June 29, 2026

The Reserve Architecture Shift Rewriting Global Gold Markets

Sovereign wealth theory has long held that reserve diversification is a slow, deliberate process governed by decades of institutional inertia rather than quarterly market signals. Yet the pattern emerging from Beijing challenges that assumption in ways that deserve careful examination. When a central bank purchases gold for 19 consecutive months through periods of price weakness, geopolitical turbulence, and elevated interest rate expectations, it is communicating something far more consequential than a tactical allocation shift. It is announcing a structural redesign of how one of the world's largest reserve holders intends to store national wealth across generations.

Understanding this shift requires moving beyond headline tonnage figures and examining the mechanics of sovereign reserve management, the geopolitical logic underpinning China PBOC gold buying, and what the persistence of this strategy signals for gold markets heading into the second half of 2026.

When big ASX news breaks, our subscribers know first

The Mechanics of Sovereign Reserve Diversification

How Central Banks Actually Build Gold Positions

Reserve management at the central bank level operates on a fundamentally different logic than institutional fund management. Where a hedge fund adjusts positions based on rolling return calculations and volatility models, a central bank reserve manager evaluates gold through a lens of monetary system resilience, counterparty risk, and multi-decade geopolitical scenario planning.

Gold occupies a unique position in this framework because it carries no counterparty risk. Unlike U.S. Treasury bonds, which require the continued goodwill and operational accessibility of American financial infrastructure, or euro-denominated assets subject to European Central Bank policy decisions, gold is a self-contained store of value. It cannot be frozen, sanctioned, or devalued by a foreign government's decree.

In practical terms, central bank gold reserves are typically built using a cost-averaging approach across multi-year timeframes. Monthly purchases are sized to avoid creating detectable price impact in liquid spot markets, while the aggregate accumulation trajectory follows a pre-determined allocation target embedded in the institution's reserve policy framework. This is why the PBOC's buying continued through May 2026 even as gold recorded a third consecutive monthly price decline, with spot prices touching as low as $4,330 per troy ounce. For reserve managers operating on 20-year horizons, a monthly price drawdown is noise, not signal.

The Significance of the 9% Threshold

China's gold now represents approximately 9% of total foreign exchange reserves, a figure that carries more analytical weight than it might initially appear. In reserve management circles, the composition of a nation's reserves is understood to reflect its assessment of systemic risk within the international monetary system. Countries with high gold allocations typically hold those positions because they have either experienced monetary crises firsthand or operate in geopolitical environments where dollar-asset accessibility cannot be guaranteed.

The United States holds gold at roughly 65-70% of total reserves, as does Germany. Russia sits at approximately 25-28%. China's 9% figure, while representing years of deliberate accumulation, still sits dramatically below these benchmarks, which is precisely why analysts consistently identify substantial structural runway for continued purchases. Furthermore, the role of gold in the monetary system becomes even more pronounced when examining how sovereign institutions respond to fragmentation in global financial architecture.

