June 10, 2026

China's automotive manufacturing landscape faces unprecedented structural pressures as multiple cost vectors converge simultaneously. The intersection of artificial intelligence infrastructure investment, commodity market volatility, and policy environment shifts creates a complex economic framework that challenges traditional manufacturing economics. The rising metal and memory prices in China's EV industry represents more than cyclical market adjustment—it signals potential industry restructuring across the world's largest electric vehicle market.

Manufacturing cost structures that remained stable for decades now experience rapid transformation. The traditional balance between raw material procurement, component sourcing, and final assembly economics requires fundamental recalibration as new technological demands compete for identical resource pools. Understanding these dynamics becomes essential for stakeholders navigating China's evolving electric mobility ecosystem.

Critical Raw Material Price Inflation Across Key Components

The foundation of electric vehicle manufacturing rests on specific material inputs that have experienced dramatic cost escalation throughout 2025 and into early 2026. Lithium carbonate, the primary feedstock for battery production, demonstrates extreme price volatility that defies historical commodity patterns, contributing significantly to lithium market insights across global markets.

Battery-grade lithium carbonate prices in China surged from RMB 75,700 per ton on January 1, 2025, to RMB 175,250 per ton by January 23, 2026, representing a 131.4% year-over-year increase. This trajectory intensified dramatically in the final quarter of 2025, with prices jumping approximately 80% from RMB 116,700 per ton on December 30, 2025, to the January 2026 peak.

The volatility pattern reveals deeper market structure changes beyond traditional supply-demand dynamics:

- December 26, 2025: RMB 121,400/ton

- January 13, 2026: RMB 163,850/ton (35% increase over 23 days)

- January 23, 2026: RMB 175,250/ton (7% increase over 10 days)

- January 26, 2026: RMB 169,250/ton (3.4% decline indicating potential correction)

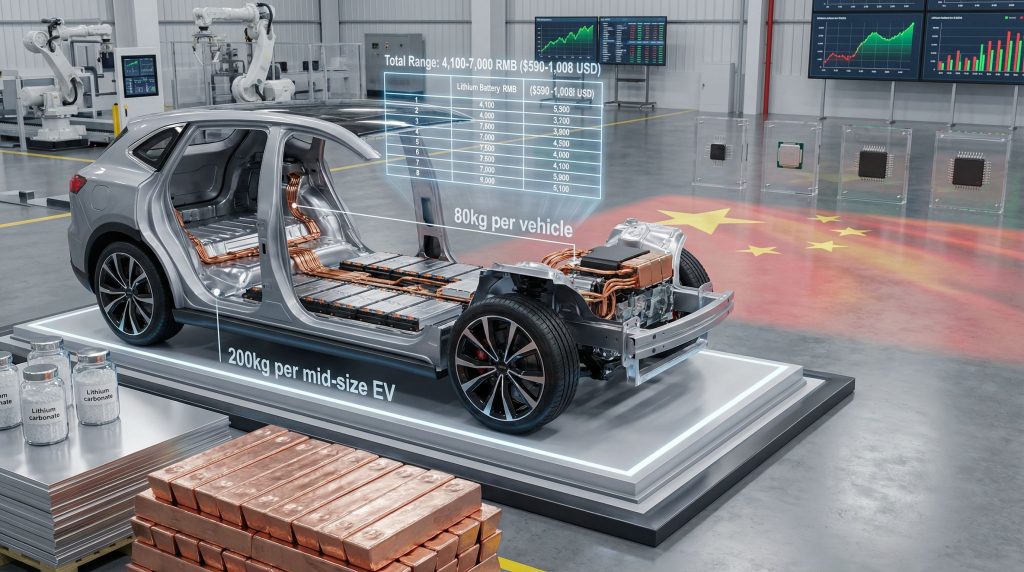

Aluminum and copper requirements present additional cost pressures with more predictable but significant impacts. Mid-size electric vehicles require approximately 200 kilograms of aluminum and 80 kilograms of copper per unit. Based on UBS analysis, aluminum costs increased by RMB 600 per vehicle over the three-month period preceding January 2026, while copper costs rose by RMB 1,200 per vehicle during the same timeframe.

