June 7, 2026

The Hidden Architecture of a Supply Chain the World Cannot Afford to Lose

Global rare earth markets operate on a paradox that most investors and policymakers have yet to fully internalise: the elements most critical to electric vehicles, wind turbines, precision-guided weapons, and consumer electronics pass through one of the world's most politically fractured corridors before they ever reach a refinery. Understanding how China Myanmar border trade and mining cooperation actually functions, beneath the diplomatic surface, reveals a supply architecture built on conflict tolerance, dual-track engagement, and structural dependency that no policy framework has yet managed to untangle.

This is not simply a story about two neighbouring nations exchanging goods. It is, furthermore, a case study in how geopolitical leverage, resource geography, and economic asymmetry combine to create a relationship that defies the conventional logic of trade disruption.

When big ASX news breaks, our subscribers know first

Myanmar's Irreplaceable Position in China's Rare Earth Supply Chain

When analysts map global rare earth supply chains, the focus typically falls on China's dominant refining capacity, estimated at approximately 90% of global processing output. Far less attention is paid to where China sources the raw feedstock for that refining infrastructure, particularly for the heavy rare earth elements (HREEs) that are the most strategically sensitive and geographically concentrated of all critical minerals.

Why Heavy Rare Earths Matter So Much

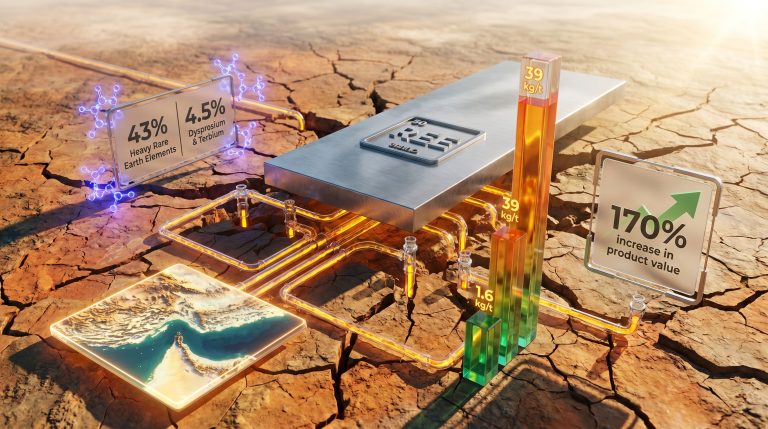

Heavy rare earth elements such as dysprosium, terbium, and holmium are not widely distributed across the earth's crust. They occur in economically extractable concentrations primarily in ion-adsorption clay deposits, a geological formation type found across southern China and, critically, in the upland regions of northern Myanmar. Myanmar has consequently emerged as China's single largest external supplier of heavy rare earth feedstock, reportedly contributing approximately 57% of China's total rare earth imports by value in the first half of 2023, representing an estimated value of around $773 million for that period alone.

What makes this figure geologically significant is that Myanmar's deposits are predominantly ion-adsorption clays, a formation where rare earth ions are loosely bonded to clay mineral surfaces rather than locked within hard-rock crystal structures. This makes them extractable through a relatively low-capital, chemically intensive leaching process, but also means they leave behind substantially damaged terrain.

The two primary extraction zones in Myanmar are Chipwi and Pang Wa districts in Kachin State, along with newer operations expanding into Shan State from approximately 2025 onward. Documented infrastructure in Kachin State alone has grown to include an estimated 370 operational sites and approximately 2,700 leaching ponds, a scale of extraction that reflects years of accelerating activity rather than a sudden surge.

| Commodity | Myanmar's Estimated Share of China's Imports | Approx. Value (H1 2023) | Primary Source Regions |

|---|---|---|---|

| Heavy Rare Earth Elements | ~57% of China's total imports | ~$773 million | Kachin State, Shan State |

| Tin | Significant contributor | Variable | Northern Shan State |

| Rubber and Timber | Secondary exports | Ongoing | Multiple border regions |

The Asymmetric Trade Ledger: Raw Materials Flow One Way, Processed Goods the Other

China's economic relationship with Myanmar is structurally asymmetric in a way that reinforces long-term dependency. Myanmar exports unprocessed or minimally processed raw materials northward into Yunnan Province, while China exports manufactured goods, fertilisers, petroleum products, and steel southward in return. Understanding the rare earth supply chain importance in this context helps clarify why this bilateral relationship carries such outsized global consequences.

