May 12, 2026

Global critical mineral supply chains face unprecedented strain as manufacturing powerhouses scramble to secure long-term access to essential resources. The intersection of energy transition demands, technological advancement, and geopolitical realignment creates complex investment scenarios that extend far beyond traditional market dynamics. Understanding these evolving patterns requires examining how strategic resource acquisition shapes industrial competitiveness across decades rather than quarterly cycles, particularly in mining projects Argentina China Latin America are pursuing together.

Resource security considerations increasingly drive capital allocation decisions in mining sectors, with particular emphasis on lithium, copper, rare earth elements, and industrial metals. The traditional approach of spot market purchasing proves insufficient when manufacturing capacity expansion requires predictable input availability spanning multiple years. This fundamental shift toward vertical integration and upstream control represents a strategic evolution affecting global commodity markets.

What Drives China's Strategic Mining Expansion Across Latin America?

China's comprehensive mining portfolio across Latin America encompasses 48 active mining assets distributed across 12 countries, with an additional 11 cases involving pending agreements or inactive situations. This extensive regional presence reflects systematic resource acquisition rather than opportunistic investment, targeting specific geological formations and regulatory environments that complement domestic manufacturing requirements.

The geographic distribution demonstrates deliberate strategic prioritisation: Argentina leads with 12 unique mining assets, Brazil follows with 11 diversified operations, and Peru contributes 8 significant copper-focused projects. Ecuador and Guyana each host 4 Chinese-controlled mining properties, while Chile maintains notably limited Chinese presence restricted to Tianqi's 22% ownership stake in SQM's lithium operations.

Critical Mineral Supply Chain Vulnerabilities

China's domestic resource constraints create fundamental dependencies on imported critical minerals, particularly for electric vehicle battery manufacturing and renewable energy infrastructure. The country's rapid industrial transformation requires unprecedented volumes of lithium, copper, cobalt, and rare earth elements that exceed domestic production capabilities by substantial margins.

Manufacturing competitiveness depends increasingly on controlling upstream mining operations rather than relying on spot market purchases. Chinese entities recognise that price volatility and supply disruptions can undermine industrial planning, creating strategic incentives to acquire producing assets in stable jurisdictions.

The concentration of critical mineral reserves in specific geographic regions amplifies supply security concerns. Furthermore, developing critical minerals and energy transition strategies requires understanding that Argentina's position within the Lithium Triangle, containing approximately 58% of global lithium reserves, creates natural strategic targets for Chinese investment. Similarly, Peru's copper endowments and Brazil's niobium deposits represent irreplaceable resource concentrations.

Latin America's Competitive Advantages for Chinese Investment

Latin American countries generally maintain regulatory frameworks facilitating foreign direct investment in extractive industries, contrasting with increasingly restrictive policies in other mining jurisdictions. This regulatory clarity enables Chinese entities to acquire controlling stakes and implement long-term operational strategies without significant political interference.

Infrastructure development opportunities create mutual dependencies that extend beyond simple resource extraction. Chinese mining investments often include transportation corridors, processing facilities, and power generation capabilities that benefit broader regional development while securing operational requirements.

The geological complementarity between Latin American mineral endowments and Chinese industrial requirements creates natural partnership opportunities. In addition to traditional deposits, companies are expanding their focus on gold and copper exploration throughout the region, while Argentina's lithium resources, Brazil's niobium and phosphate deposits, and Peru's copper reserves directly address China's most critical supply gaps.

Currency considerations also favour Chinese investment in Latin American mining projects. Local currency depreciation relative to the US dollar can create acquisition opportunities for Chinese entities while reducing operational costs for export-oriented mining operations.

When big ASX news breaks, our subscribers know first

How Does Argentina Lead China's Regional Mining Portfolio?

Argentina hosts 12 Chinese-controlled mining assets, representing 33% of China's total Latin American mining portfolio. This dominance reflects the country's strategic positioning within the Lithium Triangle, encompassing the Jujuy, Salta, and Catamarca provinces where evaporation pond methodologies enable efficient lithium extraction from high-altitude salt flats.