These increases reflect broader industrial metal price trends in China rather than electric vehicle-specific demand shocks. However, the concentration of metal requirements in EV manufacturing amplifies exposure to commodity cycles compared to traditional internal combustion engine vehicles.

Memory Chip Supply Chain Disruptions

The semiconductor component of electric vehicle manufacturing presents unique challenges distinct from traditional automotive supply chains. DRAM pricing for automotive applications experienced an extraordinary 180% increase over three months, fundamentally altering cost structures for intelligent vehicle systems.

Automotive DRAM specifications serve three critical functional domains: autonomous driving processors, infotainment systems, and real-time vehicle control networks. The cost range varies dramatically based on vehicle intelligence level, spanning $25 to $150 per vehicle depending on computational requirements.

A baseline "reasonably intelligent vehicle" typically requires approximately $100 worth of DRAM components (equivalent to RMB 700 before inflation). Following the price surge, this increased to RMB 2,000 per vehicle, representing an incremental cost burden of RMB 1,300 per unit.

Furthermore, this cost escalation stems from artificial intelligence infrastructure competition for semiconductor manufacturing capacity. Data center expansion for AI applications creates direct resource competition with automotive semiconductor allocation, fundamentally changing supply chain economics.

When big ASX news breaks, our subscribers know first

Quantified Cost Impact Analysis

The convergence of multiple cost pressures creates cumulative manufacturing cost increases that challenge existing profit margin structures across China's electric vehicle industry. UBS research quantifies these impacts with precision that demonstrates the severity of current market conditions.

| Component Category | Cost Increase (RMB) | Cost Increase (USD) | Impact Classification |

|---|---|---|---|

| Aluminum (200kg) | 600 | 86 | Moderate |

| Copper (80kg) | 1,200 | 173 | High |

| Lithium Materials | 1,000-3,800 | 144-547 | Critical |

| Memory Chips | 1,300 | 187 | High |

| Total Range | 4,100-7,000 | 590-1,008 | Severe |

The lower bound scenario (RMB 4,100 total increase) assumes minimal lithium cost impact and baseline component price increases. The upper bound (RMB 7,000) incorporates maximum lithium volatility exposure and additional component cost pressures not captured in the primary analysis.

Manufacturing Cost Structure Transformation

Traditional electric vehicle cost allocation models require fundamental revision under current market conditions. Historical cost structures typically distributed expenses across predictable categories with commodity inputs representing manageable portions of total vehicle value.

A representative mid-size Chinese electric vehicle cost structure (as of January 2026) allocates expenses across:

- Battery pack: 25-35% of vehicle cost

- Electric motor & power electronics: 15-20%

- Body & chassis: 20-25%

- Semiconductors & software: 8-12%

- Assembly & labour: 10-15%

The documented cost increases disproportionately impact battery and semiconductor cost pools. Lithium price volatility (ranging from 23% to 163% increases) primarily affects the battery cost category, while DRAM price escalation directly impacts semiconductor budgets.

For a mid-size electric vehicle with a RMB 150,000 selling price and historical profit margins of 5-8% (RMB 7,500-12,000), the cost increase scenarios present severe margin compression:

- Midpoint cost increase: RMB 5,500

- Margin impact: 3.7% of selling price absorbed

- Result: Near-complete margin elimination without price adjustments

AI-Driven Demand Competition and Smart Vehicle Requirements

The fundamental driver of memory chip cost escalation represents a structural shift in global semiconductor allocation rather than cyclical supply constraints. Artificial intelligence infrastructure development creates unprecedented demand for identical semiconductor components required for advanced electric vehicle systems.

William Li, Nio's CEO, articulated this competitive dynamic during January 2026 industry briefings, emphasising that manufacturers face direct resource competition with computing centres and AI infrastructure providers for memory chip allocation. This represents a paradigm shift from traditional automotive supply chains where component availability followed predictable allocation patterns.

