July 31, 2026

The Hidden Architecture of Rare Earth Control: How Export Licensing Became Geopolitical Leverage

Most commodity disputes play out through tariffs, quotas, and WTO filings. But the contest now unfolding across global rare earth supply chains operates by an entirely different logic. When a government restricts the flow of a material that has no commercially viable substitute, that cannot be synthesised in a laboratory, and that underpins everything from fighter jet coatings to electric vehicle drivetrains, the resulting leverage is qualitatively different from any conventional trade dispute. China rare earth export restrictions represent precisely this kind of structural power, and the world's industrial economies are only beginning to understand its full implications.

When big ASX news breaks, our subscribers know first

Why Heavy Rare Earths Are Not Like Other Commodities

The rare earth family encompasses 17 elements, but the strategic tension in current geopolitics clusters around a specific subset known as heavy rare earth elements, or HREEs. This group includes dysprosium, terbium, yttrium, holmium, and lutetium, among others. What distinguishes HREEs from their lighter counterparts is not simply scarcity but functional irreplaceability.

In neodymium-iron-boron permanent magnets, the addition of dysprosium and terbium is what allows those magnets to maintain their coercivity at elevated operating temperatures. Without these elements, the magnet loses its ability to resist demagnetisation when hot, which matters enormously in EV traction motors and aerospace actuators. No commercially deployed substitute performs comparably at scale.

Yttrium presents a similar case. As a thermal barrier coating in jet engine turbine blades and as a plasma-resistant liner in semiconductor fabrication chambers, yttrium oxide occupies a position of genuine inelasticity. Manufacturers cannot simply switch suppliers when they cannot find the material at any price that makes production economical.

Furthermore, the rare earth processing challenges compound the mining problem considerably. China's dominance is not primarily about having the largest ore reserves. It stems from having built, over three decades, an unmatched industrial capacity for separating, refining, and converting rare earth ores into usable metals, alloys, and oxides. Countries that hold rare earth deposits outside China still depend on Chinese processing infrastructure to turn that ore into something useful.

China's Export Control Regime: How the Architecture Was Built

The April 2025 Controls: Targeting the Critical Seven

The first major wave of China's rare earth export restrictions arrived in April 2025, placing seven heavy rare earth elements, along with their associated compounds, metals, and magnet products, under a mandatory licensing framework. Crucially, the measures introduced end-user disclosure requirements, meaning foreign importers were obligated to declare the ultimate application and destination of purchased materials.

The immediate downstream effects were severe. Defence contractors, electric vehicle manufacturers, and semiconductor equipment producers dependent on Chinese-origin heavy rare earths faced both supply shortfalls and a new layer of compliance complexity that extended approval timelines significantly.

The October 2025 Expansion: Extraterritorial Reach

A second, more expansive regulatory wave followed in October 2025, adding five further rare earth categories to the controlled list and extending the regime's reach in a structurally significant way. The October measures applied not only to Chinese-origin materials but also to foreign-manufactured products that incorporated Chinese rare earth technology or processing know-how, even where no direct Chinese material input was present in the finished product.

This extraterritorial design bears a structural resemblance to U.S. mechanisms such as the Foreign Direct Product Rule, which restricts foreign-made chips that rely on American technology regardless of where they are physically produced. By adopting a comparable framework, Beijing signalled a sophisticated understanding of how to maximise compliance burden on foreign manufacturers without triggering a formal WTO dispute. For a detailed analysis of consequences for global industry, independent policy research offers valuable context on the full scope of the disruption.

The November 2026 Suspension: Tactical Pause, Not Policy Reversal

China subsequently suspended the second wave of controls for a period of one year, effective November 2026. However, an analysis by Fitch Group's BMI Research concluded that this pause amounts to a tactical diplomatic gesture rather than any structural concession. The core April 2025 controls on the original seven heavy rare earth categories remain fully operational.

During high-level diplomatic engagement, Beijing indicated a willingness to address Western supply shortage concerns, but provided no binding volume commitments, no licensing transparency guarantees, and no enforceable framework for consistent supply access. The suspension preserves China's full policy optionality while offering importing nations no durable supply security.

Quantifying the Supply Disruption

The measurable impact on global heavy rare earth availability has been severe. Despite the diplomatic context surrounding the November 2026 suspension, Chinese export volumes of key materials remain deeply suppressed relative to pre-restriction levels.

