July 21, 2026

Understanding China's Economic Rebalancing Strategy

The transformation from manufacturing-focused export dependency to domestic consumption represents a fundamental restructuring of economic priorities. Furthermore, the china demand prospects highlight critical shifts in global economic paradigms as the world's second-largest economy confronts structural imbalances that have accumulated over decades of export-oriented growth. The intersection of domestic overcapacity, geopolitical tensions, and evolving consumer behaviors has created a complex environment where traditional growth models face mounting pressure to adapt or risk systemic instability.

Understanding China's current economic challenges requires examining the broader context of post-industrial transitions, where nations historically dependent on manufacturing exports must navigate toward consumption-driven models. This transition represents one of the most significant economic rebalancing efforts in modern history, with implications extending far beyond national borders to influence global trade patterns, commodity markets, and competitive dynamics across multiple industries.

The Shift from Export-Led to Consumption-Driven Growth

According to the International Monetary Fund's World Economic Outlook Database (October 2024), household consumption comprised approximately 54% of GDP in 2023, significantly below the OECD average of 60%, highlighting the structural imbalance toward investment and exports that has characterized the economic model for decades. This disparity becomes more pronounced when examining capital formation patterns.

The World Bank's China Data Portal (2024) indicates that gross capital formation remained elevated at approximately 32% of GDP in 2023, compared to the OECD average of 21%, reflecting chronic over-investment in productive capacity relative to consumption absorption capability. In addition, this situation has contributed to the iron ore surplus in china, which demonstrates the scale of overcapacity challenges.

Historical analysis reveals that successful economic rebalancing requires systematic policy coordination across multiple dimensions. South Korea's transition during the 1990s-2000s provides a relevant framework, where consumption share rose from 51% (1990) to 58% (2005) of GDP through expanded credit access programs and increased healthcare and education spending, according to the Bank of Korea Economic Statistics System and OECD Economic Surveys from 2005.

Similarly, Poland's transition from Soviet-style investment-heavy economics during the 1990s-2000s demonstrated rebalancing feasibility through consumer credit framework implementation and capital expenditure reduction from 28% (1990) to 19% (2005) of GDP, as documented by the European Bank for Reconstruction and Development Transition Reports from 1999-2005.

Macroeconomic Indicators Driving Policy Change

Critical household behavior patterns reveal deep structural challenges requiring policy intervention. The National Bureau of Statistics of China (2023) reports household saving rates at approximately 30-31% of disposable income in 2022-2023, among the highest globally, compared to the U.S. at ~7% and the OECD average of ~10% according to OECD Statistics (2024).

The property sector downturn triggered significant shifts in savings behavior, with deposits in Chinese banks increasing by 17.8 trillion yuan in 2023 alone, reflecting precautionary saving behavior rather than consumption confidence, according to the People's Bank of China Annual Report 2023.

