July 23, 2026

The Electrification Economy and the Metal That Powers It All

Copper sits at the intersection of nearly every major energy transition happening across the globe right now. It conducts electricity better than almost any other affordable metal, it cannot be easily substituted in power cables or electric motors, and it is consumed in enormous quantities wherever grids are being upgraded or vehicles are being electrified. China refined copper imports rising on strong demand is therefore not merely a trade statistic — it functions as a real-time barometer of where the world's largest industrial economy is directing its capital, and how tightly the global copper supply chain is being stretched in response.

Understanding why China's refined copper imports are rising again in mid-2026 requires looking beyond the headline customs numbers. The forces at work here involve smelter chemistry, seasonal demand rhythms, geopolitical disruption, infrastructure finance, and the peculiar market dynamics that emerge when the world's biggest consumer of a commodity is also one of its most sophisticated processors.

When big ASX news breaks, our subscribers know first

The Structural Paradox: How Can Imports Rise When Domestic Output Is Booming?

China's Dual Role as Producer and Consumer

China occupies an unusual position in global commodity markets. It is simultaneously the world's largest consumer of refined copper and one of its most significant processors of raw copper ore. Over the past several years, Chinese smelting capacity has expanded dramatically, growing by approximately 25% since 2021, which has fundamentally altered how the country sources its copper. Rather than importing large volumes of finished refined metal, China increasingly imports raw copper concentrate and processes it domestically into cathode copper.

This structural shift explains why full-year 2025 refined copper imports declined to approximately 3.35 million metric tons, representing a 10.27% year-on-year drop and the lowest net import figure recorded in roughly three years. On its face, this looked like weakening demand. In reality, it reflected growing domestic processing capacity absorbing more of the raw material pipeline.

Concentrate vs. Refined: Two Very Different Import Signals

The distinction between copper concentrate imports and refined copper imports is critical to understanding China's market position. Copper concentrate is the crushed and partially processed ore that emerges from mines before it undergoes smelting and electrolytic refining. Refined copper, by contrast, is the finished product — most commonly in the form of cathode copper — that can be directly fabricated into wire, rod, and sheet.

In April 2025, China imported approximately 2.9 million metric tons of copper concentrate, a 25% increase year-on-year, reflecting the expansion of domestic smelting infrastructure. When refined copper imports subsequently rise again in Q2 2026, this is not China reversing its strategic direction. Instead, it signals a temporary imbalance between smelting capacity and domestic refined output, driven primarily by scheduled maintenance cycles pulling refinery capacity offline.

Why Smelter Maintenance Creates Predictable Import Windows

Copper smelters require periodic shutdowns for maintenance and equipment inspection, similar to other high-temperature industrial facilities. These maintenance windows are typically scheduled during periods of lower electricity demand or aligned with seasonal production planning cycles. When a significant portion of Chinese smelting capacity goes offline simultaneously, domestic refined copper output falls, and the gap between consumption and local production must be bridged through imports. This pattern is highly predictable for experienced market participants, which is why traders and smelters typically begin placing import orders several weeks in advance of anticipated domestic output shortfalls.

What Is Actually Driving Copper Demand in China Right Now?

