June 19, 2026

The Architecture of Control: How State-Trading Authorization Is Reshaping Silver's Global Flow

Commodity markets have a long history of price cycles driven by exploration booms, technology shifts, and macroeconomic pivots. However, a more structural force is now at work in silver markets, one that operates upstream of price discovery itself. When governments reclassify a commodity from a commercial good into a strategic national asset, the rules governing who can sell it, and to whom, change fundamentally. That is precisely what is unfolding as the China silver export whitelist advances through 2026, and the implications for supply security, asset valuation, and investment strategy are only beginning to be priced in.

When big ASX news breaks, our subscribers know first

China's Silver Export Whitelist: What the Policy Actually Does

Most commentary on China's commodity export controls focuses on volume restrictions. The China silver export whitelist operates differently, and understanding that distinction matters for anyone evaluating silver supply risks.

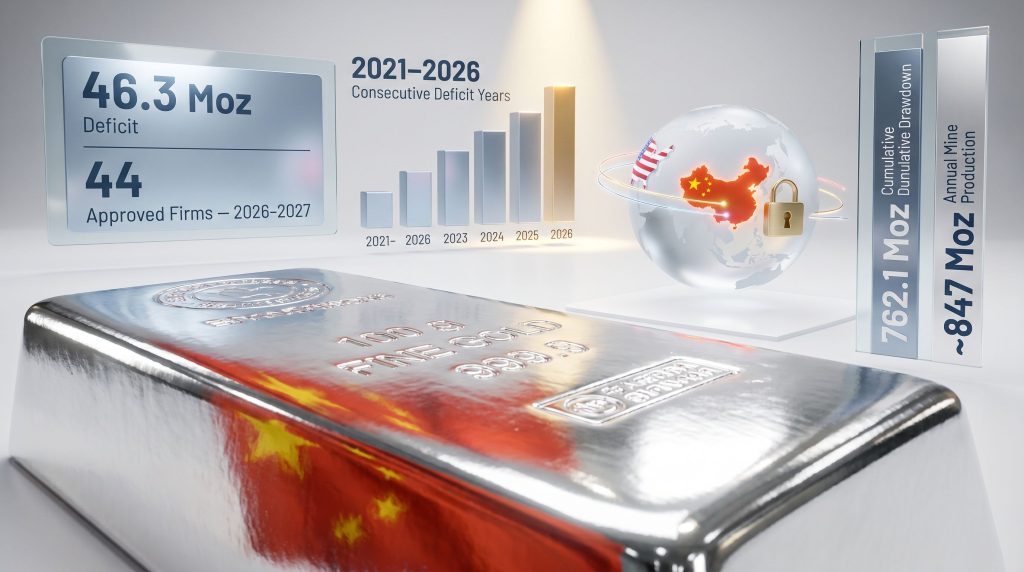

Effective January 1, 2026, China's silver export rules saw China's Ministry of Commerce replace its previous quota-based silver export mechanism with a state-trading authorization framework. Under this structure, only companies appearing on an officially published list are permitted to move silver across Chinese borders into international markets. The 2026 to 2027 whitelist names 44 approved firms, an increase of two from the prior period's 42.

How Does a Whitelist Differ From a Quota System?

The volume distinction is important but secondary. The more consequential shift is institutional. A quota system caps how much can leave. A whitelist system determines who is legally permitted to make that decision in the first place. Beijing now holds discretionary authority over which commercial entities can participate in international silver trade, an instrument of control that no quota mechanism could replicate.

This places silver within a club of commodities that China has already brought under similar state-trading frameworks:

| Strategic Material | Control Mechanism | Whitelist or Licensing |

|---|---|---|

| Rare Earths | Export licensing and quotas | Whitelist |

| Tungsten | State-trading authorization | Whitelist |

| Antimony | Export licensing | Whitelist |

| Gallium and Germanium | Export licensing | Licensing |

| Silver | State-trading whitelist | 44 approved firms (2026-2027) |

The progression is deliberate. Each addition to this framework reflects a commodity that Chinese policymakers have assessed as carrying strategic value beyond its commercial price. Furthermore, silver's inclusion is not an isolated administrative adjustment — it is the continuation of a documented policy trajectory that began accelerating in 2023. For context on how China's exclusive export list fits within broader critical metals strategy, this shift signals a deepening of state control across a widening range of materials.

