustained prices above $10,000 per tonne remain possible under bull market conditions driven by supply constraints elsewhere.

Market share redistribution among global copper producers reflects Chile's strategic positioning. While other major producers face resource depletion, infrastructure constraints, or geopolitical challenges, Chilean operations maintain cost competitiveness and operational stability that supports market share preservation or expansion.

Processing Capacity Revolution: The Smelting Infrastructure Build-Out

Domestic value-add strategies through smelting capacity expansion reduce Chile's dependence on concentrate exports while capturing additional margins through refined copper production. Moreover, the Codelco copper strategy specifically targets 1.5 million tonnes annual capacity, representing approximately 30% of current Chilean production.

Environmental compliance standards drive technology adoption across Chilean smelting operations. Advanced emissions control systems and waste heat recovery improve operational efficiency while meeting increasingly stringent environmental requirements. These investments total $400-600 million within broader infrastructure development programmes.

"Processing capacity expansion represents a fundamental shift in Chilean copper strategy, moving from concentrate export dependency toward domestic refining that captures additional value while supporting long-term competitiveness in global markets."

What Are the Investment Implications for Global Mining Portfolios?

Chilean copper development presents distinct investment considerations across different project categories and risk profiles. Understanding these dynamics helps institutional investors optimise portfolio allocation while managing execution and commodity price risks.

Capital Allocation Strategies Across Project Risk Profiles

Chile copper projects 2026 advancing to production represent lower execution risk compared to greenfield developments, offering more predictable returns for institutional portfolios. Projects with established infrastructure, proven reserves, and experienced operational teams provide risk-adjusted returns that appeal to conservative mining investment strategies.

Operational cash flow projections vary significantly across commodity price scenarios:

• Base case ($8,500-9,500/tonne): Most Chilean operations generate positive free cash flow with internal rates of return exceeding 15-20%

• Bull case (sustained above $10,000/tonne): Enhanced returns support accelerated capital investment and debt reduction

• Bear case ($7,000-8,000/tonne): Lower-cost Chilean operations maintain profitability while higher-cost global competitors face margin pressure

ESG Compliance and Sustainable Mining Practices

Water management innovations address critical resource constraints in Chile's arid mining regions. Advanced recycling systems and desalination integration enable production expansion while minimising environmental impact. These technologies require substantial upfront investment but provide long-term operational sustainability.

Carbon footprint reduction through renewable energy integration improves ESG profiles while reducing operational costs. Chilean mining operations increasingly integrate solar and wind power to offset traditional energy consumption, particularly in processing and transportation activities.

Community engagement frameworks support long-term operational stability through structured consultation processes with indigenous communities and local populations. These programmes require ongoing investment in social development, education, and healthcare infrastructure but are essential for maintaining social licence to operate.

Operational Cash Flow Projections Under Different Commodity Price Scenarios

Investment returns across Chilean copper operations demonstrate sensitivity to global commodity price movements while maintaining superior cost positions relative to many international competitors. Chilean operations typically maintain cash costs between $1.50-2.50 per pound, providing substantial margins even during commodity downturns.

Revenue visibility improves through long-term supply agreements with strategic partners, particularly in Asia and North America. These contracts provide price stability while ensuring market access during periods of supply chain disruption or trade policy uncertainty.

How Do Infrastructure Developments Support Long-Term Growth?

Infrastructure investments across transportation, logistics, and human capital development provide foundational support for Chilean copper sector expansion. These investments extend beyond individual mining operations to encompass regional economic development and export capacity enhancement.

Transportation and Logistics Network Enhancements

Port capacity expansions in Antofagasta and Valparaíso regions directly support increased mineral exports to strategic partners including the United States, European Union, Japan, and South Korea. These infrastructure improvements reduce transportation costs while improving delivery reliability for international customers.

Rail infrastructure improvements optimise transportation efficiency between mining operations and export facilities. Advanced logistics coordination reduces inventory costs while minimising environmental impact through consolidated transportation networks.

Digital supply chain optimisation integrates predictive analytics and real-time tracking across Chilean copper logistics networks. These systems improve delivery timeframes while reducing administrative costs and enhancing customer service quality.

Workforce Development and Technical Expertise Scaling

Engineering talent acquisition from international markets addresses skill shortages in specialised mining technologies. Chilean operations increasingly compete globally for experienced professionals in autonomous systems, environmental management, and advanced metallurgy.

Local technical training programmes support operational expansion while providing career development opportunities for regional populations. These initiatives include partnerships with universities and technical institutes to develop mining-specific curricula and certification programmes.

Automation impact on employment patterns requires strategic workforce planning to balance technological advancement with employment objectives. Chilean mining operations implement gradual automation deployment while providing retraining opportunities for displaced workers.

The next major ASX story will hit our subscribers first

What Risks Could Derail the 2026 Production Targets?

Multiple risk factors could potentially impact Chile copper projects 2026 timelines and production targets. Understanding these challenges enables better risk management and contingency planning across Chilean mining operations.

Regulatory and Environmental Compliance Challenges

Water usage permits in drought-affected regions present ongoing operational challenges for Chilean copper producers. Competition for limited water resources between mining, agriculture, and municipal users requires careful regulatory navigation and substantial investment in water recycling technologies.

Environmental impact assessments for expansion projects face increasingly stringent requirements that can extend approval timelines. Climate change considerations, biodiversity protection, and waste management protocols add complexity to permitting processes while requiring additional capital investment in environmental mitigation measures.