Power Grid Expansion: The Single Largest Catalyst

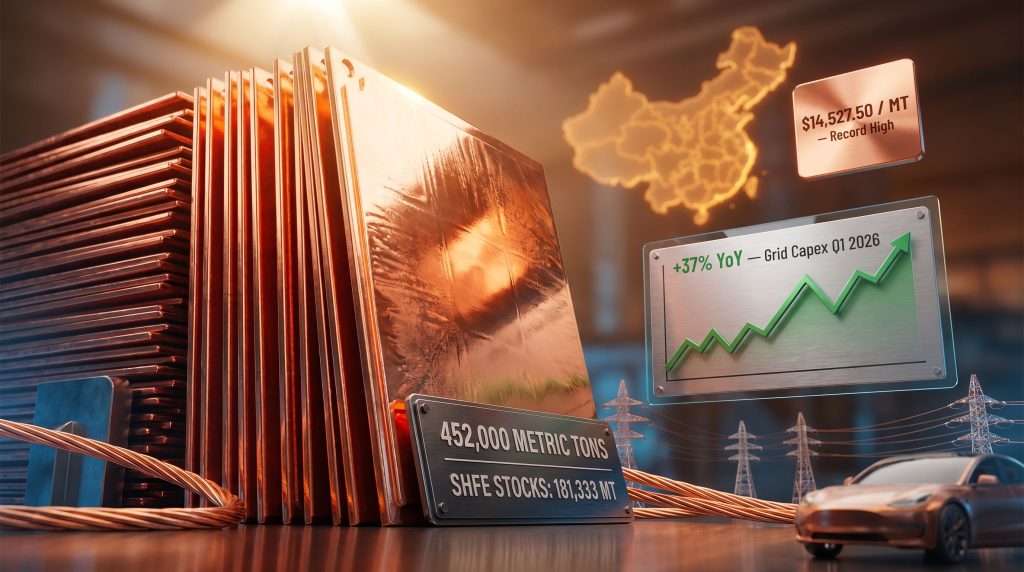

The most consequential driver of copper demand in China at present is infrastructure — specifically the rapid expansion and modernisation of the national power grid. Chinese power grid capital expenditure surged 37% year-on-year during the January-to-March period of 2026, according to state media reporting cited in industry sources. This scale of investment translates directly into copper consumption, as transmission lines, distribution cables, substations, and grid-scale equipment all rely heavily on the metal. Furthermore, energy transition minerals such as copper remain indispensable to achieving these electrification targets.

Nicholas Snowdon, Head of Metals and Mining Research at Mercuria, speaking at the LME Week conference in Hong Kong in May 2026, characterised the demand recovery as being principally driven by electrification sectors, with power grid deployment identified as the primary engine. His assessment noted that following the Lunar New Year period, Chinese industrial demand returned with a degree of price insensitivity that was notable by recent standards, suggesting genuine underlying consumption rather than speculative accumulation. According to Mining Weekly's reporting of his remarks, Snowdon described the resulting inventory drawdown as the largest and fastest depletion of onshore copper stocks observed in recent memory, signalling that cathode imports would need to rise to compensate. (Mining Weekly, May 11, 2026)

Electric Vehicle Adoption and Energy Security Pressures

The Iran conflict has had a secondary but meaningful effect on energy security calculations across China and neighbouring regions, contributing to accelerating interest in electric vehicles as a hedge against fossil fuel dependency. This geopolitical backdrop has compressed the adoption timeline for EVs in markets that might otherwise have moved more gradually.

The copper intensity of electric vehicles is substantially higher than that of conventional internal combustion engine vehicles. Each EV requires significantly more copper across its motor windings, battery management systems, charging infrastructure connections, and power electronics. As EV penetration increases across Chinese manufacturing output and regional sales volumes, the aggregate copper demand pulled from the domestic supply pool grows accordingly, further tightening the availability of refined metal for other end uses.

The Lunar New Year Recovery Effect

Copper demand follows a well-documented seasonal pattern in China. The Lunar New Year holiday period typically causes a multi-week slowdown in manufacturing and construction activity, which temporarily suppresses downstream copper orders. The first quarter of each year therefore tends to show subdued import volumes relative to Q2, as fabricators run down existing inventory rather than placing new orders during the holiday window.

The Q2 2026 recovery from this seasonal trough has been characterised as unusually robust. Rather than the typical gradual resumption of orders, downstream fabricators accelerated their purchasing timelines from March onward, with the acceleration gathering further momentum into April. This compressed ordering pattern contributed directly to the import surge recorded in April 2026 customs data.

How Tight Are China's Copper Inventories Right Now?

Shanghai Futures Exchange Stockpile Data as a Leading Indicator

Inventory levels on the Shanghai Futures Exchange serve as one of the most closely watched leading indicators for Chinese copper import demand. When SHFE warehouse stocks decline rapidly, it signals that physical consumption is outpacing domestic supply, and that import orders are likely to follow within weeks.

As of May 11, 2026, SHFE copper stockpiles had fallen 5.6% week-on-week to 181,333 metric tons, representing the lowest level recorded since January 2026. (Mining Weekly, May 11, 2026) This drawdown trajectory, combined with the broader context of smelter maintenance reducing domestic output, creates a clear directional signal for import demand acceleration through Q2. Consequently, the copper supply crunch appearing at the global level is now being felt acutely within China's own warehouse infrastructure.