| Rare Earth Element | U.S. Supply Dependence on China | Export Volume vs. Pre-Restriction Baseline | Price Impact |

|---|---|---|---|

| Dysprosium | High | ~41% | Significant escalation |

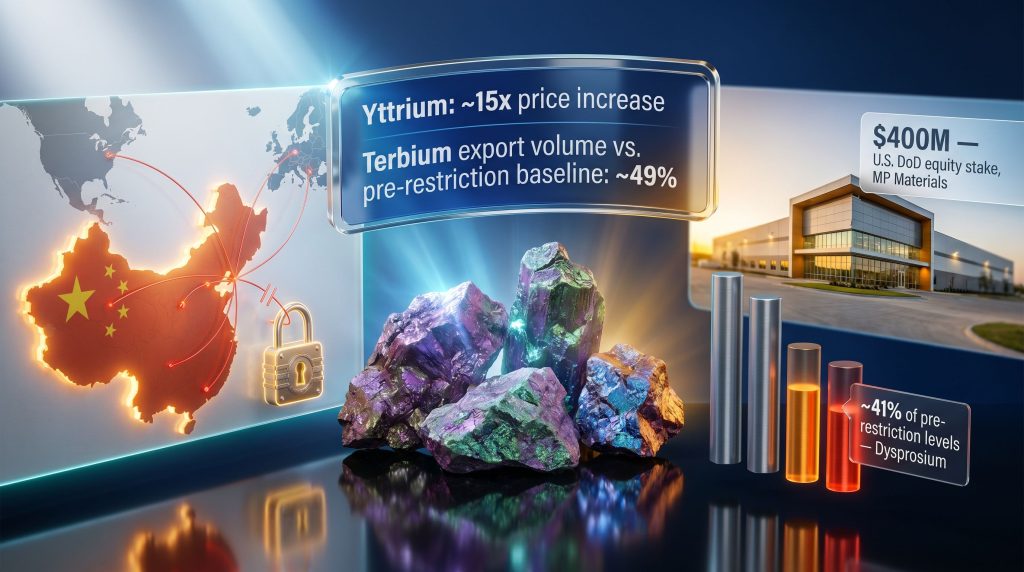

| Terbium | 100% | ~49% | Severe shortage pricing |

| Yttrium | ~70% | ~42% | Approximately 15x price increase |

| Holmium | 100% | Heavily restricted | Critical shortage |

| Lutetium | 100% | Heavily restricted | Critical shortage |

The yttrium price shock deserves particular attention. A roughly 15-fold increase in yttrium pricing has cascaded through U.S. aerospace and semiconductor manufacturing. In aerospace, yttrium-based thermal barrier coatings are applied to turbine components to allow engines to operate at temperatures exceeding the melting point of the underlying metal. There is no near-term engineering workaround when the coating material becomes economically inaccessible.

In chip fabrication, yttrium oxide chamber liners protect equipment from plasma erosion during the etching process. Shortages here directly compress semiconductor production capacity. The defence supply chain dimension extends further still, with rare earth permanent magnets appearing in precision guidance systems, radar arrays, electric motors for unmanned aerial systems, and naval propulsion.

The U.S. Response: Building a Domestic Supply Architecture

Pentagon Equity and the MP Materials Model

The U.S. Department of Defense made a landmark move by acquiring $400 million in preferred stock in MP Materials, positioning the Pentagon as the company's largest shareholder with approximately 15% equity. The transaction included a 10-year offtake agreement incorporating a price floor mechanism, ensuring that domestic rare earth magnet output flows directly to defence and commercial customers under commercially predictable terms.

MP Materials is deploying this capital alongside $1 billion in commercial debt financing from JPMorgan Chase and Goldman Sachs to construct the "10X Facility," a rare earth magnet manufacturing campus in Northlake, Texas. This represents one of the most significant investments in domestic rare earth manufacturing capacity the United States has attempted, integrating magnet production within a domestically controlled facility rather than relying on offshore processing.

CHIPS Act Funding and the Round Top Deposit

USA Rare Earth entered into a non-binding Letter of Intent with the U.S. Department of Commerce to access $1.6 billion in financing drawn from a facility established under the CHIPS and Science Act. The proposed structure comprises a $1.3 billion senior secured loan and $277 million in direct federal funding, with the U.S. government receiving a 10% equity stake and warrants for additional shares as a condition of the arrangement.

The capital is intended to accelerate the development of the Round Top deposit in Sierra Blanca, Texas, with commercial heavy rare earth production targeted for 2028. Round Top is notable for its polymetallic composition, hosting a range of heavy rare earth elements alongside lithium and other critical minerals, making it one of the more strategically complete domestic HREE deposits under active development.

REalloys and the Mine-to-Magnet Integration Strategy

REalloys (NASDAQ: ALOY) is constructing a North American mine-to-magnet position through a series of targeted agreements. The company has secured long-term supply arrangements with the Saskatchewan Research Council covering neodymium-praseodymium, dysprosium, and terbium output, while co-funding upgrades to SRC's Saskatoon processing facility. REalloys is simultaneously developing a heavy rare earth metallization platform in Ohio focused on defence-grade metal and alloy production.

Mine-to-Magnet Explained: A mine-to-magnet supply chain integrates ore extraction, chemical separation, metal conversion, alloy manufacturing, and finished magnet fabrication within a single allied-nation framework. Each link in that chain that remains outside China represents a point of strategic risk. The objective of Western supply chain investment is to eliminate each of those dependencies sequentially.

Feedstock for the REalloys platform is sourced from multiple geographic nodes, including the Tanbreez project in Greenland and the Sheep Creek rare earth deposit in Montana, providing a degree of supply diversification not achievable through single-source arrangements.

