July 1, 2026

The Invisible Chokepoint: How China Turned Mineral Processing Into Strategic Power

Most discussions about critical mineral security focus on where metals come from in the ground. Far fewer examine what happens after ore is extracted, and that oversight is precisely where the United States finds itself most exposed. The architecture of China rare earth export restrictions to the US is not primarily about geology. It is about chemistry, metallurgy, and decades of deliberate industrial policy that positioned Chinese refiners, alloyers, and magnet manufacturers as the unavoidable intermediary between raw ore and finished component.

Understanding why these restrictions are far from resolved, even after high-level diplomacy, requires starting with that processing reality, not with headlines about trade disputes. The rare earth supply chain importance extends far beyond simple mining volumes, encompassing every stage from extraction to finished component.

When big ASX news breaks, our subscribers know first

The Strategic Logic Behind Beijing's Mineral Controls

How Processing Dominance Became More Powerful Than Mining Volume

China controls approximately 60% of global rare earth mining output, according to reporting by Mexico Business News citing Fitch Group's BMI research unit. But that figure, while significant, tells only part of the story. The more consequential number is China's share of downstream processing, which encompasses separation, refining, alloying, and magnet sintering. In those stages, China's dominance approaches near-totality for many critical elements.

This distinction matters enormously for policymakers and investors alike. A country can open a new mine outside China, ship ore to port, and still find that the only facilities capable of processing that ore into usable industrial inputs are located in Jiangxi or Inner Mongolia. The mine-to-magnet supply chain is not a single pipe. It is a series of specialised industrial steps, each requiring significant capital investment, technical expertise, and years of operational refinement to replicate.

"Processing and refining rare earths is not analogous to building a factory. It involves mastering complex hydrometallurgical and pyrometallurgical techniques that China's industry has refined over multiple decades, creating a technical moat that pure capital injection cannot rapidly overcome."

From Trade Friction to Structural Resource Strategy

The framing of China's export controls as a retaliatory trade measure, mirroring US tariff escalation, understates the strategic durability of these policies. While the timing of the April 2025 Wave 1 restrictions aligned with heightened bilateral tensions, the underlying policy architecture reflects something more enduring. Beijing has been systematically tightening its grip on critical mineral supply chains since at least 2010, when it temporarily cut rare earth export quotas to Japan during a territorial dispute.

The 2025 measures represent an escalation of a well-established playbook, not an improvised reaction. Furthermore, China's rare earth trade strategy has consistently prioritised long-term structural leverage over short-term commercial considerations.

What makes the current regime structurally distinct from prior episodes is its extraterritorial dimension, which fundamentally changes the calculus for allied nations attempting to diversify away from Chinese inputs.

What China's Rare Earth Export Restrictions Actually Involve

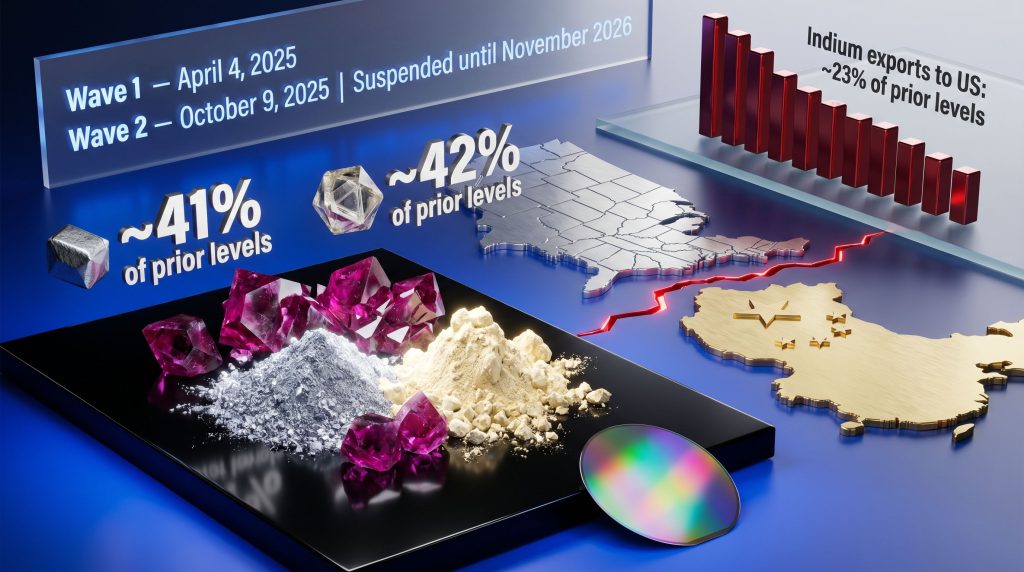

A Two-Wave Escalation Through 2025

Beijing's controls were introduced in two distinct phases, each progressively more restrictive in scope and reach.