What the Current Drawdown Means in Practice

The mechanics of how inventory depletion translates into import orders involves several steps that experienced copper market participants understand well. When SHFE stocks decline below comfort thresholds, fabricators and trading firms begin placing import orders to ensure supply continuity. Given the logistical lead times involved in shipping refined copper from major producing nations — which include lengthy sea voyages from Chile, Peru, and the Democratic Republic of Congo — orders are typically placed well before the physical shortfall becomes critical.

The current drawdown trajectory suggests Q2 import volumes are on course to exceed Q1 levels materially, extending the acceleration already visible in April's customs data.

Inventory and Import Data at a Glance

| Metric | Current Level | Prior Period | Significance |

|---|---|---|---|

| SHFE Copper Stocks | 181,333 mt | ~192,000 mt (prior week) | Lowest since January 2026 |

| Weekly Drawdown Rate | -5.6% | Varies | Accelerating depletion |

| April Import Volume | 452,000 mt | ~415,000 mt (March) | Highest since September |

| Month-on-Month Change | +9% | Declining trend in 2025 | Trend reversal signal |

| Full-Year 2025 Imports | ~3.35 million mt | ~3.73 million mt (2024 est.) | 10.27% YoY decline |

What Do April's Import Figures Reveal About the Q2 Trajectory?

April 2026 Customs Data: Reading the Numbers Carefully

China's refined copper intake in April 2026 reached 452,000 metric tons, the highest monthly volume recorded since September, representing a 9% increase over March volumes according to customs data released on May 10, 2026. (Mining Weekly, May 11, 2026) This is a key data point for understanding the broader picture of China refined copper imports rising on strong demand.

Li Ye, Deputy General Manager at commodity trader Eagle Metal, provided a trader-level perspective at the same LME Week conference in Hong Kong, noting that downstream orders had strengthened meaningfully from March onward. Critically, her framing of April's import volume as exceeding the combined total of the first three months of 2026 provides important context for the scale of the acceleration. (Mining Weekly, May 11, 2026)

This creates an important methodological nuance. If January through March combined produced less than 452,000 metric tons in total, and April alone reached 452,000 metric tons, the sequential comparison understates the shift in momentum. The quarterly pacing of 2026 imports suggests a sharp inflection point occurring at the Q1-Q2 boundary, driven by the confluence of post-holiday demand recovery, inventory pressure, and smelter maintenance-related supply constraints.

The Role of Arbitrage and Front-Loading in Amplifying Import Volumes

Physical copper trading operates across multiple benchmark systems, principally the London Metal Exchange and the Shanghai Futures Exchange. When price differentials between these two markets exceed the cost of shipping, insurance, and financing, arbitrage opportunities emerge that incentivise traders to purchase copper in one market and deliver it into another.

During 2025, significant volumes of copper were redirected toward COMEX delivery in the United States as tariff concerns created temporary price premiums in US markets. As that arbitrage window narrowed and US-bound trade flows normalised, copper that might otherwise have been routed to Western markets was redirected toward domestic Chinese consumption and LME-referenced contracts. This reorientation of trade flows contributed to the import acceleration visible in Q2 2026 data.

Is This Import Surge Sustainable, or Is It a Short-Term Restocking Event?

Separating the Structural from the Cyclical

One of the most important analytical questions for investors and industry participants watching China's refined copper imports rise is whether this represents a durable trend shift or a temporary restocking cycle. The honest answer involves separating two distinct signals that are both present simultaneously.

The cyclical component is the smelter maintenance-driven supply gap. This is inherently temporary. Once maintenance concludes and Chinese smelting facilities return to normal operational capacity, domestic refined output will recover, reducing the need for imports to bridge the shortfall. Analysts at Shanghai Metals Market have explicitly forecast that the Q2 2026 maintenance cycle will cut refined metal output, implying that this particular import driver has a defined end date.

The structural component is the underlying consumption growth driven by power grid investment and EV manufacturing. These demand drivers are not temporary. Grid investment programs operate on multi-year capital expenditure cycles. EV production growth follows vehicle fleet transition trajectories measured in decades. The copper demand generated by these sectors does not evaporate when smelter maintenance concludes.

The 2025 Context: Why This Recovery Carries Extra Weight

The significance of the Q2 2026 import acceleration is amplified by the context of 2025's depressed baseline. Full-year 2025 refined copper imports fell to approximately 3.35 million metric tons, the lowest net import figure in roughly three years, as expanded domestic smelting capacity absorbed more of the concentrate supply pipeline and as export volumes of fabricated copper products surged.