Six Consecutive Deficits: Why the Timing of Export Controls Is Significant

Policy changes do not occur in a vacuum. The China silver export whitelist has been activated against a supply backdrop that was already under stress before any regulatory intervention. Indeed, the silver-supply deficits that preceded this policy shift have left global inventories substantially thinner than they were five years ago.

According to the Silver Institute's World Silver Survey 2026, the market is projected to record a deficit of 46.3 million ounces (Moz) in 2026, extending a run of consecutive annual shortfalls that began in 2021. The cumulative drawdown from above-ground silver inventories over this period has reached 762.1 Moz, a figure that approaches the equivalent of an entire year of global mine production.

| Year | Market Condition | Notes |

|---|---|---|

| 2021 | Deficit begins | Drawdown cycle initiated |

| 2022 | Deficit continues | Inventory depletion accelerates |

| 2023 | Deficit widens | Policy restrictions begin emerging |

| 2024 | Deficit persists | Approaching critical inventory levels |

| 2025 | Fifth consecutive deficit | 762.1 Moz cumulative drawdown |

| 2026 (projected) | 46.3 Moz deficit | Sixth consecutive year |

Global mine production remains anchored near 847 Moz annually. A cumulative drawdown of 762.1 Moz therefore represents approximately 90% of one year's total mine output already removed from accessible above-ground stocks. The buffer that historically absorbed supply disruptions is consequently far thinner than it was five years ago.

Structural Risk Signal: When above-ground inventory drawdowns approach the equivalent of annual mine output, the market's capacity to absorb additional supply shocks narrows sharply. Export controls applied in this environment carry disproportionate price and availability consequences compared to the same controls imposed during periods of inventory surplus.

The October 2025 silver market provided a real-world preview of this dynamic. During that period, unencumbered LBMA silver inventories fell to historically low levels while lease rates surged, demonstrating the speed at which accessible supply can evaporate. That episode preceded the formal activation of the whitelist system and suggests the underlying supply tightness was already present before additional policy layers were introduced.

Why Silver Supply Cannot Respond Quickly to Demand Signals

One of the less widely understood structural features of silver markets is the degree to which supply decisions are made by people who are not primarily focused on silver at all. Approximately 75% of global silver production is extracted as a by-product of copper, lead, zinc, and gold mining operations.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold and Silver, has articulated this constraint clearly: the majority of silver supply cannot simply be switched on when market demand increases, because production decisions in those operations are governed by the economics of a different primary metal entirely.

| Production Category | Share of Global Supply | Price Sensitivity to Silver | Development Lead Time |

|---|---|---|---|

| By-product mining (copper, lead, zinc, gold) | ~75% | Low | Tied to primary metal decisions |

| Primary silver mines | ~25% | Higher | 5 to 10 years from discovery to production |

The consequence is structural inelasticity. Even when silver prices rise and investment rationale for new primary mines improves, the pipeline from discovery through permitting, engineering, financing, construction, and commissioning typically spans five to ten years. Higher prices today do not translate into additional mine output for the better part of a decade.

Americas Gold and Silver reported record silver production of approximately 787,000 oz in Q1 2026 and guided toward full-year output of 3.2 to 3.6 Moz. In a market where total mine supply is flat and most incremental silver comes from by-product streams, production growth from a dedicated primary silver producer carries unusual scarcity value.

Dual-Jurisdiction Control: When Both Major Economies Classify the Same Metal

China's whitelist system does not operate in isolation. The United States formally added silver to its critical minerals list in late 2025, a designation that activates government authority over stockpiling priorities, supply chain funding, and trade screening mechanisms. As a critical mineral silver designation, this reflects a broader strategic reassessment of the metal's importance to national security and industrial resilience.