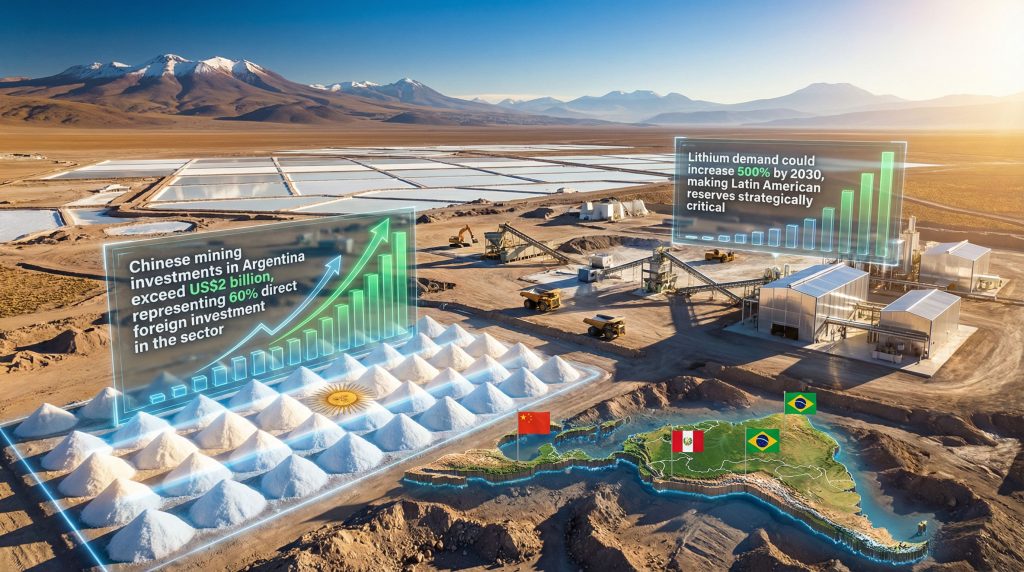

Chinese investments in Argentina exceed $2 billion, representing 60% of direct foreign investment in the mining sector. This concentration establishes Argentina as China's primary regional investment hub, significantly outweighing commitments in other Latin American countries despite their larger economies or more diversified mining sectors. Moreover, developments in the Argentina lithium market insights reveal substantial growth potential for foreign investors.

Lithium Triangle Dominance Strategy

Argentina's Chinese-Controlled Lithium Projects by Production Capacity

| Project | Chinese Entity | Ownership Stake | Annual Production Target |

|---|---|---|---|

| Cauchari-Olaroz | Ganfeng Lithium | 48% | 40,000 tonnes LCE |

| Mariana Project | Ganfeng Lithium | 100% | 20,000 tonnes LCE |

| Pozuelos-Pastos Grandes | Ganfeng Lithium | 100% | Development phase |

| Tres Quebradas | Zijin Mining | 100% | Construction underway |

Ganfeng Lithium's dominant position across multiple Argentine lithium projects demonstrates coordinated capacity building rather than diversified investment. The company's mixed ownership structures balance risk distribution through joint ventures (Cauchari-Olaroz) with operational control through complete ownership (Mariana, Pozuelos-Pastos Grandes).

The technical characteristics of lithium extraction in Argentina create specific operational advantages. Evaporation pond methodologies require extended timelines (12-18 months for lithium concentration through solar evaporation) but operate efficiently in the region's high-altitude, low-precipitation environment. This approach generates lower environmental disruption than hard rock mining while creating predictable production profiles.

Consequently, examining Zijin Mining expansion strategy shows their 100% ownership of the Tres Quebradas project in Catamarca province represents the most recent phase of Chinese lithium development in Argentina. The project's construction timeline extends into the late 2020s, indicating continued Chinese commitment to expanding regional lithium capacity beyond current operational assets.

Beyond Lithium: Diversified Asset Acquisition

Shandong Gold's operations demonstrate Chinese diversification beyond lithium into traditional mining sectors. The company maintains 50% ownership stakes in both Veladero (gold operation) and La Ortiga (copper exploration), indicating intentional positioning across multiple critical minerals within Argentine territory.

