May 19, 2026

How Does China's Rare Earth Dominance Shape Global Supply Chain Architecture?

The modern technology architecture depends on seventeen metallic elements that few recognise yet every advanced economy desperately needs. China rare earth supply chains have become the world’s most concentrated industrial bottleneck, creating dependencies that extend into national security and strategic planning. Furthermore, governments are now exploring measures such as critical minerals energy security to offset vulnerabilities.

Understanding this concentration requires examining both geological advantages and strategic decisions that positioned China as the indispensable supplier of rare earth elements. In addition, these dynamics impact technology sovereignty, manufacturing resilience, and geopolitical leverage across borders.

When big ASX news breaks, our subscribers know first

Market Concentration Analysis: Understanding the 70-85% Control Framework

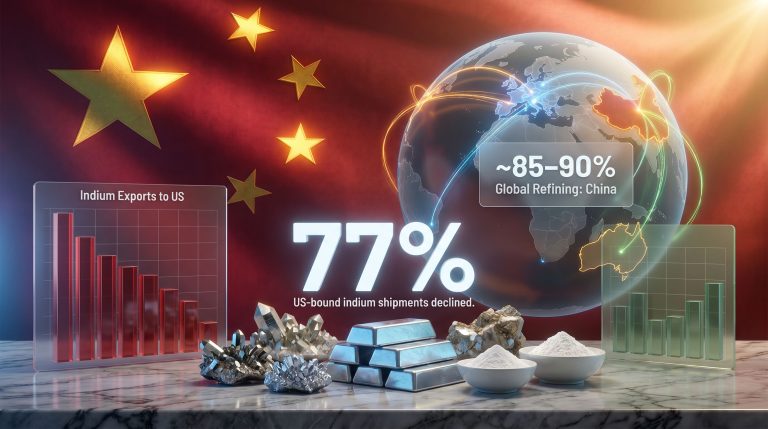

China’s control over rare earth mining represents approximately 70% of global production. However, this figure understates the true extent of dependency. The real constraint lies in processing capabilities where China commands nearly 90% of global refining capacity. Consequently, a structural chokepoint persists even when alternative mining operations emerge elsewhere.

The concentration is even more pronounced for specific elements, as seen below:

• Light rare earth elements: dominated by China’s Bayan Obo complex in Inner Mongolia

• Heavy rare earth elements: concentrated in southern ion-adsorption deposits

• Processing technology: cost advantages of 30-50% over competitors

• Vertical integration: from mining through magnet production in unified control

| Region | Mining Capacity (%) | Processing Capacity (%) | Key Deposits |

|---|---|---|---|

| China | 70 | 90 | Bayan Obo, southern ion-adsorption clays |

| Australia | 12 | 5 | Mount Weld |

| United States | 8 | 3 | Mountain Pass |

| Myanmar | 5 | 0 | Ion-adsorption deposits |

| Other | 5 | 2 | Various global deposits |

The geological concentration in China stems from unique deposit types. The Bayan Obo complex hosts massive reserves of light rare earth elements, while southern provinces hold economically viable heavy rare earth deposits. These natural cost efficiencies challenge alternative suppliers.

Vertical Integration Strategy: From Mine to Magnet

In 2011, China’s rare earth industry underwent systematic consolidation. Over 100 scattered producers merged into six major state-owned groups, creating unprecedented vertical integration. This integration has further solidified China rare earth supply chains in securing valuable resources.

Upstream Control:

• Mining rights are concentrated among state-owned enterprises.

• Resource allocation aligns with national industrial policy.

• Environmental compliance has become a consolidation mechanism.

Midstream Dominance:

• Proprietary separation and purification technologies are key.

• Industrial-scale solvent extraction facilities boost capacity.

• Rigorous quality control standards exceed international norms.

Downstream Manufacturing:

• Permanent magnet production integrates with the supply chain.

• Advanced research and development is in place for materials.

• End-user applications span automotive to aerospace sectors.

In addition, efforts like mine reclamation innovation help reduce environmental footprints while modernising production methods.

What Are the Critical Vulnerabilities in Current Rare Earth Supply Networks?

Global manufacturing sectors face vulnerabilities from supply disruptions. Some industries risk production shutdowns within months when interruptions occur. For instance, recent export restrictions led to immediate supply chain shocks for automotive and electronics sectors. Furthermore, research from global supply insights provides added perspective on these challenges.

Specialised rare earth applications and limited substitute materials amplify these risks. Automotive manufacturers faced direct supply chain shocks, while electronics companies experienced increasing costs and scheduling uncertainties for several quarters.

Heavy vs. Light REE Dependencies

The seventeen rare earth elements fall into two categories with distinct supply characteristics.

Heavy Rare Earth Elements (Critical Scarcity):

• Elements include europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, and lutetium.

• They are geographically concentrated in southern China’s ion-adsorption deposits.

• Their applications cover high-performance magnets, phosphors, and catalysts.

