July 17, 2026

When Production Meets Its Ceiling: Understanding the China Aluminium Output Surge

Global commodity markets rarely face moments where a single nation's industrial decisions reshape pricing benchmarks, trade flows, and supply chain logic simultaneously. Yet that is precisely the situation unfolding in the aluminium sector today. China's role as the world's dominant producer has long been understood in aggregate terms, but the specific mechanics of how Chinese smelters respond to profit signals, geopolitical shocks, and energy availability reveal a far more dynamic system than simple output statistics suggest. The ongoing China aluminium output surge is not merely a production story. It is a stress test of capacity ceilings, demand fundamentals, and market equilibrium.

When big ASX news breaks, our subscribers know first

The Anatomy of Record Daily Production

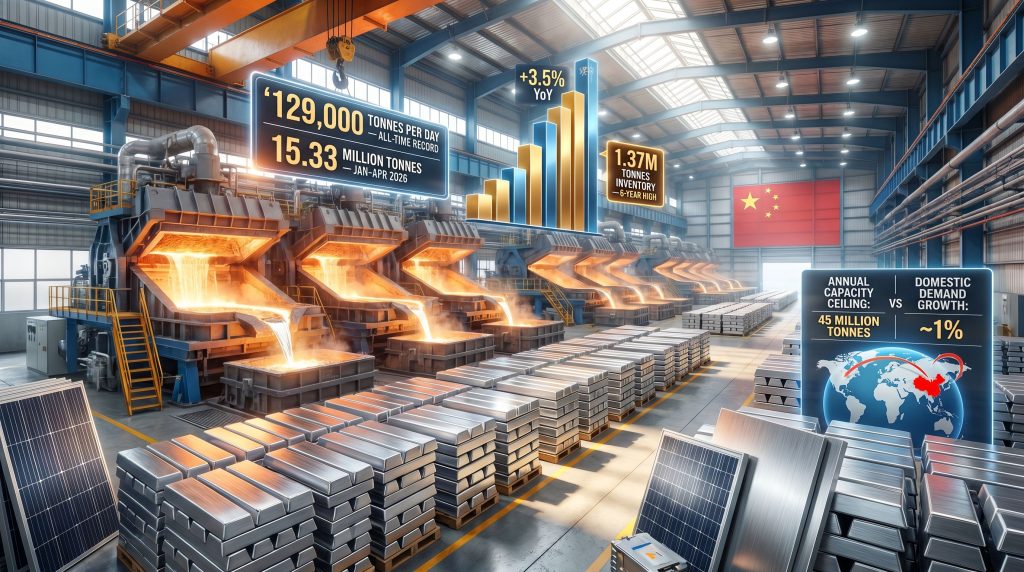

Chinese aluminium smelters pushed daily output to an all-time high of 129,000 tonnes per day in April 2026, a figure that encapsulates several converging pressures reaching their peak simultaneously. China already accounts for over 60% of global aluminium production, meaning fluctuations in its output carry disproportionate weight across international pricing and trade flows.

Three distinct forces drove the surge to this record level:

- Record smelter profit margins created powerful financial incentives to maximise throughput at every operational facility

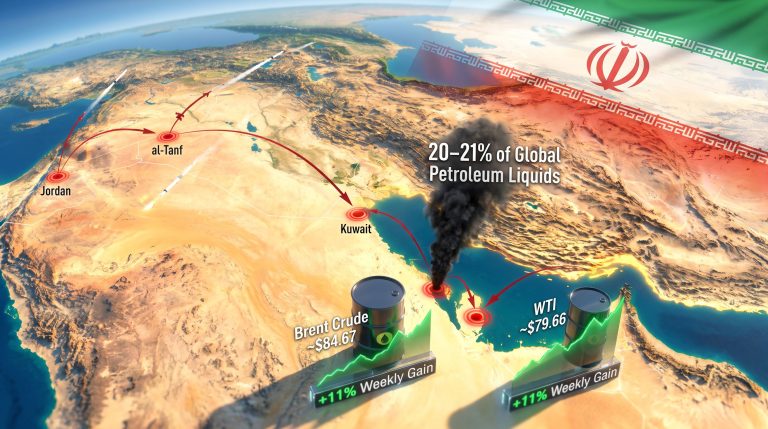

- The conflict in Iran introduced what Citigroup's analysts have characterised as the most severe aluminium supply disruption in approximately 50 years, tightening global availability outside China

- Structural demand from green energy sectors, particularly solar manufacturing and electric vehicle production, provided a longer-term production rationale beyond short-term arbitrage

What makes this output level technically significant is not just the headline figure but the mechanism behind it. China introduced a 45-million-tonne annual capacity ceiling in 2017, designed to structurally constrain oversupply, reduce carbon emissions from one of the country's most power-intensive industries, and manage electricity grid pressure. That ceiling remains formally in place.

