May 12, 2026

The global lithium market operates within complex cycles where industrial demand patterns, technological adoption rates, and geopolitical tensions create volatile pricing environments. As electric vehicle penetration accelerates worldwide and battery energy storage systems expand across multiple sectors, lithium's role as a critical mineral intensifies. These fundamental dynamics create market conditions where China lithium prices tumble scenarios emerge alongside rapid supply and demand imbalances across international markets.

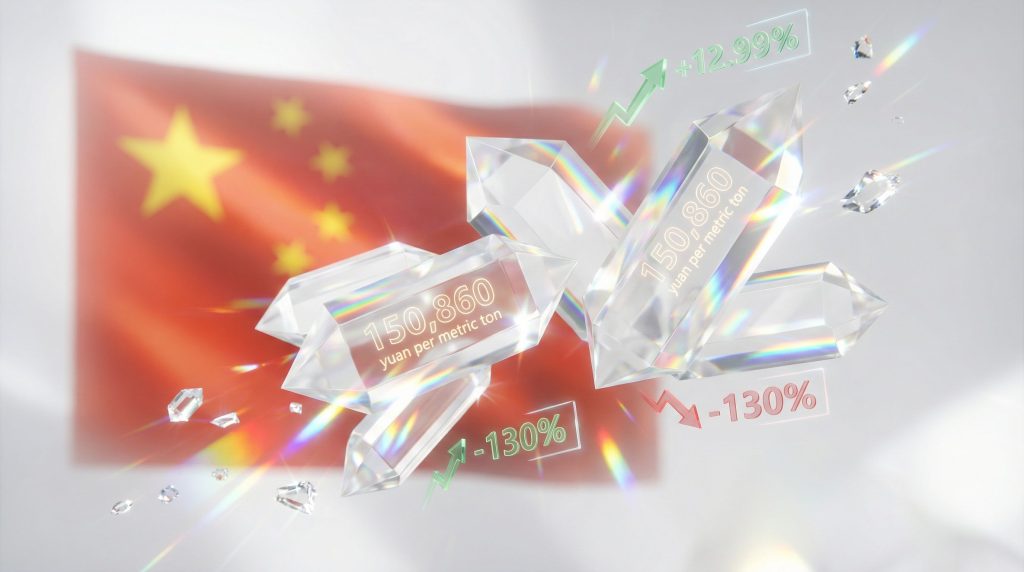

Understanding China's Lithium Market Turbulence

China's lithium carbonate futures experienced dramatic price movements in early 2026, with the most-active contract on the Guangzhou Futures Exchange declining 12.99% to close at 150,860 yuan per metric ton. This sharp decline brought prices dangerously close to the exchange's 13% daily limit, demonstrating the intensity of market sentiment shifts within China's commodity trading environment.

The magnitude of this single-day movement becomes more significant when contextualized against lithium's 130% price recovery from 2025 lows. This recovery had positioned the market for potential stabilisation before the recent dramatic reversal, highlighting the commodity's susceptibility to rapid revaluation cycles.

Daily limit mechanisms on Chinese futures exchanges serve as circuit breakers designed to prevent excessive volatility during periods of intense market stress. When China lithium prices tumble approaches the 13% threshold, it signals that market participants are rapidly reassessing fundamental value propositions without triggering complete trading halts.

The Guangzhou Futures Exchange's price discovery mechanism during this period revealed how quickly lithium markets can shift from recovery optimism to demand uncertainty. The speed of this transition underscores the commodity's sensitivity to both macroeconomic conditions and sector-specific developments across the electric vehicle and energy storage industries.

When big ASX news breaks, our subscribers know first

Electric Vehicle Sales Weakness Impacts Lithium Demand

February 2026 electric vehicle sales data from China revealed significant demand deterioration across major manufacturers. BYD, the world's largest EV producer by volume, reported sales declining more than 40% year-over-year during the month, according to lithium prices in China data. This performance from the industry leader signalled broader consumer purchasing hesitation within China's electric vehicle sector.

The timing of these sales declines coincided with lithium's price volatility, demonstrating the direct relationship between downstream demand patterns and upstream commodity pricing. As the largest consumer of lithium for battery production, China's EV market performance directly influences global supply-demand balance calculations.

Several factors contribute to EV sales fluctuations in China's market environment:

• Seasonal purchasing patterns following Lunar New Year celebrations

• Consumer confidence levels amid broader economic uncertainty

• Government incentive policy changes affecting purchase subsidies

• Technology transition periods as manufacturers introduce new battery chemistries

• Regional demand variations between urban and rural markets

The distinction between seasonal and structural demand weakness becomes critical for lithium market participants. February typically experiences post-holiday slowdowns in China's automotive sector, but the magnitude of BYD's decline suggested deeper market challenges beyond normal seasonal adjustments.

Production capacity utilisation rates across China's EV manufacturing base declined as companies adjusted output to match weaker consumer demand. This capacity adjustment directly impacted battery procurement schedules, creating ripple effects throughout the lithium supply chain from refiners to converters to cathode material producers.

