June 12, 2026

The world's commodity markets face unprecedented shifts as traditional supply-demand relationships undergo fundamental restructuring. Global trade flows increasingly reflect strategic national priorities rather than purely economic considerations, with major economies repositioning their industrial policies around resource security and export competitiveness. This transformation creates ripple effects across international steel, iron ore, and raw material markets that extend far beyond immediate pricing dynamics, particularly as china steel exports iron ore imports reach unprecedented levels.

Mining companies and commodity traders must now navigate an environment where geopolitical considerations drive market access, regulatory frameworks shape production decisions, and supply chain diversification becomes essential for long-term sustainability. Furthermore, the intersection of domestic policy adjustments and international trade relationships creates new opportunities and risks for stakeholders across the commodity value chain.

Understanding China's Dual Steel-Iron Ore Strategy

What Drives China's Record-Breaking Steel Export Performance?

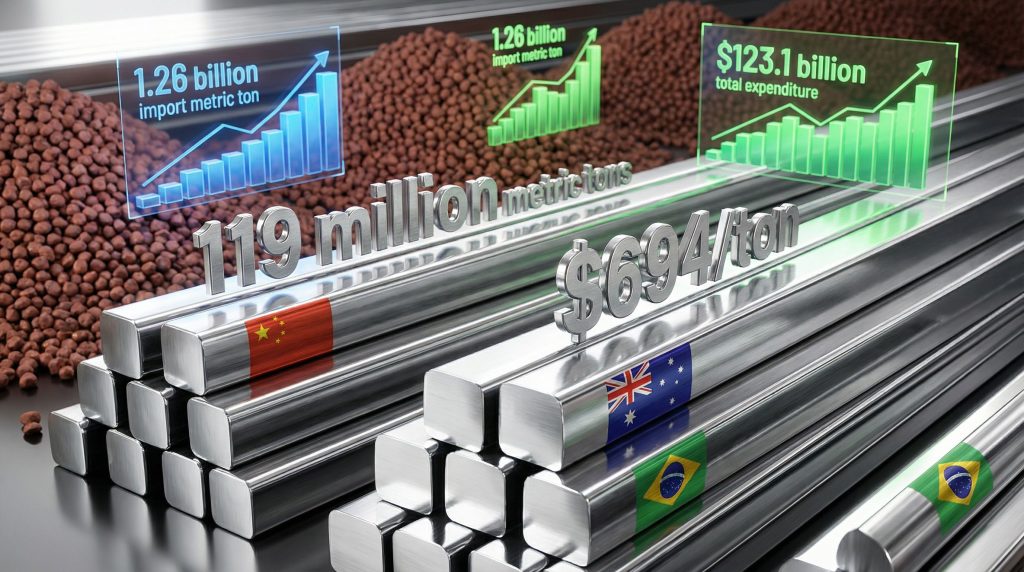

China's steel export trajectory reached unprecedented levels in 2025, with total shipments climbing to 119.02 million metric tons, representing a significant 7.5% year-over-year increase. This performance reflects deeper structural dynamics within China's industrial economy, where domestic demand constraints have redirected production capacity toward international markets.

The surge intensified dramatically in December 2025, when monthly exports peaked at 11.3 million metric tons, establishing the highest single-month record in the country's export history. Consequently, this acceleration pattern demonstrates how regulatory announcements can trigger immediate market responses, as producers rushed to maximise shipments before anticipated licensing requirements took effect.

Several interconnected factors drive this export momentum:

• Domestic property market contraction reducing internal steel consumption by 5.4% annually

• Production overcapacity absorption through international market expansion

• Front-loading strategies ahead of 2026 regulatory changes

• Export profitability margins providing attractive alternatives to domestic sales

• Currency exchange advantages supporting competitive international pricing

The property sector crisis fundamentally altered China's steel demand landscape, forcing producers to restructure their market strategies. With residential and commercial construction activity declining substantially, steelmakers pivoted toward export-oriented production models to maintain capacity utilisation rates and preserve employment levels.