However, the distinction between nameplate capacity and actual operational throughput has become increasingly important. Technological upgrades and process optimisation have allowed Chinese smelters to run approximately 3% above their rated nameplate capacity, enabling producers to extract maximum output from existing infrastructure without formally breaching the policy limit.

Total output in the first four months of 2026 reached 15.33 million tonnes, representing a 3.5% year-on-year increase, a growth rate that significantly outpaces domestic demand expansion.

| Metric | Figure |

|---|---|

| Daily output record (April 2026) | 129,000 tonnes |

| Jan–Apr 2026 total output | 15.33 million tonnes |

| Year-on-year output growth (Jan–Apr) | +3.5% |

| National annual capacity ceiling | 45 million tonnes |

| Estimated above-nameplate operating buffer | ~3% |

| Domestic demand growth (2026) | ~1% |

| Domestic inventory level (2026) | 1.37 million tonnes (6-year high) |

The Geopolitical Trigger: How the Iran Conflict Reshaped Supply Logic

Understanding the China aluminium output surge requires examining what happened outside China's borders. The conflict in Iran disrupted aluminium supply chains in ways that have not been observed since the 1970s, according to Citigroup's research division. Iran has developed significant aluminium smelting capacity over recent decades, and its removal from accessible global supply created an immediate tightening effect on international availability.

The mechanics of this transmission are relatively straightforward but often overlooked:

- Geopolitical disruption in a metal-producing region contracts available supply on international markets

- International aluminium premiums, which represent the price differential above the London Metal Exchange benchmark paid for physical delivery, widen as buyers compete for alternative sources

- Widening premiums create export arbitrage opportunities for Chinese smelters, making overseas sales more financially attractive relative to domestic transactions

- Chinese producers respond by maximising output and redirecting material toward export channels

This feedback loop helps explain why a conflict with no direct connection to Chinese smelting operations can nonetheless accelerate production intensity within China's aluminium sector. Furthermore, the geopolitical shock effectively converted Chinese surplus capacity into a globally demanded resource. Aluminium tariff impacts have added another layer of complexity to how global buyers are sourcing material in this environment.

Citigroup's analytical framework positions the current environment as historically exceptional, with the combination of Middle Eastern supply disruption and constrained non-Chinese capacity creating conditions that could sustain upward price pressure provided Chinese inventory dynamics do not deteriorate further.

The Inventory Problem: When Production Outpaces Absorption

The most visible consequence of the China aluminium output surge has been the rapid accumulation of domestic stockpiles. Chinese aluminium inventories have more than doubled in 2026, reaching 1.37 million tonnes, the highest level recorded in six years. This inventory build carries significant analytical weight because it reflects a structural misalignment between production intensity and demand reality.

Domestic demand growth has slowed to approximately 1% annually in 2026, and critically, turned negative during January and February before partially recovering. A production system running at near-maximum efficiency generating 3.5% output growth against a demand backdrop expanding at 1% produces a mathematically inevitable inventory surplus.

Chen Jingmin of Zijin Tianfeng Futures has noted that the speed at which inventories have accumulated triggered widespread debate within the Chinese aluminium industry about the sustainability of current production rates. The concern is not theoretical. Rapidly rising inventories typically precede spot price softening, which eventually compresses smelter margins and forces output discipline.

The sectors driving demand weakness are structurally significant:

- Construction activity remains subdued in China, reducing consumption in one of aluminium's largest traditional end-use categories including window frames, cladding, and structural components

- Manufacturing output growth has moderated, limiting demand from fabricators supplying domestic consumer goods markets

- Export absorption has proven insufficient to fully offset the domestic demand gap, despite rising international premiums creating favourable export economics

In addition, China industrial demand signals across related metals markets suggest that broader industrial softness is weighing on consumption recovery timelines.

Yunnan Province and the Hydropower Variable

One dimension of the China aluminium output surge that receives insufficient attention in mainstream analysis is the role of regional energy availability in driving production decisions. Aluminium smelting is extraordinarily electricity-intensive, requiring roughly 13 to 15 megawatt-hours per tonne of metal produced. This energy dependency makes Chinese smelting output particularly sensitive to regional power conditions.

Yunnan province in southwestern China has emerged as a swing production factor. The province hosts substantial smelting capacity powered significantly by hydroelectric generation. During periods of adequate rainfall and reservoir levels, Yunnan's smelters can operate at full capacity. During drought conditions, production curtailments become necessary regardless of market prices or margin incentives.

The improved hydropower availability observed in recent periods directly enabled smelter ramp-ups in Yunnan that contributed to the April 2026 daily output record. This creates a less-discussed but material risk: a return to drought conditions in Yunnan could curtail national output meaningfully, introducing a weather-driven supply variable that fundamentally cannot be modelled purely through financial incentives.

This hydropower dependency represents one of the more underappreciated volatility sources in Chinese aluminium supply modelling. When analysts project output based on margins and demand, they frequently underweight the role of seasonal precipitation patterns in Yunnan's ability to sustain electricity-intensive smelting at full capacity.