The Veladero gold operation represents one of Argentina's most significant precious metal projects, providing Chinese entities with exposure to gold price dynamics while generating cash flow supporting further regional expansion. The 50% ownership structure creates risk sharing with other international partners while maintaining substantial influence over operational decisions.

La Ortiga copper project, also held at 50% by Shandong Gold, demonstrates Chinese engagement in Argentina's copper sector despite the country's secondary position relative to Chile and Peru in regional copper production. This diversification reflects long-term strategic positioning rather than immediate production maximisation.

Investment Scale and Economic Impact

Chinese mining investments in Argentina exceed $2 billion, representing 60% of direct foreign investment in the mining sector, establishing unprecedented foreign presence in the country's extractive industries.

The employment generation from Chinese mining operations creates significant economic multiplier effects across Argentina's northern provinces. Direct employment in lithium extraction, processing, and support services generates additional indirect employment in transportation, maintenance, and local supply chains.

Technology transfer implications extend beyond operational efficiency to include environmental management, safety protocols, and technical training programmes. Chinese entities often implement automation and digital monitoring systems that exceed local industry standards while providing skill development opportunities for Argentine workers.

Local content requirements and industrial development mandates create pressure for Chinese entities to source materials and services within Argentina when possible. This generates supply chain development opportunities while potentially increasing operational costs compared to importing specialised equipment directly from China.

What Makes Brazil China's Second-Largest Mining Hub in the Region?

Brazil hosts 11 Chinese-controlled mining assets, representing 23% of China's total Latin American portfolio. Unlike Argentina's lithium concentration, Brazil's portfolio encompasses niobium, phosphate, iron ore, gold, tin, and downstream processing operations, creating operational complexity but supply chain diversification.

The strategic significance of Brazil's mining portfolio extends beyond raw material extraction toward integrated value chain development. Chinese entities acquire processing capabilities, refinement facilities, and industrial partnerships that capture greater value within Brazil while securing supplies for Chinese manufacturing.

Industrial Metals and Processing Integration

China's Brazilian Mining Assets by Commodity Type

| Commodity | Primary Operations | Chinese Entities | Strategic Significance |

|---|---|---|---|

| Niobium | CBMM (Araxá) | CITIC, Baosteel consortium (15%) | Aerospace/steel applications |

| Gold | Aurizona, Riacho dos Machados | CMOC (100% each) | Precious metals portfolio |

| Phosphate | Catalão complex | CMOC acquisition (2016) | Agricultural fertiliser supply |

| Iron ore | Various partnerships | Multiple entities | Steel production inputs |

CMOC (China Molybdenum Company) exemplifies the integrated approach through 100% ownership of Aurizona and Riacho dos Machados gold operations, combined with phosphate and niobium assets acquired from Anglo American in 2016. This diversified portfolio enables operational coordination and shared infrastructure utilisation.

The niobium sector demonstrates particularly sophisticated Chinese engagement through the CBMM consortium structure. A Chinese collective comprising CITIC, Baosteel, Ansteel, Shougang, and TISCO maintains 15% ownership in CBMM's Araxá operations, representing collaborative state-enterprise coordination for strategic mineral access.

Niobium applications in aerospace manufacturing, high-strength steel production, and specialised alloys create critical supply chain requirements for Chinese industrial development. The CBMM consortium's minority stake provides supply security while limiting capital requirements compared to majority acquisition.

Downstream Value Creation Strategy

Processing facility acquisitions enable Chinese entities to capture value beyond raw material extraction while developing technical capabilities applicable to other regional operations. CMOC's phosphate processing operations convert mineral concentrates into commercially viable fertiliser products for both domestic Brazilian markets and export to China.

Refinement capacity building creates operational flexibility enabling Chinese entities to respond to market conditions and supply chain requirements. Integrated operations can adjust between selling raw concentrates and processed products based on demand patterns and price differentials.

Technology transfer agreements associated with processing operations generate operational expertise applicable across multiple Chinese mining investments in Latin America. Brazilian operations serve as technology development and training centres supporting expansion into other regional markets.

Why Does Peru Remain China's Copper Production Cornerstone?