China's Gold Holdings: Mapping the Accumulation Trajectory

Quantifying the 19-Month Streak

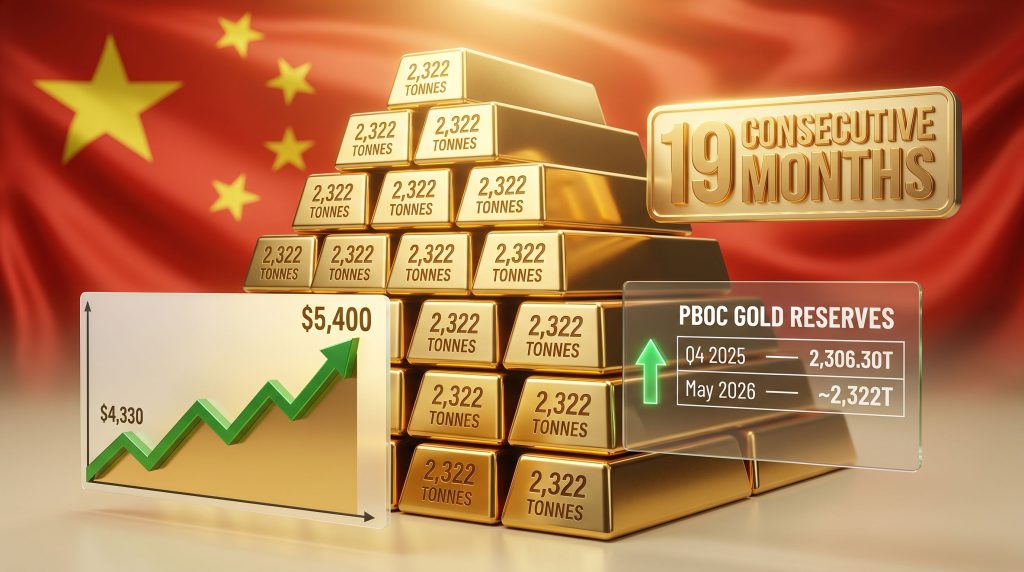

The People's Bank of China added 320,000 troy ounces, equivalent to approximately 9.9 tonnes, to its official gold reserves during May 2026. This extended the unbroken buying streak to 19 consecutive months, the longest continuous accumulation period since the PBOC began publishing standardised monthly reserve disclosures in 2015. Total declared holdings have now reached approximately 2,322 tonnes.

The progression of purchases over recent reporting periods reveals an important trend:

| Reporting Period | Estimated Gold Holdings (Tonnes) | Notable Change |

|---|---|---|

| Q4 2025 | 2,306.30 | Steady accumulation phase |

| Q1 2026 | 2,313.46 | +7.16 tonnes quarter-on-quarter |

| April 2026 | ~2,314 | +8 tonnes (largest addition since December 2024) |

| May 2026 | ~2,322 | +~9.9 tonnes (streak extended to 19 months) |

What this table reveals is not merely growth, but acceleration. The April 2026 addition of 8 tonnes was the largest single-month purchase in over 16 months. May's 9.9-tonne addition extended both the streak and the pace, contradicting any narrative that the PBOC's gold appetite is moderating. For further context on how central bank buying trends are shaping the broader gold market, the data paints a compelling picture of sustained institutional commitment.

The 2024 Pause and What It Revealed

A lesser-discussed aspect of China's accumulation history is the brief pause in purchases during mid-2024. The PBOC temporarily halted reported gold buying for several months before resuming with renewed conviction. Rather than interpreting this pause as a strategic retreat, analysts who tracked the subsequent resumption pointed to it as confirmation of the institutional commitment underlying the program. The pause aligned with a period of elevated gold prices, consistent with the cost-averaging methodology described above, and the resumption confirmed that the broader allocation target remained intact regardless of short-term price levels.

Macroeconomic Forces Shaping PBOC Demand in 2026

Why Buying During Price Weakness Is Strategically Rational

Gold recorded three consecutive monthly price declines heading into June 2026, with persistent inflation concerns and elevated interest rate expectations suppressing non-yielding asset demand across Western institutional markets. This dynamic creates a genuine paradox for market observers accustomed to thinking about gold demand through a retail or fund-management lens.

For sovereign reserve managers, price weakness in a core strategic asset is not a reason to pause accumulation. It is a cost reduction opportunity within a long-horizon allocation program that operates entirely outside the quarterly performance cycle that governs institutional investor behaviour.

This behavioural distinction matters enormously for understanding how China PBOC gold buying interacts with gold price formation. While institutional investors in New York and London may reduce exposure to gold in response to hawkish Federal Reserve signalling, the PBOC's purchasing desk operates according to reserve architecture targets that remain unchanged by short-term rate expectations.

Goldman Sachs' $5,400 Price Target: The Three-Pillar Framework

Goldman Sachs maintained its year-end 2026 gold price forecast of $5,400 per troy ounce even as prices retreated toward $4,330 during May, representing projected upside of approximately 24-25% from that trough. The bank's analytical framework rests on three reinforcing pillars:

- Sustained and potentially accelerating central bank purchases globally, with the PBOC's streak representing the most visible example of sovereign demand providing a structural price floor.

- Geopolitical risk premium, with ongoing Middle East conflict maintaining elevated uncertainty across commodity and currency markets, reinforcing safe-haven demand from sovereign and private buyers alike.

- Eventual monetary policy easing, which would reduce the opportunity cost of holding non-yielding assets and unlock a significant wave of institutional re-engagement with bullion.

Goldman specifically noted that geopolitical developments are expected to reinforce reserve diversification pressures globally, a conclusion that points directly toward continued central bank purchases rather than a retreat.