| Restriction Wave | Date | Elements and Products Covered | Key Feature |

|---|---|---|---|

| Wave 1 | April 4, 2025 | 7 heavy rare earths, compounds, metals, magnets | Triggered alongside US tariff escalation |

| Wave 2 | October 9, 2025 | Expanded rare earths, processing equipment, technologies | Extraterritorial reach over foreign-made products |

| Partial Suspension | Late October 2025 | Wave 2 measures only | Suspended until November 2026 |

Wave 1 targeted seven heavy rare earth elements including dysprosium and terbium, along with their compounds, refined metals, and the permanent magnets manufactured from them. Wave 2 broadened controls to five additional elements and, critically, extended licensing requirements to products manufactured outside China if those products incorporated Chinese-sourced materials or technologies.

The Extraterritorial Dimension: When Chinese Rules Reach Beyond China's Borders

The extraterritorial feature of Wave 2 represents a qualitative shift in how mineral export controls function as a geopolitical instrument. Under this framework, a Japanese or German manufacturer producing magnets using Chinese rare earth inputs could theoretically require a Chinese export licence to sell that finished product to a US defence contractor.

This mechanism directly undermines the logic of allied supply chain diversification. If third-party processing facilities are using Chinese feedstock because no alternative feedstock exists at commercial scale, then their output remains subject to Beijing's licensing regime regardless of where manufacturing occurs. Allied nations building midstream processing capacity from non-Chinese ore would need to demonstrate an unbroken chain of provenance to avoid this licensing exposure. The rare earth processing challenges facing nations attempting to build independent capacity outside China are consequently far greater than simple capital investment would suggest.

Licensing as Precision Geopolitical Leverage

The export control regime is not a blanket embargo. Licences continue to be issued for sectors including automotive manufacturing and consumer electronics. The friction is selective and deliberate. Industries where rare earth applications intersect with military end-uses, including aerospace, guided munitions, and advanced radar systems, have reported persistent delays and effective denials.

This selectivity is strategically significant. It allows China to maintain economic relationships with US civilian industries while simultaneously constraining the Pentagon's access to critical inputs. The licensing structure creates a form of disaggregated pressure that is difficult for the United States to counter through blanket countermeasures without harming its own commercial sectors.

How Severe Are the Supply Disruptions Hitting US Industries?

Quantifying the Import Collapse

Even accounting for the partial suspension of Wave 2 measures, shipments of export-controlled rare earths to the United States have remained dramatically below historical norms, according to customs data analysed by BMI.

| Rare Earth or Mineral | Import Volume vs. Pre-Restriction Baseline | Primary US Industrial Application |

|---|---|---|

| Yttrium | ~42% of prior levels | Turbine blade coatings, semiconductor insulators |

| Dysprosium | ~41% of prior levels | Permanent magnets for defence and EVs |

| Terbium | ~49% of prior levels | High-performance magnets, phosphors |

| Indium (global exports) | ~33% of prior levels | Photonic chips, LED screens, fibre optics |

| Indium (US-specific) | ~23% of prior levels | AI data centre optical components |

These figures reflect a supply environment that is, in practical terms, operating at a fraction of normal capacity despite diplomatic assurances of goodwill from both sides.

The Yttrium Price Shock and Its Industrial Consequences

Yttrium's 15-fold price increase since controls took effect has concentrated minds in two critical US industries. In aerospace, yttrium-stabilised zirconia is applied as a thermal barrier coating on turbine blades, protecting engine components from extreme heat during operation. Without adequate yttrium supply at commercially viable prices, manufacturers face cost pressure that cannot simply be passed through to defence procurement contracts priced years in advance.

In semiconductor fabrication, yttrium serves a dual function: as a protective coating on chamber components inside plasma etch systems, and as an insulating material in certain device architectures. Licensing delays compound standard lead times across the semiconductor supply chain, creating a cascading effect that reaches far beyond the immediate rare earth shortage.