This strategic shift reflects broader economic transition patterns, where China's industrial sectors adapt to reduced infrastructure-intensive domestic development while leveraging manufacturing capabilities to serve global markets. In addition, the $694 per ton average export pricing demonstrates competitive positioning that enables market penetration despite international trade barriers and tariffs impact overview.

How China's Iron Ore Import Dependency Reaches New Heights

China's iron ore import volumes reached record levels in 2025, totalling 1.26 billion metric tons with a 1.8% increase from 2024 levels. This growth occurred despite declining domestic steel production, creating an apparent paradox that reveals sophisticated inventory and production management strategies within China's steel sector.

December 2025 marked a particularly significant milestone, with monthly imports surging 8.2% month-over-month to 119.65 million tons, establishing the highest monthly import volume on record. This timing coincided with year-end restocking activities and strategic inventory building ahead of anticipated 2026 market changes.

The import surge stems from multiple converging factors:

• Low in-plant inventory levels maintained since late 2022 creating restocking demand

• Improved steel profit margins encouraging additional raw material purchases

• Attractive global pricing at approximately $98 per metric ton average

• Export-oriented production requirements necessitating consistent raw material input

• Working capital optimisation strategies maximising inventory turns

Chinese steelmakers deliberately maintained below-optimal inventory levels throughout 2023-2024 due to cash flow pressures from the property market crisis. This conservative approach created pent-up restocking demand that materialised in 2025 as export opportunities improved and financing conditions stabilised.

The $123.1 billion total expenditure on iron ore imports demonstrates the massive scale of China's raw material requirements. However, this investment reflects strategic calculations where import costs are justified by export revenue generation and competitive positioning in global steel markets, linking directly to iron ore price trends.

Geographic supply concentration remains a critical consideration, with Australia and Brazil dominating China's import supply chain. This concentration creates both negotiation leverage for bulk purchasing and strategic vulnerability if geopolitical tensions affect supplier relationships.

When big ASX news breaks, our subscribers know first

Global Supply Chain Implications

What Does China's Steel Export Boom Mean for International Markets?

China's record steel export performance creates cascading effects across global steel markets, fundamentally altering competitive dynamics in major importing regions. The 119.02 million ton annual export volume represents the largest single-country steel export programme in modern industrial history, generating both opportunities and challenges for international stakeholders.

Trade protection responses have proliferated across major economies, yet have proven insufficient to counteract China's export momentum. Multiple countries have implemented anti-dumping duties, import quotas, and tariff measures, arguing that domestic manufacturing sectors face competitive displacement from Chinese imports, particularly amid broader us-china trade war effects.

Key market impacts include:

• Downward price pressure on global steel markets from increased supply

• Competitive displacement affecting regional steel producers' market share

• Infrastructure project economics benefiting from lower steel input costs

• Trade dispute escalation as importing nations seek protection measures

• Supply chain realignment as buyers optimise sourcing strategies

The price dynamics create complex trade-offs for importing nations. Lower steel costs benefit construction, manufacturing, and infrastructure sectors, potentially accelerating economic development projects. However, these same price advantages threaten domestic steel producers' viability, creating employment and industrial capacity concerns.

Regional market displacement patterns vary significantly across different geographic areas. Southeast Asian countries, with developing industrial bases, often welcome competitive steel imports to support infrastructure development. In contrast, established steel-producing nations in North America and Europe face greater pressure to protect domestic manufacturing capabilities.

How Global Iron Ore Producers Benefit from China's Import Appetite

Global iron ore producers experience sustained demand growth despite China's reduced domestic steel production, reflecting the export-oriented production strategies that maintain raw material requirements. The 1.26 billion metric tons of annual Chinese imports represent approximately 60-65% of worldwide iron ore trade flows.

Industry analysts project 2.5% global supply growth in 2026, with 36-38 million additional metric tons directed toward Chinese markets. This supply expansion occurs against sustained demand from China's export-focused steel production, creating relatively stable market conditions despite increased volumes and supporting iron ore demand insights.