• Substitution is difficult for high-temperature applications.

Light Rare Earth Elements (Volume Dependency):

• Elements include lanthanum, cerium, praseodymium, neodymium, promethium, and samarium.

• Although more globally available in mining, Chinese processing dominance remains.

• They are crucial for magnets, batteries, and glass additives.

• Viable alternatives exist in Australia, the US, and other regions.

The ion-adsorption clay deposits in southern China yield the world’s most economically viable heavy rare earth elements due to advantageous geology and established infrastructure.

Manufacturing Sector Exposure Assessment

Different industries encounter varied timeframes for disruption:

• Immediate Impact (0-3 months):

– Permanent magnet manufacturers

– Phosphor producers for lighting and displays

– Catalytic converter production

• Medium-term Impact (3-12 months):

– Electric vehicle motor production

– Wind turbine generator manufacturing

– Advanced electronics assembly

• Long-term Impact (1-3 years):

– Defence equipment programmes (defence critical materials strategy)

– Aerospace components

– Advanced medical imaging equipment

The automotive sector’s vulnerability became evident during recent restrictions. Electric vehicle manufacturers faced potential delays due to dysprosium and neodymium constraints, leading to cascade effects in the industry.

How Do Export Controls Function as Geopolitical Leverage Tools?

Export control mechanisms have evolved into sophisticated policy instruments that differentiate based on end-use, destination, and strategy. Recent restrictions on exports to the United States and India illustrate how swiftly supply interruptions manifest as industrial impacts. Moreover, at times, measures such as US‑China trade war impacts have compounded these challenges.

China’s export system operates through a multi-tiered licensing framework. For example, comprehensive export control risks discussions highlight technical and geopolitical facets. Licences differentiate between civilian and dual-use applications, thereby introducing further strategic considerations.

Licensing Framework and Implementation

The licensing process exhibits several categories:

• Civilian-use applications: Processed swiftly for non-sensitive items.

• Dual-use technology restrictions: Subject to enhanced scrutiny.

• Strategic case reviews: Deployed for exports to specific countries or entities.

These processes include government oversight, end-use certification, periodic reviews, and strict compliance monitoring to ensure proper control.

Extraterritorial Enforcement Mechanisms

China’s control extends even to products containing its rare earth materials. This extraterritorial approach poses additional challenges for global manufacturers. It requires strict documentation, periodic audits, and penalties for unauthorised re-exports.

In December 2025, a Chinese Foreign Ministry spokesperson noted that civilian applications would receive prompt approval. However, practical implementation remains subject to diplomatic nuances.

What Alternative Supply Chain Models Are Emerging Globally?

The 50-country coalition led by the Trump administration exemplifies the international response to supply vulnerabilities. This coalition underscores that supply security needs coordinated action rather than isolated national measures.

Developing alternative supply chains faces technical and economic hurdles. While mining outside China is increasing, establishing competitive processing requires huge capital, technology transfer, and multi-year development.

Geographic Diversification Initiatives

• Australia – Mount Weld Operations:

– Hosts one of the world’s highest-grade rare earth deposits.

– Historically produces around 15,000 tonnes per annum of rare earth oxide concentrate.

– Faces challenges in developing downstream processing.

• United States – Mountain Pass Facility:

– Operated by MP Materials Corporation in California.

– Re-opened commercially in 2020 to meet domestic processing needs.

– Holds strategic importance for US supply security objectives.

• Malaysia – Lynas Advanced Materials Plant:

– A significant non-Chinese processing facility in Kuantan, Pahang.

– Operational since 2014 and adhering to stringent environmental standards.

– Provides a viable alternative as part of global diversification.

Developing Processing Capacity Outside China

Building competitive processing capacity requires overcoming several challenges:

• Technology Transfer Barriers:

– Proprietary purification processes hinder replication.

– Intellectual property concerns limit sharing.

– Building a skilled workforce is essential.

• Capital Investment Requirements:

– Cost of constructing advanced facilities runs into multi-billion dollars.

– Extended payback periods occur due to cost competition.

– Regulatory and permitting processes add delays.

• Timeline Projections:

– 3-5 years: Facility commissioning.

– 2-3 additional years: Commercial efficiency.

– 5-10 years total: Parity with Chinese operations.

The next major ASX story will hit our subscribers first

How Do Environmental Costs Impact Supply Chain Sustainability?

Environmental issues have become central to evaluating rare earth supply chains. China’s historical mining practices have left significant legacies that continue to affect production costs and operational standards. Consolidation post-2016 tightened environmental compliance, reducing the number of producers and minimising ecological impacts.

Southern China Environmental Legacy Issues

Mining regions in Jiangxi, Guangdong, and Hunan bear lasting impacts. For example, water contamination from acid mine drainage is a persistent problem. Radioactive waste and soil degradation further burden communities and agriculture. Remediation programmes, including land rehabilitation and water treatment systems, are now critical to ongoing sustainability efforts.

