June 19, 2026

The Structural Shift Rewriting Global Oil Market Logic

For most of modern energy market history, the conventional wisdom held firm: close the Strait of Hormuz, and crude prices detonate. Analysts modelled geopolitical disruptions through a relatively simple framework, one where physical supply shortfalls translated mechanically into price spikes, and where demand was treated as a rigid, inelastic constant. That framework is now structurally compromised, and the mechanism responsible is China flex crude supply and oil prices — specifically, China's demonstrated capacity to flex its crude oil consumption on a scale nobody had fully modelled.

Understanding why that framework broke down matters more than simply observing that it did. The answer lies not in a single policy decision or temporary anomaly, but in a compounding set of structural changes to how China sources, stores, and substitutes its hydrocarbon energy base.

When big ASX news breaks, our subscribers know first

The $150 Oil Forecast That Never Arrived

When geopolitical risk in the Middle East escalated sharply in early 2026, the weight of analytical consensus pointed toward a dramatic crude price spike. Forecasts of $150 to $200 per barrel circulated widely, anchored to historical precedent and the assumption that any meaningful disruption to Hormuz transit flows would overwhelm available supply buffers. These predictions were not fringe views. They were the considered output of sophisticated market participants drawing on decades of precedent.

The market told a different story almost immediately. Brent crude failed to breach $100 per barrel despite one of the largest simultaneous supply disruptions in modern energy market history, estimated at roughly 8 million barrels per day at its peak. Rather than confirming the extreme thesis, price action consistently faded each spike, forcing a fundamental reassessment. This dynamic is broadly consistent with oil price rally patterns observed during other periods of elevated geopolitical tension.

What the Market Was Actually Pricing

The divergence between forecast and outcome was not a market failure. It was the market correctly pricing a variable that most models had underweighted: China's demand elasticity. Rather than absorbing every barrel at any price as legacy frameworks assumed, China demonstrated that it could meaningfully reduce crude imports while keeping its economy operational. That single capability changed everything.

Markets that are globally traded, deeply liquid, and populated by sophisticated actors — including national oil companies, sovereign wealth funds, and dark trading houses — are extraordinarily difficult to manipulate over extended periods. When prices persistently refused to confirm the $150 narrative, the evidence-based response was to question the thesis, not the market.

What China's Flex Crude Capacity Actually Means

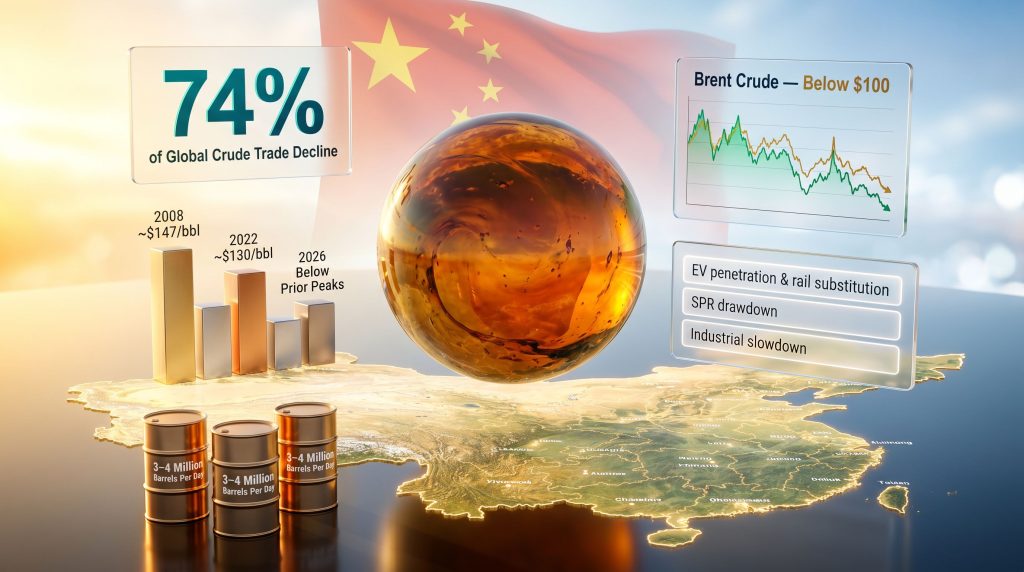

The term flex crude supply refers to China's structural ability to reduce its crude oil import volumes rapidly, substantially, and for extended durations without triggering acute economic disruption. This is not a theoretical model. During the 2026 disruption period, China demonstrated it could reduce crude intake by an estimated 3 to 4 million barrels per day, sustained over weeks and potentially months.