Europe's Regulatory Response: The Critical Raw Materials Act Framework

The European Union's Critical Raw Materials Act introduces mandatory diversification thresholds designed to prevent the kind of single-country dependency that has left European industry exposed to Chinese supply controls. The context for this legislation is stark: the EU currently sources approximately 100% of its heavy rare earth supply, 85% of its light rare earth supply, and 98% of its rare earth magnets from China.

Understanding the broader rare earth supply chain vulnerabilities is essential to appreciating why Europe has moved with such urgency. The CRMA framework operates across several dimensions:

- Single-country dependency caps that require member states to diversify sourcing below defined concentration thresholds.

- Strategic project designation for European and allied-nation extraction and processing initiatives that meet defined security-of-supply criteria.

- The RESourceEU Action Plan, backed by up to €3 billion in coordinated funding, which pools demand aggregation, supply stress testing, and joint purchasing capacity across EU member states.

- A 25% recycled content mandate requiring that at least a quarter of the EU's strategic raw material requirements be met through recycled waste streams by 2030.

The European critical raw materials supply framework also reflects a growing recognition that urban mining — recovering rare earths from end-of-life electronics, motors, and batteries — offers a complementary supply pathway that bypasses primary extraction and Chinese processing entirely. Current European recycling rates for rare earths are very low, meaning substantial infrastructure investment is required to close the gap before 2030.

European manufacturers are, in addition, pursuing material substitution strategies. Several automakers are actively developing synchronous reluctance motors and induction motor architectures that eliminate neodymium-based permanent magnets from EV drivetrains entirely. These designs involve trade-offs in power density and efficiency, however the supply security calculus is shifting the cost-benefit analysis in favour of magnet-free approaches for certain vehicle platforms.

The next major ASX story will hit our subscribers first

Scenario Pathways: Where China's Rare Earth Policy Goes From Here

Three plausible trajectories exist for Beijing's rare earth export control regime through 2028:

- Controlled Continuation — China maintains the current licensing framework with selective and opaque approvals, preserving leverage while avoiding the full supply cutoff that would most aggressively accelerate Western supply chain independence. This is the most probable near-term trajectory.

- Escalatory Reinstatement — The second-wave extraterritorial controls are fully reinstated when the November 2026 suspension expires, expanding compliance burdens to encompass foreign manufacturers using Chinese-origin rare earth processing technology regardless of where they operate.

- Negotiated Framework — A bilateral or multilateral agreement produces minimum volume commitments and licensing transparency in exchange for technology access concessions from Western parties. Given current policy trajectories, this scenario appears structurally unlikely in the near term.

The key asymmetry is that China faces limited incentive to abandon a leverage instrument that carries low economic cost to itself while imposing high disruption costs on adversaries. The complexities of rare earth geopolitics make this dynamic particularly difficult for Western policymakers to counteract in the short term. For further context, the European Parliament Research Service has published analysis examining how these controls reshape industrial policy priorities across member states.

The Investment Imperative: Closing the Processing Gap Before 2028

Committed public capital across Western nations now stands at material levels:

| Programme | Capital Committed | Mechanism |

|---|---|---|

| U.S. DoD / MP Materials | $400 million | Preferred equity + offtake |

| CHIPS Act / USA Rare Earth | $1.6 billion (proposed) | Loan + direct federal funding |

| EU RESourceEU Action Plan | Up to €3 billion | Coordinated demand and supply funding |

The structural challenge, however, is not simply capital availability. Building rare earth processing capacity requires specialised solvent extraction chemistry, environmental permitting for radioactive byproduct management, and the development of metallization capabilities that the Western industrial base largely abandoned decades ago when Chinese processing became economically dominant.

Allied-nation resource diplomacy adds a further dimension. Greenland, Canada, and Australia each host significant rare earth deposits that are increasingly subject to bilateral offtake arrangements and government-backed development financing. Coordinating these investments to avoid duplication, standardise processing technology, and align supply timelines with demand requirements represents a policy challenge as significant as the capital mobilisation itself.

Investment Consideration: The strategic shift in rare earth supply chains carries significant implications across multiple asset classes, from mining equities and processing infrastructure to defence contractors and EV manufacturers. Investors should note that timelines for domestic supply chain independence remain long, production targets carry execution risk, and diplomatic developments can affect market sentiment rapidly. This article does not constitute financial advice.

The gap between current dependency levels and achievable supply independence is measurable: domestic U.S. HREE production at meaningful scale is targeted for 2028 at the earliest, EU recycled content mandates extend to 2030, and Western magnet manufacturing capacity remains a fraction of Chinese output today. China rare earth export restrictions were built into a formidable architecture over decades. Replacing that architecture will require sustained capital deployment, policy consistency, and industrial coordination across allied nations on a timeline that remains compressed relative to the urgency of current supply disruptions.

Want to Identify ASX Opportunities Emerging From the Rare Earth Supply Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including rare earth and critical mineral announcements — instantly translating complex geological data into actionable investment insights for traders and long-term investors alike. Explore how historic mineral discoveries have generated substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.