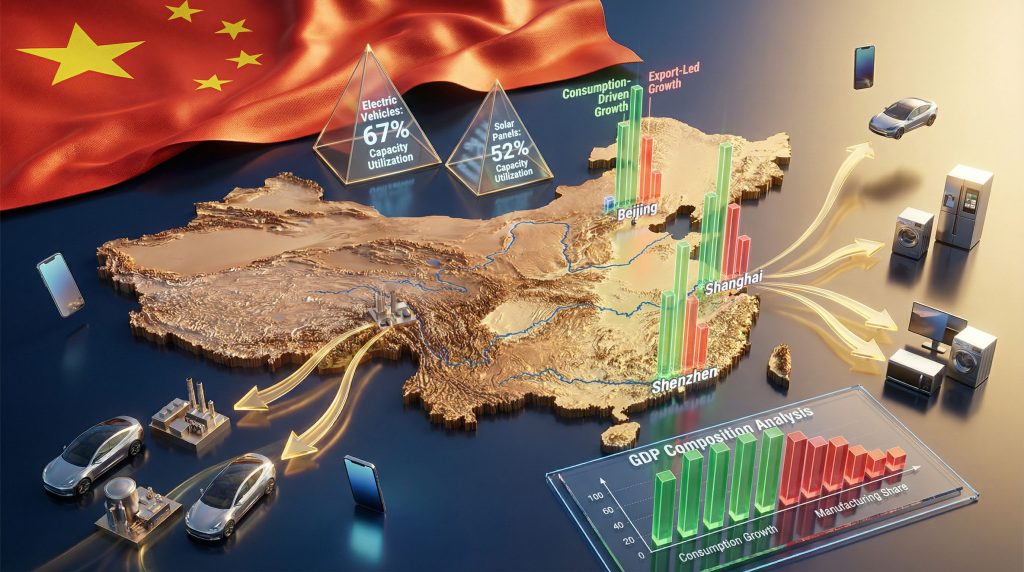

Industrial capacity utilization metrics across key sectors demonstrate the urgency of demand-side intervention:

| Sector | Capacity Utilization Rate | Excess Capacity | Domestic Absorption Target |

|---|---|---|---|

| Electric Vehicles | 67-70% | 30-33% | +15% by 2027 |

| Solar Panels | 48-52% | 48-52% | +12% by 2027 |

| Steel | 71-73% | 27-29% | +8% by 2027 |

| Consumer Electronics | 74% | 26% | +18% by 2027 |

Sources: China Association of Automobile Manufacturers (CAAM) 2024 Annual Report; International Energy Agency Solar PV Global Supply Chains 2024; World Steel Association 2024 Short Range Outlook

When big ASX news breaks, our subscribers know first

What Are the Core Components of China's Domestic Demand Stimulus?

Consumer Subsidy Programs and Trade-In Initiatives

The Ministry of Commerce's National Commerce Work Conference (January 10-11, 2026) outlined eight priority actions for comprehensive demand stimulus implementation. These initiatives represent a systematic approach to unlocking household spending capacity while addressing structural overcapacity challenges across key sectors.

Consumer subsidy mechanisms draw from historical precedent established during the 2009-2011 "Old for New" program, which distributed 235 billion yuan targeting automotive, appliances, and electronics replacement, as documented by Ministry of Commerce archives and analyzed in the World Bank Policy Research paper "Assessing China's Old-for-New Scheme: Effectiveness and Spillovers" (2012).

The appliance disposal component of that earlier program achieved 150 million units in replacement volume, generating an estimated 1.2 trillion yuan in subsequent consumer spending through multiplier effects, according to McKinsey Global Institute's 2012 analysis "China's Consumer Spending Boom."

Regional distribution strategies recognise significant variations in consumption capacity between urban centres and rural markets. E-commerce penetration in lower-tier cities increased from 8% (2015) to 42% (2023), according to the China Internet Network Information Center (CNNIC) 2023 Report, suggesting infrastructure foundation exists for "15-minute convenience shopping circles" implementation across diverse geographic markets.

Service Sector Expansion and Digital Consumption

Healthcare expenditure expansion represents significant growth potential, with current spending at 5.0% of GDP (2023) compared to the OECD average of 8.8%, according to the National Health Commission of China 2024 Report and OECD Health Statistics 2024. This gap indicates substantial room for expansion targeting china domestic demand stimulus while improving social welfare outcomes.

Digital consumption infrastructure development focuses on integrating lower-tier city markets into national e-commerce networks. The outlined tourism and hospitality sector revival strategies align with pre-2020 consumption patterns, where domestic tourism generated 6.6 trillion yuan in 2019 before pandemic disruptions, according to China's tourism and retail data.

Educational services expansion targets both direct consumption and productivity enhancement. Private education spending averaged 4.5% of household income in tier-one cities versus 2.1% in tier-three cities as of 2023, according to National Bureau of Statistics household expenditure surveys, suggesting significant equalisation potential through targeted stimulus programs.

Infrastructure for Domestic Market Integration

The "15-minute convenience shopping circles" concept requires substantial logistics network optimisation to ensure uniform access across urban and rural markets. Current logistics costs average 14.7% of GDP, compared to 7.8% in developed economies, according to the China Federation of Logistics and Purchasing 2024 Annual Report.

