July 23, 2026

The Hidden Architecture of Rare Earth Dependency: Why Heavy Elements Are Different

Most discussions of critical mineral supply chains focus on volume — tonnes mined, reserves identified, production capacity. But the more instructive lens for understanding the strategic weight of heavy rare earth elements is not abundance; it is irreplaceability. Unlike many industrial commodities where substitution is commercially inconvenient but technically feasible, heavy rare earths occupy a category where the absence of supply does not raise costs — it stops production lines entirely.

This is the industrial reality now confronting Japan. The country's manufacturers, which collectively operate the world's largest rare earth magnet production base outside China, are navigating a sustained and increasingly formalised supply squeeze driven by China rare earth export curbs to Japan. The restrictions, which have now extended across multiple rounds of tightening, have reduced shipments of critical heavy rare earth oxides to near zero. Understanding how this situation developed, what the data confirms, and what the long-term structural implications are for rare earth supply chains requires moving well beyond the diplomatic headlines.

When big ASX news breaks, our subscribers know first

Understanding Why Heavy Rare Earths Are Functionally Irreplaceable

The rare earth family comprises 17 elements, but not all carry equal strategic weight. The distinction between light rare earths (LREEs) and heavy rare earths (HREEs) is not merely taxonomic — it reflects fundamentally different industrial functions, geographic concentrations, and supply risk profiles.

Light rare earths like cerium and lanthanum are relatively abundant and serve in applications including catalysts, glass polishing, and battery anodes. Heavy rare earths — particularly dysprosium, terbium, and yttrium — are scarcer, more geographically concentrated, and occupy roles in high-performance applications where they cannot currently be substituted without significant performance loss.

Dysprosium and Terbium: The Thermal Performance Enablers

The central application driving strategic concern is the neodymium-iron-boron (NdFeB) permanent magnet. These magnets are the core component of the synchronous motors used in electric vehicles, direct-drive wind turbines, industrial robotics, and military actuation systems. Without dysprosium and terbium additions, NdFeB magnets lose coercivity — their resistance to demagnetisation — at elevated operating temperatures. For an EV motor running at 150 to 180 degrees Celsius, this is not a marginal performance issue. It is a functional failure mode.

Dysprosium additions of roughly 2 to 5 percent by weight are typically required in high-performance NdFeB magnets. Terbium, while used in smaller quantities, delivers superior coercivity enhancement per unit added and has become increasingly favoured in designs targeting weight reduction. There is no commercially viable synthetic substitute that replicates these thermal stability functions at production scale.

Yttrium Oxide: Breadth Across Advanced Manufacturing

Yttrium sits in a different application profile. While not a magnet material in the conventional sense, yttrium oxide is a critical input across semiconductor manufacturing (plasma-resistant chamber coatings), phosphors for displays and lighting, and specialty alloys for aerospace-grade components. Its processing is similarly concentrated in China, and its restriction compounds the supply squeeze beyond the magnet sector alone.

| Element | Primary Industrial Use | Key End Markets | China's Estimated Global Share of Processing |

|---|---|---|---|

| Dysprosium | NdFeB magnet thermal stability | EVs, wind turbines, defense | ~90% |

| Terbium | Magnet coercivity enhancement | EV motors, aerospace | ~85%+ |

| Yttrium | Specialty alloys, coatings, phosphors | Electronics, semiconductors | ~70%+ |

| Gallium | Semiconductors, compound chips | Consumer electronics, defense | ~80%+ |

"Heavy rare earth elements are not commodity inputs with elastic supply curves. They are performance-critical materials embedded into irreplaceable industrial functions. The geopolitical leverage this creates is structural, not incidental."

Japan's Unique Exposure: The World's Largest Magnet Manufacturing Base Outside China

Japan's vulnerability to China rare earth export curbs is not accidental — it is the product of deliberate industrial specialisation over several decades. Japanese companies including Shin-Etsu Chemical, TDK, and Hitachi Metals built magnet manufacturing capabilities that supply global automakers, robotics producers, and defense contractors. This industrial ecosystem requires consistent access to refined heavy rare earth oxides, the overwhelming majority of which originate from Chinese processing facilities.

The concentration problem is multi-layered. China does not merely dominate rare earth mining. It controls the separation and refining of rare earth oxides, which is the technically complex and capital-intensive step that transforms mined ore into the high-purity oxide powders that magnet manufacturers require. Furthermore, even rare earth ores mined in Australia, Africa, or North America have historically been shipped to China for processing, meaning that geographic diversification of mining does not automatically translate into supply chain independence.