To put that figure in context, it represents a demand withdrawal roughly equivalent to the total crude output of a major OPEC member. When one country can turn that volume on and off in response to price signals, the global market's price formation mechanism changes at its foundation. Furthermore, OPEC's market influence must now be assessed alongside China's demand-side flexibility as a co-determining force in global price formation.

China's proven ability to reduce crude imports by 3 to 4 million barrels per day, sustained over an extended period, represents a structural recalibration of how global oil demand inelasticity should be modelled, not a temporary anomaly driven by short-term circumstance.

The Three Structural Drivers Behind the Reduction

China's flex capacity did not emerge from a single policy lever. It reflects the convergence of at least three distinct structural forces operating simultaneously:

| Demand Reduction Driver | Estimated Daily Impact | Duration Outlook |

|---|---|---|

| EV penetration and high-speed rail substitution | Structural displacement of liquid fuel demand | Long-term, permanent |

| Strategic Petroleum Reserve drawdown | Approximately 1 to 1.5 million bbl/day buffer | Finite, measured in months |

| Industrial and petrochemical slowdown | Cyclical, amplified by trade headwinds | Medium-term |

Driver 1: The Transport Substitution Effect. China's electric vehicle penetration rate and the scale of its high-speed rail network have created a genuine structural reduction in liquid fuel demand for personal and freight transport. Unlike inventory-based buffers, this displacement is not reversible. As EV adoption continues, the baseline level of crude required per unit of economic output continues to decline.

Driver 2: Strategic Reserve Deployment. China operates one of the world's largest strategic petroleum reserves, estimated at approximately 1.4 billion barrels. Drawing on these reserves allows China to maintain industrial throughput while simultaneously reducing spot market crude purchases. This buffer is finite, but its scale provides meaningful insulation over a conflict timeline measured in months rather than years.

Driver 3: Industrial Demand Compression. Trade-related headwinds, particularly those linked to tariff escalation — and closely connected to the broader US-China trade war — compressed petrochemical and industrial activity in China during the same period. This cyclical reduction compounded the structural and strategic factors to produce an aggregate demand reduction of extraordinary scale.

China's Share of the Global Trade Decline

The arithmetic of what occurred in global crude markets during the 2026 disruption is striking. China's reduction in crude imports, estimated at approximately 3 million barrels per day, accounted for roughly 74% of the total decline in global crude trade over the same period. This single figure reframes the entire discussion about oil price formation.

An 8 million barrel per day supply disruption, in prior market regimes, would have been expected to produce violent and sustained upward price pressure. Instead, Chinese demand withdrawal absorbed the majority of the supply loss before it could fully propagate into physical market tightness. Brent crude remained below $100 per barrel throughout.

This outcome was not coincidental. It reflects a structural shift in how the largest marginal buyer of crude oil on the planet interacts with supply shocks. The consequence for price modelling is significant: the geopolitical risk premium embedded in crude oil prices must be recalibrated downward to reflect this demonstrated demand elasticity. According to analysis from Kpler, the real oil shock may only materialise when China returns to spot markets as a buyer, rather than during the supply disruption itself.

The Inventory Ceiling Problem and the Restocking Risk

The China flex crude story has a critical second chapter that investors must not overlook. Commercial petroleum reserves drawn down during a supply shock cannot remain at reduced levels indefinitely. Operational minimums exist, and once those thresholds approach, China will be compelled to return to spot markets as an aggressive buyer.

Once China's commercial petroleum reserves approach operational minimum thresholds, the country re-enters spot markets with substantial restocking demand, potentially triggering a sharp and rapid repricing of crude from current depressed levels.

Key Signals Worth Monitoring

Investors tracking the restocking trigger should watch for:

- Chinese commercial crude inventory data approaching multi-year lows

- A resumption of normal or above-average crude import volumes in tanker tracking data

- Widening backwardation in forward Brent curves signalling near-term physical tightness

- Chinese refinery utilisation rates recovering toward pre-disruption norms

The timing of restocking remains uncertain. What is not uncertain is that it will occur, and that the price impact could be sharp given how aggressively inventories were drawn down during the conflict period.