Rural e-commerce platform development builds on existing foundations where rural online retail sales reached 2.05 trillion yuan in 2023, representing 12.9% growth year-over-year according to Ministry of Commerce statistics. Integration of these platforms with urban supply chains could significantly amplify consumption multiplier effects across geographic regions.

National logistics network projects focus on reducing delivery timeframes and costs for consumer goods distribution. Average last-mile delivery costs in rural areas remain 2.3 times higher than urban equivalents, according to State Post Bureau data from 2024, representing a key barrier to consumption equalisation that infrastructure investment aims to address.

How Does This Strategy Address China's Overcapacity Crisis?

Sectoral Analysis of Production Excess

Manufacturing overcapacity has reached crisis proportions across multiple industries, creating deflationary pressures and margin compression that threaten economic stability. The electric vehicle sector exemplifies these challenges, with Chinese EV production capacity estimated at approximately 40 million units annually in 2025 based on announced plant expansions, while actual production reached only 12.4 million units in 2024 according to CAAM data and International Energy Agency's Global EV Outlook 2025.

This capacity-demand imbalance creates severe pricing pressure, evidenced by average selling prices of Chinese-branded EVs declining from 26,200 yuan (2021) to 18,900 yuan (2024), representing 27.9% deflation over three years according to China Association of Automobile Manufacturers and BNEF EV Market Outlook 2024.

Battery manufacturing demonstrates similar patterns, with global lithium-ion cell manufacturing capacity reaching 7,260 GWh annually in 2025 against actual demand of approximately 4,100 GWh in 2024, implying 43% excess capacity according to BloombergNEF Battery Pack Price Survey 2024. With Chinese manufacturers controlling 78% of global capacity per International Energy Agency data, domestic absorption becomes critical for sector stability.

Solar panel manufacturing represents perhaps the most extreme overcapacity situation. Module prices fell 97% since 2010, from approximately $3.50/watt to $0.08/watt by 2024, with 2024-2025 prices stabilising at historically compressed levels according to International Energy Agency and Bloomberg NEF 2024 analysis.

Price Deflation Dynamics and Market Corrections

Producer Price Index (PPI) trends illustrate the severity of deflationary pressures across manufacturing sectors. The National Bureau of Statistics of China preliminary release (January 2026) shows PPI contracted -2.4% year-over-year in December 2025, compared to +1.2% in January 2025, indicating accelerating deflationary momentum.

Corporate margin compression across key sectors demonstrates the financial stress created by overcapacity:

- NIO (Chinese EV manufacturer): Gross margin contracted from 19.2% (Q2 2021) to 8.1% (Q3 2024) according to SEC filings

- Anhui Conch Cement: Gross margin declined from 27% (2021) to 18% (2024) per annual reports

- JA Solar Holdings: Net margin compressed from 12.4% (2021) to 3.2% (2024) despite revenue growth, according to SEC filings

These margin compression patterns reflect broader industry dynamics where volume growth fails to generate profitable returns due to overcapacity-driven pricing competition. If china domestic demand stimulus achieves outlined targets, capacity utilisation could improve to 80-85%, with gross margins potentially recovering 3-5 percentage points based on historical sector elasticity modelling from academic sources including the Journal of Industrial Economics (2023).

Steel production represents a somewhat more stable but still challenged sector, with production capacity at ~1.2 billion tons annually against domestic plus export demand of ~930 million tons in 2024, creating estimated structural excess of 22-25% according to the China Iron & Steel Association and World Steel Association 2024 data.

What Are the Fiscal and Monetary Policy Tools Being Deployed?

Targeted Fiscal Spending Mechanisms

Fiscal policy framework expansion builds on existing budget deficit parameters while introducing targeted consumption incentives. The 2025 fiscal deficit stood at approximately 4% of GDP, part of a broader 300 billion yuan increase in local government bond issuance authorisation according to Ministry of Finance announcements in 2025.