This processing bottleneck is the core structural vulnerability that China's export control framework exploits. Indeed, the rare earth processing challenges faced by non-Chinese producers remain a defining constraint on how quickly the global industry can respond.

How China's Export Restrictions Escalated: A Policy Chronology

The current supply squeeze did not emerge suddenly. It followed a traceable diplomatic and regulatory escalation sequence.

In November 2024, remarks by Japan's Prime Minister relating to Taiwan triggered a breakdown in bilateral relations with Beijing. Rather than responding through conventional diplomatic channels alone, China began deploying its rare earth export control framework as a pressure mechanism — one that had been formalised and expanded in the years following the 2010 dispute. China's rare earth export restrictions have consequently redrawn strategic assumptions across global supply chains.

The formal timeline of restrictions:

- April 2025: Beijing introduces formal export controls covering categories of heavy rare earths and the magnets that contain them.

- January 2026: Controls are publicly tightened specifically against Japan, with major industrial conglomerates named as targets.

- February 2026: Two further rounds of tightening occur within a single month, indicating deliberate escalatory pressure.

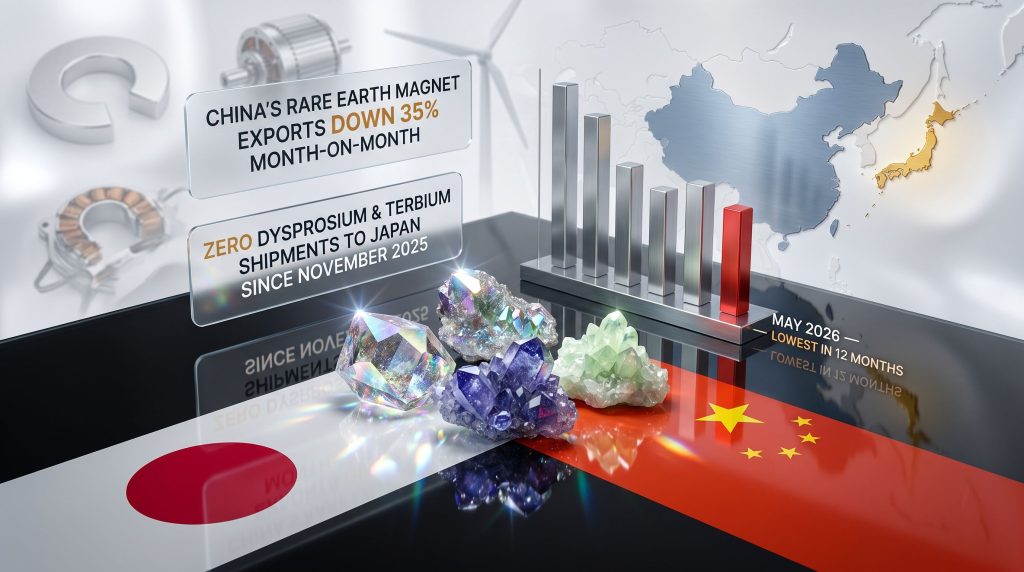

- May 2026: Chinese customs data confirms the cumulative effect — shipments of terbium oxide and dysprosium oxide to Japan have been zero since November 2025, with yttrium oxide recorded at only negligible volumes since December 2025.

Beijing has framed these restrictions within its dual-use materials regulatory framework, classifying rare earth elements as materials with potential military applications. This legal architecture provides significant strategic flexibility: controls can be applied selectively by destination country without requiring a formal blanket ban, maintaining diplomatic deniability while achieving targeted supply disruption.

What the May 2026 Customs Data Actually Reveals

The release of Chinese customs data for May 2026 provides the clearest quantitative picture yet of the supply situation. The figures confirm that the restrictions are not a temporary administrative slowdown but a sustained, near-total interruption of heavy rare earth oxide flows to Japan.

Key figures from May 2026 Chinese customs data:

- Terbium oxide shipments to Japan: zero since November 2025

- Dysprosium oxide shipments to Japan: zero since November 2025

- Yttrium oxide shipments to Japan: negligible since December 2025

- China's total rare earth magnet exports in May 2026: down 35% month-on-month, reaching their lowest volume since May 2025

- Gallium shipments to Japan in May 2026: first significant shipment recorded since December 2025

The gallium data point is analytically interesting. After months of near-zero shipments, Japan received a meaningful gallium consignment in May. Gallium is essential for compound semiconductor production — a sector where Japan holds significant manufacturing capabilities. The partial resumption of gallium flows may reflect strategic calibration by Beijing: maintaining maximum pressure on magnet-related materials while selectively easing restrictions on a semiconductor input that affects broader allied-nation supply chains, including those touching US interests.