Scenario Modelling: Three Pathways for Gold in H2 2026

| Scenario | Key Assumptions | Implied Gold Price Range |

|---|---|---|

| Bull Case | Rate cuts materialise + PBOC accelerates buying + geopolitical escalation | $5,200 – $5,600/oz |

| Base Case | PBOC maintains current pace + rates plateau + geopolitical stability | $4,700 – $5,100/oz |

| Bear Case | Rate hikes resume + PBOC pauses buying + risk-off USD rally | $4,100 – $4,500/oz |

Disclaimer: Price forecasts involve inherent uncertainty and should not be interpreted as financial advice. Past accumulation patterns do not guarantee future price performance.

China vs. the World: How PBOC Holdings Compare

Global Reserve Benchmarking

Positioning China's gold holdings within the global central bank landscape provides essential context for evaluating both the significance of the current accumulation streak and the likely duration of the buying program. In addition, understanding how central banks are influencing gold prices globally helps contextualise China's outsised role in the current cycle.

| Central Bank | Estimated Gold Holdings | Gold as % of Reserves (Approx.) |

|---|---|---|

| United States Federal Reserve | ~8,133 tonnes | ~65-70% |

| Germany (Bundesbank) | ~3,352 tonnes | ~65% |

| IMF | ~2,814 tonnes | N/A |

| Russia (Bank of Russia) | ~2,332 tonnes | ~25-28% |

| People's Bank of China | ~2,322 tonnes | ~9% |

The gap between China's 9% allocation and the Western central bank norm of 65% is not simply a statistical curiosity. It reflects decades of reserve policy anchored to dollar-denominated assets, a strategy that made economic sense during a period of deep U.S.-China financial integration but carries growing vulnerability in an era of geopolitical fragmentation. According to China's official gold reserves data, the trajectory of accumulation has been remarkably consistent across recent reporting periods.

The Emerging Market Context

China's accumulation does not occur in isolation. Central banks in Poland, Turkey, and India have simultaneously expanded gold allocations, and the World Gold Council identifies this collective sovereign demand as one of three primary structural pillars supporting bullion prices alongside ETF inflows and physical jewellery consumption. The coordinated nature of this shift across diverse geographies suggests it is driven by a systemic reassessment of reserve risk rather than country-specific circumstances. Consequently, central bank gold demand is now widely regarded as one of the most structurally significant forces in bullion markets.

De-Dollarisation: Reading the Strategic Signal

The Post-2022 Reserve Risk Reassessment

The freezing of Russian sovereign foreign exchange reserves following the 2022 invasion of Ukraine sent a signal through global central banking circles that reverberated far beyond Moscow. The episode demonstrated concretely that dollar-denominated reserve assets held within Western financial infrastructure could be rendered inaccessible through political decision-making, regardless of international law precedents or the nominal sovereignty of the holder.

For China's reserve managers, this was not an abstract risk. U.S.-China financial tensions had been escalating across multiple dimensions, from technology export controls to bilateral investment restrictions, and the Russian precedent established a credible scenario in which Chinese sovereign assets could face similar treatment in an extreme geopolitical confrontation.

Gold offers a direct hedge against this scenario. It is physically custodied within China's borders, subject to no foreign jurisdiction, and its value is not dependent on the continued functioning of any external financial system. This is what analysts mean when they describe PBOC gold buying as a dual-purpose instrument: it simultaneously diversifies reserve composition and reduces the leverage that dollar-system access provides to geopolitical adversaries.

What a Rising Gold Ratio Means for Dollar Assets

As China's gold allocation approaches and potentially moves beyond 10% of total reserves, the mathematical consequence is a reduction in the relative share of U.S. Treasury holdings within the same portfolio. This dynamic carries implications well beyond the gold market, touching the structural demand foundations of U.S. government debt and, by extension, the long-term sustainability of dollar reserve currency dominance.

This is not a near-term crisis scenario. China's U.S. Treasury holdings, while reduced from peak levels, remain substantial. However, the directional shift is unambiguous, and the 19-month gold accumulation streak is one of the most quantitatively reliable data series tracking that transition in real time. As Reuters recently reported, the PBOC's sustained commitment to accumulation has continued even through periods of significant price volatility.

The next major ASX story will hit our subscribers first

The Price Support Mechanism: How Central Bank Buying Creates a Demand Floor

Structural vs. Cyclical Demand in Bullion Markets

Gold market analysts distinguish carefully between cyclical demand, driven by interest rate expectations, inflation psychology, and ETF flows, and structural demand, anchored in long-horizon commitments from sovereign institutions and physical consumption markets. The PBOC's buying program belongs firmly in the structural category, which is precisely why it provides meaningful price support even during periods when cyclical headwinds are significant.