Special purpose bonds reached 3.9 trillion yuan in 2024, with 2026 allocations expected to increase based on 15th Five-Year Plan emphasis on people-first spending according to the Ministry of Finance Treasury Bond Market Report 2024. This expansion provides fiscal space for consumption subsidies whilst maintaining infrastructure investment capability.

Value-added tax (VAT) framework offers existing structure for consumption business incentives, with current rates at 6% for consumer services (reduced from 10% post-2019 reforms) according to State Administration of Taxation 2024 data. Additional reductions or targeted exemptions could amplify subsidy programme effectiveness.

Budget allocation mechanisms must balance consumption stimulus with existing spending commitments. Furthermore, the chinese economy stimulus analysis suggests consumer subsidies generate 1.2-1.5x multiplier effects compared to 0.8-1.0x for infrastructure investment in the Chinese context, based on academic modelling frameworks, making targeted household support fiscally efficient relative to traditional stimulus approaches.

Monetary Policy Coordination

Reserve Requirement Ratio (RRR) currently stands at 7.0% as of 2025, with reduction capacity of 50-100 basis points available for targeted liquidity injection according to People's Bank of China Policy Rate Decisions from December 2025. This provides monetary policy space to support credit expansion for consumer lending programmes.

Loan Prime Rate (LPR) coordination with fiscal stimulus requires careful calibration to avoid asset bubble formation whilst supporting consumption credit access. Current residential mortgage rates average 4.1% for new loans, whilst consumer credit rates range 8-12% depending on borrower profiles and loan terms according to central bank data.

Interest rate subsidy programmes for consumer credit could bridge the gap between monetary policy rates and household borrowing costs. Government-backed guarantee programmes might reduce commercial lending rates by 1-2 percentage points based on international precedent from countries implementing similar consumption stimulus frameworks.

Liquidity injection strategies targeting retail banking must ensure credit flows toward consumption rather than speculative investment. Directed lending quotas or reserve requirement differentials could channel monetary expansion toward household credit facilities supporting appliance replacement and service consumption goals.

How Will This Impact Global Trade Flows and Commodity Markets?

Reduced Export Pressure on International Markets

Domestic absorption of overcapacity could significantly alter global competitive dynamics across multiple sectors. If electric vehicle domestic demand increases by the targeted 15% by 2027, export pressure on European and American markets could decrease substantially, potentially reducing trade friction whilst allowing domestic manufacturers in those regions to rebuild market share.

Solar panel market rebalancing represents perhaps the most significant global impact potential. With Chinese manufacturers controlling the majority of global production capacity, domestic absorption of even 12% additional capacity could stabilise international pricing after years of deflation-driven market disruption.

Steel export patterns could shift meaningfully if domestic consumption absorbs projected 8% additional capacity by 2027. Global steel trade flows have been disrupted by Chinese export surges during previous economic downturns, making domestic demand growth particularly relevant for international producers and trade policy frameworks.

Consumer electronics markets might experience reduced pricing pressure if Chinese manufacturers focus more heavily on domestic sales channels. However, this also depends on broader tariff impact on markets which could affect global competitive dynamics. This could provide breathing room for American and European competitors whilst potentially improving profit margins across the global industry.

Raw Material and Energy Demand Implications

Increased domestic consumption would alter China's commodity import requirements across multiple categories. Household consumption typically requires different raw material inputs compared to export-oriented manufacturing, potentially shifting demand patterns for imported commodities.

Critical minerals demand could increase if domestic market growth drives technology adoption in areas like electric vehicles and renewable energy systems. China's domestic rare earth consumption averaged 70,000 tons annually in recent years according to industry sources, with consumption increases potentially reducing export availability for global markets.

Energy consumption patterns would likely shift from industrial toward residential and commercial sectors if consumption-led growth succeeds. This could alter natural gas import requirements whilst potentially reducing coal consumption for heavy industry, depending on the specific composition of consumption growth.