Major iron ore mining companies benefit through:

• Sustained volume growth from China's import expansion

• Long-term demand visibility supporting investment planning

• Market share concentration among established suppliers

• Pricing stability despite increased global supply capacity

• Geographic diversification reducing dependence on single markets

Australia and Brazil maintain dominant positions in China's supply chain, controlling over 80% of import volumes. This concentration provides significant bargaining power for major mining companies while creating supply security considerations for Chinese steelmakers, similar to expansion strategies employed by companies like zijin mining expansion.

The forecast supply increases may generate downward pricing pressure throughout 2026, as analysts anticipate that production growth could outpace demand expansion. However, China's continued import appetite provides a substantial demand floor supporting global iron ore markets.

Economic and Policy Framework Analysis

Why China's 2026 Export Licensing System Matters

China's introduction of export licensing requirements beginning in 2026 represents a fundamental shift from quantity-based to quality-focused trade policies. This regulatory transformation responds to mounting international protectionist pressure while enabling Chinese authorities to manage export flows more strategically.

The licensing system announcement triggered immediate market responses, with producers accelerating shipments to establish higher baseline volumes before regulatory implementation. December 2025's 11.3 million ton monthly exports directly resulted from this front-loading behaviour.

Key regulatory implications include:

• Export volume management enabling government control over international shipments

• Product quality emphasis encouraging higher-value steel production

• Trade relationship management addressing international concerns proactively

• Industry consolidation pressure favouring larger, more efficient producers

• WTO compliance considerations maintaining consistency with international trade rules

The transition from unrestricted exports to licensed shipments fundamentally alters China's steel industry dynamics. For instance, producers must now demonstrate export value rather than simply maximising volume, encouraging technological upgrades and product specialisation.

Expected export volume corrections suggest annual shipments may decline to 90-100 million tons range, representing a 15-20% reduction from 2025 levels. This adjustment could ease international trade tensions while maintaining China's position as a major global steel supplier.

What China's Steel Consumption Decline Reveals About Economic Transition

China's domestic steel consumption declined 5.4% in 2025, with projections indicating further 1% reduction in 2026. This consumption pattern reflects broader economic transformation as China transitions from infrastructure-intensive growth toward service sector expansion.

The property sector crisis serves as the primary driver of reduced steel demand, with residential and commercial construction activity falling substantially. Consequently, this sectoral shift forces steel producers to fundamentally restructure their business models and market strategies.

Economic transition indicators include:

• Infrastructure investment moderation reducing steel-intensive development projects

• Service sector growth generating lower raw material requirements per GDP unit

• Industrial efficiency improvements optimising steel utilisation in manufacturing

• Export dependency increase as domestic demand stabilises at lower levels

• Regional development rebalancing affecting steel consumption geographic distribution

This transition creates long-term implications for global commodity markets, as China's traditional role as the world's primary raw material consumer evolves toward more selective, efficiency-focused demand patterns.

Market Dynamics and Investment Perspectives

How Steel Production Efficiency Changes Affect Raw Material Demand

China's steel sector demonstrates improving production efficiency through the relationship between output and raw material consumption. The 892 million tons of steel production against 1.26 billion tons of iron ore imports reflects technological advancement and inventory optimisation strategies.

Efficiency improvements manifest through:

• Higher ore utilisation rates from technological advancement

• Inventory management optimisation reducing working capital requirements

• Production scheduling flexibility enabling demand-responsive output

• Quality upgrading focusing on higher-value product segments

• Energy efficiency gains reducing production costs per ton

These efficiency trends affect global commodity demand patterns, as China's steel sector maintains output levels with optimised raw material consumption. Furthermore, the implications extend beyond iron ore to include coking coal, limestone, and other steelmaking inputs.

What Global Commodity Price Trends Signal for 2026

Commodity price dynamics reflect the complex interaction between Chinese demand patterns, global supply capacity, and international trade policies. Iron ore pricing at $98 per metric ton provides attractive economics for Chinese imports while supporting global mining industry profitability.