China exported approximately 790,000 metric tons of refined copper in 2025, a 73.67% year-on-year increase, enabled partly by value-added tax rebates on fabricated copper products and lucrative arbitrage to Western markets. This export surge was a structural anomaly rather than a sign of long-term domestic surplus. The Q2 2026 import uptick therefore represents not merely a seasonal correction but a meaningful reversal of a multi-year trend in net refined copper trade flows.

When a trend as entrenched as China's declining net refined copper imports reverses sharply within a single quarter, the prudent analytical response is to investigate whether the structural forces supporting that reversal are durable or transient.

The next major ASX story will hit our subscribers first

How Are Global Copper Prices Responding to China's Import Signals?

LME Benchmark Price Movements

On May 9, 2026, LME copper prices climbed to their highest level since January 29, the date when the benchmark reached an all-time record of $14,527.50 per metric ton. (Mining Weekly, May 11, 2026) The copper price highs seen in recent months reflect a market pricing in the combination of Chinese physical demand acceleration, smelter maintenance-related supply constraints, and the broader speculative positioning that tends to follow momentum in precious metals markets.

Price strength has been most pronounced during Asian trading hours, a pattern consistent with the weight of Chinese physical demand signals rather than purely speculative Western positioning.

| Price Milestone | Level | Period | Driver |

|---|---|---|---|

| All-Time Record High | $14,527.50/mt | January 29, 2026 | Multiple demand catalysts |

| Near-Record Recovery | Approaching record | May 2026 | China import acceleration |

| 2025 Average | Below $14,000/mt | Full year 2025 | Export surge, weak net imports |

| Q1 2026 Average | Recovering | Jan-Mar 2026 | Grid investment recovery |

The COMEX-LME Spread and Trade Flow Distortions

The 2025 COMEX premium driven by US tariff concerns created a temporary but significant distortion in global copper trade flows. Chinese copper that would normally have been absorbed into domestic fabrication was rerouted toward COMEX delivery, reducing the volume available for local consumption. As this arbitrage window closed and COMEX premiums normalised, the redirected supply came back into the Chinese consumption pool, initially easing import pressure but subsequently creating inventory conditions that now support rising imports as stockpiles have drawn down.

Current market structure appears to reflect modest contango in forward curves, suggesting that near-term physical supply remains broadly adequate but that tighter conditions are anticipated in coming months. This forward curve dynamic is consistent with the broader narrative of Q2 imports rising to bridge a maintenance-induced supply gap before smelter capacity returns online. In addition, the underlying copper price drivers continue to reinforce the structural case for elevated prices across both benchmark markets.

What Are the Broader Structural Forces Reshaping China's Copper Import Patterns?

The Long-Term Demand Architecture

China accounts for approximately 40-50% of global copper consumption, a share that has remained remarkably stable even as domestic processing capacity has expanded. The underlying demand drivers supporting this consumption level are becoming more entrenched, not less:

- Power grid modernisation requires sustained copper investment across transmission, distribution, and smart grid infrastructure for years to come

- Electric vehicle manufacturing continues to expand as both domestic demand and export ambitions grow

- Renewable energy integration at utility scale requires copper-intensive inverters, cables, and grid connection equipment

- Data centre construction, accelerated by artificial intelligence infrastructure investment, adds a newer but rapidly growing source of copper consumption

Supply-Side Constraints from Major Producing Nations

While China's demand trajectory points upward, the supply side of the global copper equation faces its own set of pressures. Major producing nations including Chile, Peru, and the Democratic Republic of Congo have all faced production challenges in recent years from ore grade deterioration, water access constraints, community opposition, and regulatory changes. These supply-side risks create a structural floor beneath copper prices that complements the demand-driven price support from Chinese consumption.

African copper producers in the DRC and Zambia, along with South American exporters, stand to benefit most from any sustained increase in Chinese import demand. Elevated import volumes from China provide revenue certainty for mining operations in these regions and can incentivise additional capital investment in expansion projects.

The Evolving Import Composition: A Long-Term Structural Shift

The most important long-term trend reshaping China's copper import pattern is the shift from refined metal imports toward concentrate imports. As Chinese smelting capacity continues to grow, the country's preference will increasingly be to import raw material and capture the processing margin domestically rather than paying for finished refined metal.