How China Redefined Hydrocarbon Fungibility

Perhaps the deepest structural implication of the 2026 experience is what it revealed about the convergence of hydrocarbon energy carriers at the margin. For China, crude oil is not an irreplaceable input. It is one of several hydrocarbons, each with different price points, that can be substituted against one another within its industrial and energy system.

| Hydrocarbon | Approximate Price (Barrel of Oil Equivalent) | Premium vs. Crude |

|---|---|---|

| US Natural Gas | Approximately $15/boe | Significant discount |

| Natural Gas Liquids (NGLs) | Approximately $35 to $40/boe | Moderate discount |

| Crude Oil (WTI) | Approximately $73 to $75/bbl | Benchmark |

If coal, natural gas, and natural gas liquids can all serve as partial substitutes for crude at the margins — and China just demonstrated that those margins are far wider than previously assumed — then the structural price premium crude commands over alternative hydrocarbons must compress over time. The arbitrage between energy carriers can only persist while real-world substitution is difficult or slow. China proved it is neither.

This has a direct implication for long-term crude oil price ceilings. If natural gas trades at roughly $15 per barrel of oil equivalent and NGLs at $35 to $40, and China can systematically substitute away from crude at scale, then crude's structural price ceiling is materially lower than pre-2026 consensus models assumed.

The next major ASX story will hit our subscribers first

Three Decades of Fading Geopolitical Super-Spikes

The 2026 experience does not stand alone. Viewed across a 25-year inflation-adjusted price history of WTI crude, a clear pattern emerges: each successive geopolitical super-spike has produced a progressively lower real price peak.

| Oil Price Super-Spike | Nominal Peak | Inflation-Adjusted Peak | Primary Trigger |

|---|---|---|---|

| 2008 | Approximately $147/bbl | High | Peak oil fears, financial speculation |

| 2022 | Approximately $130/bbl | Moderate | Russia-Ukraine conflict, sanctions |

| 2026 | Below prior peaks | Lower in real terms | Iran conflict, Hormuz transit risk |

This declining pattern is not random. It reflects the cumulative effect of energy system resilience building, demand diversification, expanding alternative supply sources, and now, China's demonstrated flex capacity. Each crisis teaches the global energy system something new about how to absorb shocks, and each subsequent crisis encounters a more adaptive system.

For investors, the long-run implication is uncomfortable but clear: treating geopolitical oil spikes as buying opportunities rather than fading opportunities carries a structurally deteriorating risk-reward profile. The market's repeated refusal to confirm extreme price theses is itself the signal.

Copper, Silver, Uranium, and Gold: Broader Commodity Implications

The structural logic that has capped crude oil's geopolitical premium applies, with varying intensity, across the broader commodity complex.

Copper and the Counterintuitive Grade Argument

The standard bull thesis for copper rests partly on declining ore grades at existing mines. As grades fall, the argument goes, supply becomes more constrained and prices must rise. However, current copper market trends suggest this narrative deserves scrutiny. As mining companies develop profitable extraction methods at progressively lower ore grades, the economically viable copper resource base expands dramatically.

A grade threshold of 0.5% copper that was once uneconomic becomes a viable target once processing technology improves, and at that point, a vastly larger pyramid of previously stranded resource becomes accessible. Declining copper grades, viewed through this lens, are structurally deflationary rather than inflationary for long-term copper prices.

An additional demand-side consideration worth noting: solar panel installations in China, which represent a significant source of copper and silver demand, appear to have peaked in 2025 following a government incentive-driven rush to complete projects. New solar installations in China declined markedly in 2026, removing a significant demand tailwind that copper and silver bulls had relied upon heavily in their forecasts.

Uranium: The Structural Exception

Uranium occupies a unique position in the commodity framework. While the long-term real price trajectory of most commodities trends lower, uranium has a specific structural characteristic that warrants separate consideration: the concentration of market accumulation by a single large, legally operating entity that has explicitly stated its intent to accumulate physical uranium supply.

There is a second distinguishing feature. Uranium's cost as a percentage of total nuclear power plant operating expenses is extraordinarily small. A doubling or tripling of uranium prices would have negligible impact on electricity generation economics, meaning demand destruction from price increases is essentially non-existent. This price inelasticity at the demand side makes uranium's supply-demand dynamics meaningfully different from crude oil or copper.

Silver's Solar Dependency

Silver carries an echo of monetary metal status but functions primarily as an industrial commodity. Its fortunes are closely tied to solar panel manufacturing demand, which, as noted above, appears to be softening in China. The supply side presents an unusual structural constraint: the majority of silver production occurs as a byproduct of mining other metals, meaning supply cannot respond rapidly to demand shortfalls. This cuts both ways. A new mine opened primarily for copper or lead will dump its silver byproduct into the market regardless of silver's price trajectory.