The competition operates across multiple semiconductor categories:

- High-performance DRAM for real-time processing applications

- Specialised automotive microcontrollers with AI acceleration capabilities

- Graphics processing units adapted for automotive inference workloads

What are Smart Vehicle Feature Requirements?

Modern electric vehicles incorporate computational requirements that approach data centre specifications for certain applications. Autonomous driving systems require continuous real-time processing of sensor data streams, generating memory bandwidth requirements previously associated with enterprise computing applications.

The variance in per-vehicle DRAM costs ($25-$150) reflects fundamental differences in vehicle intelligence architectures:

- Basic connectivity vehicles ($25-40 DRAM): Limited to infotainment and basic vehicle control

- Advanced driver assistance ($60-90 DRAM): Lane keeping, adaptive cruise control, parking assistance

- Autonomous-capable platforms ($100-150 DRAM): Full sensor fusion, real-time mapping, predictive analytics

Automotive-grade DRAM specifications exceed consumer electronics requirements for temperature tolerance, vibration resistance, and reliability standards. These enhanced specifications contribute to price premiums that amplify cost sensitivity during supply shortage periods.

Market Dynamics Preventing Cost Pass-Through

China's electric vehicle market structure in early 2026 presents unique constraints that prevent traditional cost pass-through mechanisms from operating effectively. Unlike historical commodity price cycles where industry-wide cost increases typically distribute across supply chain participants, current market conditions create structural barriers to price adjustment.

Competitive Landscape Constraints

Market saturation combined with aggressive pricing competition limits manufacturers' ability to implement cost increases without losing market share. The Chinese electric vehicle market features over 100 active brands competing across overlapping price segments, creating pricing pressure that persists despite uniform cost increases.

Consumer price sensitivity increased following government stimulus withdrawal and the reimposition of purchase taxes. The 5% purchase tax effective January 2026 represents additional cost burden that consumers must absorb simultaneously with potential vehicle price increases.

However, historical analysis demonstrates that commodity cost pass-through rates approach 80-90% when all industry players face identical challenges under normal market conditions. Current market structure breaks this pattern through several mechanisms:

- Inventory overhang from 2025 overproduction

- Brand positioning pressure in premium segments

- Government policy uncertainty regarding future incentives

- Consumer demand weakness following stimulus period

Policy Environment Challenges

The regulatory environment compounds cost absorption pressures through multiple simultaneous policy changes. Purchase tax reinstatement eliminates government support that previously offset vehicle cost increases for consumers, particularly amidst the ongoing US–China trade conflict tensions.

Additional regulatory compliance costs accumulate across:

- Enhanced safety testing requirements for smart vehicles

- Data security regulations for connected car platforms

- Environmental compliance for battery recycling systems

- Export certification for international market access

Consequently, these regulatory costs represent fixed expenses that cannot be reduced through operational efficiency, creating additional margin pressure beyond commodity cost increases.

Strategic Cost Management Approaches

Electric vehicle manufacturers implement diverse strategies to address cost pressures while maintaining competitive positioning. These approaches vary significantly based on company scale, market position, and financial resources.

Premium brands demonstrate superior ability to maintain margins through value-added features and brand premium pricing. Companies like Nio, Li Auto, and emerging luxury manufacturers can potentially absorb cost increases more effectively than mass-market producers.

Supply Chain Optimisation Initiatives

Vertical integration emerges as a critical strategy for managing commodity cost volatility. Leading manufacturers pursue direct relationships with mining companies and battery material processors to secure supply at predetermined pricing structures, embracing mining industry innovation practices.

BYD's integrated approach exemplifies this strategy through:

- Direct lithium mining investments in South America

- Captive battery cell manufacturing capacity

- Semiconductor design and procurement partnerships

- Vertical integration across key component categories

Alternative sourcing strategies focus on supplier diversification and long-term contract negotiations. Manufacturers actively develop secondary supplier relationships to reduce dependence on spot market pricing for critical components.

Hedging mechanisms for commodity exposure include:

- Forward purchase contracts for key materials

- Financial hedging instruments for metal price exposure

- Strategic inventory accumulation during price valleys

- Joint procurement initiatives with industry partners

For instance, effective market volatility hedging strategies have become essential for maintaining operational stability.