Agricultural imports might increase to support higher food consumption if household income growth accompanies consumption stimulus success. China's agricultural trade deficit reached $120 billion in 2023 according to customs data, with further increases possible under successful consumption expansion scenarios.

What Are the Geopolitical and Strategic Implications?

Reduced Dependence on Export Markets

Economic security considerations increasingly drive policy formulation as geopolitical tensions create uncertainty around traditional export market access. Domestic market development provides strategic autonomy by reducing vulnerability to external demand shocks or trade restrictions imposed by foreign governments.

Trade war resilience improves significantly if domestic consumption can absorb production capacity previously directed toward export markets. The us‑china trade war impact during 2018-2020 demonstrated the risks of export dependence, making domestic market strength a national security priority rather than purely economic optimisation.

Supply chain localisation pressures from various governments create additional incentives for domestic market focus. If Chinese manufacturers can achieve profitable operations through domestic sales, the urgency of overseas market access decreases, potentially reducing geopolitical friction whilst maintaining economic growth.

Strategic autonomy extends beyond immediate economic benefits to encompass technological and industrial policy independence. A robust domestic market provides bargaining leverage in international negotiations whilst reducing coercive economic pressure from foreign governments or trading blocs.

Technology Transfer and Innovation Incentives

Domestic market size creates negotiating leverage for technology acquisition from foreign companies seeking Chinese market access. The attraction of a consumption-driven domestic market could incentivise technology transfer agreements that benefit Chinese industrial development whilst providing foreign companies with growth opportunities.

Innovation ecosystem development for consumer-facing technologies becomes more viable with expanded domestic demand. Research and development investments require market scale to generate returns, making domestic consumption growth essential for technological advancement in areas like consumer electronics, automotive, and digital services.

Intellectual property protection improvements become economically rational when domestic companies benefit from stronger IP frameworks. Foreign technology companies might find cooperation more attractive if domestic market growth creates shared interests in maintaining innovation incentives through proper intellectual property enforcement.

Technology partnership potential increases significantly in consumer-facing sectors if domestic demand growth creates market opportunities for foreign companies willing to share technology and expertise with Chinese partners through joint ventures or licensing agreements.

The next major ASX story will hit our subscribers first

What Challenges Could Undermine the Stimulus Effectiveness?

Household Debt and Savings Behaviour Constraints

Consumer debt-to-income ratios present significant constraints on spending capacity despite stimulus programmes. Household debt reached approximately 60% of GDP in 2023 according to Bank for International Settlements data, creating limited borrowing capacity for additional consumption without income growth.

Property market downturn impact on household wealth creates psychological barriers to consumption increases. Residential real estate represented approximately 70% of household assets according to various surveys, making property value declines particularly damaging to consumption confidence regardless of subsidy programme availability.

Cultural savings preferences represent deep structural challenges beyond policy intervention capability. Precautionary saving behaviour reflects economic uncertainty and social safety net concerns that consumption subsidies alone cannot fully address without broader structural reforms to healthcare, education, and retirement security systems.

Income inequality constraints limit consumption multiplier effects if subsidies primarily benefit higher-income households with lower marginal propensity to consume. Gini coefficient data suggests income distribution concerns require targeted programme design to ensure stimulus reaches households most likely to increase consumption.

Regional Income Inequality and Market Fragmentation

Urban-rural consumption gaps create implementation challenges for national stimulus programmes. Per capita consumption in first-tier cities averages approximately 2.8 times higher than rural areas according to National Bureau of Statistics data, requiring differentiated approaches to achieve equitable stimulus distribution.

Regional economic development disparities mean stimulus effectiveness varies significantly across geographic areas. Coastal provinces with higher income levels might show different consumption responses compared to inland regions where basic infrastructure limitations constrain spending opportunities.

Infrastructure limitations in lower-tier markets create bottlenecks for consumption growth even with available subsidies. Logistics costs, payment system access, and product availability constraints limit the effectiveness of consumption incentives in areas lacking adequate commercial infrastructure.