Indium Phosphide and the Photonic Chip Bottleneck

Indium entered the bilateral trade dialogue for the first time following the May 2026 summit, marking a significant shift in how Washington frames the mineral dependency problem. China placed indium on its export control list in February 2025. Over the following 14 months, Chinese exports of the mineral fell by approximately two-thirds globally and by 77% to the United States specifically, based on customs data reported by Mexico Business News.

The strategic importance of indium phosphide extends well beyond its relatively obscure profile in public discourse. It is the foundational material for:

- Next-generation photonic chips that transmit data using light rather than electrons, enabling far higher bandwidth at lower energy consumption

- High-speed optical lasers used in fibre optic networks and emerging 6G infrastructure

- Indium tin oxide, a transparent conductive material essential for LED displays across consumer electronics

Demand for indium phosphide-based components is rising sharply as hyperscale data centre operators integrate photonic interconnects into AI infrastructure. Coherent, which holds a 40% global market share in indium phosphide optical components, was represented in the executive delegation that accompanied the US presidential team to Beijing, underscoring how commercially critical this material has become at the highest levels of bilateral negotiations.

Paul Triolo, Partner and China Technology Policy Lead at DGA-Albright Stonebridge Group, has noted that if Chinese licensing remains slow or subject to political conditions, companies with significant indium phosphide exposure could face escalating input costs, supply allocation constraints, delayed capacity expansion, and increasing difficulty fulfilling demand from hyperscale cloud operators.

Which US Sectors Face the Greatest Strategic Vulnerability?

Defence Supply Chains: The Most Structurally Exposed

The Centre for Strategic and International Studies has characterised China's export restrictions impact as among the most consequential actions Beijing has taken specifically targeting US defence industrial capacity. Heavy rare earths, particularly dysprosium and terbium, are indispensable in the permanent magnets used in:

- Precision-guided munitions requiring high-coercivity magnets to maintain performance across temperature extremes

- Radar and electronic warfare systems dependent on neodymium-iron-boron magnets enhanced with heavy rare earth additions

- Jet engine actuators, where weight-to-force efficiency is non-negotiable

The military end-use denial policy embedded in China's licensing regime creates a structural barrier rather than a temporary delay. There is no diplomatic pathway that resolves this problem while China retains the discretion to define military end-use broadly.

AI Infrastructure and the Data Centre Capacity Dilemma

The intersection of indium phosphide scarcity and AI infrastructure buildout creates a compounding vulnerability that is underappreciated in most trade policy discussions. Photonic interconnects are not a future technology. They are actively being deployed in current-generation hyperscale data centres to address bandwidth constraints between GPU clusters. Without reliable access to indium phosphide, the pace of AI infrastructure capacity expansion in the United States faces a material constraint that no amount of chip manufacturing investment can resolve independently.

Aerospace and the Civilian-Military Supply Chain Convergence

Commercial aerospace and defence aerospace share supply chains in ways that make selective restriction particularly damaging. Turbine blade coatings, precision actuators, and electronic systems components draw from the same upstream rare earth supply pool. Disruptions intended to target military applications inevitably affect commercial aircraft programmes, creating broader economic pressure that extends well beyond the defence sector.

Did the May 2026 Xi-Trump Beijing Summit Change Anything?

What Was and Was Not Agreed at the Summit

The May 14–15 summit in Beijing produced no formal agreement to remove or permanently modify China rare earth export restrictions to the US. The White House stated that China had committed to addressing US concerns over supply shortages, but China's Ministry of Commerce published its own summit summary that made no mention of rare earths whatsoever.

Cory Combs, Associate Director at Trivium China, characterised the gap between the two governments' public accounts as suboptimal but not critical. His assessment was that the more important outcome was that both sides had credibly signalled mutual interest in stability and demonstrated the ability to communicate that signal effectively to their respective domestic audiences.

"The absence of a formal rare earth agreement should be read as a feature of the current diplomatic environment, not a failure. Both governments retain maximum flexibility while having established a rhetorical framework for de-escalation that neither side needs to immediately honour with substantive policy changes."