Long-Term Industry Structure Implications

The sustained cost pressure environment accelerates market consolidation dynamics across China's electric vehicle industry. Margin compression disproportionately impacts smaller manufacturers with limited financial resources and scale advantages.

Market Consolidation Scenarios

Industry analysts project that 30-40% of current electric vehicle manufacturers may exit the market or merge with larger competitors by 2027 if cost pressures persist. This consolidation pattern follows historical precedent in automotive industry development.

Economies of scale advantages become increasingly critical for survival. Large manufacturers can:

- Negotiate volume purchasing agreements for key components

- Amortise research and development costs across larger production volumes

- Access capital markets for working capital during margin compression periods

- Implement cost reduction initiatives through operational scale

The consolidation timeline depends heavily on government intervention policies. As one industry expert noted, "Government intervention policies that support struggling manufacturers may extend the consolidation period, while market-driven dynamics would accelerate industry restructuring toward sustainable competitive structures."

Innovation and Efficiency Drivers

Cost pressures accelerate technological innovation focused on material efficiency and alternative technologies. Research and development priorities shift toward:

- Sodium-ion battery chemistry to reduce lithium dependence

- Silicon carbide semiconductors for improved power efficiency

- Lightweight materials to reduce metal content per vehicle

- Modular manufacturing approaches to improve production efficiency

Alternative material research receives increased investment attention as companies seek to reduce exposure to volatile commodity markets. Solid-state battery technology development accelerates as manufacturers pursue lithium-efficient energy storage solutions.

The next major ASX story will hit our subscribers first

Global Context and Competitive Positioning

China's electric vehicle cost pressures exist within broader global industry dynamics that affect competitive positioning across international markets. Chinese manufacturers face unique challenges compared to global competitors due to supply chain concentration and domestic market characteristics.

International Market Context

Chinese electric vehicle manufacturers demonstrate cost advantages in labour and manufacturing scale that partially offset commodity cost pressures. However, rising metal and memory prices in China's EV industry impact global production equally, reducing China's relative cost advantages.

Regional supply chain vulnerabilities create different cost structures across major manufacturing centres:

- China: High concentration in battery supply chain, semiconductor vulnerability

- Europe: Raw material import dependence, regulatory compliance costs

- United States: Limited battery manufacturing capacity, supply chain reshoring costs

- Japan/Korea: Advanced semiconductor capabilities, limited raw material access

Currency impact on material costs provides competitive advantages for manufacturers with diversified currency exposure. Chinese manufacturers primarily operate in RMB-denominated cost structures while competing in USD-denominated export markets.

Export Market Implications

Rising domestic production costs affect Chinese manufacturers' export competitiveness across key international markets. European and North American markets implement additional tariffs and regulatory requirements that compound cost pressures. According to CnEVPost analysis, these rising costs are creating significant headwinds for Chinese electric vehicle exports.

Strategic responses include:

- Local manufacturing investments to avoid trade barriers

- Premium positioning to justify higher pricing in export markets

- Technology licensing arrangements with international partners

- Joint venture structures for market access and cost sharing

Furthermore, Chinese automakers face additional pressure as memory chip prices surge amid global demand, creating supply chain bottlenecks that extend beyond national borders.

Mitigation Strategies for Industry Stakeholders

Stakeholders across the electric vehicle ecosystem require comprehensive strategies to address sustained cost inflation while maintaining competitive positioning. These strategies span short-term tactical responses and long-term strategic adaptations.