According to rare earth prices hitting record highs amid China's export curbs, market pricing has already begun to reflect the severity of these disruptions, with benchmark heavy rare earth oxide prices surging sharply in response to reduced availability outside China.

"The selective nature of these controls reveals their sophistication. This is not a blunt embargo — it is a precisely targeted instrument applied with diplomatic intent, element by element, buyer by buyer."

Comparing 2010 and 2025: Similar Playbook, Very Different Architecture

The 2010 China-Japan rare earth dispute has become the standard historical reference point, but the comparison requires careful handling. The structural similarities are real, but the mechanisms are fundamentally different in ways that carry significant implications for resolution timelines and market responses.

| Dimension | 2010 Episode | 2025–2026 Episode |

|---|---|---|

| Trigger | Senkaku Islands maritime incident | Taiwan-related political statements |

| Mechanism | Informal export slowdown | Formal dual-use export control regulations |

| Elements targeted | Broad rare earth categories | Heavy rare earths (dysprosium, terbium, yttrium) + magnets |

| Duration to date | Months | 7+ months and continuing |

| Japan's dependency level | Extremely high | Reduced but still structurally significant |

| Global response | Diversification push, WTO complaint | Investment surge in non-Chinese supply |

In 2010, China's restrictions operated primarily through administrative friction — customs delays, reduced export quotas applied informally, bureaucratic slowdowns. These were difficult to challenge legally because they lacked a formal regulatory basis. The current framework is in some respects the opposite: it relies on formal export control designations under domestic law, which provides Beijing with legally defensible authority but also creates a more rigid and persistent mechanism.

One underappreciated dimension of the 2025-2026 episode is its element-specific precision. Rather than restricting all rare earths broadly, Beijing has targeted the heavy rare earth oxides that are most critical and least substitutable. This selectivity signals that China's rare earth trade strategy has matured considerably since 2010 and reflects deep knowledge of downstream industrial dependencies.

The next major ASX story will hit our subscribers first

Japan's Industrial Response: From Stockpiling to Structural Investment

Japan's reaction to the current supply squeeze has been both faster and more institutionally coordinated than its response to the 2010 episode. The clearest signal of this shift came from Shin-Etsu Chemical, which announced plans to build its first new rare earth refining facility since 2008. For a company of Shin-Etsu's industrial scale and strategic significance, such a commitment represents a structural repositioning, not a tactical hedge.

The broader Japanese industrial response encompasses several parallel strategies:

- Strategic stockpile expansion: Government-backed reserve programmes are being extended to cover longer supply disruption scenarios, with specific focus on dysprosium and terbium.

- Allied-nation supply engagement: Japanese trading houses and manufacturers are accelerating investment discussions with rare earth projects in Australia, Canada, and other allied-nation jurisdictions.

- Rare earth recycling and urban mining: Japan's well-developed electronics recycling infrastructure is being re-evaluated as a supplementary source of recovered heavy rare earth materials, particularly from end-of-life EV motors and industrial equipment.

- Magnet design adaptation: Some manufacturers are investing in research into grain boundary diffusion techniques that reduce the quantity of dysprosium and terbium required per magnet without sacrificing thermal performance — though this is a partial mitigation, not a substitute.

The downstream sectors facing the greatest near-term risk include EV and hybrid vehicle manufacturers dependent on NdFeB permanent magnets, industrial robotics producers, defense and aerospace contractors requiring high-coercivity alloys, and consumer electronics manufacturers using yttrium-based phosphors and coatings.

Global Supply Chain Implications: Beyond the Japan-China Bilateral

The significance of China rare earth export curbs to Japan extends well beyond the bilateral relationship. Japan functions as a critical node in global manufacturing supply chains. Its rare earth magnets flow into EV motors assembled in Europe, industrial robots deployed in North American factories, and defense components supplied to allied militaries. Supply disruption at Japan's magnet producers propagates downstream with a lag measured in months, not years.

The 35% month-on-month decline in China's total rare earth magnet exports in May 2026 confirms that the supply pressure extends beyond Japan-specific restrictions. Global OEMs monitoring inventory positions are beginning to treat Chinese rare earth supply as structurally unreliable for strategic planning purposes — a significant recalibration from the assumption of stable Chinese supply that dominated procurement thinking for the prior decade.