Peru hosts 8 Chinese-controlled mining assets, representing the third-largest concentration of Chinese mining investments in Latin America. The country's position as China's copper production cornerstone reflects both geological advantages and established operational infrastructure supporting large-scale copper extraction and processing.

Chinese entities control approximately 30% of Peru's copper production through strategic mine ownership, creating substantial influence over global copper supply forecast dynamics. This concentration provides operational coordination opportunities while generating significant exposure to copper price volatility.

Large-Scale Copper Asset Portfolio

Las Bambas operates as one of Peru's largest copper mines under Chinese control, generating substantial production volumes supporting Chinese manufacturing requirements. The operation's scale enables operational efficiency while creating significant logistical coordination requirements for concentrate transportation and processing.

Toromocho represents another major Chinese-controlled copper operation in Peru, demonstrating long-term commitment to Peruvian copper production. The mine's operational performance and reserve life provide production visibility extending multiple decades, supporting long-term supply planning for Chinese industrial requirements.

Galeno development project represents future capacity expansion under Chinese control, with construction timelines and investment requirements extending into the late 2020s. The project's development demonstrates continued Chinese commitment to expanding Peruvian copper capacity despite challenging economic conditions affecting global mining investment.

MMG, Zijin Mining, and Jinzhao Mining Peru represent the primary Chinese entities operating in Peru's copper sector. Each maintains distinct operational approaches and asset portfolios while contributing to China's overall copper supply security from Peruvian sources.

Infrastructure and Logistics Advantages

Peru's established mining infrastructure provides operational advantages for Chinese entities entering the market. Existing transportation networks, port facilities, and processing capabilities reduce capital requirements compared to greenfield development in less developed mining regions.

Processing facility integration with mining operations enables Chinese entities to coordinate extraction and refinement activities, potentially improving operational efficiency while reducing transportation costs. This integration creates operational complexity but provides greater control over production quality and timing.

Long-term offtake agreements between Chinese-controlled Peruvian mines and Chinese manufacturing entities create supply chain coordination extending beyond simple market transactions. These agreements provide price stability and volume guarantees supporting both mining operations and manufacturing planning.

How Do Chinese Mining Investments Create Strategic Opportunities?

Chinese mining investments in Latin America generate opportunities extending beyond traditional financial returns through capital provision, technological integration, and market access coordination. These multifaceted benefits create value for host countries, local communities, and Chinese entities while potentially reshaping regional mining sector dynamics.

Capital Market Access and Project Financing

Funding Gap Analysis for Latin American Mining Projects

- Marginal project development: Chinese capital fills financing gaps that Western capital sources address selectively

- Risk tolerance comparison: Chinese entities demonstrate greater acceptance of political and operational risks

- Development timeline acceleration: Patient capital enables longer development cycles without quarterly pressure

- Infrastructure coordination: Integrated investment approaches include transportation and processing facilities

Chinese capital sources often provide financing for mining projects that struggle to attract Western investment due to perceived risks or marginal economics. This capital availability enables project development that might otherwise remain inactive, creating regional employment and economic activity.

Risk tolerance differences between Chinese and Western capital sources reflect distinct investment horizons and strategic objectives. Chinese state-influenced entities can accept longer payback periods and higher political risks when projects serve strategic supply security objectives rather than purely financial returns.

Development timeline acceleration occurs when Chinese entities provide patient capital supporting extended construction periods without quarterly earnings pressure. This approach enables complex projects requiring substantial infrastructure development to proceed despite uncertain market conditions.

Industrial Integration and Value Chain Development

Processing facility co-location with mining operations creates operational synergies while capturing additional value within host countries. Chinese entities often invest in refinement and processing capabilities that traditional mining companies might outsource to specialised facilities.

Technology transfer requirements associated with Chinese mining investments generate knowledge spillovers benefiting broader regional mining sectors. Advanced extraction techniques, environmental management systems, and operational automation contribute to regional technical capacity development.

Supply chain coordination between Chinese mining operations and manufacturing entities reduces transportation costs while improving delivery reliability. This coordination creates operational advantages unavailable through traditional arm's-length market transactions.