In 2023, Chinese exports to Myanmar totalled approximately $9.76 billion, one of the most imbalanced bilateral trade relationships in the Southeast Asian region. Monthly figures illustrate the continued depth of Myanmar's import dependency: in February 2026, Myanmar's imports from China reached approximately $790 million, with Chinese exports to Myanmar including steel and related products estimated at approximately $968 million for that same month across all categories.

The structural reality is that Myanmar functions as a raw material extraction zone feeding China's industrial processing base, while China functions as Myanmar's primary source of manufactured inputs. This configuration reinforces Myanmar's economic dependency and amplifies China's leverage over Myanmar's political trajectory.

This asymmetry is not accidental. It is, however, the logical outcome of decades of investment patterns, infrastructure development, and deliberate supply chain integration that have made Myanmar's northern mining regions economically legible only in relation to Chinese demand.

How the 2021 Coup Reorganised the Physical Geography of Cross-Border Commerce

The February 2021 military coup did not simply disrupt Myanmar's economy. It fundamentally reorganised the spatial architecture of how goods move between Myanmar and China, in ways that have proved more durable than most analysts initially anticipated.

The Redistribution of Border Control

The most important structural change was the redistribution of border control. Prior to 2021, official crossing points such as the Muse border gate in northern Shan State handled the majority of overland trade volume. By mid-2024, conflict-related disruptions had reduced volumes through Muse by an estimated 41 to 46%, as fighting and political instability undermined the operational reliability of junta-controlled crossings.

However, trade did not simply collapse. It rerouted. By 2024, an estimated 91% of overland trade routes between China and Myanmar fell under the operational control of Ethnic Armed Organisations (EAOs) rather than the central military government. This is perhaps the single most important structural fact about China Myanmar border trade and mining cooperation that is consistently underreported in mainstream analysis.

Three Key Trade Corridors

The post-coup period also accelerated the development of three distinct multi-modal trade corridors, as documented research on conflict and development in the Myanmar-China border region has examined in detail:

- Wang Pong Port expansion in Shan State, which absorbed diverted freight volumes from disrupted official crossings and expanded overland freight handling capacity from Yunnan Province.

- The Yunnan-Yangon-Singapore Rail-Road-Sea Route, a multi-modal corridor providing China's landlocked western provinces with access to the Indian Ocean, reducing dependency on the Malacca Strait as a transit chokepoint.

- The Chongqing-Laos-Thailand-Myanmar corridor, connecting China's interior to Southeast Asian maritime networks through a regional integration framework that bypasses politically unstable Myanmar territories where possible.

These corridors align with the China-Myanmar Economic Corridor (CMEC), the bilateral infrastructure framework connecting Yunnan Province to the deep-sea port at Kyaukphyu on Myanmar's Indian Ocean coastline. Myanmar's accession to the Regional Comprehensive Economic Partnership (RCEP) in January 2022 further activated preferential trade linkages, adding a southern maritime dimension to what had previously been a predominantly overland commercial relationship.

The EAO Factor: Why Armed Ethnic Groups Now Determine Trade Flows

The United Wa State Army (UWSA) and the Kachin Independence Organisation (KIO) are the two most consequential non-state actors shaping China-Myanmar commerce. Understanding their role is now a prerequisite for any serious analysis of this bilateral relationship.

The UWSA controls substantial territory in eastern Shan State and has facilitated the expansion of new rare earth mining operations under its governance framework from approximately 2025 onward. Shan State's relative stability under UWSA administration has made it an increasingly attractive operational environment for Chinese mining enterprises seeking alternatives to the more volatile Kachin State operations.

In Kachin State, the 2024 KIO seizure of territory previously held by junta-aligned forces created a brief operational disruption for Chinese mining enterprises, followed by a resumption of activity under KIO governance. The KIO has publicly stated interest in attracting non-Chinese mining partners, partly as a response to sustained community backlash against environmental degradation from chemical leaching processes, though this diversification has not yet materialised at scale.

China has effectively adapted to EAO border dominance by maintaining parallel engagement with both the central government in Naypyidaw and the armed ethnic organisations that physically control the border corridors. This dual-track strategy maximises operational access regardless of which political actor controls specific territories at any given time.

Wang Yi's Naypyidaw Visit: Diplomatic Architecture and Strategic Signalling

Chinese Foreign Minister Wang Yi's April 2026 visit to Naypyidaw, part of a regional circuit encompassing Thailand and Cambodia, confirmed that China-Myanmar economic cooperation remains a high-priority strategic agenda item for Beijing. This occurred despite Myanmar's deteriorating political and security environment, reflecting China's rare earth trade strategy that prioritises resource access over political conditionality.