The simultaneous classification of silver as strategically critical by the world's two largest economies creates a market condition with no modern precedent in silver trading history. Each policy framework independently restricts the free movement of silver. Combined, they create overlapping constraints that reduce the total volume of silver flowing freely through international markets.

| Policy Dimension | China | United States |

|---|---|---|

| Classification | Strategic material | Critical mineral |

| Export mechanism | 44-company whitelist | Export screening (developing) |

| Stockpiling intent | State-directed | Domestic reserve building signalled |

| Effective date | January 1, 2026 | Late 2025 designation |

| Primary scope | Export authorisation control | Supply chain security |

Historical precedents in adjacent markets suggest this type of dual-jurisdiction convergence can trigger meaningful valuation divergence. Moreover, antimony shortage risks have already demonstrated how similar export control frameworks can reshape supply chains for critical industrial materials. Silver is at an earlier stage of this repricing process.

Development-Stage Projects and the Gap Between Feasibility and First Metal

Even economically compelling silver projects face a substantial timeline between completing a feasibility study and delivering metal into international markets. Vizsla Silver's November 2025 feasibility study for the Panuco project in Mexico illustrates both the quality of projects currently advancing through the development pipeline and the development gap that separates a study from production.

| Panuco Project Parameter | Feasibility Study Figure |

|---|---|

| Average annual production | 17.4 Moz silver equivalent |

| Initial mine life | 9.4 years |

| After-tax NPV | US$1.8 billion |

| IRR | 111% |

| Payback period | 7 months |

| Silver price assumption | US$35.50/oz |

| Gold price assumption | US$3,100/oz |

Those economics are exceptional by any historical benchmark. Yet permitting, detailed engineering, equipment procurement, financing, and construction still separate those numbers from a tonne of ore processed and an ounce of silver poured.

Jesus Velador, Vice President of Exploration at Vizsla Silver, has described the disciplined focus on de-risking the mineral resource at the Copala area, where the company envisions the initial years of production at Panuco, including the establishment of a measured resource within the high-grade central portion of Copala for the first time.

The next major ASX story will hit our subscribers first

Exploration Drilling as the Earliest Stage of Future Supply

Drill results occupy a distinct position in the silver supply chain. They represent the earliest identifiable signal of potential future metal availability, but they sit several steps removed from production decisions, resource classifications, feasibility studies, and mine construction.

GR Silver Mining's May 2026 drill result at the San Marcial project returned 45.1 metres of true width grading 1,623 g/t silver, including an interval of 8.25 metres at 8,579 g/t. Understanding true width drill results is essential here, as these figures reflect actual mineralised thickness rather than apparent widths that can overstate a deposit's significance. Results of that grade are exceptional within the context of global silver exploration, but they do not by themselves establish a resource estimate, demonstrate project economics, or define a production timeline.

Eric Zaunscherb, Interim President and Chief Executive Officer of GR Silver Mining, has outlined the company's belief that its existing resource base of 134 million ounces of silver equivalent has significant growth potential through a 20,000-metre drill programme. The San Marcial resource's average thickness of approximately 22 metres is noted as a geological characteristic that supports efficient resource expansion.

Demand Trends: Where the Structural Support Is Coming From

Solar panel manufacturers have reduced silver loadings per unit by approximately 19% through ongoing thrifting and substitution efforts. However, demand from AI infrastructure build-out, data centre power systems, advanced electronics, and physical investment continues to offset industrial thrifting gains.

The Silver Institute projects that rising investment demand will partially compensate for weakness in industrial fabrication in 2026. Net demand nevertheless exceeds net supply, producing the sixth consecutive annual deficit. The silver market squeeze dynamic has consequently become a more pressing concern for institutional investors and policymakers alike, particularly as the structural demand base has broadened considerably beyond any single industrial application.

Risk Factors That Could Undermine the Supply Security Thesis

A balanced assessment of the China silver export whitelist and its implications requires acknowledging the forces that could limit or delay the bullish supply security thesis:

- Monetary policy headwinds: A hawkish US Federal Reserve and a strengthening US dollar increase the opportunity cost of holding non-yielding assets. Silver prices can decline in the near term even when structural deficits persist.