Market Access and Commercial Partnerships

Guaranteed offtake agreements between Chinese mining operations and Chinese manufacturing entities reduce market risk while providing price stability for host countries. These long-term commitments enable project financing and operational planning extending multiple years.

Long-term pricing mechanisms create alternatives to spot market volatility that can undermine mining project economics. Chinese entities often negotiate pricing formulas that balance market exposure with price stability, supporting both mining operations and manufacturing cost planning.

Logistics coordination and shipping optimisation generate operational efficiencies when Chinese entities control both mining operations and downstream transportation. Coordinated shipping schedules, port utilisation, and inventory management create cost advantages over fragmented supply chains.

What Challenges and Risks Accompany Chinese Mining Expansion?

Chinese mining expansion in Latin America generates complex challenges spanning regulatory compliance, operational management, and geopolitical considerations. Understanding these risk factors enables more informed assessment of investment sustainability and potential conflicts affecting project development.

Regulatory and Political Risk Factors

Host country policy changes affecting foreign ownership create ongoing uncertainty for Chinese mining investments. Regulatory frameworks can evolve in response to political pressures, environmental concerns, or strategic resource nationalism, potentially affecting operational permissions or ownership structures.

Environmental compliance requirements increasingly affect mining operations across Latin America, with Chinese entities needing to meet evolving standards that may exceed Chinese domestic requirements. This compliance creates additional costs while potentially generating operational constraints affecting production planning.

Community relations management requires ongoing attention to local social impacts, indigenous rights, and regional development expectations. Chinese entities often face cultural and linguistic barriers that complicate stakeholder engagement while requiring substantial community investment commitments.

Currency fluctuation and capital repatriation restrictions affect profit distribution and financial planning for Chinese mining investments. Host country monetary policies, exchange rate management, and capital controls can significantly impact investment returns and cash flow management.

Operational and Technical Challenges

Remote location infrastructure development requirements create substantial capital commitments extending beyond mining operations. Chinese entities often need to invest in transportation networks, power generation, and communication systems before mining operations can commence.

Skilled workforce availability and training programmes require sustained investment in human resource development. Local technical expertise may be limited, requiring Chinese entities to import specialised personnel while developing local capability through training and education programmes.

Environmental impact mitigation and sustainability standards create ongoing operational requirements that affect both costs and operational flexibility. Chinese entities must implement environmental management systems that meet international standards while potentially exceeding requirements in domestic Chinese operations.

Geopolitical Implications for Host Countries

Balancing Chinese investment with Western partnership requirements creates complex diplomatic considerations that affect trade relationships, security cooperation, and regional integration across Latin America.

Critical mineral security versus foreign dependency concerns create policy tensions for host countries seeking investment while maintaining strategic autonomy. Chinese control over essential mineral supplies generates concerns about potential supply manipulation during diplomatic disputes.

Regional integration effects occur when Chinese mining investments create economic dependencies that influence broader trade relationships and diplomatic alignment. Host countries must balance Chinese investment benefits with maintaining diverse international partnerships.

Trade relationship impacts extend beyond mining sectors when Chinese investments create broader economic integration affecting multiple industry sectors. Mining investments often serve as entry points for expanded Chinese economic engagement in host countries.

The next major ASX story will hit our subscribers first

Which Investment Models Prove Most Successful for Regional Development?

Investment model selection significantly affects outcomes for Chinese entities, host countries, and local communities. Understanding successful approaches enables better evaluation of future investment opportunities while identifying strategies that maximise mutual benefits across stakeholder groups.

Joint Venture Structures vs. Full Ownership

Risk sharing mechanisms through joint venture structures enable Chinese entities to access local expertise while reducing capital requirements and political exposure. Local partners contribute regulatory knowledge, community relationships, and operational experience that Chinese entities might lack.

Technology transfer requirements often prove more effective in joint venture structures where local partners have incentives to absorb and apply advanced techniques. Knowledge spillovers occur more readily when local entities maintain ownership stakes requiring operational involvement rather than simple employment relationships.