The November 2026 Cliff: What Happens When the Suspension Expires

No clarity has been provided on whether the one-year suspension of Wave 2 measures will be renewed when it lapses in November 2026. This creates a known uncertainty event that supply chain managers, procurement teams, and investors must factor into planning horizons. According to Reuters, China has maintained that its controls are lawful and has pledged only to cooperate with what it deems "reasonable concerns." Three scenarios consequently emerge:

- Managed Stability: Licensing volumes recover toward pre-restriction baselines as diplomatic goodwill translates into operational policy changes

- Prolonged Selective Friction: The suspension is renewed but licensing continues to function as a precision geopolitical instrument, maintaining pressure on defence-adjacent industries

- Escalation Restart: Wave 2 measures are reinstated without renewal, extending extraterritorial controls and further disrupting allied midstream processing ambitions

Processing Technology Controls: A Separate Layer of Restriction

The White House fact sheet specifically noted that China would address US concerns over export restrictions on rare earth processing technology. This is a dimension of the control regime that receives insufficient attention. Beijing actively restricts the transfer of separation and refining technologies to protect the competitive advantage of domestic processors. Even if mining investments outside China succeed, building genuinely independent processing capacity requires access to technical knowledge that China has made structurally difficult to acquire.

The next major ASX story will hit our subscribers first

What the United States Is Doing to Reduce Rare Earth Dependency

Domestic Investment: The Mine-to-Magnet Ambition

Washington has committed approximately US$2 billion in domestic rare earth infrastructure investment, comprising:

- US$400 million directed to MP Materials, the only operating rare earth mine in the United States, located at Mountain Pass, California

- US$1.6 billion in funding for USA Rare Earth, which is developing a deposit in Texas and constructing downstream processing capacity

These investments are significant in absolute terms but face a fundamental timing problem. Building separation and refining facilities capable of operating at commercial scale requires years of permitting, construction, and process optimisation. China's processing advantage was not built in a single electoral cycle, and it cannot be neutralised in one either.

International Diversification: Where Washington Is Sourcing Allies

| Partner Region or Country | Strategic Role |

|---|---|

| Australia | Established mining output, developing allied processing capacity |

| Canada | Integrated North American supply chain potential |

| Greenland | Untapped heavy rare earth deposits, geopolitical significance |

| Angola and Mozambique | Emerging African mineral diplomacy frameworks |

| Brazil | Significant reserves, processing investment target |

| Saudi Arabia | Strategic financing and offtake partnership potential |

America's rare earth supply chain ambitions depend heavily on these international partnerships delivering practical processing capacity, not merely mining agreements, within commercially viable timeframes.

The Processing Bottleneck: Why Mining Alone Won't Resolve the Crisis

A critical and frequently overlooked point is that upstream mining investment does not automatically translate into supply security. Ore must be concentrated, separated by element, refined into metals, alloyed, and then manufactured into magnets or other components before it becomes industrially useful. Each of these steps requires specialised facilities, chemical reagents, and technical expertise.

Countries that succeed in opening new mines but lack processing infrastructure will find themselves shipping ore to China for refining, recreating precisely the dependency they sought to escape. Realistic timelines for meaningful alternative processing capacity range from five to fifteen years depending on the element, the jurisdiction, and the regulatory environment. This gap between political urgency and industrial reality defines the medium-term vulnerability window.

How Investors and Industry Operators Should Read This Risk Environment

Supply Chain Resilience Strategies for US Manufacturers

For companies with significant rare earth exposure, the following approaches are being actively pursued across the industry:

- Qualifying alternative indium and yttrium sources from non-Chinese suppliers, even at higher cost, to establish dual-sourcing capability

- Building strategic stockpiles calibrated to critical programme timelines rather than just-in-time procurement assumptions

- Engaging in government-facilitated offtake agreements through allied-nation partnerships to secure forward supply commitments

- Investing in material efficiency and substitution research to reduce per-unit rare earth intensity in key applications

The Investment Case for Non-Chinese Rare Earth Producers

For investors evaluating opportunities in the rare earth space, processing capability is the critical differentiator between projects with genuine near-term value and those that remain perpetually in the pre-revenue development phase. A mining asset in a favourable jurisdiction with integrated separation and refining capacity commands a fundamentally different risk-adjusted return profile than a mine that requires Chinese processing.

As analysed by CSIS, jurisdictions offering the most credible near-term production timelines include Australia, where Lynas Rare Earths operates the largest rare earth processing facility outside China, and Canada, where proximity to US industrial demand centres provides logistical advantages that matter at commercial scale.