The clearest beneficiaries of this structural repricing are rare earth projects in allied-nation jurisdictions with genuine heavy rare earth content. Alternative rare earth supply chains are attracting accelerated investment interest, particularly where projects carry meaningful dysprosium and terbium grades. As noted in analysis of the broader strategic stakes, the shift in investor and government attention towards non-Chinese supply is now a structural rather than cyclical trend.

A less widely recognised dynamic is the role of ionic clay deposits in heavy rare earth supply. Unlike hard rock rare earth mineralisation, ionic clay deposits in regions including southern China and parts of Southeast Asia carry naturally elevated heavy rare earth fractions and are processable using heap leach methods without the energy-intensive cracking steps required for hard rock ores. The identification of analogous ionic clay systems in non-Chinese jurisdictions has become a priority exploration target — and a potential longer-term supply solution that bypasses Chinese processing infrastructure entirely.

"For global investors and supply chain strategists, the Japan situation represents a live case study in what supply chain weaponisation looks like in practice. The lesson is that concentration risk in critical material processing is not a theoretical concern — it is an operational variable with quantifiable consequences."

Frequently Asked Questions: China Rare Earth Export Curbs to Japan

What rare earths is China restricting exports of to Japan?

Chinese customs data confirms that shipments of dysprosium oxide and terbium oxide to Japan have been zero since November 2025, with yttrium oxide recorded at only negligible volumes since December 2025. These heavy rare earth oxides are essential inputs for manufacturing high-performance NdFeB permanent magnets used in electric vehicles, industrial motors, wind turbines, and defense systems.

Why did China impose rare earth export controls on Japan?

The restrictions followed a diplomatic breakdown triggered by Taiwan-related comments made by Japan's Prime Minister in late 2024. Beijing has formalised the controls under its dual-use materials regulatory framework, classifying rare earth elements as materials with potential military applications — a legal structure that permits selective application by destination country.

How does this compare to the 2010 China-Japan rare earth dispute?

Both episodes involve China deploying rare earth supply as a diplomatic instrument against Japan. However, the 2025-2026 restrictions are more formally structured, applying to specifically targeted heavy rare earth elements rather than broad categories, and are enforced through established domestic export control law rather than informal administrative pressure.

What is Japan doing to address the supply squeeze?

Responses include Shin-Etsu Chemical's planned construction of its first new rare earth refining facility since 2008, accelerated investment engagement with rare earth projects in allied-nation jurisdictions, strategic stockpile expansion, and research into magnet design techniques that reduce heavy rare earth consumption per unit.

Is gallium also affected by China's export restrictions on Japan?

Japan received its first significant gallium shipment from China since December 2025 in May 2026, suggesting a partial easing of gallium restrictions. Analysts note that this selective resumption may reflect strategic calibration rather than a broader policy reversal, given that gallium affects semiconductor supply chains with wider allied-nation implications.

Key Takeaways

- China has recorded zero or negligible shipments of dysprosium oxide, terbium oxide, and yttrium oxide to Japan since November-December 2025, confirmed by Chinese customs data for May 2026

- The restrictions follow a diplomatic breakdown over Taiwan-related political statements and are enforced under China's dual-use materials export control framework

- Japan hosts the world's largest rare earth magnet manufacturing base outside China, creating disproportionate exposure to heavy rare earth supply disruption

- China's total rare earth magnet exports fell 35% month-on-month in May 2026, reaching their lowest volume since May 2025

- Shin-Etsu Chemical has announced its first new rare earth refining facility since 2008, signalling a structural rather than temporary shift in sourcing strategy

- The 2025-2026 episode is structurally more sophisticated than the 2010 dispute, with formal regulatory mechanisms replacing informal administrative pressure and targeting specific heavy rare earth elements

- Global supply chain planners, EV manufacturers, and defense contractors are closely monitoring developments as a leading indicator of broader critical mineral geopolitical risk

- Ionic clay rare earth deposits in non-Chinese jurisdictions have emerged as a priority exploration target given their natural enrichment in heavy rare earth fractions and processing advantages over hard rock mineralisation

This article contains forward-looking analysis and references to market dynamics, policy trajectories, and investment themes. Such content is intended for informational purposes only and does not constitute financial advice. Readers should conduct independent research before making investment decisions.

Want to Capitalise on the Next Major Rare Earth Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including rare earth projects with strategic heavy element content — and delivering actionable alerts to subscribers ahead of the crowd. Explore historic examples of major mineral discoveries and their returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself at the forefront of critical mineral opportunities.