Green Energy Demand: Structural Support With Embedded Tension

The China aluminium output surge is being partially justified by demand growth from clean energy sectors, which are consuming aluminium at an accelerating rate. Solar panel manufacturing relies on aluminium frames and mounting structures. Electric vehicle production uses aluminium extensively in battery housings, structural components, and thermal management systems. Grid-scale energy storage infrastructure requires aluminium in both the battery technology and the supporting structures.

This creates a genuine structural demand driver that partially offsets weakness in traditional construction-linked consumption. As China's EV fleet expands and solar installation targets accelerate, aluminium industry leaders are increasingly aligning capital allocation with green sector growth projections. Consequently, aluminium demand per unit of economic output may actually increase even as the construction sector contracts.

However, the green demand narrative contains an inherent paradox. Aluminium smelting is among the most carbon-intensive industrial processes in existence when powered by coal-fired electricity. China's decarbonisation commitments sit in direct tension with the energy demands of an expanding aluminium sector. Mining decarbonisation trends are increasingly shaping how producers and policymakers approach this contradiction, particularly where renewable energy integration into smelting operations is concerned.

The broader policy contradiction involves using a carbon-intensive process to produce materials essential for a lower-carbon economy, a trade-off that policymakers have not yet formally resolved through the capacity ceiling framework. ING's green sector analysis has further highlighted how China's clean energy growth is fundamentally reshaping aluminium consumption patterns over the medium term.

The next major ASX story will hit our subscribers first

Global Price Transmission: How Chinese Decisions Reach Every Market

China's 60% share of global aluminium output means its production decisions transmit directly into LME benchmark pricing and international premiums. The pricing mechanism operates as follows: when Chinese exports increase, additional supply enters global markets, compressing the premium buyers pay above the LME benchmark for physical delivery. When Chinese production tightens, international availability contracts and premiums widen.

The current scenario presents competing pressures:

| Scenario | Key Driver | Price Implication |

|---|---|---|

| Bull Case | Prolonged geopolitical disruption + green demand surge | Continued rally; LME prices test new highs |

| Base Case | Gradual demand recovery + stable Chinese output | Moderate price consolidation |

| Bear Case | Inventory overhang + domestic demand contraction | Price correction; margin compression for smelters |

The bull case rests on the assumption that Middle East supply disruption persists while green energy demand continues accelerating, maintaining upward pressure that Chinese exports cannot fully offset. The bear case acknowledges that Chinese inventory at a six-year high represents a substantial overhang capable of capping prices if export volumes increase materially or if domestic demand fails to recover. Reuters has also noted how Western markets are responding to this dynamic by reinforcing supply defences against Chinese output growth.

Bauxite Imports and Upstream Dependency

A critical upstream dimension of the China aluminium output surge involves bauxite import trends. China's domestic bauxite reserves are increasingly characterised by declining ore grades, forcing greater reliance on imported raw material. Bauxite imports climbed 34.2% year-on-year in July 2025, reflecting the upstream demand generated by sustained smelting ambition.

China's primary bauxite import sources include Guinea in West Africa and Australia, and global bauxite supply dynamics have consequently become a more closely watched variable among aluminium market analysts. Any disruption to Guinean export capacity, whether from political instability or infrastructure constraints, would directly impact Chinese alumina refining and subsequently aluminium smelting throughput. This upstream vulnerability rarely features in mainstream China aluminium output analysis but represents a genuine medium-term supply risk.

Key Indicators for Monitoring the Next Phase

What Should Investors Watch Most Closely?

Investors and market participants tracking the China aluminium output surge should focus on the following leading indicators:

- Monthly domestic inventory levels relative to the current 1.37-million-tonne benchmark as a demand absorption signal

- Year-on-year export volume data indicating whether overseas markets are absorbing Chinese surplus effectively

- Bauxite import trends as a forward-looking indicator of sustained smelting ambition

- Hydropower reservoir levels and rainfall patterns in Yunnan province as a production swing factor

- LME aluminium spot price trajectory and its relationship to Chinese export competitiveness and international premium dynamics

- Policy signals from Chinese authorities regarding the 45-million-tonne capacity ceiling, particularly any language suggesting upward revision or tighter enforcement

The three structural constraints that will ultimately define the next phase of Chinese aluminium production are the capacity ceiling, the demand absorption capacity of both domestic and export markets, and the ongoing tension between electricity-intensive smelting and decarbonisation commitments. How these constraints interact will determine whether the current output surge represents a cyclical peak or a new production baseline.

This article contains forward-looking analysis and market scenario modelling. Readers should note that commodity markets are subject to significant uncertainty, and projections discussed herein should not be construed as financial advice. Past production trends and analyst forecasts do not guarantee future outcomes.

Want To Spot The Next Major ASX Mineral Discovery Before The Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the noise across 30+ commodities to surface actionable opportunities the moment they are announced. Explore historic discoveries that generated exceptional returns or start your 14-day free trial today to position yourself ahead of the broader market.