Global Environmental Standards Comparison

Alternative suppliers face stricter standards:

| Jurisdiction | Environmental Standards | Compliance Costs | Timeline Impact |

|---|---|---|---|

| Australia | Stringent assessments | High capital requirements | Extended permitting |

| United States | Federal and state regulations | Comprehensive remediation | Multi-year approvals |

| Canada | Indigenous consultation procedures | Community benefit agreements | Complex stakeholder ties |

| EU | Rigorous waste management | Advanced treatment needs | Stringent monitoring |

Such standards increasingly sway investor decisions, with environmental, social, and governance criteria now critical in assessing project viability.

What Strategic Scenarios Could Reshape Rare Earth Markets?

Market evolution is tied to demand growth, supply diversification, and technology change. Negotiations between the Trump administration and China on semiconductor export permissions illustrate this. For instance, recent talks within the critical minerals semiconductor coalition highlight how supply security now intertwines with broader trade policies.

Demand Surge Modelling Through 2030

Rising demand is anticipated from several sectors:

• Electric Vehicle Expansion:

– Each EV requires 1-2 kilograms of rare earths for motors and batteries.

– Projections indicate a 5-fold increase in demand for automotive rare earths by 2030.

– Efficiency-driven needs for neodymium and dysprosium persist.

• Wind Energy Growth:

– Offshore turbines require 200-600 kilograms each.

– Permanent magnets are critical for efficiency.

– Global wind capacity expansion adds substantial demand.

• 5G Infrastructure:

– Telecommunications equipment relies on rare earth components.

– Advanced antenna systems utilise specialised materials.

– The global rollout supports long-term demand.

Supply Shock Response Mechanisms

Supply disruptions could vary in duration:

• Short-term (0-6 months):

– Strategic reserves may be tapped.

– Inventory drawdowns could trigger price volatility.

– Procurement competition intensifies.

• Medium-term (6 months–2 years):

– Capacity expansion by alternative suppliers begins.

– Recycling technologies see accelerated deployment.

– Research into substitute materials gains momentum.

• Long-term (2-10 years):

– Greater geographic diversification comes into play.

– Technology innovations may reduce rare earth intensity.

– New deposits outside China could reshape markets.

How Should Investors Evaluate Rare Earth Exposure Risks?

Investors must assess rare earth exposure through supply security, price volatility, and regulatory frameworks. Conventional commodity approaches often fall short given the concentrated supply and geopolitical intricacies. The emergence of the 50-country coalition signals a multi-year investment theme that requires a nuanced approach.

Portfolio Diversification Strategies

Investors can manage risk by diversifying geographically and technologically:

• Geographic Risk Distribution:

– Spread mining exposure across multiple jurisdictions.

– Invest in alternative processing capacity development.

– Balance end-user sector exposure to avoid overconcentration.

• Technology Risk Management:

– Support research into alternative materials.

– Invest in recycling technologies to reclaim rare earths.

– Monitor efficiency improvements that reduce raw material needs.

• Regulatory Compliance Monitoring:

– Implement systems to track export licence changes.

– Ensure supply chain transparency through rigorous due diligence.

– Budget for potential increases in compliance costs.

Investment Timeline Considerations

Opportunities exist over various timeframes:

• Near-term (1-2 years):

– Secure alternative supplier premiums might emerge.

– Inventory management and strategic purchasing are key.

– Systems for regulatory compliance will be developed.

• Medium-term (2-5 years):

– Alternative processing capacity is expected to come online.

– Technology innovations could reduce supply dependencies.

– The market may shift toward non-Chinese suppliers.

• Long-term (5-10 years):

– Structural diversification of supply chains is anticipated.

– New deposit development could emerge outside China.

– Innovations may reduce the overall rare earth intensity.

What Long-Term Market Structure Changes Are Anticipated?

The present market dynamics suggest a transitional phase rather than permanence. While current pressures fortify China’s dominance, structural changes are emerging. In this climate, technology, policy, and investment converge to challenge established models.

Technology Innovation Impact Assessment:

• Recycling advances are boosting urban mining potential.

• Substitute material research offers cost-effective alternatives.

• New separation technologies promise improved energy efficiency.

• Automation integration is reducing labour and production costs.

Ultimately, China rare earth supply chains will face new challenges as innovation and policy reshape the landscape. This evolving scenario will determine future market structures over the coming decade.

Disclaimer: This analysis involves forecasts and speculation. Rare earth markets are volatile and subject to regulatory and geopolitical changes. Investors should conduct thorough due diligence and consider multiple scenarios when making decisions.

Ready to Capitalise on Critical Minerals Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including rare earth and critical mineral opportunities that could benefit from global supply chain diversification. With China's dominance creating investment opportunities in alternative suppliers, subscribers gain actionable insights to position themselves ahead of market movements in this strategically important sector, beginning with a 14-day free trial at Discovery Alert.