Operational control distribution in joint ventures creates decision-making complexity but can improve stakeholder acceptance and regulatory approval processes. Shared control demonstrates commitment to local partnership while providing Chinese entities with operational influence proportional to their investment commitments.

Full ownership structures provide Chinese entities with complete operational control and strategic flexibility but may generate greater political resistance and regulatory scrutiny. Complete ownership eliminates partner coordination requirements while concentrating all risks and rewards within Chinese entities.

Integrated Value Chain Development

Processing Facility Co-location Benefits

| Benefit Category | Quantified Impact | Implementation Timeline |

|---|---|---|

| Transportation cost reduction | 15-25% operational savings | 2-3 years post-construction |

| Employment multiplier effects | 3-5x direct job creation | 5-7 years full development |

| Technology transfer acceleration | 2-3 year timeline reduction | Ongoing operational period |

| Infrastructure sharing opportunities | 20-30% capital cost reduction | Project development phase |

Transportation cost reduction through processing facility co-location generates substantial operational savings by eliminating intermediate shipping and handling requirements. Raw materials processed on-site avoid transportation costs to distant processing facilities while reducing logistical complexity.

Employment multiplier effects occur when processing facilities create additional job opportunities beyond basic mining operations. Processing, maintenance, technical support, and administrative positions generate employment for skilled workers while supporting local service industries.

Technology transfer acceleration occurs when processing facilities require advanced technical expertise that local workers can acquire through direct operational involvement. This knowledge transfer creates regional technical capabilities applicable to other mining and industrial operations.

Community Development and Social Licence

Local procurement requirements create supply chain opportunities for regional businesses while potentially increasing operational costs for Chinese mining entities. Balancing local sourcing mandates with operational efficiency requires careful supplier development and quality management programmes.

Infrastructure sharing agreements enable mining operations to contribute to broader regional development while reducing individual project infrastructure costs. Shared transportation networks, power generation, and communication systems benefit multiple stakeholders while improving project economics.

Environmental stewardship and restoration commitments create long-term operational obligations but support social licence maintenance and regulatory compliance. Chinese entities increasingly implement environmental management programmes that exceed minimum requirements to demonstrate responsible operational practices.

What Future Scenarios Shape China's Latin American Mining Strategy?

Future scenario development requires analysing technological evolution, competitive responses, and regulatory changes that could significantly affect Chinese mining strategy in Latin America. Understanding these potential developments enables more informed assessment of investment sustainability and strategic positioning for mining projects Argentina China Latin America continue developing.

Electric Vehicle Demand Growth Projections

Lithium demand could increase 500% by 2030, making Latin American reserves strategically critical for global electric vehicle production and energy storage applications. This demand growth substantially exceeds current production capacity, creating supply security imperatives for countries dependent on lithium imports.

Battery technology evolution affects mineral requirement patterns, with potential shifts between lithium-ion chemistries changing demand profiles for lithium, cobalt, nickel, and other critical materials. Chinese entities must balance current capacity investments with flexibility to adapt to evolving battery technologies.

Supply security versus market price optimisation creates strategic trade-offs for Chinese entities controlling substantial lithium production capacity. Market power concentration enables price influence but may generate political resistance and alternative supply source development by consuming countries.

Energy storage demand beyond electric vehicles, including grid-scale storage supporting renewable energy integration, creates additional lithium demand growth that could exceed electric vehicle requirements. This diversified demand provides market stability while potentially creating supply constraints.

Competitive Response from Western Investors

Alternative financing mechanisms from Western capital sources respond to increased Chinese presence through competitive investment terms and partnership structures. Western entities increasingly offer patient capital and long-term partnerships to compete with Chinese strategic investments. However, the U.S. critical minerals strategy in Latin America demonstrates heightened competition for resource access.

Technology competition and innovation investment priorities create differentiation opportunities for Western entities emphasising environmental sustainability, community engagement, and governance standards. These competitive advantages may appeal to host countries balancing Chinese investment with Western partnerships.

Market share defence strategies by Western mining companies include acquiring strategic assets, forming defensive partnerships, and developing alternative supply chains that reduce dependence on Chinese-controlled sources. These strategies create competitive pressure while potentially increasing asset values.