Short-Term Tactical Responses

Inventory management becomes critical for navigating commodity price volatility. Companies optimise procurement timing through:

- Strategic stockpiling during price valleys for key materials

- Just-in-time adjustments for non-critical components

- Supply contract renegotiation with flexible pricing mechanisms

- Product mix optimisation toward higher-margin vehicle segments

Pricing strategy adjustments require careful balance between cost recovery and market share preservation:

- Selective price increases on premium models with lower demand elasticity

- Value-added feature bundling to justify higher pricing

- Financing incentives to offset sticker price increases for consumers

- Trade-in programmes to maintain sales volume despite higher prices

Long-Term Strategic Adaptations

Technology roadmap adjustments focus on reducing exposure to volatile material markets while maintaining product competitiveness. Key priorities include:

- Battery chemistry diversification beyond lithium-dependent technologies

- Semiconductor architecture optimisation to reduce memory requirements

- Manufacturing process innovation to improve material efficiency

- Supply chain regionalisation to reduce transportation and currency risks

Partnership strategies enable resource sharing and risk distribution across industry participants. Collaborative approaches include:

- Joint procurement initiatives for commodity purchasing power

- Technology sharing agreements for research and development costs

- Manufacturing partnerships for scale economies in production

- Financial partnerships for working capital during margin compression

Investment Decision Framework and Strategic Planning

The current cost inflation environment requires sophisticated analysis frameworks for investment decisions across China's electric vehicle industry. Traditional valuation models require adjustment to account for sustained margin pressure and industry restructuring dynamics.

Risk Assessment Criteria

Investment analysis must incorporate multiple risk factors unique to the current market environment:

Operational Risk Factors:

- Commodity price volatility exposure across key materials

- Supply chain concentration in critical component categories

- Technology transition risks from emerging alternatives

- Regulatory compliance cost escalation

Financial Risk Factors:

- Working capital requirements during margin compression

- Access to capital markets for operational funding

- Currency exposure for internationally active companies

- Debt service capability under reduced profitability

Strategic Risk Factors:

- Market share sustainability under pricing pressure

- Competitive positioning against consolidated industry leaders

- Technology differentiation maintenance during cost cutting

- Brand value preservation through industry restructuring

Due Diligence Considerations

Material cost volatility requires enhanced due diligence processes that evaluate companies' exposure and mitigation capabilities:

- Supply contract analysis for fixed-price vs. spot-market exposure

- Inventory management practices and working capital efficiency

- Vertical integration levels and supplier relationship strength

- Technology roadmap alignment with cost reduction priorities

Portfolio diversification strategies should account for correlation between industry participants during systematic cost shocks. Traditional sector diversification may provide limited protection when entire industries face identical cost pressures simultaneously.

How Should Companies Model Different Scenarios?

Effective strategic planning requires comprehensive scenario analysis that addresses multiple potential cost trajectory paths:

Optimistic Scenario:

- Commodity prices stabilise at current levels by Q3 2026

- Memory chip supply increases through capacity expansion

- Government implements targeted industry support measures

- Export markets provide pricing power for premium products

Base Case Scenario:

- Continued cost volatility with gradual stabilisation through 2027

- Industry consolidation accelerates with 25-30% participant reduction

- Technology innovation partially offsets material cost increases

- Market share redistribution toward financially stronger companies

Pessimistic Scenario:

- Sustained commodity price increases through 2026-2027

- Memory chip shortages persist due to AI infrastructure competition

- Consumer demand contraction due to affordability constraints

- Government support programmes remain limited due to fiscal pressures

Investment timing considerations vary significantly across scenarios. Market entry during consolidation periods may provide acquisition opportunities, while established market positions face different optimisation requirements.

Competitive advantage sustainability depends on companies' ability to navigate cost pressures while maintaining technological leadership and market positioning. Organisations with superior cost management capabilities and financial resources demonstrate improved probability of market share gains during industry stress periods.

The convergence of rising metal and memory prices in China's EV industry represents more than temporary market volatility. These dynamics signal fundamental shifts in global resource allocation, technological competition, and industry structure that will shape the electric mobility landscape for years to come. In addition, stakeholders who develop comprehensive strategies addressing both immediate cost pressures and long-term structural changes position themselves most effectively for sustained success in this evolving marketplace.

Looking to Capitalise on China's EV Industry Transformation?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications about significant ASX mineral discoveries, helping you identify opportunities in the metals and materials driving global electric vehicle production. With lithium prices surging 131% and unprecedented demand for critical minerals across automotive supply chains, stay ahead of major discoveries that could reshape commodity markets.