Gold as a Monetary Reserve Asset

Gold occupies a fundamentally different category from the commodities discussed above. Its primary economic function is not industrial consumption but rather serving as a neutral reserve asset for the settlement of international trade imbalances. In addition, the gold market outlook points to growing structural demand as the world transitions from unipolar toward multipolar international monetary arrangements. This reserve diversification trend is likely to persist regardless of short-term price volatility. Research from the Columbia University Energy Policy Center further contextualises how China's energy security strategy intersects with broader shifts in commodity and reserve asset positioning.

Frequently Asked Questions: China Flex Crude Supply and Oil Prices

What does flex crude supply mean in the context of China's energy strategy?

Flex crude supply refers to China's demonstrated ability to rapidly reduce its crude oil import volumes by several million barrels per day over extended periods. This capability is enabled by strategic reserve drawdowns, fuel substitution across alternative hydrocarbons, and structural reductions in liquid fuel demand driven by EV adoption and high-speed rail use.

How did China manage to keep oil prices below $100 during a major supply disruption?

China's reduction of approximately 3 million barrels per day in crude imports absorbed around 74% of the total decline in global crude trade during the 2026 disruption. This demand withdrawal offset the majority of the supply shock before it could propagate fully into physical market tightness.

Will oil prices spike when China resumes normal crude imports?

A restocking-driven price recovery is possible, particularly if Chinese commercial inventories approach operational minimums simultaneously with a return to normal import patterns. The scale and speed of any price move will depend on how quickly China re-enters spot markets and what OPEC production levels look like at that time.

Is China's strategic petroleum reserve large enough to sustain current import reductions?

China's strategic petroleum reserve is estimated at approximately 1.4 billion barrels. At a drawdown rate of 1 to 1.5 million barrels per day, this reserve provides a buffer measured in months rather than years. It is a finite mechanism, not a permanent solution.

How does China's hydrocarbon substitution affect long-term crude oil pricing?

If China can substitute crude with natural gas, NGLs, and coal at the margins, the arbitrage between these energy carriers must eventually close. Given that natural gas trades at roughly $15 per barrel of oil equivalent and NGLs at $35 to $40, crude oil's structural price ceiling is lower than pre-2026 models assumed. Consequently, China flex crude supply and oil prices are now inextricably linked in any credible long-term pricing model.

What does the 2026 oil market response reveal about the future of geopolitical risk premiums?

Each successive geopolitical oil shock since 2008 has produced a lower inflation-adjusted price peak. This pattern suggests that geopolitical risk premiums embedded in crude prices are structurally declining as energy systems become more resilient, diversified, and adaptive. Investors who treat geopolitical spikes as buying rather than fading opportunities face deteriorating risk-reward outcomes.

Key Takeaways for Energy Market Investors

- China's capacity to reduce crude imports by 3 to 4 million barrels per day is now a proven and repeatable market mechanism, not a theoretical model

- China accounted for approximately 74% of the total decline in global crude trade during the 2026 disruption, demonstrating the outsized influence of Chinese demand elasticity on global price formation

- Brent crude's failure to breach $100 during an 8 million barrel per day supply disruption represents a permanent recalibration of oil's geopolitical risk premium

- The convergence of hydrocarbon energy carriers at the margin suggests crude oil's structural price ceiling is materially lower than pre-2026 consensus models assumed

- The long-term real price trajectory of most commodities trends lower as extraction technology improves and substitution options expand

- Investors who treat geopolitical oil spikes as buying rather than fading opportunities face a structurally deteriorating risk-reward profile going forward

- Gold, classified as a monetary metal rather than a commodity, stands as a structural exception to the deflationary commodity thesis in a multipolar reserve diversification environment

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any financial product, security, or commodity. All forecasts and projections discussed involve uncertainty and should not be relied upon as predictions of future outcomes. Past price behaviour is not indicative of future results. Readers should conduct their own research and consult a qualified financial adviser before making any investment decisions.

Want to Capitalise on the Next Major Mineral Discovery Before the Market Moves?

While energy market dynamics continue to reshape global commodity pricing, significant mineral discoveries on the ASX represent a distinct category of opportunity — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those discoveries are announced, translating complex geological data into actionable insights for investors at every level. Explore historic discovery returns to understand the scale of opportunity, then begin your 14-day free trial to position yourself ahead of the broader market.