Government support for Western mining investments responds to supply security concerns through loan guarantees, diplomatic support, and preferential trade terms. Furthermore, the U.S. has committed $1 billion to critical minerals development across Latin America, creating institutional support and competitive alternatives to Chinese investment while potentially reducing host country bargaining power.

Regional Integration and Trade Agreement Evolution

Belt and Road Initiative expansion into Latin America creates opportunities for coordinated infrastructure development spanning multiple countries and industry sectors. Mining investments serve as anchor projects supporting broader Chinese economic engagement while creating regional integration opportunities.

Bilateral trade agreement negotiations increasingly include mineral supply provisions, technology transfer requirements, and investment protection mechanisms. These agreements create institutional frameworks supporting Chinese mining investments while potentially constraining operational flexibility.

Infrastructure development coordination across multiple countries enables Chinese entities to develop regional transportation networks, processing facilities, and logistical capabilities that support operations spanning national boundaries. This coordination creates operational efficiencies while potentially generating political concerns about Chinese regional influence.

How Can Regional Governments Maximise Benefits from Chinese Investment?

Regional governments possess significant leverage in negotiating terms with Chinese mining investors, particularly when controlling access to essential mineral reserves or strategic locations. Understanding successful negotiation strategies enables governments to capture greater value while maintaining attractive investment environments for mining projects Argentina China Latin America jointly pursue.

Policy Framework Optimisation

Best Practices for Foreign Mining Investment Management

- Local content requirements with realistic implementation timelines enabling gradual supplier development rather than immediate compliance mandates

- Technology transfer mandates with measurable outcomes including training programmes, research partnerships, and knowledge documentation requirements

- Environmental standards exceeding international benchmarks while providing clear compliance pathways and technical assistance

- Community benefit sharing mechanisms ensuring local populations receive direct benefits from mining operations through employment, infrastructure, or revenue sharing

- Infrastructure development coordination requirements ensuring mining investments contribute to broader regional development rather than isolated industrial operations

Local content requirements prove most effective when implemented gradually with technical assistance supporting local supplier development. Immediate high-percentage requirements often generate compliance difficulties while gradual increases enable capacity building and quality improvement.

Technology transfer mandates require specific measurable outcomes rather than general commitments. Training programme enrollment, local employment ratios, research partnership establishment, and knowledge documentation provide concrete benchmarks for compliance assessment and benefit realisation.

Environmental standards that exceed international benchmarks demonstrate commitment to sustainability while potentially creating competitive advantages for host countries. Clear compliance pathways and technical assistance reduce implementation barriers while ensuring effective environmental protection.

Capacity Building and Knowledge Transfer

Technical education partnerships with Chinese universities and research institutions create knowledge transfer opportunities extending beyond operational training. These partnerships enable local technical capacity development while providing Chinese entities with research collaboration opportunities.

Operational training programmes for local workforce development generate sustainable employment opportunities while reducing Chinese entities' dependence on imported labour. Comprehensive training programmes create regional technical expertise applicable to multiple mining operations and related industries.

Research and development collaboration in mining technologies creates innovation opportunities while addressing region-specific operational challenges. Joint research programmes enable technology adaptation to local geological conditions while developing intellectual property with potential commercial applications.

Regional Coordination and Bargaining Power

Multi-country negotiation frameworks enable regional governments to coordinate investment terms and requirements, potentially improving bargaining positions with Chinese entities seeking regional presence. Coordinated approaches prevent competitive underbidding between countries while ensuring consistent standards.

Shared infrastructure development reduces individual country costs while creating regional integration benefits. Coordinated transportation networks, processing facilities, and port infrastructure enable operational efficiencies while distributing development costs across multiple beneficiary countries.

Environmental and social standard harmonisation across borders creates consistent operational requirements while preventing regulatory arbitrage. Common standards enable operational coordination while ensuring environmental protection and community benefit standards apply consistently throughout regions.

This analysis is based on publicly available information and market research. Investment decisions should consider additional factors including regulatory changes, market conditions, and individual risk tolerance. Cryptocurrency and mining investments carry inherent risks including total loss of capital.

Ready to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why historic discoveries can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.