The official discussion agenda covered border trade resumption, energy cooperation, mining collaboration, agricultural development, and technology transfer. Wang Yi conveyed to Myanmar President Min Aung Hlaing that China views Myanmar as capable of achieving long-term development under its current leadership structure, a diplomatic signal that provides the Myanmar government with a degree of international legitimacy that Western nations and ASEAN have declined to extend.

Min Aung Hlaing, the 69-year-old former military commander, was sworn in as president earlier in April 2026 following an election conducted exclusively in military-controlled territories and widely criticised by international observers. The Myanmar government had also imposed martial law across 60 of the country's 330 townships during the same period, in areas where ethnic armed groups remain operationally active.

ASEAN has maintained its exclusion of Min Aung Hlaing from bloc-level summits since the February 2021 coup. This posture was, however, simultaneously accompanied by Thailand's Foreign Minister offering Myanmar backing for ASEAN normalisation during a parallel diplomatic visit. The convergence of these visits in late April 2026 suggests coordinated regional signalling rather than coincidental diplomatic scheduling, as further explored in reporting on China's diplomatic offensive to support the new Myanmar regime.

The next major ASX story will hit our subscribers first

Ion-Adsorption Clay Mining: The Technical Reality Behind the Supply Chain

One of the most consequential and least understood technical dimensions of Myanmar's rare earth sector is the extraction method itself. The overwhelming majority of heavy rare earth production in both Kachin and Shan States relies on ion-adsorption clay leaching, a process that is low in capital cost but high in environmental consequence. These rare earth processing challenges are increasingly drawing scrutiny from downstream manufacturers and ESG-focused investors.

How Ion-Adsorption Clay Leaching Works

The process works as follows:

- Ion-adsorption clay deposits are identified at or near the surface, typically in tropical upland terrain.

- A chemical solution, most commonly ammonium sulphate or ammonium bicarbonate, is applied to the clay either through heap leaching or in-situ injection.

- The reagent displaces rare earth ions from clay mineral surfaces, creating a pregnant leach solution.

- The solution is then collected, processed, and the rare earth content precipitated for export.

The efficiency of this method depends on deposit grade, clay mineralogy, and reagent concentration. Myanmar's deposits are particularly attractive because of their high relative concentration of the most valuable heavy rare earth elements, including dysprosium and terbium, which command significant price premiums over light rare earths due to their critical role in high-performance permanent magnets used in EV motors and wind turbine generators.

The environmental cost is, furthermore, substantial. Chemical reagent application causes soil acidification, disrupts groundwater chemistry, and produces acid mine drainage that affects downstream agricultural land. The near-complete absence of enforceable environmental regulation in Myanmar's mining zones since 2021 has allowed these impacts to accumulate without meaningful mitigation.

The Regulatory Vacuum and Its Long-Term Consequences

| Dimension | Myanmar | China (Domestic) | Australia | Rest of World |

|---|---|---|---|---|

| Regulatory Oversight | Minimal / Fragmented | Moderate to Strong | High | Variable |

| Environmental Standards | Very Low | Improving | High | Variable |

| Political Risk | Very High | Low | Very Low | Moderate |

| Cost of Production | Very Low | Low to Moderate | Moderate to High | Variable |

| Share of China's REE Imports | ~57% | Domestic supply | Minor | Minor |

The collapse of central government regulatory capacity since 2021 has created conditions where extraction site proliferation is essentially self-regulating, governed more by commercial incentive and EAO tolerance than by any formal permitting regime. This creates three distinct categories of long-term risk:

- ESG liability accumulation: Downstream users of Chinese-refined rare earths face increasing institutional scrutiny over the provenance of Myanmar-sourced feedstock, with sustainability-focused investors and electronics manufacturers beginning to demand supply chain transparency that current opacity makes impossible to provide.

- Operational continuity risk: The absence of formal legal frameworks for mining concessions means Chinese operators depend entirely on informal arrangements with EAOs, arrangements that can be renegotiated or suspended with limited notice when political or military dynamics shift.

- Reputational risk to end-use manufacturers: Consumer electronics companies, EV manufacturers, and defence contractors whose products incorporate rare earth permanent magnets face growing exposure to reputational damage if Myanmar supply chain linkages become more publicly prominent.