When Western institutional investors reduce gold exposure in response to hawkish Federal Reserve guidance, sovereign buyers absorb a portion of that selling pressure, compressing the downside in a way that would not occur in a purely speculative market. This mechanism helps explain why gold, despite three consecutive monthly price declines through May 2026, remained elevated relative to historical levels.

Factors That Could Interrupt the Buying Streak

While the structural case for continued PBOC accumulation is robust, intellectual honesty requires acknowledging the scenarios under which the streak could pause:

- A rapid, sustained gold price rally could prompt temporary pauses as reserve managers manage cost-averaging targets more conservatively.

- Meaningful improvement in U.S.-China diplomatic and financial relations could reduce the urgency of diversifying away from dollar assets, though this appears a low-probability scenario in the near term.

- Domestic macroeconomic pressures requiring the deployment of foreign exchange reserves could temporarily reprioritise liquidity over gold accumulation.

- A sharp strengthening of the U.S. dollar could increase the domestic yuan cost of gold purchases, potentially moderating the pace of buying.

None of these scenarios appear imminent based on current conditions, but they represent legitimate analytical considerations for investors tracking the PBOC's reserve disclosures.

Frequently Asked Questions: China PBOC Gold Buying

How many consecutive months has the PBOC been buying gold?

As of May 2026, the People's Bank of China has added gold to its reserves for 19 consecutive months, the longest unbroken accumulation streak since the central bank began publishing regular monthly reserve data in 2015.

How much gold does China officially hold in 2026?

Official Chinese gold reserves stand at approximately 2,322 tonnes as of May 2026, representing roughly 9% of total foreign exchange reserves.

Why does the PBOC continue buying gold when prices are falling?

Sovereign reserve managers operate on multi-decade investment horizons where short-term price movements are secondary to long-term allocation targets. Price weakness is typically treated as a cost reduction opportunity within a pre-determined accumulation programme rather than a deterrent to continued buying.

What is Goldman Sachs' gold price forecast for 2026?

Goldman Sachs maintains a year-end 2026 gold price target of $5,400 per troy ounce, citing sustained central bank demand, geopolitical risk premiums, and the anticipated eventual easing of monetary policy as the primary supporting factors.

How does China's gold allocation compare to Western central banks?

China's gold represents approximately 9% of total reserves, compared to roughly 65-70% for the United States, approximately 65% for Germany, and around 25-28% for Russia. This gap suggests substantial structural room for continued PBOC accumulation over the long term.

Does China's gold buying affect global prices?

Sovereign purchases at the scale of the PBOC create a meaningful structural demand floor that partially offsets selling pressure from institutional investors during cyclical downturns. The 19-month accumulation streak has been consistently identified by market analysts as a key pillar of structural support for gold valuations.

The Long-Term Outlook: Structural Conviction Over Market Cycles

The analytical picture that emerges from examining China PBOC gold buying across these dimensions is one of institutional conviction operating largely independently of the market cycles that dominate financial media coverage. With a gold-to-reserves ratio of approximately 9% sitting far below both Western benchmarks and China's own likely long-term strategic targets, the fundamental rationale for continued accumulation remains firmly intact.

Geopolitical fragmentation, demonstrated vulnerability of dollar-denominated reserve assets to political intervention, and the structural economics of cost-averaging across a multi-decade allocation programme all point in the same direction. The 19-month streak is less a market story than a monetary architecture story, one that is rewriting the structural demand landscape for gold in ways that will likely persist well beyond the current accumulation cycle.

The PBOC's sustained gold accumulation strategy reflects a fundamental reassessment of reserve risk in a fractured geopolitical environment. With China's allocation still well below Western central bank norms and the conditions driving diversification showing no sign of reversal, the structural case for continued buying remains compelling regardless of where spot gold prices trade in any given month.

This article is intended for informational purposes only and does not constitute financial advice. Price forecasts and scenario analyses are speculative in nature and subject to significant uncertainty. Readers should conduct independent research and consult qualified financial professionals before making investment decisions.

Want to Track the Next Major ASX Gold Discovery in Real Time?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements daily, delivering instant alerts on significant mineral discoveries — including gold — and translating complex data into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.