- Policy reversal risk: Whitelists and critical mineral designations are administrative instruments. A shift in geopolitical conditions or trade negotiations could modify, suspend, or expand the scope of export controls.

- Demand-side substitution: Manufacturers continue to reduce silver intensity per unit where technically feasible. If thrifting accelerates beyond current projections, the demand side of the equation could weaken regardless of supply constraints.

- Financing and permitting risk: Development-stage projects with compelling feasibility economics can still encounter financing market weakness, permitting delays, or construction cost overruns that extend timelines beyond initial projections.

How Jurisdiction Is Becoming a Silver Valuation Variable

Institutional investors applying enterprise value per ounce (EV/oz) frameworks to silver resource companies traditionally weight resource size, grade, and project economics most heavily. However, export controls are introducing a fourth dimension: whether the silver can reach international markets freely once it is produced.

Projects located in jurisdictions with unrestricted trade access, including the United States, Canada, Mexico, and Australia, may attract increasing relative attention. Furthermore, China's silver export licensing requirements taking effect in early 2026 have reinforced why jurisdictional positioning is becoming a more systematically priced consideration in silver asset valuations.

| Valuation Factor | Pre-Whitelist Weight | Post-Whitelist Consideration |

|---|---|---|

| Resource size (Moz) | High | Unchanged |

| Grade (g/t) | High | Unchanged |

| Project economics (NPV, IRR) | High | Unchanged |

| Jurisdiction and trade access | Low to Medium | Increasing |

| Development stage | Medium | Increasing |

| Export restriction exposure | Minimal | Emerging risk variable |

This repricing dynamic has not yet reached the degree of valuation divergence observed in rare earth markets following China's 2010 export restrictions. Silver is at an earlier stage of that process, meaning the jurisdictional premium has not yet been fully captured in current market valuations.

Frequently Asked Questions: China's Silver Export Whitelist and Global Supply Security

What is China's silver export whitelist and how does it operate?

China's Ministry of Commerce replaced its quota-based silver export system with a state-trading authorisation framework effective January 1, 2026. Only companies appearing on the officially published whitelist — comprising 44 approved firms for 2026 to 2027 — are legally authorised to export silver from China. This adds an institutional approval layer to silver exports that the previous quota system did not require.

Why does the whitelist matter when only two companies were added to the list?

The number of approved firms is less significant than the structural mechanism itself. The whitelist determines who can participate in silver export at all, not merely how much can leave. Any company outside the 44-firm list faces a legal barrier to exporting silver regardless of price or demand conditions.

Could silver prices fall even if export controls remain active?

Yes. Monetary policy operates independently of commodity supply fundamentals. A hawkish Federal Reserve and a stronger US dollar can suppress silver prices by increasing the opportunity cost of holding non-yielding assets. Silver can consequently experience price weakness in the near term even when structural deficits persist and export controls remain in place.

How quickly can new primary silver supply realistically reach the market?

New primary silver mines require approximately five to ten years from discovery through permitting, engineering, financing, and construction before production commences. By-product silver supply, which represents roughly 75% of global mine output, cannot be directed toward silver production in response to silver price signals alone.

What should investors examine when evaluating silver assets in this environment?

Three analytical lenses are increasingly relevant. First, supply security and jurisdiction: assess whether silver production is located in jurisdictions with unrestricted market access. Second, production stage and development timeline: distinguish between operating producers, development-stage projects, and exploration-stage assets. Third, monetary policy versus structural fundamentals: recognise that near-term price movements may diverge from multi-year supply dynamics.

This article is for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and forward-looking statements involve inherent uncertainty. Readers should conduct their own due diligence and consult a qualified financial adviser before making any investment decisions. References to specific companies and projects are for illustrative purposes and do not constitute a recommendation to buy or sell any security.

Want to Know Which ASX Silver Explorers Could Benefit From Tightening Global Supply?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex exploration data into actionable investment insights — explore historic discoveries and their returns to understand what major finds can mean for early investors, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.