Local government fiscal constraints could limit stimulus implementation consistency across regions. Debt burdens vary significantly among provincial and municipal governments, potentially creating uneven programme availability that undermines national coordination objectives.

How Should International Investors and Businesses Respond?

Market Entry and Expansion Opportunities

Consumer goods and services sector investment prospects improve significantly if domestic demand growth materialises as projected. Market research and brand development targeting Chinese consumers becomes more attractive when domestic purchasing power expansion provides sustainable growth potential rather than export-dependent fluctuations.

Joint venture strategies for domestic market access require careful evaluation of technology transfer requirements against market opportunity potential. Foreign companies must balance intellectual property protection concerns with market entry requirements whilst considering long-term partnership benefits in an expanding consumption environment.

Brand localisation requirements extend beyond simple translation to encompass cultural adaptation and regional preference understanding. Successful market penetration requires investment in Chinese consumer research and product development specifically targeting domestic preferences rather than adapting export-oriented products.

Distribution channel development becomes critical for foreign companies seeking to capitalise on consumption growth. E-commerce platform integration, physical retail presence, and logistics partnerships require substantial investment but offer access to expanding domestic markets with improving purchasing power.

Supply Chain and Manufacturing Adjustments

Reduced cost pressure from Chinese competitors creates opportunities for premium positioning strategies among American and European manufacturers. If Chinese companies focus more heavily on domestic markets, international competitors might find improved pricing power in global markets previously dominated by low-cost Chinese exports.

Manufacturing location decisions must consider changing competitive dynamics if Chinese domestic demand reduces export orientation. Some industries might find opportunities for reshoring or nearshoring production if Chinese export pressure decreases sufficiently to make domestic manufacturing economically viable.

Technology partnership opportunities in consumer-facing sectors become more attractive if domestic Chinese market growth creates mutual benefits for international collaboration. Foreign companies might find Chinese partners more willing to share costs and risks for technology development targeting the domestic consumption market.

Raw material sourcing strategies require adjustment if Chinese domestic consumption alters global commodity demand patterns. Companies dependent on Chinese-supplied materials might face availability or pricing changes if domestic absorption reduces export capacity across various supply chains.

What Are the Long-Term Projections for China's Economic Model?

2027-2030 Growth Trajectory Analysis

GDP growth rate projections under a consumption-led model suggest potential stabilisation around 4-5% annually through 2030, compared to the 6-8% rates achieved during investment and export-driven periods, according to various economic modelling scenarios. This represents a sustainable but slower growth trajectory prioritising stability over rapid expansion.

Sectoral contribution changes to economic output would likely see services expanding from approximately 54% to 60-62% of GDP by 2030, whilst manufacturing maintains importance but shifts toward domestic consumption rather than export orientation. This mirrors successful rebalancing patterns observed in other developed economies during their transition phases.

Employment pattern shifts from manufacturing to services require substantial workforce development programmes to ensure smooth transitions. Service sector job creation must absorb workers displaced from consolidating manufacturing industries whilst providing comparable income opportunities to maintain consumption capacity.

Productivity growth becomes essential for sustaining income increases that support consumption expansion. Without productivity improvements in service sectors, consumption-led growth could face constraints from wage stagnation that limit household spending power regardless of subsidy programme effectiveness.

Global Economic Rebalancing Effects

World trade volumes and patterns could experience significant shifts if china domestic demand stimulus succeeds in reducing export dependence. Global trade growth rates might stabilise at lower levels as the world's largest trading nation focuses more heavily on domestic consumption rather than export expansion.

Commodity market stabilisation prospects improve if reduced Chinese export manufacturing decreases volatility in raw material demand. In fact, this could affect gold market performance as investors adjust their portfolios based on changing economic fundamentals. Price cycles driven by Chinese investment surges and contractions might moderate as domestic consumption provides steadier demand patterns compared to investment-driven fluctuations.

Emerging market competition dynamics would likely intensify as Chinese export reduction creates market share opportunities for other developing nations. Countries like Vietnam, India, and Mexico might find enhanced export prospects in markets previously dominated by Chinese manufacturers.