Furthermore, the battery recycling breakthrough initiatives in China may provide alternative lithium sources, potentially affecting traditional mining demand patterns.

Geopolitical Tensions Create Demand Uncertainty

Middle East regional conflicts introduced additional complexity to lithium demand forecasting, particularly impacting China's battery energy storage system export prospects. The region represents one of the fastest-growing markets for Chinese BESS technology, but escalating tensions created uncertainty around infrastructure investment timelines and trade continuity.

Geopolitical risk factors affecting lithium markets include:

• Trade route disruptions impacting shipping costs and delivery schedules

• Infrastructure project delays in conflict-affected regions

• Risk premium adjustments in commodity futures pricing

• Alternative market development as companies diversify geographic exposure

• Supply chain security reassessment by major consuming industries

The battery energy storage market's growth trajectory in the Middle East had been supporting bullish lithium demand projections through 2026-2027. Regional governments' commitments to renewable energy infrastructure and grid modernisation projects created significant lithium consumption potential through utility-scale storage installations.

However, conflict escalation forced lithium market participants to reassess the reliability of this demand growth. The Middle East exploration impact on global lithium supply chains became increasingly significant as companies sought alternative regional strategies.

Chinese battery manufacturers had positioned the Middle East as a strategic growth market for both residential and commercial energy storage systems. Export volumes to the region represented an important demand component supporting lithium price recovery efforts throughout 2025 and early 2026.

Market Response to Regional Instability

Risk premium calculations in lithium futures markets began incorporating geopolitical uncertainty premiums, though quantifying these impacts remained challenging given the complexity of regional supply chain relationships and alternative market substitution possibilities.

The interconnected nature of global lithium markets means that regional disruptions can have cascading effects across multiple continents. This interconnectedness highlights the importance of diversified supply chains and strategic inventory management.

Supply Constraint Developments Shape Market Dynamics

Zimbabwe's decision to suspend lithium concentrate and raw mineral exports created significant supply-side support for global lithium markets prior to the recent price decline. This policy intervention aimed to encourage domestic refining capacity development while capturing more value-added processing within Zimbabwe's borders.

The suspension impacted global supply chain dynamics by:

• Reducing raw material availability for international refiners

• Encouraging local processing investment within Zimbabwe

• Creating short-term supply tightness in concentrate markets

• Shifting trade flow patterns toward alternative suppliers

• Supporting price floors through reduced export volumes

Zimbabwe's lithium reserves rank among the world's largest, making export policy changes particularly significant for global supply balance calculations. The country's shift toward value-added processing reflects broader trends among resource-rich nations seeking to capture more economic value from natural resource endowments.

Local refining capacity development requires substantial capital investment and technical expertise, creating implementation timelines extending several years. During this transition period, global lithium markets must adjust to reduced raw material availability from Zimbabwe's operations.

In addition, developments in geothermal lithium extraction technologies are providing new supply sources that could help offset traditional mining constraints.

Regional Supply Chain Evolution

Regional supply chain reconfiguration effects extended beyond Zimbabwe as other African lithium producers evaluated similar value-addition strategies. Mali, Ghana, and the Democratic Republic of Congo began considering export restriction policies to encourage domestic processing development.

International lithium consumers responded by diversifying supply sources and evaluating vertical integration opportunities to reduce exposure to export policy changes. This strategic shift influenced investment patterns across the lithium value chain from mining through battery manufacturing.

Infrastructure Investment Supporting Long-Term Demand Growth

China's commitment to expanding electric vehicle charging infrastructure represents a critical demand driver for lithium consumption through 2027 and beyond. Charging network expansion requires substantial battery energy storage integration to manage grid stability and peak demand management across urban and rural deployment areas.

Key infrastructure development areas include:

• Public charging station networks requiring grid-connected storage systems

• Private residential charging infrastructure with integrated battery backup

• Commercial fleet charging facilities incorporating demand management storage

• Highway corridor charging networks requiring high-capacity energy storage

• Rural electrification programmes combining renewable generation with lithium storage

Energy storage market growth projections indicate significant expansion across multiple applications beyond electric vehicle charging. Data centre power requirements continue increasing as cloud computing and artificial intelligence applications expand, creating sustained lithium demand from backup power and grid stabilisation systems.

Industrial energy storage adoption accelerated across China's manufacturing sectors as companies sought to manage electricity costs and improve power quality. Large-scale industrial facilities began integrating megawatt-hour scale battery systems for peak shaving and renewable energy integration purposes.

Grid modernisation initiatives throughout China required substantial battery energy storage deployment to manage variable renewable energy sources and improve system reliability. These utility-scale projects represented some of the largest single sources of lithium demand growth across the energy storage sector.

The convergence of electric vehicle adoption, renewable energy expansion, and grid modernisation created multiple overlapping demand streams supporting long-term lithium consumption growth despite near-term volatility in specific market segments.

Investment Implications and Market Analysis

Technical analysis of lithium futures behaviour on the Guangzhou Futures Exchange revealed important patterns during the 12.99% decline period. The speed and magnitude of price movements indicated institutional participation rather than retail-driven volatility, suggesting sophisticated market participants were rapidly repositioning based on fundamental reassessments.