Frequently Asked Questions: China Rare Earth Export Restrictions and the US

What rare earths did China restrict exports of to the United States?

Wave 1 controls, introduced in April 2025, targeted seven heavy rare earth elements including dysprosium and terbium, along with related compounds, refined metals, and permanent magnets. Wave 2, introduced in October 2025 and partially suspended until November 2026, extended controls to five additional elements and introduced extraterritorial licensing requirements.

Why did China impose rare earth export controls in 2025?

The initial wave aligned with escalating US tariff actions, but the controls reflect a longer-term strategic posture. China has used critical mineral supply chains as geopolitical leverage in previous bilateral disputes and has been progressively tightening its downstream processing advantage through export restrictions on processing technologies and refined products.

How much have US imports of rare earths fallen since the restrictions began?

Yttrium shipments to the US fell to approximately 42% of pre-restriction volumes, dysprosium to 41%, and terbium to 49%. Indium exports from China to the US fell by approximately 77% over the 14 months following Beijing's February 2025 controls, according to customs data reported by Mexico Business News.

Are China's rare earth export controls a permanent ban or a licensing regime?

The controls operate as a licensing regime rather than an outright ban. Licences continue to be issued for civilian applications including automotive and consumer electronics. Industries with defence-adjacent applications have faced persistent delays and effective denials. The selective nature of the regime is a deliberate feature, not an administrative backlog.

What is indium phosphide and why does it matter for US technology supply chains?

Indium phosphide is a compound semiconductor used to manufacture photonic chips that transmit data using light, high-speed optical lasers for fibre optic and 6G networks, and other advanced photonic components. It is central to next-generation AI data centre infrastructure and represents a supply vulnerability that sits at the intersection of semiconductor policy, AI strategy, and critical mineral security.

Did the Trump-Xi summit in May 2026 resolve the rare earth dispute?

No formal agreement was reached to remove or permanently modify China's export restrictions. The White House characterised the outcome as China committing to address US supply concerns, while China's Ministry of Commerce made no mention of rare earths in its own summit summary. The November 2026 expiry of the Wave 2 suspension remains unaddressed.

What is the US government doing to reduce dependence on Chinese rare earths?

Washington has committed US$2 billion in domestic rare earth infrastructure investment across MP Materials and USA Rare Earth, and is pursuing international sourcing partnerships across Australia, Canada, Greenland, Angola, Mozambique, Brazil, and Saudi Arabia. Structural processing capacity gaps mean these initiatives will take years to deliver meaningful supply independence.

When do China's suspended Wave 2 restrictions expire, and what happens next?

The partial suspension of Wave 2 measures expires in November 2026. No clarity has been provided on whether the suspension will be renewed. The outcome of that decision will serve as a critical signal about the durability of any diplomatic progress achieved through 2025–2026 negotiations.

The Long View: Rare Earth Dependency as a Structural Geopolitical Risk

The current predicament facing the United States in critical mineral supply chains is not the product of a single policy failure or a single administration's oversight. It reflects three decades of decisions, made across multiple governments, to prioritise cheap inputs and efficient supply chains over supply security and industrial redundancy. China rare earth export restrictions to the US are the consequence of that accumulated choice.

Reversing it requires not just investment capital but institutional knowledge, industrial workforce development, regulatory frameworks for processing facilities, and the political patience to sustain programmes across electoral cycles without guaranteed near-term results. The race to build alternative supply chains is real, but the timeline required for genuine processing independence is measured in decades, not years.

"Investors and policymakers who benchmark success against electoral calendars will consistently underestimate how long genuine supply chain independence takes to achieve in the rare earth sector. The mineralogy does not negotiate with political urgency."

For industries and investors navigating this environment today, the operative reality is that China rare earth export restrictions to the US will continue to function as a structural constraint on US defence, semiconductor, and AI infrastructure capacity for the foreseeable future, regardless of what diplomatic language surrounds the next bilateral summit.

This article contains forward-looking analysis and scenario projections based on publicly available information. It does not constitute financial or investment advice. Readers should conduct independent due diligence before making investment decisions related to any companies or sectors discussed.

Want To Capitalise on the Next Major Rare Earth or Critical Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological and commodity data into clear, actionable investment insights across rare earths and more than 30 other commodities. Explore why major mineral discoveries have historically generated exceptional returns and begin your 14-day free trial today to position yourself ahead of the market.