Monitoring the ratio of concentrate imports to refined metal imports over time provides investors and analysts with a leading indicator of China's smelting capacity utilisation rate and its appetite for finished copper from external sources. When concentrate imports surge while refined imports decline, it signals Chinese smelter expansion. When refined imports rise despite high domestic capacity — as is occurring in Q2 2026 — it signals a genuine consumption-supply imbalance that the processing system cannot immediately correct.

FAQ: China's Refined Copper Imports and Global Market Implications

Why Are China's Refined Copper Imports Rising in Q2 2026 After Falling in 2025?

The Q2 2026 acceleration reflects several overlapping forces: post-Lunar New Year demand recovery that has been stronger and less price-sensitive than typical, scheduled smelter maintenance reducing domestic refined output, rapid SHFE inventory drawdowns signalling near-term supply tightness, and accelerating downstream orders from power grid and EV sectors.

What Was China's Refined Copper Import Volume in April 2026?

China imported approximately 452,000 metric tons of refined copper in April 2026, the highest monthly figure since September, representing a 9% increase over March according to customs data released on May 10, 2026.

How Low Are Shanghai Futures Exchange Copper Stockpiles?

As of May 11, 2026, SHFE copper stockpiles stood at 181,333 metric tons, the lowest level since January 2026, following a 5.6% week-on-week decline.

What Is Driving Copper Price Strength in 2026?

Prices are being supported by Chinese physical demand acceleration, smelter maintenance-related supply constraints, speculative investor positioning following precious metals momentum, and proximity to the all-time benchmark record of $14,527.50 per metric ton set on January 29, 2026.

What Sectors Are Consuming the Most Copper in China Right Now?

Power grid infrastructure represents the primary demand driver, with grid investment rising 37% year-on-year in Q1 2026. Electric vehicle manufacturing is the second major growth sector, with demand further accelerated by regional energy security concerns linked to the Iran conflict.

Is the Q2 2026 Import Surge Likely to Persist Beyond the Smelter Maintenance Cycle?

The maintenance-driven component of the surge will normalise once smelters return to full operation. However, the structural demand from grid investment and EV manufacturing provides a durable consumption floor that will continue pulling on available domestic copper supply regardless of smelting capacity levels.

Key Takeaways: What China's Import Surge Means for Investors and Industry

Short-Term Positioning Considerations (Q2-Q3 2026)

- Refined copper import volumes are likely to remain elevated through Q2 while smelter maintenance continues and inventory drawdowns persist

- The self-reinforcing dynamic of fabricators front-loading orders to avoid supply disruptions can amplify import volumes beyond what underlying consumption growth alone would suggest

- LME and SHFE price benchmarks face upward pressure, particularly if supply disruptions at major South American or African mines coincide with peak Chinese demand periods

Medium-Term Structural Considerations

- China's long-term trajectory favours greater domestic processing self-sufficiency, which will structurally reduce refined import dependence over time even as concentrate imports continue growing

- The Q2 2026 surge may represent a cyclical correction within a broader multi-year trend toward lower net refined imports, making it important not to extrapolate the current pace indefinitely

- The concentrate-to-refined import ratio remains the most reliable structural indicator of whether China's smelting capacity is absorbing more of the raw material pipeline or creating genuine gaps that require finished metal imports

Global Supply Chain Implications

Higher Chinese demand for refined copper pulls available inventory away from European and North American markets, tightening global physical availability and supporting benchmark prices across all regions. For investors monitoring copper producers, smelters, and downstream fabricators across multiple geographies, the directional signal from China refined copper imports rising on strong demand is clear: the world's dominant copper consumer is drawing more heavily on the global supply pool, and the structural forces sustaining that consumption are not diminishing. Those exploring copper investment strategies should consider how this demand trajectory reinforces both near-term and long-term positioning within the metal's market cycle.

This article draws on data and market commentary reported by Mining Weekly (May 11, 2026), including statements made by Nicholas Snowdon of Mercuria and Li Ye of Eagle Metal at the LME Week conference in Hong Kong. The analysis reflects conditions as of publication and should not be construed as financial advice. Commodity markets involve significant uncertainty, and forward projections regarding import volumes, price levels, and demand trajectories are inherently speculative. Readers should conduct independent research and seek professional guidance before making investment decisions.

Want to Stay Ahead of the Next Major Copper Discovery on the ASX?

As copper demand surges on the back of China's accelerating grid investment and EV manufacturing boom, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX copper and critical mineral discoveries — transforming complex market data into actionable investment insights the moment they hit the exchange. Explore how major mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.