The proximity to daily limit thresholds demonstrated how quickly sentiment shifts can impact lithium pricing mechanisms. When futures contracts approach exchange-imposed limits, it indicates the market is attempting to price in substantial valuation changes without triggering circuit breaker halts.

Volume and open interest metrics during volatile periods provide insights into market participation patterns and position liquidation pressures. However, detailed trading data from the Guangzhou Futures Exchange requires direct access to official exchange reporting systems.

Fundamental value assessment frameworks for lithium markets must incorporate multiple variables:

| Assessment Factor | Key Metrics | Impact on Pricing |

|---|---|---|

| Production Costs | Cash costs per tonne, all-in sustaining costs | Establishes price floors |

| Demand Elasticity | EV adoption sensitivity, BESS growth rates | Determines demand response |

| Supply Flexibility | Capacity expansion timelines, inventory levels | Influences supply response |

| Inventory Cycles | Pipeline stock levels, strategic reserves | Creates price volatility |

Long-term supply-demand balance projections through 2030 must account for both demand growth acceleration and supply capacity additions. Electric vehicle penetration rates, battery energy storage deployment schedules, and new lithium production capacity all influence fundamental value calculations.

Market Correlation Analysis

Correlation analysis with broader commodity market movements provides context for lithium's price behaviour during risk-on and risk-off market environments. Industrial metals, energy commodities, and precious metals often exhibit related movement patterns during macroeconomic uncertainty periods.

Current commodity trading data shows how lithium correlates with broader industrial metal trends, particularly during periods of economic uncertainty.

The next major ASX story will hit our subscribers first

Market Recovery Indicators and Future Outlook

Short-term price stabilisation factors for China lithium prices tumble recovery depend on several key market developments. Inventory level adjustments throughout the supply chain create potential demand support as downstream consumers maintain strategic stock levels despite current price volatility.

Seasonal demand pattern normalisation expectations focus on whether February 2026 weakness represents typical post-holiday slowdowns or indicates structural demand deterioration. Historical monthly demand patterns provide baseline comparisons for assessing current market conditions.

Producer margin sustainability becomes critical as lithium prices approach operational break-even levels for higher-cost operations. Mining companies with elevated production costs may reduce output if prices remain below cash cost thresholds for extended periods.

Key recovery indicators to monitor include:

• EV sales normalisation in March and April 2026 data releases

• Battery energy storage project announcements and installation schedules

• Inventory draw-down patterns across refiners and converters

• Producer capacity utilisation rates and production guidance updates

• Futures market positioning through commitment of traders reports

Long-term growth driver analysis supports continued lithium demand expansion despite near-term volatility. The lithium industry innovations in Australia and other markets continue driving technological advancement and cost reduction initiatives.

Technology and Market Development

Lithium iron phosphate (LiFePO4) technology adoption rates continue increasing as battery manufacturers optimise cost structures and performance characteristics. LFP chemistry requires substantial lithium content while offering competitive advantages in certain applications, supporting sustained demand growth.

Global electric vehicle penetration targets established by various national governments provide policy support for lithium demand expansion through the remainder of the decade. These commitments create minimum demand floors even during cyclical market weakness periods.

Additionally, insights from lithium brine insights in Argentina show how new extraction methods are expanding global supply potential.

Strategic Positioning for Market Participants

Price range expectations for lithium markets focus on establishing sustainable trading ranges between 150,000-200,000 yuan per tonne based on current cost structures and demand fundamentals. Factors supporting higher price floors include production cost inflation and supply constraint developments, while downside risks include demand destruction from economic slowdowns or technology substitution.

Investment thesis development requires careful consideration of value chain positioning strategies. Upstream exposure through mining companies offers leverage to commodity price recovery but includes operational and geological risks. Downstream positioning through battery manufacturers or electric vehicle companies provides demand growth exposure while reducing direct commodity price sensitivity.

Geographic diversification benefits become increasingly important as lithium markets mature and regional supply-demand imbalances create arbitrage opportunities. Projects in stable jurisdictions with established regulatory frameworks may command valuation premiums despite potentially higher development costs.

Technology integration opportunities across processing and recycling segments offer additional value creation potential. As lithium demand growth continues, recycling technologies become economically viable and strategically important for supply security.

Risk assessment frameworks must incorporate multiple scenario analyses including demand growth acceleration, supply constraint intensification, and technology disruption possibilities. Sodium-ion battery development represents a potential substitution threat in certain applications, though lithium's performance advantages maintain market share in premium segments.

Market participants should monitor regulatory developments across major consuming regions as governments implement critical mineral security policies. Strategic stockpiling programmes, domestic processing requirements, and supply chain resilience initiatives may create additional demand sources supporting long-term price stability.

The convergence of electrification trends, energy storage expansion, and grid modernisation requirements creates multiple reinforcing demand drivers supporting lithium market fundamentals despite periodic volatility from economic cycles or geopolitical events.

Looking to Capitalise on Lithium Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX lithium discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage in the volatile commodities sector.