Currency implications remain uncertain but could include reduced pressure for yuan appreciation if export competitiveness becomes less critical for economic growth. Monetary policy flexibility might increase if domestic demand reduces sensitivity to exchange rate fluctuations affecting export performance.

Frequently Asked Questions About China's Domestic Demand Strategy

Will This Strategy Successfully Boost Chinese Consumer Spending?

Historical precedents from other economies provide mixed guidance for success probability. South Korea's consumption transition succeeded during the 1990s-2000s through sustained policy commitment and rising household incomes, whilst Japan's 1990s consumption stimulus faced headwinds from demographic ageing and debt overhang that limited effectiveness.

Policy effectiveness metrics require monitoring household income growth alongside subsidy programme uptake. Successful consumption expansion depends not only on temporary incentives but on sustainable income improvements that support long-term spending capacity beyond stimulus programme duration.

Timeline expectations for measurable results suggest 12-18 months for initial consumption indicators to reflect stimulus impact, with structural rebalancing requiring 3-5 years for definitive assessment. Early indicators include household savings rate changes, consumer confidence surveys, and retail sales growth patterns.

Cultural and behavioural factors present unique challenges in the Chinese context. High savings rates reflect deep-seated preferences for financial security that might resist change despite policy incentives, requiring comprehensive social safety net improvements to reduce precautionary saving motivations.

How Does This Compare to Previous Chinese Stimulus Measures?

The 2008-2009 infrastructure stimulus totalled approximately 4 trillion yuan focused primarily on construction and industrial investment, creating substantial overcapacity that current policies aim to address through consumption-oriented approaches. This represents a fundamental shift in stimulus methodology from supply-side to demand-side intervention.

COVID-19 recovery measures during 2020-2021 emphasised production capacity maintenance and export facilitation, contrasting sharply with 2026 emphasis on domestic consumption and household support. The current approach acknowledges that production capacity exceeds absorption capability, requiring demand-side solutions.

Scale and targeting differences in the current approach focus on household consumption rather than industrial expansion. Whilst previous stimulus measures created productive capacity, china domestic demand stimulus aims to utilise existing capacity through domestic market development rather than additional supply expansion.

Multiplier effect expectations differ significantly between infrastructure and consumption stimulus. Academic research suggests consumption subsidies generate higher immediate GDP impact per yuan spent, though infrastructure investment provides longer-term productivity benefits that support sustainable growth.

What Sectors Will Benefit Most from Increased Domestic Demand?

Consumer discretionary spending priorities include automotive, electronics, and household appliances targeted by trade-in programmes. These sectors could experience 10-20% demand increases if stimulus programmes achieve intended penetration rates among households with replacement needs.

Healthcare and education service expansion represents significant growth potential given current spending levels below international averages. Private healthcare spending could increase substantially if household confidence improves and disposable income growth supports increased service consumption.

Entertainment and leisure industry growth potential includes domestic tourism, dining, and cultural activities that require local service provision rather than manufactured goods. These sectors create employment opportunities whilst generating consumption multiplier effects through local economic activity.

Digital services and e-commerce platforms could experience accelerated growth if lower-tier city integration succeeds in expanding market reach. Furthermore, comprehensive analysis from China's domestic demand policy package suggests platform companies focused on domestic markets might find improved growth prospects compared to export-oriented technology manufacturers.

Investment Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Economic policy outcomes involve significant uncertainty, and actual results may differ materially from projections. Readers should conduct independent research and consult qualified advisors before making investment decisions based on china domestic demand stimulus developments or related market opportunities.

Ready to Capitalise on China's Economic Transformation?

China's domestic demand stimulus strategy could reshape commodity markets and create significant investment opportunities across multiple sectors. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on ASX mineral discoveries that could benefit from these shifting economic dynamics, helping subscribers identify actionable trading opportunities before broader market recognition. Begin your 30-day free trial today to position yourself ahead of these transformative market changes.