Indigenous community consultation requirements mandate structured engagement processes that can influence project timelines and operational parameters. These consultations, while essential for social licence maintenance, introduce potential delays and additional compliance costs that must be factored into project planning.

Technical and Operational Risk Factors

Ore grade decline mitigation strategies require ongoing investment in exploration, advanced processing technologies, and operational optimisation. While Chilean copper deposits maintain superior grades relative to many international competitors, gradual decline trends necessitate productivity improvements to maintain cost competitiveness.

Equipment availability constraints during global supply chain disruptions can impact project timelines and operational efficiency. Specialised mining equipment often requires extended lead times, making inventory management and supplier relationship maintenance critical for operational continuity.

Skilled labour shortages in remote mining locations present ongoing recruitment and retention challenges. Competition for experienced mining professionals, particularly in emerging technologies like autonomous systems and environmental management, requires competitive compensation and career development programmes.

Market Volatility and External Economic Pressures

Currency fluctuation impacts on project economics require active financial risk management across Chilean mining operations. The Chilean peso's relationship to the U.S. dollar affects both operational costs and revenue realisation, necessitating hedging strategies and financial planning flexibility.

Global recession scenarios affecting demand projections could alter the viability of expansion projects and impact commodity pricing. Economic downturns in major consuming regions (China, Europe, North America) directly influence copper demand and pricing dynamics.

Competition from alternative copper sources and recycling presents long-term market share challenges. Technological advancement in copper recycling and development of new production regions could potentially reduce Chilean market share despite production expansion efforts.

Why Chile's Copper Strategy Matters for Global Energy Transition

Chilean copper production plays a fundamental role in enabling global decarbonisation efforts through renewable energy infrastructure and electric vehicle deployment. Understanding this relationship provides insight into the strategic importance of Chilean mining sector development.

Critical Mineral Security for Renewable Energy Infrastructure

Copper intensity requirements for wind and solar installations create structural demand growth that extends well beyond traditional industrial applications. Wind installations require 4-5 tonnes of copper per 2-3 MW unit, while solar farms with integrated storage systems need 3.0-4.0 kg per megawatt of capacity.

Grid modernisation demands driven by renewable energy integration require substantial copper inputs for transmission infrastructure, smart grid technologies, and energy storage systems. Global grid investments estimated at $1.5-2.0 trillion through 2035 will consume significant copper volumes while requiring supply chain reliability that Chilean operations can provide.

Energy storage technology copper content analysis reveals increasing intensity requirements as battery systems scale and grid integration expands. Advanced battery systems, grid-scale storage, and electric vehicle charging infrastructure all require substantial copper inputs that must be sourced from reliable, environmentally responsible suppliers.

Strategic Partnerships and International Investment Flows

Asian market integration through long-term supply agreements provides revenue stability while supporting regional energy transition objectives. Chinese, Japanese, and South Korean copper consumption continues growing as these nations expand renewable energy capacity and electric vehicle adoption.

European Union critical raw materials partnership opportunities emerge through trade cooperation and investment frameworks. EU strategic autonomy objectives prioritise diversified supply chains that include Chilean copper as an alternative to Chinese-controlled processing capacity.

North American nearshoring trends benefit Chilean exports through preferential trade treatment and strategic partnership development. In addition, implementing a comprehensive copper growth strategy and bilateral cooperation agreements improve market access while supporting North American supply chain resilience objectives.

Positioning for the Next Decade of Copper Market Evolution

Chilean copper sector development through 2030 will significantly influence global mining markets, renewable energy deployment, and critical mineral security across major economies. Success in executing Chile copper projects 2026 will determine whether global copper supply can meet accelerating demand from electrification and renewable energy deployment.

Key Performance Indicators to Monitor Through 2026

Monthly production ramp-up rates across major Chilean projects provide early indicators of execution success and potential supply contributions. Projects achieving production milestones ahead of schedule could provide additional market supply during periods of tight global balance.

Capital expenditure efficiency metrics versus global benchmarks demonstrate Chilean operational competitiveness and potential for continued investment attraction. Superior capital productivity supports additional project development while maintaining cost advantages over international competitors.

Market share evolution in key consuming regions reflects Chilean copper's competitive positioning and strategic relationship development. Maintaining or expanding market share in Asia, Europe, and North America validates Chile's role in global supply chain diversification efforts.

Long-Term Competitive Advantages and Sustainability Factors

Geological resource quality maintaining cost competitiveness ensures Chilean copper operations remain profitable across commodity cycles. Superior ore grades, established infrastructure, and operational expertise provide structural advantages that support long-term market positioning.

Technological innovation adoption supporting productivity gains enables Chilean operations to offset grade decline while improving environmental performance. Autonomous systems, advanced processing technologies, and digital optimisation contribute to sustained competitiveness.

Environmental stewardship enhancing social licence to operate becomes increasingly important for long-term operational sustainability. Water management innovations, carbon footprint reduction, and community engagement programmes support continued operational approval while meeting evolving ESG requirements.

For instance, Marimaca Copper's critical environmental approval demonstrates how successful permitting processes enable project advancement while maintaining environmental standards.

This analysis is based on publicly available information and industry research as of late 2024. Mining investments involve substantial risks including commodity price volatility, operational challenges, and regulatory changes. Readers should conduct independent due diligence and consult qualified professionals before making investment decisions.

Looking to Capitalise on Chile's Copper Market Expansion?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant copper discoveries across the ASX, empowering investors to identify actionable opportunities ahead of the broader market. Explore historic examples of exceptional returns from major mineral discoveries on Discovery Alert's dedicated discoveries page and begin your 30-day free trial today to position yourself ahead of the market.