Price trajectory analysis for 2026 suggests:

| Factor | Impact Direction | Magnitude | Timeline |

|---|---|---|---|

| China Import Growth | Price Support | Moderate | Q1-Q2 2026 |

| Global Supply Expansion | Price Pressure | Significant | H2 2026 |

| Export Licensing Effects | Mixed Impact | Variable | Throughout 2026 |

| Currency Fluctuations | Volatility | High | Ongoing |

Steel export pricing faces margin pressure from both international competition and domestic cost structures. The average $694 per ton export price reflects competitive positioning that may face adjustment as global trade policies evolve.

Strategic Scenarios and Future Outlook

Scenario 1: Successful Export Quality Upgrade

China's transition toward higher-value steel exports could fundamentally reshape global trade relationships. This scenario assumes successful industry adaptation to licensing requirements and quality-focused production strategies.

China Steel Export Transformation Projections

| Metric | Current (2025) | Upgraded Scenario (2026) | Impact |

|---|---|---|---|

| Export Volume | 119M tons | 95M tons | -20% quantity |

| Average Price | $694/ton | $850/ton | +22% value |

| High-Value Products | 35% | 55% | +57% share |

| Trade Disputes | High | Moderate | Reduced friction |

This transformation would benefit both Chinese producers through improved margins and international markets through reduced commodity-grade competition. However, implementation challenges include technology transfer costs, market acceptance of higher-priced Chinese steel, and coordination across thousands of producers.

Scenario 2: Continued Import Dependency Growth

China's iron ore import requirements may continue expanding despite domestic production adjustments, driven by export-oriented steel production and strategic inventory policies.

Supply security considerations include:

• Geographic concentration risks from Australia-Brazil dependence

• Alternative sourcing development requiring substantial investment and time

• Strategic reserve accumulation balancing security against storage costs

• Bilateral relationship management with major supplier nations

• Price negotiation dynamics reflecting import volume leverage

This scenario emphasises the importance of supply chain diversification for both Chinese buyers and global suppliers, with implications for mining investment patterns and trade relationship development.

The next major ASX story will hit our subscribers first

Key Takeaways and Market Implications

Critical Success Factors for Global Steel Markets

China's export licensing transition represents the most significant structural change in global steel trade since the 2015-2016 capacity reduction campaigns, requiring strategic adaptation from both Chinese producers and international competitors.

The convergence of record exports, import dependency, and regulatory transformation creates unprecedented market dynamics. Stakeholders must navigate reduced export volumes, improved product quality, and evolving trade relationships simultaneously.

Success factors include:

• Technological advancement enabling quality upgrading and cost competitiveness

• Supply chain flexibility accommodating regulatory and market changes

• Financial management optimising working capital and inventory strategies

• Trade relationship development reducing friction and protectionist responses

• Market diversification expanding beyond traditional commodity-grade segments

Investment Considerations for Commodity Stakeholders

Iron ore producers face sustained demand growth despite China's steel production decline, reflecting export-oriented consumption patterns and inventory rebuilding. The 36-38 million ton projected increase in China-bound shipments supports mining sector investment and expansion planning.

Steel importers should prepare for potential supply disruptions as China upgrades its export product mix. While overall volumes may decline, higher-value products could command premium pricing, affecting procurement strategies and cost structures.

Currency hedging becomes critical given China's $123.1 billion annual iron ore import exposure. Exchange rate volatility creates both opportunities and risks for international commodity trade relationships.

Regional steel producers may benefit from reduced Chinese competition in commodity-grade segments, potentially improving market share and pricing power in traditional manufacturing applications. However, increased Chinese focus on high-value products could intensify competition in premium market segments.

Investors and industry stakeholders should consult specialised commodity research platforms and mining industry publications for detailed market analysis and investment guidance tailored to specific regional and sectoral considerations.

Ready to Capitalise on China's Massive Commodity Market Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in iron ore and steel-related sectors ahead of the broader market. With China importing 1.26 billion metric tons of iron ore annually, understanding which ASX discoveries could benefit from these unprecedented commodity flows gives investors a crucial edge—explore how major mineral discoveries have historically delivered exceptional returns and begin your 30-day free trial today.