Scenario Pathways: How This Relationship Could Evolve Through 2030

Given the structural variables at play, four distinct trajectories deserve analytical attention. These represent scenarios rather than forecasts, and investors and policymakers should consequently treat them as probability-weighted planning frameworks rather than predictive statements.

Scenario 1: EAO Governance Formalisation

EAOs consolidate territorial control, establish quasi-regulatory concession frameworks, and negotiate long-term mining agreements with Chinese state-linked enterprises. Trade volumes stabilise and potentially expand under informal but durable governance arrangements. This trajectory is already partially visible in UWSA-controlled Shan State and represents the most likely near-term baseline.

Scenario 2: Managed Diplomatic Normalisation

Chinese diplomatic pressure, combined with ASEAN engagement and Thailand's mediation efforts, produces a managed ceasefire and partial normalisation. Official border crossings including Muse recover volume and CMEC infrastructure investments accelerate. This scenario, however, requires conflict resolution progress that currently has no clear pathway.

Scenario 3: Supply Chain Disruption From Escalating Conflict

Intensification of fighting across Kachin and Shan States forces operational suspensions at key mining sites, reducing Chinese heavy rare earth import volumes and triggering price volatility in global markets for dysprosium, terbium, and related elements. Precedent exists from partial disruptions in 2023 and 2024. In addition, the rare earth export restrictions already enacted by Beijing in 2025 demonstrate how quickly supply shocks can cascade through global markets.

Scenario 4: Western-Driven Diversification Pressure

ESG-driven institutional pressure, sanctions regime expansion, and consumer electronics manufacturer scrutiny force Chinese refiners to reduce Myanmar feedstock dependency, accelerating investment in domestic ionic clay deposits and alternative supplier nations. This scenario is structurally plausible but economically costly to execute rapidly. Furthermore, given critical minerals demand continuing to accelerate with the energy transition, the urgency of finding alternatives will only intensify through the decade.

Frequently Asked Questions: China Myanmar Border Trade and Mining Cooperation

What minerals does Myanmar supply to China?

Myanmar is China's leading external supplier of heavy rare earth elements, contributing an estimated 57% of China's total rare earth imports. Additional exports include tin, rubber, timber, and select base metals from northern border regions.

How has the 2021 coup affected China-Myanmar trade?

The coup disrupted official border crossing volumes, with the Muse crossing recording declines of 41 to 46% by mid-2024, but simultaneously accelerated alternative trade corridor development and deepened Chinese commercial engagement with ethnic armed organisations that now control approximately 91% of overland border trade routes.

What is the China-Myanmar Economic Corridor?

CMEC is a bilateral infrastructure and investment framework connecting China's Yunnan Province to Myanmar's Indian Ocean coastline, including the deep-sea port at Kyaukphyu. It forms a key component of China's strategy for accessing Indian Ocean maritime routes independent of the Malacca Strait.

Why does China engage with ethnic armed organisations in Myanmar?

Chinese commercial interests require operational access to border regions that EAOs physically control. Maintaining working relationships with groups including the UWSA and KIO allows Chinese enterprises to continue China Myanmar border trade and mining cooperation regardless of which political authority nominally governs the territory.

What are the environmental risks of rare earth mining in Myanmar?

The dominant ion-adsorption clay leaching method produces soil acidification, groundwater contamination, and deforestation. The near-complete absence of regulatory enforcement since 2021 has allowed these impacts to expand without meaningful mitigation across Kachin and Shan State mining corridors.

How significant is Myanmar to global rare earth supply chains?

Given China's control of approximately 90% of global rare earth refining capacity and Myanmar's contribution of the majority of China's heavy rare earth ore imports, disruptions to Myanmar's mining sector carry direct implications for global supplies of elements critical to EV motors, wind turbines, defence systems, and consumer electronics. Mining.com has also reported on China's active efforts to reopen border trade cooperation in mining, underscoring how strategically critical this relationship remains.

Disclaimer: Statistical figures including trade values, import share percentages, and site counts referenced in this article are drawn from industry reporting and available analytical sources as of the publication date. Figures relating to EAO territorial control, extraction site inventories, and forward scenario projections involve estimations and should not be treated as definitive. Readers making investment decisions should consult primary sources and professional financial advice. This article does not constitute investment advice.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

As geopolitical pressure on rare earth and critical mineral supply chains intensifies, Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries — turning complex data across 30-plus commodities into clear, actionable insights for traders and investors alike. Explore how major mineral discoveries have historically delivered extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.